Quick Navigation

Report Overview

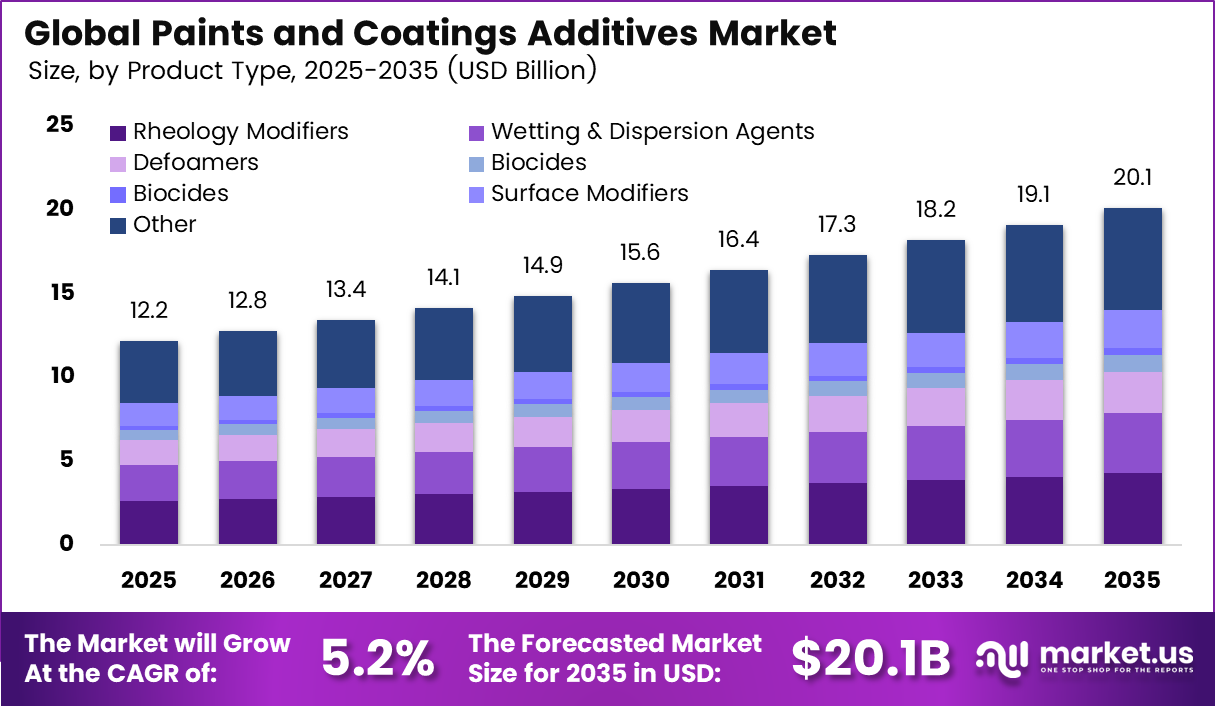

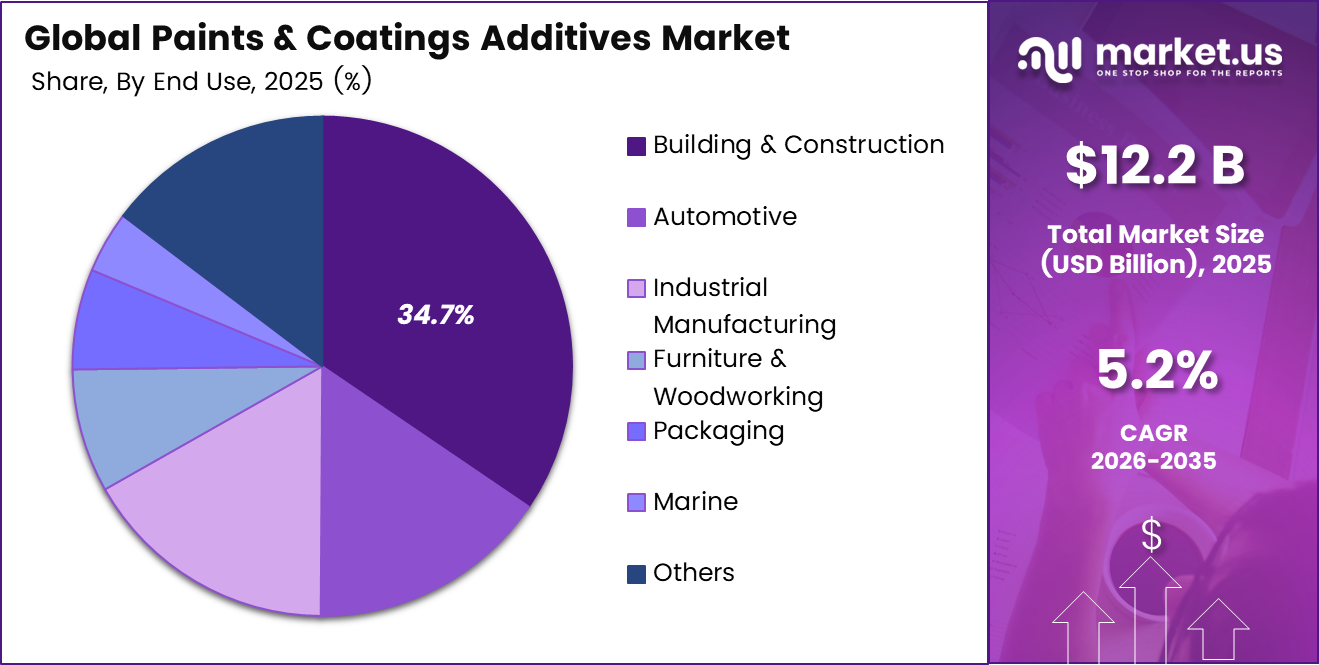

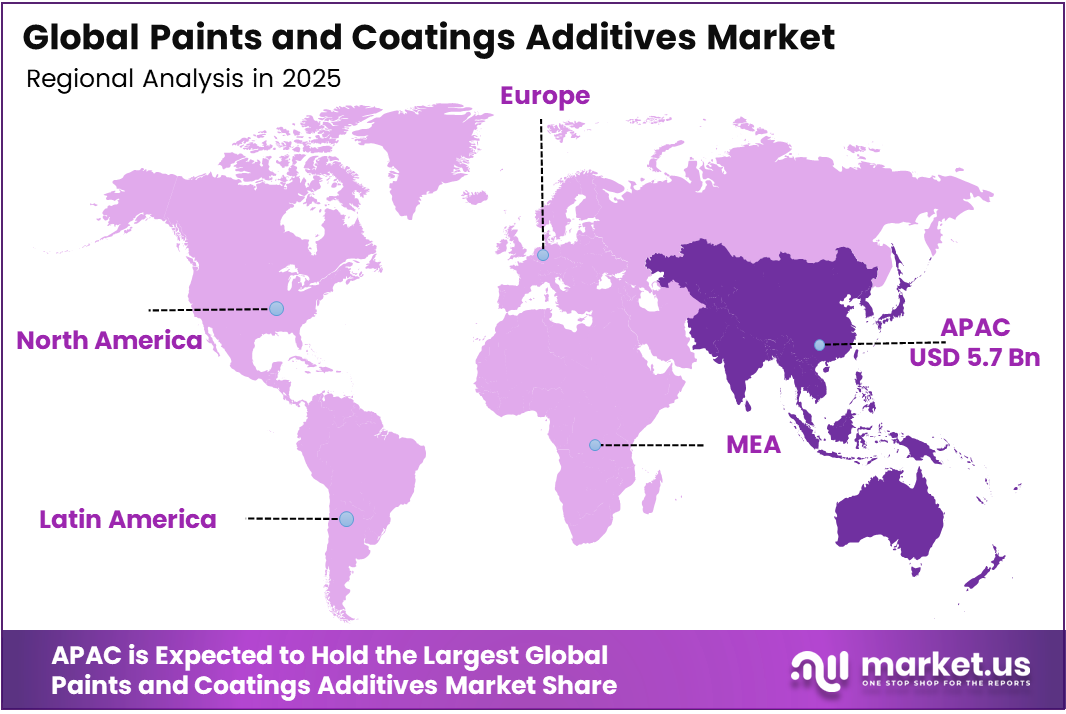

The Global Paints and Additives for Coatings Market size is expected to be worth around USD 12.2 Billion by 2025, growing at a CAGR of 5.2% during the forecast period from 2026 to 2035, reaching USD 20.1 Billion by 2035. Asia Pacific held a dominant market position, capturing more than a 46.5% share, holding USD 5.7 Billion in revenue.

