Quick Navigation

Report Overview

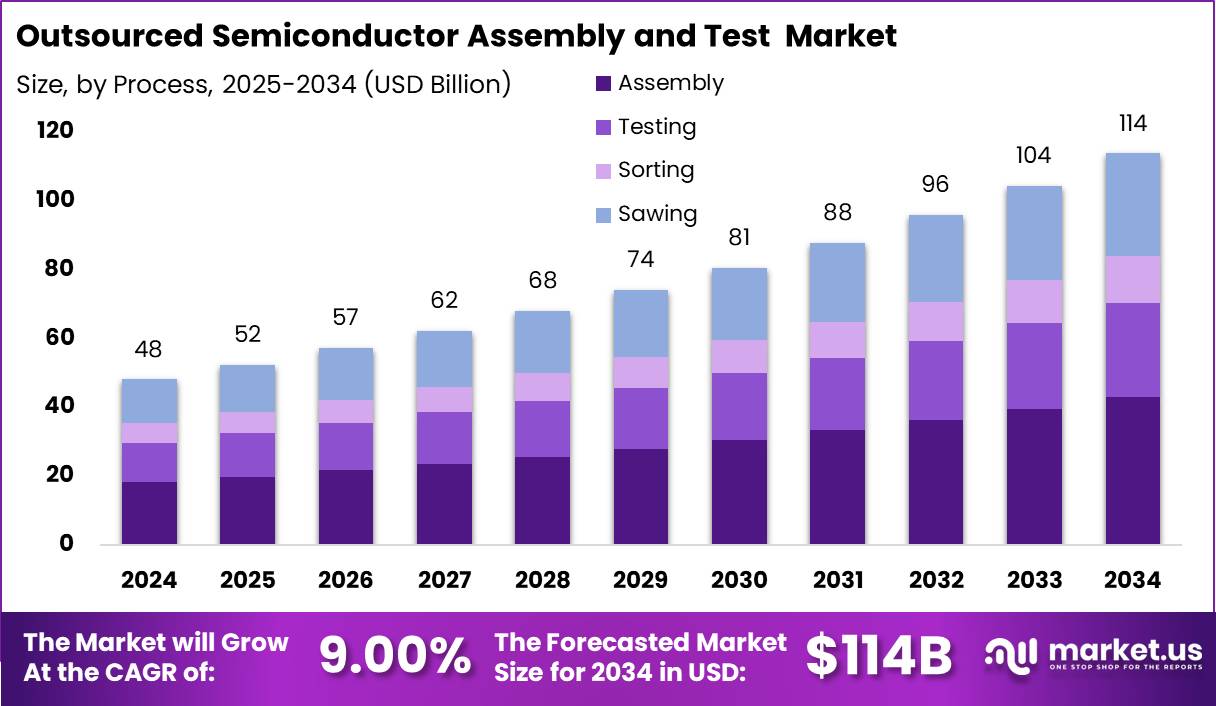

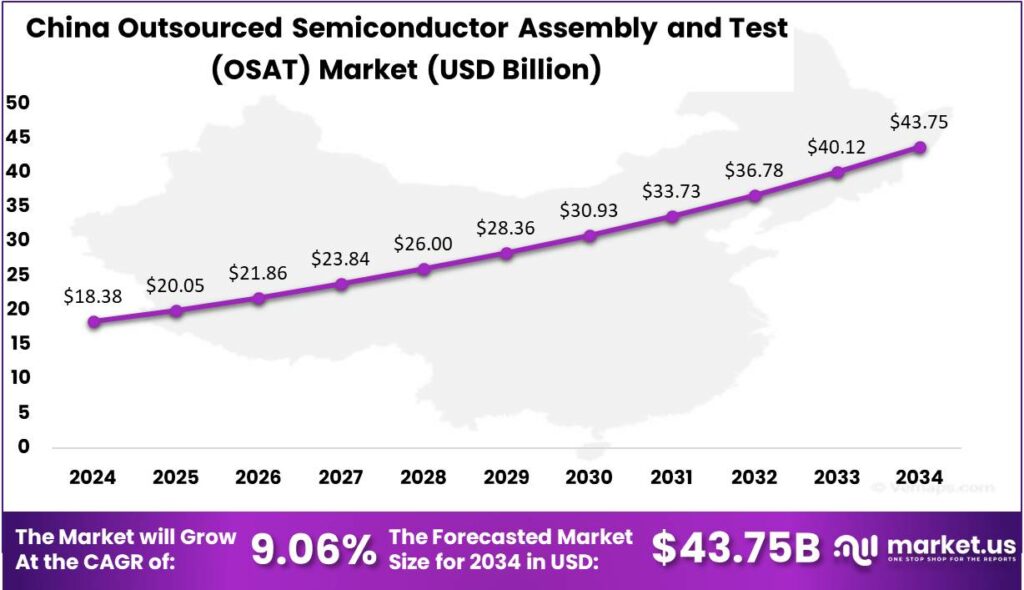

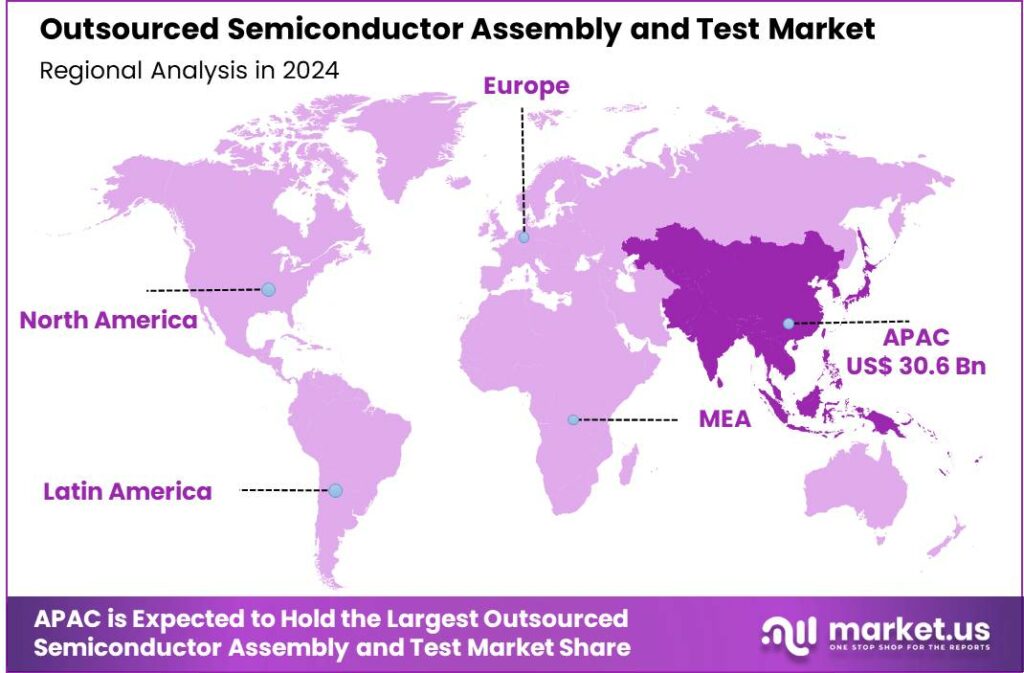

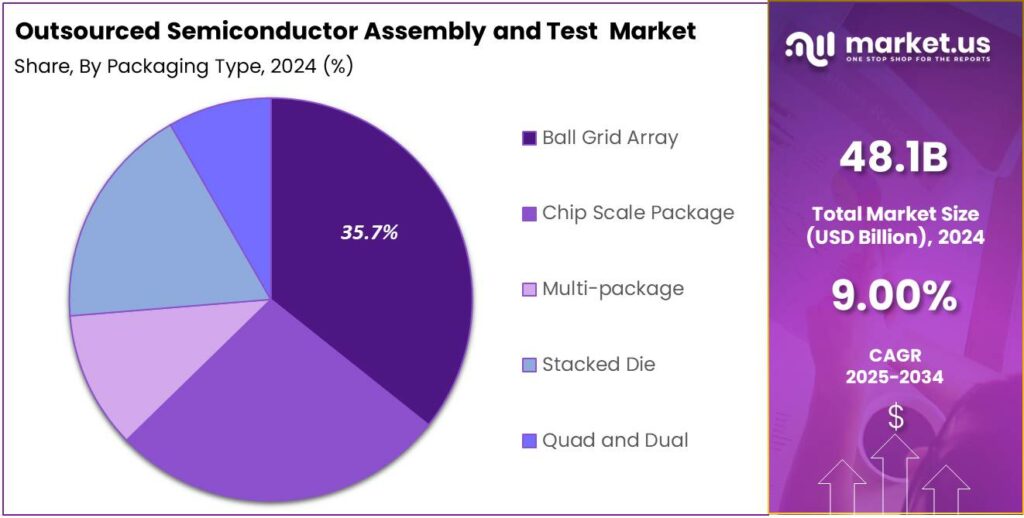

The Global Outsourced Semiconductor Assembly and Test Market size is expected to be worth around USD 114 Billion By 2034, from USD 48.1 Billion in 2024, growing at a CAGR of 9.00% during the forecast period from 2025 to 2034. In 2024, the Asia-Pacific region dominated the OSAT market with over 63.7% share, generating USD 30.6 billion in revenue. China’s OSAT market, valued at USD 18.38 billion, is projected to grow at a CAGR of 9.06%.

Outsourced Semiconductor Assembly and Test (OSAT) refers to the practice where semiconductor companies outsource the assembly, packaging, and testing aspects of their manufacturing process to third-party service providers. This model lets semiconductor firms focus on design and wafer fabrication while relying on OSAT providers for specialized expertise, boosting efficiency, reducing costs, and speeding up time-to-market.

