Quick Navigation

- Report Scope

- Key Takeaways

- Key Statistics

- Analyst’s Viewpoint

- Regional Analysis

- By Component

- By Type

- By Industry Vertical

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunities

- Challenging Factors

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Recent Developments

- Report Scope

Report Scope

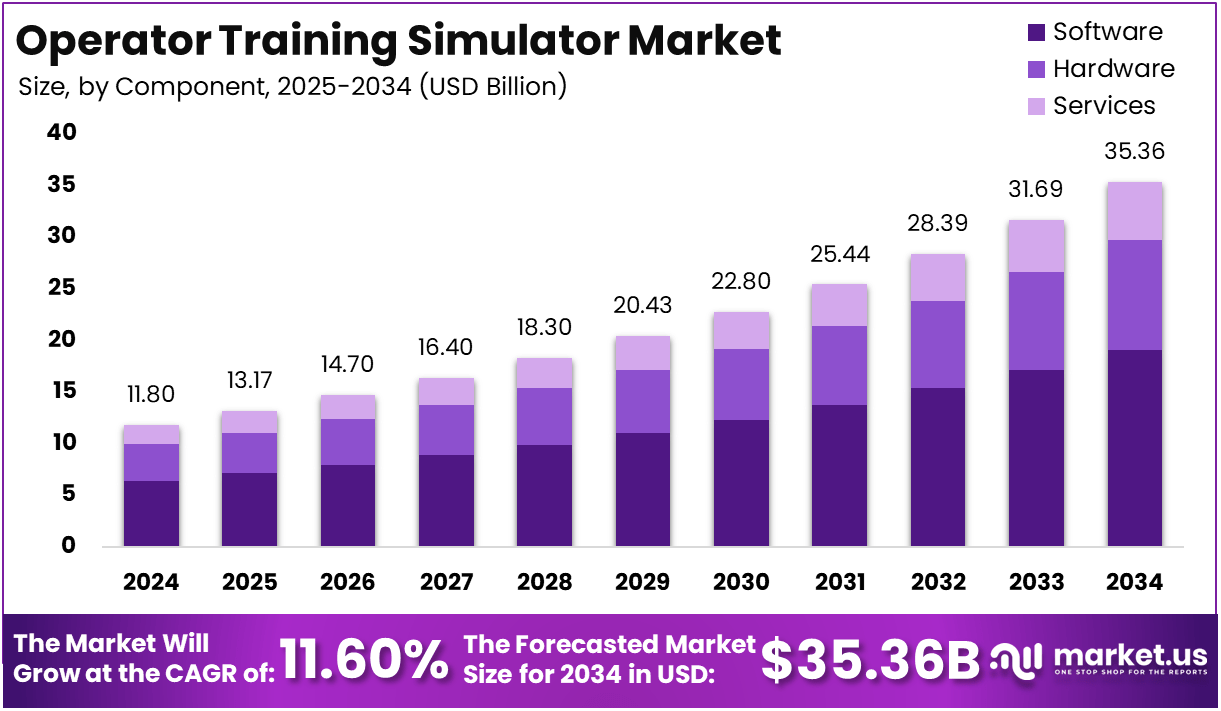