Paints and coatings additives are specialty chemicals added in precise quantities to improve flow, adhesion, durability, UV protection, microbial resistance, and surface performance. These products include rheology modifiers, wetting and dispersing agents, defoamers, UV stabilizers, biocides, and surface additives. Demand is supported by expanding construction activity in Asia Pacific and the Middle East, advanced automotive coating technologies, and the shift toward low-VOC, water-based formulations.

Regulatory and performance requirements are increasing additive consumption across major coating applications. The European Chemicals Agency reportedly indicated that approximately 35% of professional coating formulations in Europe required reformulation to comply with revised REACH and VOC requirements.

Waterborne systems generally need larger quantities of rheology modifiers, wetting agents, dispersants, and defoamers to achieve solvent-borne performance, with rheology modifiers accounting for 43.2% of additive revenues in waterborne coatings. India’s Ministry of Housing and Urban Affairs also allocated US$1.54 billion to urban housing under PM Awas Yojana Urban 2.0, supporting demand for architectural coatings and related additives.

Raw-material volatility and sustainability requirements continue to influence supplier strategies. BASF faced an estimated 23% increase in acrylic acid feedstock prices during H1 2024, contributing to a reported 1.8% reduction in EBITDA margin. AkzoNobel recorded a 34% year-on-year rise in European procurement enquiries for sustainable coating additives, which were priced approximately 18% above conventional alternatives. Clariant also reported that customers using its AI-assisted formulation platform reduced waterborne coating qualification timelines by an average of 40%, helping manufacturers accelerate product development in Europe and North America.

Key Takeaways

- In 2025, the global market for paints and coatings additives was projected to be worth over US$ 12.2 billion.

- By 2035, the global market for paints and coatings additives is expected to reach a size of US$ 20.1 billion.

- The market is anticipated to grow at a compound annual growth rate (CAGR) of 5.2% between 2026 and 2035.

- In the case of Rheology Modifiers, the product type segment’s market share was 21.3%.

- Building & Construction held the largest share (34.5%) in the end-use industry segment.

- As far as the second-largest end-use segment is concerned, Industrial Manufacturing was ranked second with a market share of 16.7%.

- The wetting & dispersion agent product type segment holds a market share of 17.8% owing to increasing requirements for improved pigment dispersion in water-based and high-end coating applications.

- The Asia Pacific region dominates the Paints and Coating Additives market with a market share of 46.5% owing to large-scale production of coatings in China, growing construction industry in India, and fast-paced industrialization in Southeast Asia.

Product Type Analysis

Rheology Modifiers Lead the Market Owing to Universal Formulation Compatibility

Rheology modifiers dominate the product type segment, accounting for 21.3% of total revenue. Their leading position stems from their critical function in controlling viscosity, flow, levelling, and sag resistance across both waterborne and solvent-borne coating systems. They are specified by formulators in every coating category from architectural emulsions to industrial maintenance coatings, making their procurement non-discretionary.

The breadth of rheology modifier product families (HASE, HEUR, cellulosics, clay-based, polyurea) enables formulators to meet an exceptionally wide range of application and performance requirements across regions and end-use industries. Customers’ demand for cellulose rheology modifiers was estimated to be 640,000 tons in 2024, with 42% of that demand coming from the Asia-Pacific area. This shows the size of customer raw purchases that support this category’s dominance in the market.

The Wetting & Dispersion Agents product type enjoys a share of 17.8% and constitutes the fastest-growing product type due to increasing consumption of nanoparticle pigments and ultra-fine extenders in premium water-based coatings that need excellent pigment stabilization and colour development capability.

The growth in this product category is being further fueled by the global shift in the coating industry from solvent-borne to waterborne coatings, where matching the level of pigment dispersion in solvent-borne coating systems needs much more complex additives. Defoamers have a share of 12.3%, while Surface Modifiers and UV Stabilizers follow at 11.2% and 10.8%, respectively.