The growth of the OSAT market is fueled by the increasing complexity of semiconductor designs, which require advanced assembly and testing technologies beyond in-house capabilities. Additionally, the rapid evolution of technology in sectors like mobile devices, automotive electronics, and IoT demands faster innovation cycles, which OSAT companies are well-equipped to manage.

The growing demand for semiconductor devices has increased reliance on OSAT providers to scale production without requiring significant investments in new facilities. This trend is further driven by the global shift towards advanced packaging solutions that deliver better performance in smaller form factors.

The OSAT market’s popularity stems from its cost-efficiency and specialization. Semiconductor companies can adjust production capacity and technology without the overhead of maintaining packaging and testing facilities. This outsourcing speeds up time-to-market for new technologies, giving companies a competitive edge.

According to research conducted by Market.us, the semiconductor market is projected to grow from $530 bn in 2023 to approximately $996 bn by 2033, reflecting a CAGR of 6.5% during the forecast period from 2024 to 2033. In 2023, the Asia-Pacific (APAC) region held a dominant position, capturing more than 63.91% of the market share, equating to revenues of about $388.7 billion.

The Semiconductor Industry Association reports that approximately 31% of all semiconductors manufactured are utilized for communications applications, including networking equipment and smartphone radios. This underscores the critical role of Outsourced Semiconductor Assembly and Test (OSAT) services in the industry.

In July 2023, Taiwan Semiconductor Manufacturing Company (TSMC) announced a significant investment of around $2.89 billion to establish an advanced chip packaging plant in Miaoli, northern Taiwan, with volume production expected to commence by mid-2027.

The expansion of the OSAT market is anticipated to continue as the global demand for more sophisticated electronics grows. The shift towards electric vehicles, renewable energy, and smarter electronics will drive ongoing demand for advanced semiconductor assembly and testing services, showcasing the market’s vitality and adaptability to emerging technologies.

Key Takeaways

- The Global Outsourced Semiconductor Assembly and Test (OSAT) Market size is projected to reach USD 114 billion by 2034, growing from USD 48.1 billion in 2024, at a CAGR of 9.00% during the forecast period from 2025 to 2034.

- In 2024, the Assembly segment held a dominant position in the OSAT market, capturing more than a 37.8% share.