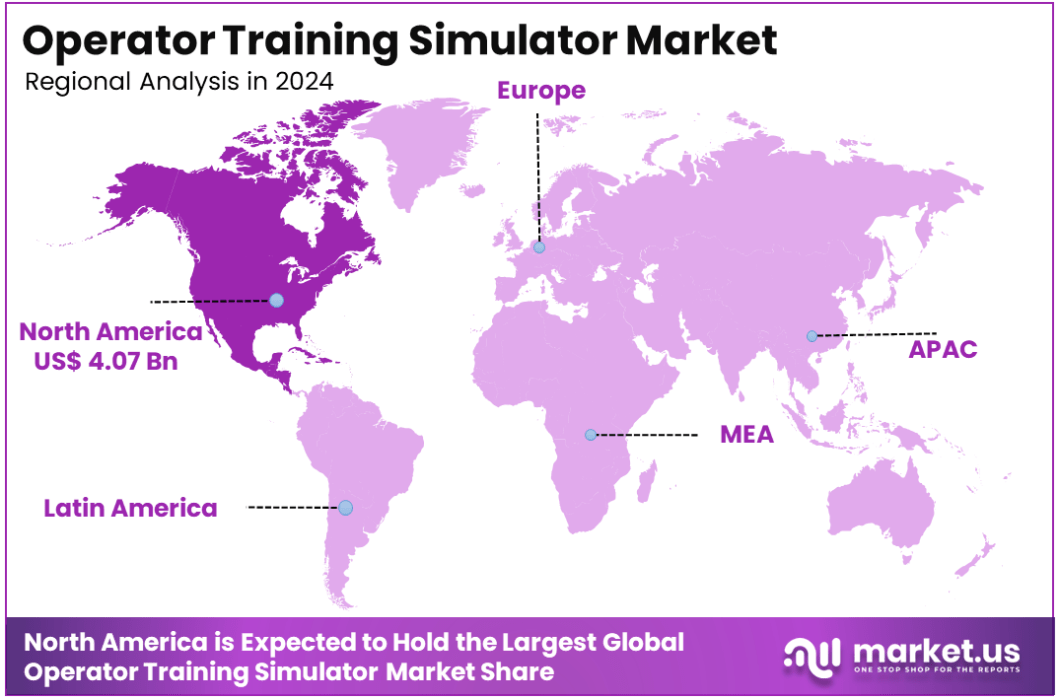

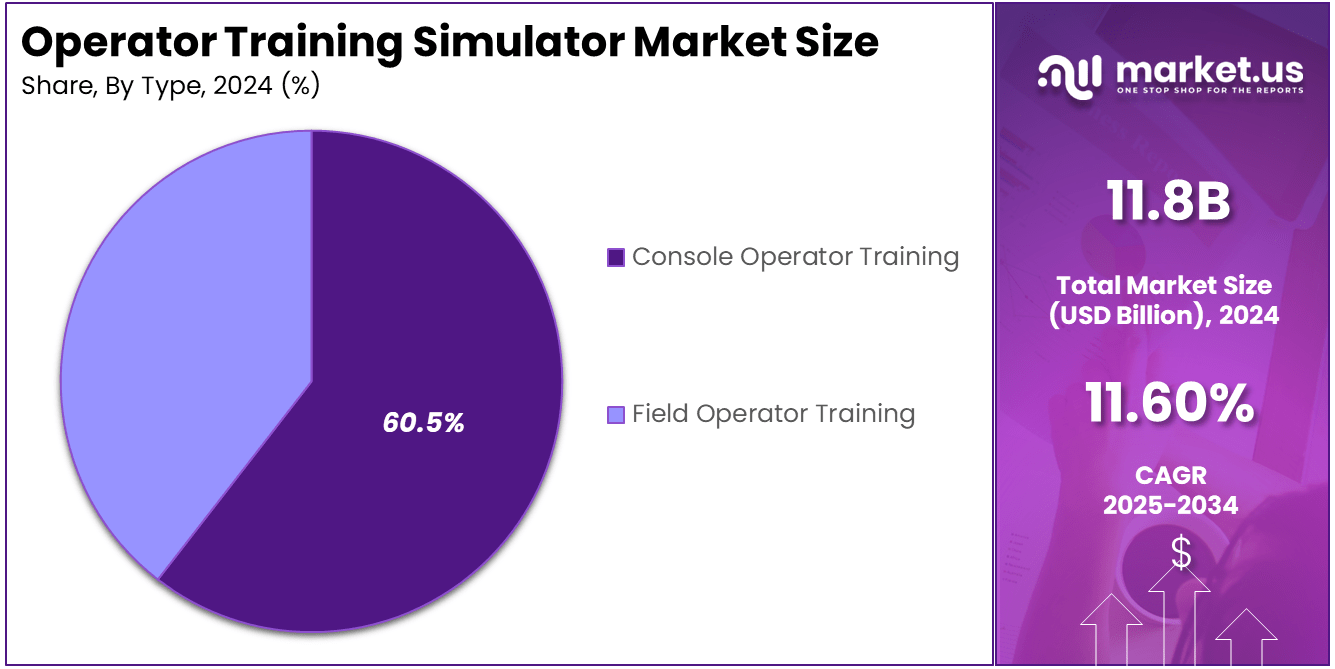

The Global Operator Training Simulator Market is expected to be worth around USD 35.36 Billion By 2034, up from USD 11.8 Billion in 2024. It is expected to grow at a CAGR of 11.60% from 2025 to 2034. In 2024, North America held a dominant market position, capturing over a 34.5% share and earning USD 4.07 Billion in revenue.