End-Use Industry Analysis

Building & construction accounts for the largest end-use share at 34.5%, due to sustained urbanization trends across Asia Pacific, the Middle East, and Latin America, combined with renovation activity in mature North American and European markets. To satisfy durability, aesthetic, and legal requirements, architectural coatings, such as wood finishes, outside façade coatings, and interior wall paints, need a wide range of additives, such as rheology modifiers, biocides, and UV stabilizers.

Industrial Manufacturing ranks second with a 16.7% share, driven by growing demand for high-performance protective coatings across metal fabrication, heavy machinery, electronics, and consumer appliance manufacturing — particularly across expanding Asia Pacific manufacturing hubs requiring advanced corrosion resistance and adhesion additive systems.

Automotive follows at 15.6% as the fastest-growing end-use segment, driven by OEM lightweighting trends, rising electric vehicle production, and increasingly stringent exterior durability and scratch resistance coating specifications requiring premium additive formulations. Consumer Goods (9.8%), Furniture & Woodworking (8.0%), Packaging (6.5%), Marine (4.0%), and Aerospace & Defence (3.4%) complete the remaining end-use architecture.

Key Market Segments

By Product Type

- Rheology Modifiers

- Wetting & Dispersion Agents

- Defoamers

- Biocides

- Impact Modifiers

- Surface Modifiers

- Adhesion Promoters

- UV Stabilizers

- Anti-foaming Agents

- Thickening Agents

- Others

By End-Use Industry

- Building & Construction

- Automotive

- Industrial Manufacturing

- Furniture & Woodworking

- Packaging

- Marine

- Aerospace & Defense

- Consumer Goods

- Others

Market Dynamics

Challenge

PFAS & SVHC Regulatory Cascade

PFAS and SVHC regulations are becoming a major compliance challenge for coatings additive manufacturers. The ECHA RAC adopted its opinion on the EU PFAS restriction in March 2026, with the SEAC final opinion expected by end-2026 and final regulation likely in 2027-2028. The REACH Candidate List reached 253 SVHCs in February 2026, adding 2 new substances, Bisphenol AF (BPAF) and n-Hexane.

The proposed EU restriction covers more than 10,000 PFAS substances, including fluorinated surfactants, waxes, binders, fluoroacrylates, and fluorourethane oligomers used at below 0.5% w/w. Manufacturers must complete a 5-7 step substitution process involving TF and EOF testing, LC-MS/MS analysis of 80-100 PFAS species, and reformulation with silicon-, acrylate-, or sol-gel-based alternatives that currently deliver 15-25% lower performance in contact angle, chemical resistance, and UV weathering.

In the US, California, Vermont, Illinois, Oregon, and Minnesota introduced PFAS restrictions during 2025-2026, while Vermont will tighten the limit to 50 ppm total organic fluorine by July 2027. The CMR Annex XVII update also added 22 new carcinogenic, mutagenic, or reprotoxic substances, requiring 18-36 month reformulation cycles and multi-million-dollar R&D investments, increasing compliance costs and pressuring near-term margins.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| PFAS & SVHC Regulatory Cascade | -1.2% | EU regulatory hubs, North America state-level, APAC export corridors | Long term (≥ 4 years) |

| Feedstock Volatility & TiO₂ Price Instability | -1.0% | Global; acute in North America, EU import markets | Medium term (2–4 years) |

| Geopolitical Freight & Logistics Friction | -0.8% | Asia-Europe corridors, Red Sea/Suez-dependent lanes, APAC logistics hubs | Medium term (2–4 years) |

| Formulation Scientist & STEM Talent Deficit | -0.9% | EU (DACH, Benelux), North America, UK; nascent in South/Southeast Asia | Long term (≥ 4 years) |

| Bio-based Additive Performance Gap | -0.7% | EU Green Deal mandated markets; North America eco-label segments | Medium term (2–4 years) |

| China Overcapacity & Margin Compression | -0.6% | Global commodity-grade additive markets; APAC, Middle East, South Asia | Long term (≥ 4 years) |

Opportunity

AI-Powered Digital Formulation Platforms as a Monetizable SaaS Layer

The paints and coatings additives sector is shifting from transactional product sales to AI-enabled formulation intelligence platforms, driven by predictive formulation tools, defect diagnosis, and data-driven additive selection systems. Despite growing adoption, most current platforms (e.g., COATINO and ClariCoat) are still offered as free customer-retention tools, with no major additive supplier monetizing formulation intelligence as a standalone SaaS product.