- The Ball Grid Array (BGA) segment in 2024 also held a leading position, accounting for over 35.7% share of the OSAT market.

- The Consumer Electronics segment dominated the OSAT market in 2024, capturing more than a 41.5% share.

- In 2024, the Asia-Pacific region held a commanding position in the OSAT market, accounting for more than 63.7% share, with revenues reaching USD 30.6 billion.

- The OSAT market in China was valued at USD 18.38 billion in 2024, and it is projected to grow at a CAGR of 9.06%.

China Market Size

In 2024, the market for Outsourced Semiconductor Assembly and Test (OSAT) in China was valued at USD 18.38 billion. This market is projected to grow at a compound annual growth rate (CAGR) of 9.06%. The sector’s growth is driven by rising demand for consumer electronics and the expansion of 5G and IoT technologies.

The OSAT market is crucial for the semiconductor industry as it involves the provision of third-party IC-packaging and testing services, which are vital for the functionality and performance of semiconductors. The rise of telecommunications infrastructure and automotive electronics in China has significantly contributed to the expansion of this market.

Another key driver for the growth of the OSAT market in China is the global shift in semiconductor supply chains. To mitigate supply chain risks, companies are diversifying operations, making China a key hub for semiconductor assembly and testing due to its infrastructure and skilled workforce. This shift ensures continued market growth driven by domestic and international demand.

In 2024, the Asia-Pacific region held a dominant position in the Outsourced Semiconductor Assembly and Test (OSAT) market, capturing more than a 63.7% share with revenues reaching USD 30.6 billion. Asia-Pacific’s substantial market share in semiconductor assembly and testing is driven by several key factors, positioning it as an industry leader.

The region’s success is driven by leading semiconductor manufacturing countries like Taiwan, South Korea, and China, which have advanced capabilities and strong government support. The integration of production with assembly and testing services enhances efficiency and lowers logistical costs.

Additionally, the increasing demand for consumer electronics, automobiles, and communication devices in Asia-Pacific countries has spurred further development in the OSAT sector. The region’s massive consumer base and its rapidly expanding middle class have led to increased consumption of technology products that rely on semiconductors.

Strategic partnerships and R&D investments have enhanced the technological capabilities of OSAT providers in the region. The adoption of advanced technologies like 3D packaging and silicon photonics strengthens the competitive edge of the Asia-Pacific OSAT market, attracting global semiconductor companies in need of cutting-edge assembly and testing services.

Analysts’ Viewpoint

The investment landscape in the OSAT sector is robust, with opportunities driven by the need for advanced packaging solutions and increased manufacturing capacity to meet the growing demands of high-tech industries. Regulatory factors also play a crucial role, especially in regions like the EU and the US, where safety and environmental regulations are prompting automotive manufacturers to incorporate more advanced semiconductor technologies in vehicles.

Recent advancements include the development of copper pillar flip-chip technologies, enhanced wafer-level packaging, and improved test methodologies that cater to the high-frequency requirements of modern wireless devices. Such innovations not only enhance the performance and reliability of semiconductors but also drive the OSAT market’s growth by meeting the increasingly stringent standards of various end-user industries.

The regulatory environment for the OSAT market is largely influenced by global semiconductor policies, trade agreements, and intellectual property laws, which impact the operations and strategic decisions of OSAT providers. Regulations regarding electronic waste, as well as standards for product safety and quality, also play a crucial role in shaping the market dynamics.

Process Analysis

In 2024, the Assembly segment held a dominant position in the Outsourced Semiconductor Assembly and Test (OSAT) market, capturing more than a 37.8% share. This leadership can be attributed to several factors that underscore the critical role of assembly in semiconductor production.

Assembly involves integrating silicon wafers and semiconductor materials into final products, making it crucial for turning technological advancements into market-ready devices. As semiconductor devices become more complex and demand for compact, efficient packaging grows, sophisticated assembly techniques often handled by specialized OSAT providers are increasingly important.