The Operator Training Simulator (OTS) market has grown significantly over the past few years, primarily driven by increasing demand across industries such as oil and gas, defense, power, and manufacturing. These simulators allow operators to undergo realistic, risk-free training in complex environments, without the need to access actual machinery or hazardous conditions.

With the rising complexity of industrial processes and a focus on safety, adopting these simulators has become crucial for enhancing operational efficiency and reducing costs. The market is expected to continue its expansion as organizations prioritize employee training to meet the challenges posed by modern technological advancements.

The growth of the OTS market is propelled by several key factors. First, the growing emphasis on operational safety and risk management across industries has created a strong need for realistic training solutions. Operators in sectors like oil and gas, where safety is paramount, are increasingly relying on OTS to gain experience in simulated hazardous conditions.

Additionally, the rising focus on workforce skill development, along with the need for training at scale, is pushing organizations to adopt cost-effective training methods that simulators can provide. Another important factor is the increased adoption of digital technologies such as Virtual Reality (VR) and Augmented Reality (AR), which enhance the realism of training programs and boost their effectiveness.

Key Takeaways

- Market Size and Growth: The global Operator Training Simulator market is valued at USD 11.8 billion in 2024 and is expected to grow to USD 35.36 billion by 2034, reflecting a robust CAGR of 11.60%.

- Component Breakdown: Software accounts for the largest share, making up 54.1% of the total market.

- Training Type: The market is dominated by Console Operator Training, which represents 60.5% of the market share, indicating a strong preference for this type of simulation training.

- Industry Vertical Focus: The Aerospace and Defense sector leads the market with 26.8% of the share, highlighting the critical need for high-quality operator training in these high-risk industries.

- Geographical Insights: North America holds a dominant position, accounting for 34.5% of the market, driven by strong demand in industries like aerospace, defense, and energy.

- Market Growth Drivers: Factors such as the increasing demand for safer training solutions, advancements in technology (like VR, AR, and AI), and regulatory pressures are fueling the market’s growth trajectory.

Key Statistics

Usage and Users

- User Base: Specific numbers of users are not provided, but the demand for skilled operators drives the market. For example, a large industrial facility might have 500 operators trained annually.

- Usage Frequency: Operators use OTS regularly for training, with some facilities reporting 20 hours of simulator use per operator per month.

Quantity

- Number of Simulators: Exact quantities of OTS units deployed are not provided in the available data. However, a large industrial company might deploy 20 OTS units across its facilities.

Industry Verticals

- Aerospace and Defense: Leads the market with 26.8% of the share, equating to about USD 3.15 billion.

- Energy and Utilities: Holds a significant share, though exact figures are not specified in the available data.

Analyst’s Viewpoint

The demand for Operator Training Simulators has been particularly strong in high-risk industries. For instance, the oil and gas sector requires highly trained personnel to operate complex machinery safely. Similarly, sectors like defense, aviation, and power generation also benefit from OTS for training on critical equipment and systems.

Demand is also increasing in emerging economies, where industrial development is accelerating, and the need for skilled operators is growing. Furthermore, regulatory bodies in many regions are enforcing stricter safety standards, further driving the demand for OTS to ensure operators meet compliance and safety certifications.

The demand for Operator Training Simulators has been particularly strong in high-risk industries. For instance, the oil and gas sector requires highly trained personnel to operate complex machinery safely. Similarly, sectors like defense, aviation, and power generation also benefit from OTS for training on critical equipment and systems.

Demand is also increasing in emerging economies, where industrial development is accelerating, and the need for skilled operators is growing. Furthermore, regulatory bodies in many regions are enforcing stricter safety standards, further driving the demand for OTS to ensure operators meet compliance and safety certifications.

Technological advancements are a crucial factor in shaping the evolution of the OTS market. The integration of VR and AR into simulators has significantly enhanced the immersive experience, providing a more realistic and engaging training environment. Additionally, the use of cloud computing in OTS systems allows for flexible, scalable training solutions that can be accessed remotely, reducing the need for expensive on-site facilities.