The opportunity lies in converting proprietary lab datasets (over 10,000+ formulation trials and 500+ defect cases) into a paid formulation-intelligence-as-a-service model. A SaaS pricing structure of USD 50,000–250,000 per enterprise client per year could realistically attract 200–400 customers over 5 years, generating USD 20–100 million in recurring revenue at >70% gross margins, independent of raw material cycles.

This model is further strengthened by regulatory digitalization, including the EU Product Environmental Footprint (PEF) framework and Digital Product Passports (DPP) rolling out between 2026–2030, which will require structured digital traceability of formulation and additive inputs, creating a compliance-driven adoption pathway for AI formulation platforms.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Smart & Self-Healing Additive Systems for Industrial & Automotive OEM | +2.8% | North America, EU, APAC (Japan, South Korea) | Medium term (2–4 years) |

| Bio-Based & Carbon-Compliant Additive Platforms under EU CBAM & Green Deal | +1.8% | EU core, UK, North America | Short term (≤ 2 years) |

| India & South/Southeast Asia Infrastructure-Driven Protective Additive TAM | +1.5% | India, Vietnam, Indonesia, Bangladesh | Short-to-Medium term (1–3 years) |

| AI-Powered Digital Formulation Platforms as a Monetizable SaaS/Outcome Layer | +1.2% | North America, EU, APAC | Medium term (2–4 years) |

| Renewable Energy Sector (Wind, Solar) Functional Additive Specialization | +1.0% | EU, North America, China, India | Medium term (2–4 years) |

| Specialty Antimicrobial & Antifouling Additive Roll-Up via M&A | +0.8% | North America, EU, APAC | Long term (≥ 4 years) |

Driver

Bio-based & Sustainable Additive Innovation — Substituting Petroleum-Derived Chemistries

Sustainability regulations and disclosure frameworks, including the EU Green Deal and CSRD requirements, are driving a structural shift from petroleum-based to bio-based and mass-balance-certified additives in paints and coatings. This transition is already commercialized at scale, with multiple tier-one launches: Arkema introduced Rheotech and Thixol bio-based thickeners, Evonik launched TEGO Wet 270 eCO and TEGO Foamex 812 eCO certified under ISCC PLUS, and earlier introduced TEGO Wet 570 Terra and TEGO Wet 580 Terra bio-surfactants for coatings and inks.

Bio-based and mass-balance-certified additives typically command a 20–40% price premium over petrochemical equivalents, improving revenue intensity while enabling downstream paint manufacturers to achieve certifications such as EU Ecolabel and Nordic Swan, which unlock regulated procurement in public infrastructure projects.

The EU Biocidal Products Regulation (BPR) review process, with stakeholder consultation through March 2026 and revised legislation targeted for Q1 2027, further accelerates reformulation toward bio-compatible preservatives, with full active substance review extended to December 2030. However, bio-based production routes still carry 30–50% higher raw material costs, limiting near-term adoption in price-sensitive Asian markets, where uptake typically lags Europe by 3–5 years due to weaker regulatory pull and cost sensitivity.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| VOC Regulatory Mandates driving waterborne additive reformulation | +1.8% | EU core, North America, China (GB standards), India (BIS/CPCB) | Short term (≤ 2 years) |

| Residential & Infrastructure Construction Boom lifting decorative & protective coating volumes | +1.5% | India (PMAY-U/G), APAC corridors, Middle East spill-over, North America | Medium term (2–4 years) |

| EV & Automotive OEM Expansion creating demand for lightweight, functional, and e-coat additives | +1.2% | APAC (China, India), EU, North America | Medium term (2–4 years) |

| Bio-based & Sustainable Additive Innovation substituting petroleum-derived chemistries | +0.9% | EU green mandate core, North America, Australia; APAC adoption lag | Long term (≥ 4 years) |

| Anti-Corrosion & Smart Functional Additives for energy, marine, and industrial protection | +1.0% | Middle East, North America upstream O&G, India NIP infra, EU offshore | Medium term (2–4 years) |

| High-Performance UV/Powder-Cure Additive Systems for zero-VOC industrial applications | +0.7% | North America, EU, South Korea, Japan; India emerging | Long term (≥ 4 years) |