The Assembly segment is strengthened by advanced packaging technologies like System in Package (SiP) and 3D integrated circuits, which require precise assembly to integrate multiple functions into compact units. This trend, driven by demand for higher performance and miniaturization, is prominent in consumer electronics, automotive, and industrial sectors.

The push for faster time-to-market drives semiconductor companies to optimize production cycles. The Assembly segment plays a key role by ensuring quicker transitions from chip fabrication to market-ready devices. OSAT providers in this sector offer rapid turnaround times, helping semiconductor firms stay competitive in fast-paced markets like consumer electronics and mobile devices.

Packaging Type Analysis

In 2024, the Ball Grid Array (BGA) segment held a dominant position in the Outsourced Semiconductor Assembly and Test (OSAT) market, capturing more than a 35.7% share. The popularity of BGA packaging is primarily due to its ability to provide more interconnection pins than can be achieved with other packaging types.

BGAs use the underside of the package for connections, which allows for a dense grid of pins to be spread out over the entire bottom surface of the chip. This configuration supports higher levels of performance and is particularly suited to applications requiring high-speed signal transmission, making it indispensable in high-performance computing and telecommunications sectors.

The Chip Scale Package (CSP) segment is vital in the OSAT market due to its compact size, reducing the package footprint on circuit boards. This is essential for space-constrained devices like smartphones and tablets. CSPs improve device thinness, weight, and thermal and electrical performance, boosting their adoption across various applications.

The Multi-package segment, which involves integrating multiple semiconductor dies into a single package, is gaining traction due to its ability to provide enhanced functionality while saving space. This packaging type is becoming popular in devices that require a combination of diverse technologies, such as mixed-signal applications or multi-chip modules.

Application Analysis

In 2024, the Consumer Electronics segment held a dominant market position within the Outsourced Semiconductor Assembly and Test (OSAT) market, capturing more than a 41.5% share. This segment’s leadership is largely driven by the relentless demand for consumer electronics products such as smartphones, tablets, wearable devices, and other smart technologies that are integral to daily life.

The rise in consumer electronics is driven by technological advancements and the global adoption of smart devices. As devices become more complex, they require advanced semiconductor components. OSAT providers are crucial in efficiently assembling and testing these components, ensuring the mass production of reliable consumer electronics.

The consumer electronics market’s short product life cycles and rapid innovation demand quick turnaround times and flexible supply chains. OSAT companies meet these needs with scalable, agile testing and assembly services, making them essential for manufacturers aiming to capitalize on emerging trends.

The growth of the Internet of Things (IoT) and the integration of connectivity features into consumer devices has expanded the OSAT market in consumer electronics. As devices become more compact, the demand for high-performance, miniaturized semiconductor packages increases, driving the need for advanced OSAT solutions.

Key Market Segments

By Process

- Sawing

- Sorting

- Testing

- Assembly

By Packaging Type

- Ball Grid Array

- Chip Scale Package

- Multi-package

- Stacked Die

- Quad and Dual

By Application

- Automotive

- Consumer Electronics

- Industrial

- Telecommunication

- Aerospace and Defense

- Medical and Healthcare

- Logistics and Transportation

- Others

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Technological Advancements in Packaging Solutions

The OSAT industry has experienced significant growth due to continuous advancements in packaging technologies. Innovations such as fan-out wafer-level packaging (FO-WLP), wafer-level chip-scale packaging, flip chip, 2.5D and 3D packaging, system-in-package (SiP), and copper wire bonding have been pivotal.

These technologies allow for the creation of smaller, more efficient, and higher-performing semiconductors, meeting the growing demand for compact, powerful electronics. For instance, FO-WLP facilitates ultra-thin, high-density packages, catering to the market’s need for thinner mobile devices. SiP technology integrates multiple integrated circuits within a single package, supporting the functionality of wearables, mobile devices, and IoT applications. The adoption of these advanced packaging solutions has positioned OSAT providers to meet evolving industry requirements effectively.