AI-driven simulations are also becoming more prevalent, allowing for more personalized and dynamic training experiences. These innovations are helping operators acquire the skills and knowledge needed to handle complex tasks more effectively, without the risks associated with traditional training methods.

Regional Analysis

In 2024, North America held a dominant market position, capturing more than a 34.5% share, equating to USD 4.07 billion in revenue. The region’s strong market presence is driven by a high demand for advanced training solutions across industries such as aerospace, defense, oil and gas, and manufacturing.

North America has a well-established industrial base and a high adoption rate of cutting-edge technologies, including VR, AR, and AI, which are increasingly integrated into operator training simulators. Additionally, the stringent safety regulations and the need for regulatory compliance in these high-risk industries further fuel the demand for OTS solutions in the region.

The U.S., in particular, remains a key contributor to this market share, driven by its robust defense sector and its leadership in the aviation and aerospace industries. Government investments and military contracts aimed at improving operational readiness and safety have bolstered the growth of operator training simulators. Moreover, the presence of leading companies in the simulator industry in North America has strengthened the region’s position, allowing for continuous innovation and offering a wide range of simulation products and services.

In Europe, the OTS market is projected to experience steady growth, with a focus on sectors like aerospace, automotive, and energy. Europe’s emphasis on technological innovation and the push for safety standards, especially in industries like aviation and nuclear power, are key drivers of market expansion. Countries like Germany, France, and the UK have been at the forefront of adopting sophisticated training systems, providing a favorable environment for market players. However, Europe holds a smaller share compared to North America, contributing to around 25-28% of the total market in 2024.

In the Asia-Pacific (APAC) region, the OTS market is poised for rapid growth, projected to expand at one of the highest CAGRs due to the rapid industrialization in emerging economies like China and India. APAC’s demand for operator training simulators is growing as industries such as manufacturing, energy, and transportation scale up, creating a need for well-trained operators. Although APAC holds a smaller market share in comparison to North America and Europe, it is anticipated to gain momentum, driven by increased investments in automation and technology infrastructure.

Latin America, the Middle East, and Africa each represent smaller shares of the global market but show potential for future growth. In Latin America, growth is driven by the expansion of the oil and gas sector, particularly in Brazil, while the Middle East sees rising investments in the defense and energy sectors, pushing demand for advanced training solutions. Africa, with its emerging industries, is starting to embrace operator training simulators, especially in mining and energy, although adoption rates remain lower compared to other regions.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

By Component

In 2024, the Software segment held a dominant market position, capturing more than 54.1% of the market share, contributing significantly to the overall growth of the Operator Training Simulator market.

The dominance of the software component is driven by the increasing demand for highly sophisticated and interactive training programs that leverage advanced technologies such as Virtual Reality (VR), Augmented Reality (AR), and Artificial Intelligence (AI).

These software solutions offer realistic and immersive simulations that allow operators to practice their skills in a risk-free environment, which is especially crucial in high-stakes industries such as aerospace, defense, and energy.

The software provides the flexibility to simulate complex scenarios, customize training modules, and track performance, making it an essential part of any operator training system. As industries continue to prioritize safety, compliance, and skill development, the demand for software-driven simulators has surged.

Additionally, the continuous advancements in software technologies, including cloud-based platforms and real-time analytics, further enhance their appeal, enabling remote and scalable training solutions. This growing reliance on advanced software tools is a key reason why the Software segment remains the leading component in the OTS market.

By Type

In 2024, the Console Operator Training segment held a dominant market position, capturing more than a 60.5% share of the Operator Training Simulator market. This leadership can be attributed to several key factors. Console operator training offers a highly immersive and controlled environment that closely replicates real-life operations.

It allows operators to simulate complex scenarios without the risk of real-world consequences, making it an essential tool in industries such as oil and gas, manufacturing, and power generation. Furthermore, advancements in virtual reality (VR) and augmented reality (AR) technologies have significantly enhanced the effectiveness of console training, providing a more engaging and interactive experience.

These technologies allow operators to practice their skills in a safe yet realistic setting, improving both efficiency and safety. Moreover, the growing demand for skilled operators, along with an increasing focus on safety regulations, is driving the demand for console-based training systems. The ability to train on specific equipment and processes ensures that console operator training continues to be a preferred choice for companies across various sectors.

By Industry Vertical

In 2024, the Aerospace and Defense segment held a dominant market position in the Operator Training Simulator market, capturing more than a 26.8% share. This leadership is largely driven by the critical need for highly specialized and safety-focused training in the aerospace and defense sectors. Operators in these industries are required to handle complex systems and equipment, often under high-pressure situations, where mistakes can have severe consequences.

Operator training simulators offer a safe, cost-effective way to train personnel without the risks associated with real-world training exercises. The growing demand for advanced military technologies and sophisticated aircraft further boosts the need for training simulators. Additionally, regulatory pressures related to safety and operational efficiency in both military and commercial aviation contribute to the segment’s growth.

The aerospace and defense sector’s adoption of cutting-edge simulation technologies, including virtual and augmented reality, has made training more realistic and effective, making it an essential tool for preparing operators to handle critical situations with precision and confidence. This ensures that the Aerospace and Defense segment continues to lead the market.

Key Market Segments

By Component

- Hardware

- Software

- Services

By Type

- Console Operator Training

- Field Operator Training

By Industry Vertical

- Oil and Gas

- Aerospace and Defense

- Medical and Healthcare

- Energy and Power

- Other Industry Verticals

Driving Factors

Increasing Demand for Skilled Operators

The escalating demand for a highly skilled workforce across various industries is a pivotal factor propelling the growth of the operator training simulator market. As technological complexity increases, these simulators offer a crucial solution for training operators efficiently and cost-effectively.

Industries such as aerospace, defense, energy, and manufacturing require operators to manage intricate systems and processes. Operator training simulators provide a safe and controlled environment to practice and refine skills, ensuring operators are well-prepared for real-world challenges. This approach not only enhances operational efficiency but also significantly reduces the risk of errors that could lead to costly accidents or downtime.

Furthermore, the integration of advanced technologies like virtual reality (VR) and augmented reality (AR) into training simulators has revolutionized the learning experience. These technologies offer immersive and interactive training scenarios, allowing operators to engage in realistic simulations that closely mimic actual operational conditions. Such advancements contribute to more effective skill development and better preparedness for complex tasks.

Restraining Factors

High Costs Associated with Simulator Implementation

Despite the advantages, the high costs associated with setting up and maintaining operator training simulators pose a significant challenge for many organizations. The initial investment required for purchasing advanced simulators, along with ongoing maintenance expenses, can be substantial.

For small and medium-sized enterprises (SMEs), these financial burdens can be particularly daunting. The substantial capital investment required for advanced simulators, coupled with ongoing maintenance expenses, can strain the financial resources of SMEs. This financial strain may lead to delays in adopting such technologies, potentially hindering their competitiveness in the market.

Additionally, the rapid pace of technological advancements means that simulators can become outdated relatively quickly. This necessitates regular updates and upgrades to the training systems, further increasing the total cost of ownership. Organizations must balance the benefits of enhanced training capabilities with the financial implications of these investments.

Growth Opportunities

Adoption of Cloud-Based Training Solutions

The adoption of cloud-based training solutions presents a significant growth opportunity for the operator training simulator market. Cloud technology enables organizations to access training modules and simulations remotely, reducing the need for extensive on-premises infrastructure.

Cloud-based simulators offer enhanced accessibility, allowing operators to engage in training sessions from various locations. This flexibility is particularly beneficial for organizations with multiple sites or those operating in remote areas. It also facilitates continuous learning and skill development, as operators can access training materials at their convenience.

Moreover, cloud-based solutions often come with scalable options, enabling organizations to adjust their training resources based on current needs. This scalability ensures that companies can efficiently manage training costs and resources, adapting to changes in workforce size or operational requirements.

Challenging Factors

Complexity in Developing Accurate Simulation Models

A significant challenge in the operator training simulator market is the complexity involved in developing accurate and dynamic simulation models. Creating a simulator that accurately replicates real-world processes requires detailed information about equipment specifications, process responses, and controller settings.

Industries such as chemical processing, aerospace, and energy involve intricate systems with numerous variables interacting in complex ways. Modeling these systems accurately demands a deep understanding of the underlying processes and access to comprehensive data. The absence of such detailed information can lead to oversimplified models that fail to provide realistic training scenarios.

Additionally, the dynamic nature of industrial processes means that simulators must be continuously updated to reflect changes in equipment, processes, and operational procedures. This ongoing need for updates adds to the development complexity and can increase the time and resources required to maintain the simulators.

Growth Factors

The operator training simulator market is experiencing robust growth, driven by several key factors. As industries increasingly prioritize safety and efficiency, the demand for advanced training solutions has surged.

Operator training simulators offer a cost-effective and risk-free environment for operators to practice complex scenarios, thereby enhancing their skills and reducing the likelihood of operational errors. This focus on skill development is particularly evident in sectors such as aerospace, defense, and energy, where precision and safety are paramount.

Emerging Trends

Several emerging trends are shaping the operator training simulator market. One notable trend is the increasing adoption of digital twin technology. This technology creates highly accurate virtual replicas of physical systems, enabling operators to train on simulations that mirror real-world conditions. For example, in March 2022, ETAP and Schneider Electric announced the integration of EcoStruxure Power Operation with ETAP Operator Training Simulator, significantly reducing operational risks.

Another trend is the growing emphasis on personalized and scenario-based training modules. These modules are tailored to simulate specific operational challenges, providing trainees with hands-on experience in dealing with real-world situations. This approach enhances the relevance and effectiveness of training programs, ensuring that operators are well-prepared for the complexities of their respective industries.

Business Benefits

Implementing operator training simulators offers numerous business benefits. Firstly, they enhance safety by allowing operators to practice handling complex equipment and emergency scenarios in a controlled environment. This practice reduces the risk of accidents and operational errors, leading to improved safety records and compliance with industry regulations.

Secondly, training simulators improve operational efficiency. By providing realistic training experiences, operators can develop and refine their skills, leading to better decision-making and more efficient operations. This efficiency translates into cost savings and increased productivity for organizations.

Thirdly, simulators offer a cost-effective training solution. They eliminate the need for expensive physical training setups and reduce downtime associated with traditional training methods. This cost-effectiveness makes simulators an attractive option for organizations looking to invest in workforce development without incurring significant expenses.

Lastly, simulators provide a scalable training solution. Organizations can train multiple operators simultaneously, regardless of their location, through cloud-based platforms. This scalability ensures that training programs can be efficiently managed and expanded as needed, supporting the growth and development of the organization.

Key Player Analysis

ABB Group, a global leader in power and automation technologies, has been actively expanding its capabilities in the operator training simulator market through strategic acquisitions. In May 2023, ABB completed the acquisition of Siemens’ low-voltage NEMA motor business, enhancing its position in the industrial motor sector. This acquisition not only broadened ABB’s product portfolio but also strengthened its market presence, enabling the company to offer a more comprehensive range of solutions to its customers.

Honeywell International Inc. has been proactive in enhancing its operator training simulator offerings through strategic initiatives. In April 2018, Honeywell launched a cloud-based simulator solution that combines virtual reality (VR) and augmented reality (AR) technologies. This innovative platform enables industrial workers to engage in immersive training experiences, improving their skills and safety awareness.

Siemens AG, a global technology powerhouse, has been instrumental in advancing operator training simulators through strategic initiatives. In December 2024, Siemens Gamesa agreed to sell its power electronics unit to ABB Group, a move that is expected to conclude in the second half of 2025. This transaction aims to bolster ABB’s position in the renewable power conversion technology market.

Top Key Players in the Market

- ABB Group

- Honeywell International Inc.

- Siemens AG

- Emerson Electric Co.

- Schneider Electric SE

- Yokogawa Electric Corporation

- GSE Solutions

- Operation Technology, Inc.

- ANDRITZ AG

- Kongsberg Gruppen ASA

- Other Key Players

Recent Developments

- In 2024, Honeywell International launched an advanced cloud-based operator training simulator integrating virtual and augmented reality technologies, enhancing immersive training experiences.

- In 2024, ABB Group acquired the low-voltage NEMA motor business from Siemens, expanding its capabilities to offer more comprehensive operator training solutions in industrial sectors.