Restraint

Raw Material Cost Inflation — TiO₂, Propylene Oxide & Resin Volatility

The paints and coatings additives market is facing sustained input cost pressure from disruptions across key raw material chains, particularly titanium dioxide (TiO₂), propylene oxide, and acrylic resin feedstocks. TiO₂ prices ranged between USD 2,000–2,900/ton in June 2025, rising to USD 2,900–3,500/ton (CIF US imports) due to Red Sea shipping disruptions that increased freight costs by 12–18% year-on-year. At the same time, ilmenite and rutile ore shortages pushed feedstock costs to USD 250–350/ton, while capacity cuts by major producers including Chemours, Tronox, and Venator removed significant global supply, creating a structural imbalance.

On the resin side, propylene oxide prices rebounded 12.4%, rising from USD 1.005/kg to USD 1.13/kg after a prior 23% decline, reflecting restocking volatility rather than true demand recovery. This feeds into acrylic resin volatility in downstream coatings systems, where feedstock fluctuations in propylene and acrylic acid are driving 200–400 basis points of margin compression in waterborne additive grades.

For small and mid-sized additive manufacturers lacking hedging capability, this environment compresses EBITDA margins toward breakeven, delays new product launches due to procurement uncertainty, and forces frequent 60–90 day price renegotiations with OEM customers, structurally limiting short- to medium-term volume growth.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material Price Volatility (TiO₂, Acrylic Resins, Propylene Oxide) | −1.4% | Global; APAC, North America core, EU manufacturing corridors | Short term (≤ 2 years) |

| REACH/SVHC & PFAS Regulatory Tightening | −1.1% | EU core, EEA, with secondary spillover to UK, APAC export-facing producers | Medium term (2–4 years) |

| US Tariff Disruptions on Specialty Chemicals & Intermediates | −0.9% | North America, China-to-US supply corridors, India export routes | Short term (≤ 2 years) |

| PFAS Phase-Out & High-Performance Additive Reformulation Costs | −0.8% | EU core, North America; fluoropolymer-dependent industrial/OEM sectors | Medium term (2–4 years) |

| Weak End-Market Demand (Construction Softness & Industrial Slowdown) | −0.7% | EU, North America; China residential construction corridor | Short-to-Medium term (1–3 years) |

| Skilled Technical Workforce Deficit in Specialty Formulation R&D | −0.5% | Europe, North America; moderate pressure in India and APAC emerging markets | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Geopolitical Tensions and Supply Chain Disruptions Increasing Raw Material and Production Costs

Geopolitical concerns emerge as a leading structural risk affecting the paints and coatings additives market. As most additives are produced using petrochemical feedstocks, the manufacturing costs of these products are highly exposed to geopolitical risks and crude oil prices. In this regard, the heightened tension between the United States, Israel, and Iran since late February 2026 affected the energy sector and trade routes in the Middle East region; thus, Brent crude prices rose sharply to USD 80-120 per barrel by early March 2026.

As 40-60% of the total manufacturing costs of paints result from petroleum-based ingredients such as resins, solvents, and additives, these developments have increased manufacturing costs for additive and coatings manufacturers around the globe. The imposition of additional US tariffs in 2025 added a further layer of complexity to the manufacturing process through increased costs and sourcing issues; therefore, producers were forced to reconsider procurement practices, develop local manufacturing capacity, and engage in vertical integration as well as other supply chain strategies.

The tightening of regulations in Europe and Asia-Pacific accelerated the shift towards bio-based and low toxicity additives. For instance, during Q1 2026, Evonik Industries AG reported that disruption in energy markets in the Middle East along with higher crude oil prices resulted in an average of 15% rise in the cost of raw materials in the coating additives product line, necessitating customer price discussions and rapid substitution of feedstock by bio-based products wherever possible.

Regional Analysis

Asia Pacific Leads Global Demand While North America and Europe Advance Sustainable Additive Technologies

The Asia Pacific region leads the worldwide Paints and Coatings Additives market with a revenue share of 46.5% worth approximately US$ 5.7 billion in 2025. China holds the leading country share within the region, attributed to being the world’s largest coatings producer, attributed to being the biggest coatings producer in the world, whereas India is growing the fastest due to investments in infrastructure, housing, and smart cities through 2030.