Restraint

Geopolitical Tensions and Supply Chain Vulnerabilities

The OSAT sector faces challenges stemming from geopolitical tensions and supply chain vulnerabilities. As local governments invest heavily in boosting domestic semiconductor capabilities, foreign OSAT providers may struggle to maintain their competitive edge, particularly in markets where local companies are receiving strong government support and subsidies.

The semiconductor industry, including OSAT providers, is under increasing pressure to reduce its carbon footprint and adopt sustainable practices. Companies like ASML and TSMC are emphasizing sustainability to maintain competitiveness, focusing on reducing waste through reuse and recycling, and securing renewable energy sources. However, accessing renewable energy remains a challenge in regions like Asia, impacting the industry’s ability to meet sustainability goals.

Opportunity

Expansion into Emerging Markets

The OSAT industry has the opportunity to expand into emerging markets, particularly in Southeast Asia. By investing in cutting-edge technologies like chiplet integration, System-in-Package (SiP) solutions, and advanced 3D packaging, OSAT providers can differentiate themselves in these high-growth markets, offering specialized services that cater to the evolving needs of industries like automotive, telecommunications, and consumer electronics.

Countries like Vietnam are attracting significant investments from tech giants such as Meta, which plans to manufacture its latest virtual reality headset in the country by 2025. Vietnam’s growing electronics production capabilities and large user base present a promising market for OSAT providers. By establishing operations in these emerging markets, OSAT companies can tap into new customer bases and benefit from favorable manufacturing conditions.

Challenge

Rapid Technological Advancements and Competition

The OSAT industry faces the challenge of keeping pace with rapid technological advancements and increasing competition. Companies must continuously innovate to meet the evolving demands of the semiconductor market, such as developing advanced packaging solutions for AI processors and other cutting-edge applications.

Additionally, competition from emerging players, particularly in regions like China, requires established OSAT providers to maintain their technological edge and adapt to changing market dynamics. Moreover, the increasing adoption of automation and artificial intelligence in the semiconductor assembly and testing processes is intensifying competition within the OSAT industry. Emerging players, particularly in regions like China, are investing heavily in these advanced technologies to improve efficiency and reduce costs.

Emerging Trends

The OSAT industry is evolving to meet semiconductor market demands, with advanced packaging technologies like System-in-Package (SiP) and 3D packaging gaining prominence. These innovations integrate multiple functions into a single chip, boosting performance and enabling device miniaturization.

Another notable development is the industry’s focus on sustainability and energy efficiency. OSAT providers are implementing eco-friendly practices, including the use of energy-efficient equipment and waste reduction strategies, to align with global environmental standards.

The automotive sector’s increasing demand for advanced driver-assistance systems (ADAS) is also influencing OSAT services. ADAS technologies require specialized semiconductor components, necessitating sophisticated packaging and testing solutions.

Furthermore, the rise of 5G networks is driving the need for semiconductors capable of supporting faster data transmission and enhanced connectivity. OSAT companies are developing advanced assembly and testing services to cater to 5G-enabled devices and infrastructure components.

Business Benefits

Engaging OSAT providers offers semiconductor companies several strategic advantages. It allows firms to focus on their core competencies, such as design and innovation, by outsourcing assembly and testing processes. This specialization can lead to accelerated technological advancements and product development.

OSAT services provide cost-effectiveness by eliminating the need for substantial capital investments in specialized assembly and testing facilities. This reduction in operational costs enables companies to allocate resources more efficiently.

OSAT providers offer scalability, allowing semiconductor companies to adjust production volumes in response to market demand without the constraints of in-house facility capacities. This flexibility is crucial in the rapidly changing semiconductor industry.

Additionally, OSAT firms often possess expertise in advanced packaging and testing technologies, ensuring high-quality and reliable semiconductor products. Access to such specialized knowledge can enhance product performance and competitiveness.

Key Player Analysis

ASE Technology Holding Co. Ltd is one of the largest and most prominent players in the OSAT market. Headquartered in Taiwan, ASE offers a broad range of assembly and testing services, from wafer-level packaging to advanced system-in-package (SiP) solutions. Their vast portfolio caters to various industries, including consumer electronics, automotive, and communications.

Amkor Technology Inc., another leader in the OSAT industry, is known for its innovative packaging solutions and extensive service offerings. With a presence in over 10 countries, Amkor serves a wide range of industries, from mobile devices to consumer electronics and automotive sectors.

Powertech Technology Inc. (PTI), based in Taiwan, is a well-established provider of semiconductor assembly and testing services, particularly known for its expertise in providing testing solutions for memory and logic devices. PTI’s advanced technologies and extensive testing capabilities make it a preferred partner for many leading semiconductor companies.

Top Key Players in the Market

- ASE Technology Holding Co. Ltd

- Amkor Technology Inc.

- Powertech Technology Inc.

- ChipMOS Technologies Inc.

- King Yuan Electronics Co. Ltd

- Formosa Advanced Technologies Co. Ltd

- Jiangsu Changjiang Electronics Technology Co. Ltd

- UTAC Holdings Ltd

- Lingsen Precision Industries Ltd

- Tongfu Microelectronics Co.

- Chipbond Technology Corporation

- Hana Micron Inc.

- Integrated Micro-electronics Inc.

- Tianshui Huatian Technology Co. Ltd

- Other Major Players

Top Opportunities Awaiting for Players

- Cost Efficiency and Specialization: As semiconductor companies continue to seek cost-effective solutions while focusing on core competencies like research and development, the demand for specialized OSAT providers is increasing. This trend allows OSAT companies to offer more competitive and advanced testing and packaging services.

- Expansion into Electric Vehicles (EVs): The automotive industry’s shift towards electric and autonomous vehicles is creating a surge in demand for semiconductors, which are critical for various functions from battery management to in-car electronics. OSAT providers have a significant opportunity to tailor their services for the high-performance requirements of this sector.

- Technological Advancements: Innovations such as 3D packaging, chiplet-based designs, and system-in-package (SiP) technologies are defining the future of semiconductor packaging. These technologies enable higher performance and integration, creating opportunities for OSAT providers to offer more advanced solutions.

- Geographic Expansion: The Asia-Pacific region remains a hotspot for OSAT providers due to the concentration of semiconductor manufacturing. Expanding or establishing partnerships in this region could provide strategic advantages, given the robust demand from local electronics sectors.

- Strategic Collaborations: There is a growing trend towards strategic partnerships and acquisitions in the OSAT market. These collaborations can help OSAT providers enhance their technological capabilities, expand their service offerings, and access new markets. This strategy is particularly crucial in maintaining competitive advantage and fostering innovation.

Recent Developments

- In December 2024, Amkor received up to $407 million in funding under the CHIPS Incentives Program to support its $2 billion investment in a new advanced packaging and test facility in Peoria, Arizona. This project aims to create over 2,000 jobs and enhance domestic semiconductor supply chain resilience.

- In August 2024, the Indian government unveiled an ambitious USD 15.1 billion plan to enhance the country’s semiconductor manufacturing capabilities. This initiative is part of India’s broader strategy to become a leader in the global semiconductor supply chain.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 48.1 Bn |

| Forecast Revenue (2034) | USD 114 Bn |

| CAGR (2025-2034) | 9.00% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Process (Sawing, Sorting, Testing, Assembly), By Packaging Type (Ball Grid Array, Chip Scale Package, Multi-package, Stacked Die, Quad and Dual), By Application (Automotive, Consumer Electronics, Industrial, Telecommunication, Aerospace and Defense, Medical and Healthcare, Logistics and Transportation, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | ASE Technology Holding Co. Ltd, Amkor Technology Inc., Powertech Technology Inc., ChipMOS Technologies Inc., King Yuan Electronics Co. Ltd, Formosa Advanced Technologies Co. Ltd, Jiangsu Changjiang Electronics Technology Co. Ltd, UTAC Holdings Ltd, Lingsen Precision Industries Ltd, Tongfu Microelectronics Co., Chipbond Technology Corporation, Hana Micron Inc., Integrated Micro-electronics Inc., Tianshui Huatian Technology Co. Ltd, Other Major Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Market")