For instance, in the case of Asian Paints, in 2024, there was a 22% growth in the purchase of specialty coatings additives from year to year owing to increased building activity in the residential sector and increased activity in infrastructural projects in India’s Tier 2 and Tier 3 cities, with water-based architectural coating additives being the highest consumed additive.

North America has the second-largest market position, marked by very strict EPA and CARB VOC norms, which are pushing up the use of premium waterborne additives, infrastructure upgrade initiatives, and automotive OEM coating industry leadership.

Europe has the highest standards of REACH and sustainability, which have made its market for specialty additives highly lucrative. Latin America is growing due to increased construction activities and the revival of the automotive industry in Brazil, whereas the Middle East & Africa region is growing due to massive GCC petrochemical-funded projects in the region until 2035.

Key Regions and Countries Covered in this Report

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of Middle East & Africa

Key Players Analysis

Paints and Coatings Additives industry rivalry is driven by sustainable innovation in formulations, diversity of additives, and technical services offered to coating formulators around the world. The industry is somewhat concentrated, with market leadership going to companies such as Dow, BASF SE, Altana Group (BYK), Evonik Industries AG, and Elementis PLC, who compete using their unique chemical platforms and strong relationships with their customers in terms of formulations.

Important aspects of competition include certification for biodegradable additives, compliance with REACH/EPA regulations, and offering all types of additives. Companies are exploring options for diversification of suppliers and changes in inventory management practices amid the instability of tariffs and regional regulations.

Market Key Players

- AGC Inc.

- ALTANA AG (BYK)

- Arkema S.A.

- Ashland Inc.

- BASF SE

- Cabot Corporation

- DAIKIN INDUSTRIES, Ltd.

- Dow Inc.

- Dynea AS

- ELEMENTIS PLC

- Evonik Industries AG

- K-TECH (INDIA) LIMITED

- Momentive Performance Materials Inc.

- Nouryon

- Solvay S.A.

- The Lubrizol Corporation

- Other Key Players

Key Development

- In February 2026, Eastman Chemical Company developed specialty additives for coatings improving scratch resistance, gloss retention, and sustainability across waterborne and solventborne systems for architectural and industrial applications. This development strengthens Eastman’s positioning among premium coating additive buyers seeking high-durability, low-VOC-compatible additive solutions across North American and European markets.

- In March 2026, Dow Inc. expanded its paint additives portfolio with innovative rheology modifiers and dispersants enhancing durability and application performance across architectural and industrial coating formulations. These additions strengthen Dow’s ability to serve coating manufacturers transitioning from solventborne to waterborne systems requiring advanced rheology and dispersion performance.

- In May 2026, Evonik Industries AG implemented a streamlined North American distribution network for its coating additives line, appointing Andicor Specialty Chemicals as exclusive Canadian distributor and establishing new regional distributor partnerships across the United States. This restructured commercial infrastructure enhances Evonik’s market coverage and order fulfillment responsiveness across the region’s expanding architectural and industrial coatings manufacturing base.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 12.2 Billion |

| Forecast Revenue (2035) | USD 20.1 Billion |

| CAGR (2026-2035) | 5.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Rheology Modifiers, Wetting & Dispersion Agents, Defoamers, Biocides, Impact Modifiers, Surface Modifiers, Adhesion Promoters, UV Stabilizers, Anti-foaming Agents, Thickening Agents, Others), By End-use Industry (Building & Construction, Automotive, Industrial Manufacturing, Furniture & Woodworking, Packaging, Marine, Aerospace & Defence, Consumer Goods, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC – China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America – Brazil, Mexico & Rest of Latin America; Middle East & Africa – GCC, South Africa & Rest of MEA |

| Competitive Landscape | AGC Inc., ALTANA AG (BYK), Arkema S.A., Ashland Inc., BASF SE, Cabot Corporation, DAIKIN Industries Ltd., Dow Inc., Dynea AS, ELEMENTIS PLC, Evonik Industries AG, K-TECH (India) Limited, Momentive Performance Materials Inc., Nouryon, Solvay S.A., The Lubrizol Corporation, other players. |

| Customization Scope | Customization for segments and region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |