Quick Navigation

Report Overview

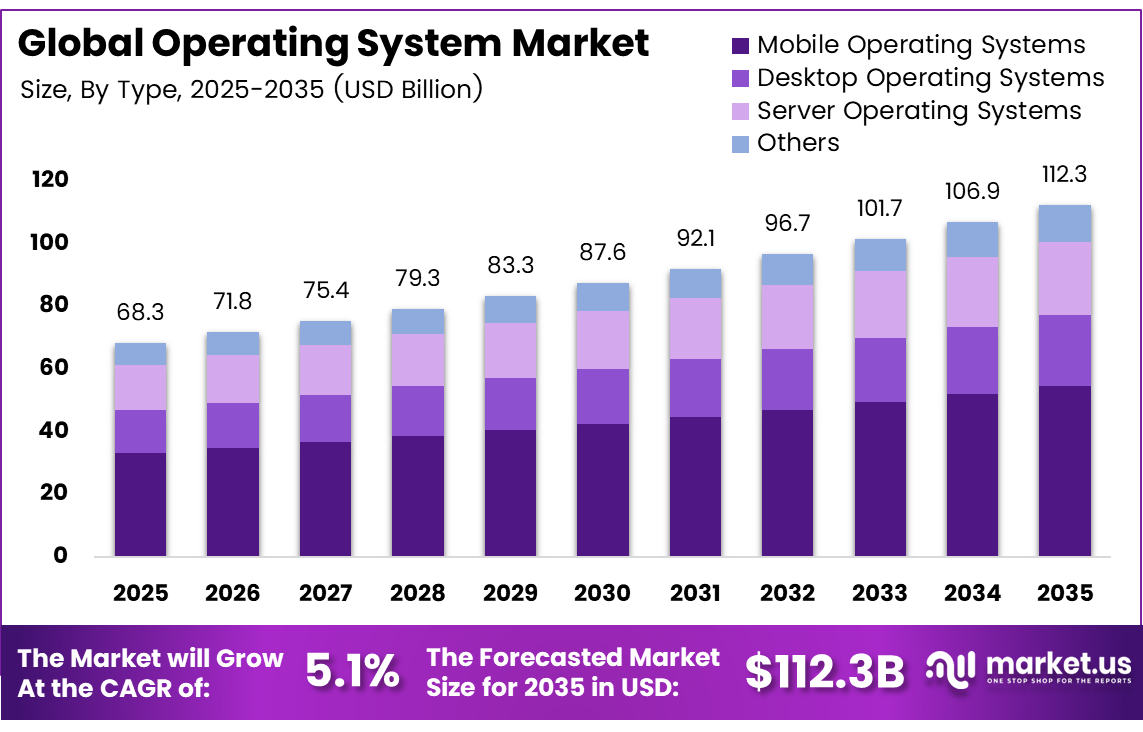

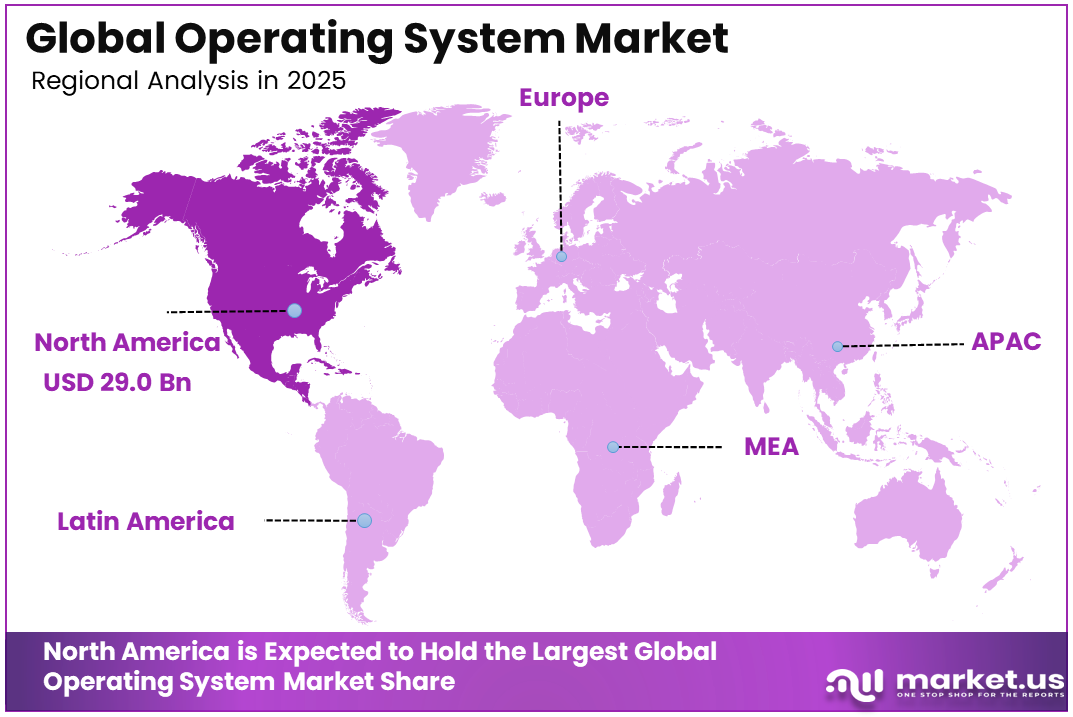

The Global Operating System Market size is expected to be worth around USD 112.3 billion by 2035, from USD 68.3 billion in 2025, growing at a CAGR of 5.1% during the forecast period from 2026 to 2035. North America held a dominant market position, capturing more than a 42.5% share, holding USD 29.0 billion in revenue.

An operating system refers to the core software that manages a device’s hardware, applications, memory, storage, and user interactions. It allows computers, smartphones, servers, and connected devices to run programs smoothly. It also controls system resources, supports security functions, and provides the basic interface needed for users and software to work efficiently.

Top driving factors include the rising need for secure, reliable, and stable operating systems across connected devices. Modern operating systems support more than 90% of connected devices, including smartphones, industrial controllers, and edge systems. As cloud workloads, connected services, and frequent updates increase, CIOs are prioritizing platforms that reduce downtime and support high user volumes.

The market for operating systems is driven by the rising use of smartphones, laptops, servers, cloud platforms, and connected devices. Businesses need stable software environments to manage applications, data, security, and user access. Growing digital services, remote work, and enterprise modernization are also increasing demand for reliable operating systems that support performance, updates, and smooth device management.

Demand Analysis shows that operating system adoption is strongly tied to shipments of smartphones, PCs, IoT nodes, and other connected hardware. These devices need a stable platform layer to run applications and services. Demand is also supported by cloud and server deployments, as data centers refresh infrastructure every 3 to 5 years to meet traffic and security needs.

For instance, in June 2025, SUSE advanced its Linux and edge OS offerings, targeting industrial and telco deployments that need hardened, real-time capabilities. With enterprises pursuing vendor diversification beyond Red Hat, SUSE is carving out growth in specialised, high-reliability environments where long-term support and certified stacks are non-negotiable buying criteria.

Key Takeaway

- In 2025, the Mobile Operating Systems segment held a dominant market position, capturing a 48.7% share of the Global Operating System Market.

- In 2025, the Proprietary/Commercial segment held a dominant market position, capturing a 65.3% share of the Global Operating System Market.

- In 2025, the On-premises segment held a dominant market position, capturing a 71.2% share of the Global Operating System Market.

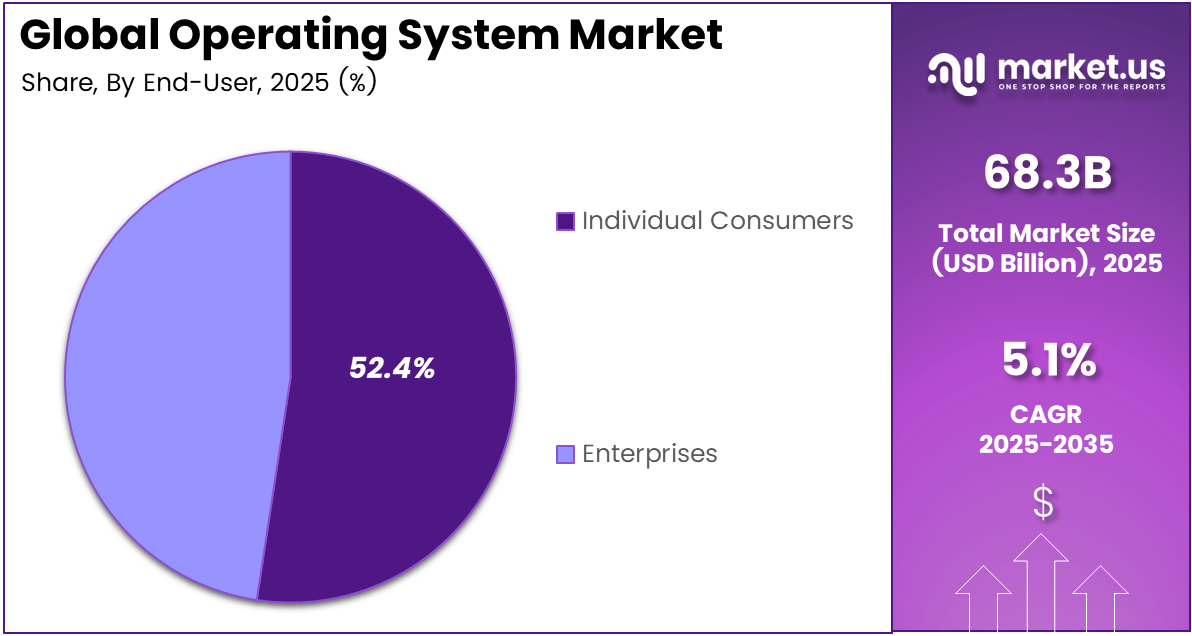

- In 2025, the Individual Consumers segment held a dominant market position, capturing a 52.4% share of the Global Operating System Market.

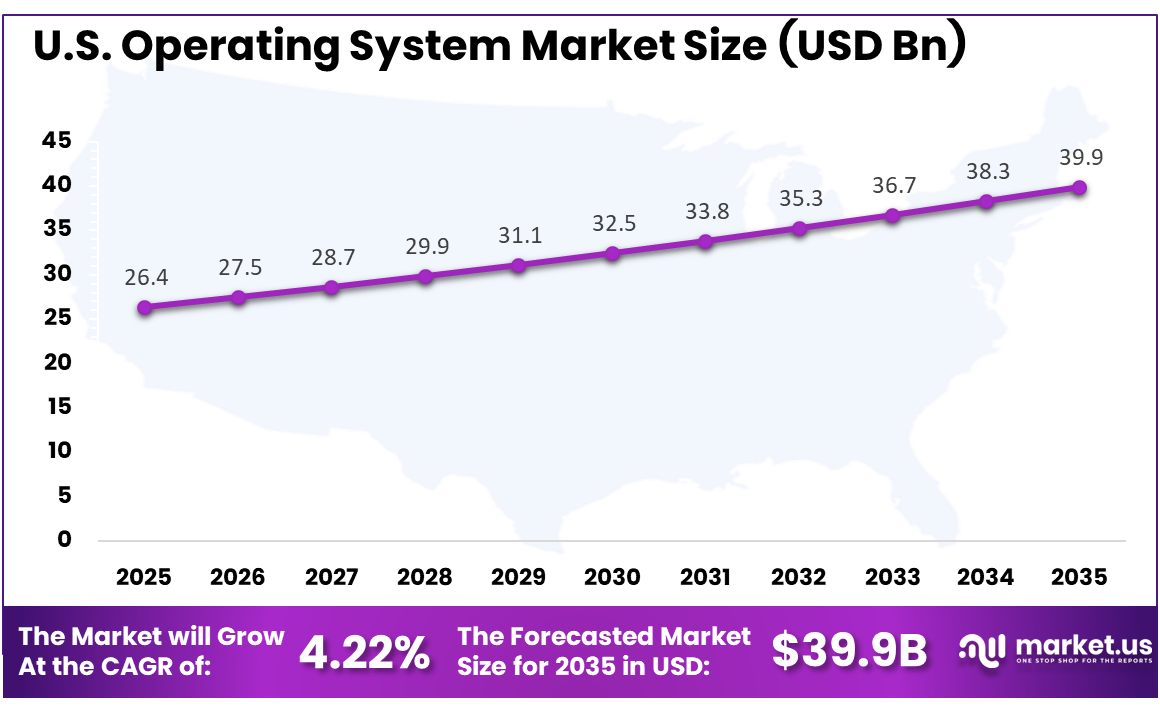

- The U.S. Operating System Market was valued at USD 26.4 billion in 2025, with a robust CAGR of 4.22%.

- In 2025, North America held a dominant market position in the Global Operating System Market, capturing more than a 42.5% share.

Role of Generative AI

Generative AI is becoming part of the operating system layer, not just a separate tool. It helps users search, manage tasks, automate workflows, and interact through natural language. With around 53% of C-suite leaders already using generative AI regularly, demand is rising for OS level intelligence.

This shift is changing how operating systems are designed. Vendors are focusing on user experience, smarter resource use, and built-in automation. AI can learn user behavior, manage notifications, improve power use, and predict which files or applications may be needed next, making devices more responsive and personal.

Investment and Business Benefits

Investment opportunities are growing in open source platforms, cloud-optimized distributions, and specialized operating systems for telecom, data centers, and industrial equipment. Linux already powers over 60% of servers, which supports investor interest in flexible platform models. Edge gateways, automotive systems, and VR or AR devices are also creating demand for new operating environments.

Business Benefits include lower downtime, stronger process handling, better user productivity, and reduced infrastructure cost. The right operating system strategy helps companies use virtualization and cloud models to scale resources when required. Standardizing fewer OS variants also reduces support work, simplifies patching, and lowers the risk of security incidents and unplanned outages across endpoints and servers.

Regional Analysis

In 2025, North America held a dominant market position in the Global Operating System Market, capturing more than a 42.5% share, holding USD 29.0 billion in revenue. This dominance is due to strong technology adoption, high use of smartphones, PCs, cloud platforms, and enterprise servers across the region. The presence of advanced IT infrastructure, large software ecosystems, and early adoption of secure digital platforms also supports growth. Rising demand from businesses and consumers continues to strengthen North America’s leadership.

For instance, in September 2025, Microsoft announced Windows 12 with integrated AI threat detection, advanced biometric security, and tighter cloud integration, reinforcing Windows’ central role in North American PCs and enterprise endpoints. The OS quickly saw strong enterprise uptake, underscoring Microsoft’s dominance in desktop and server operating systems across the region.

U.S. Operating System Market Size

The market for operating systems within the U.S. is growing tremendously and is currently valued at USD 26.4 billion; the market has a projected CAGR of 4.22%. The market is growing due to strong demand for smartphones, laptops, enterprise servers, cloud platforms, and connected devices. U.S. businesses are also upgrading operating environments to improve security, support remote work, and manage software updates more efficiently. Rising use of AI, edge computing, and digital services further supports steady operating system adoption.

For instance, in September 2025, Google continued strengthening Android’s position as the leading mobile operating system in North America through security hardening and AI-driven optimization updates. Enhanced protection against zero-day exploits and tighter integration with Google services helped Android remain the default platform for most regional smartphone OEMs and users.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Type Analysis

In 2025, the Mobile Operating Systems segment held a dominant market position, capturing a 48.7% share of the Global Operating System Market. This dominance is due to the wide use of smartphones, tablets, and connected personal devices in daily life. Mobile operating systems support apps, payments, communication, entertainment, and work tasks through one platform. Their simple interface and regular updates make them important for both consumers and businesses.

The segment also benefits from the strong link between mobile devices and digital services. Users expect smooth app performance, secure access, and fast system response. As mobile-first behavior grows across banking, shopping, gaming, and remote work, mobile operating systems continue to remain central to the operating system market.

For instance, in October 2025, Apple introduced a major iOS release that focused on device intelligence and cross-device continuity for iPhone, iPad, and Mac users. The company focused on subtle improvements that make everyday tasks feel more fluid, helping it defend the premium end of the mobile OS space and lock in loyal users within its ecosystem.

License Type Analysis

In 2025, the Proprietary/Commercial segment held a dominant market position, capturing a 65.3% share of the Global Operating System Market. This dominance is due to the strong trust placed in licensed operating systems by businesses, institutions, and individual users. Proprietary platforms are often preferred because they offer structured support, regular updates, security patches, and controlled system management. This makes them suitable for environments where reliability and accountability are important.

Commercial operating systems also help organizations simplify compliance, device control, and software compatibility. Enterprises often choose these systems because they work well with productivity tools, security software, and managed IT frameworks. Their predictable support model continues to strengthen adoption across professional and personal computing environments.

For instance, in March 2026, Microsoft rolled out another wave of Windows enhancements that deepen ties with its productivity and collaboration tools. The company stressed security, device management, and cloud connectivity, showing how a commercial operating system can anchor a full stack of paid services for both consumers and enterprises.

Deployment Analysis

In 2025, the On-premises segment held a dominant market position, capturing a 71.2% share of the Global Operating System Market. This dominance is due to the need for direct control over operating systems, infrastructure, and sensitive data. Many organizations prefer on-premises deployment because it allows internal teams to manage access, updates, hardware, and security policies. This approach is important in sectors with strict compliance and operational control needs.

On-premises deployment also supports customized system environments and stable internal operations. Businesses with legacy applications, private networks, and critical workloads often prefer keeping systems within their own facilities. This helps reduce dependency on external platforms while giving IT teams stronger control over performance, maintenance, and risk management.

For instance, in January 2026, SUSE reiterated its commitment to enterprise Linux for regulated and performance-sensitive environments that still rely heavily on on-premises infrastructure. It highlighted tools to simplify life cycle management across physical servers and private clouds, showing that on-site operating systems remain a core part of many IT roadmaps.

End-User Analysis

In 2025, the Individual Consumers segment held a dominant market position, capturing a 52.4% share of the Global Operating System Market. This dominance is due to the everyday use of operating systems in smartphones, laptops, tablets, and personal computers. Individual consumers depend on these systems for browsing, messaging, payments, learning, entertainment, and app access. A simple user experience and regular updates make operating systems essential for daily digital activity.

Consumer demand is also supported by frequent device usage and rising comfort with digital services. People expect operating systems to be fast, secure, and easy to use across different devices. As personal technology becomes part of work, education, and lifestyle needs, individual users remain a major market group.

For instance, in March 2026, Google pushed a new Android interface and privacy improvements aimed at everyday users, including easier permission controls and better customization. These updates target individual consumers who want more control over how apps behave, helping Android remain attractive across many price points and regions.

Key Market Segments

By Type

- Desktop Operating Systems

- Mobile Operating Systems

- Server Operating Systems

- Others

By License Type

- Proprietary/Commercial

- Open Source

By Deployment

- On-premises

- Cloud-based

By End-User

- Individual Consumers

- Enterprises

Emerging Trends

Operating systems are moving toward built-in AI support, where users can search, write, automate tasks, and manage files through natural language. This trend is changing the OS from a passive software layer into a more active assistant that supports daily work across apps, screens, and devices.

Another key trend is the rise of cloud and edge-ready operating systems. Enterprises need platforms that can run workloads across data centers, remote sites, and connected devices with better control. This is increasing demand for secure, flexible, and lightweight OS environments that support distributed computing needs.

Growth Factors

Growth is supported by rising enterprise demand for automation, security, and better workload management. Businesses now expect operating systems to support intelligent resource allocation, predictive maintenance, and AI-based threat detection. This reduces dependence on external software tools and helps IT teams manage complex digital environments more efficiently.

IoT and edge deployments are also creating strong demand for AI-infused operating systems. These systems can run smaller AI models locally, reduce latency, and support faster decisions. In factories, vehicles, and connected devices, local intelligence helps detect issues, trigger actions, and send only selected data back to central systems.

Market Dynamics

Drivers - Growing Connected Devices and Cloud Use

The operating system market is driven by the rising use of connected devices across homes, offices, factories, and public services. Each device needs a stable platform to run applications, manage data, and support secure communication. This makes operating systems a basic layer of modern digital infrastructure.

Cloud adoption is also increasing the need for reliable operating environments. Businesses depend on cloud platforms to manage workloads, store data, and support remote access. Operating systems help connect devices, servers, and applications smoothly, which supports better performance, stronger control, and easier system management.

For instance, in April 2026, Microsoft highlights Windows Server as a cloud-ready operating system that ties on-premises infrastructure to Azure services, helping enterprises run connected workloads across data centers and cloud regions. This approach supports growing device fleets and hybrid deployments by giving IT teams one OS family for identity, storage, and application hosting across environments.

Restraint - High Development and Maintenance Complexity

Operating system development requires deep technical expertise, long testing cycles, and continuous improvement. Developers must ensure that the system works with different hardware, applications, security tools, and user needs. This complexity increases cost and makes it difficult for new vendors to enter the market.

Maintenance also creates pressure because operating systems need regular fixes, compatibility checks, and security updates. Any error can affect device performance, business operations, or user trust. Companies must invest heavily in support teams, testing systems, and update management, which can slow wider adoption.

For instance, in October 2025, a UK competition investigation into Google’s mobile operating system describes strong network effects and limited switching, but also highlights fragmentation and ecosystem complexity as ongoing issues. Supporting many device types and software versions makes development and maintenance harder, forcing Google and partners to invest heavily in compatibility, updates, and quality control across the Android platform.

Opportunities - Cloud and Edge Expansion

Cloud and edge expansion are creating strong opportunities for operating system providers. Businesses need platforms that can support workloads across data centers, remote sites, and connected devices. Operating systems that offer flexibility, stability, and smooth workload movement are becoming more valuable in modern IT environments.

Edge computing also requires lightweight, secure operating systems that can process data closer to users and machines. This is important for industries using sensors, automation, and real-time monitoring. As digital systems move beyond central data centers, demand for specialized operating platforms is expected to grow.

For instance, in May 2026, VMware announced Cloud Foundation Edge 9.1 as an autonomous edge platform that can run virtual machines and Kubernetes workloads across distributed sites. This responds directly to cloud and edge expansion by treating the OS and virtualization stack as a unified layer that brings cloud-like operations to retail outlets, plants, and remote branches.

Challenges - Security and Update Pressure

Security and update pressure remain a major challenge for the operating system market. Every operating system must protect devices from threats while supporting smooth performance. Frequent updates are needed to fix risks, but they must be planned carefully to avoid disruption in business and consumer environments.

Large organizations often manage many devices across different locations, which makes update control more difficult. Delayed patches can increase security exposure, while rushed updates may cause software issues. This creates a constant need for careful testing, clear policies, and strong system monitoring across all operating environments.

For instance, in May 2026, Red Hat introduced RHEL 10.2 and 9.8, focusing on post-quantum cryptography, AI-assisted operations, and streamlined upgrade paths to address emerging security threats. These releases show the updated pressure on OS vendors, who must continuously harden systems, manage vulnerabilities, and simplify upgrades so enterprises can keep pace without excessive manual effort.

Key Players Analysis

One of the leading players in April 2025, Microsoft expanded Windows 11 enterprise adoption by tightening integration with its cloud stack, promoting security features like enhanced credential isolation and automated patching. This strategy helps defend its 70+% desktop share in organisations, even as some customers delay upgrades, reinforcing Windows as the de facto standard for corporate endpoint operating systems.

Top Key Players in the Market

- Microsoft Corporation

- Google LLC

- Apple, Inc.

- Canonical, Ltd.

- Red Hat, Inc. (an IBM company)

- Amazon Web Services, Inc.

- Huawei Technologies Co., Ltd.

- Samsung Electronics Co., Ltd.

- Oracle Corporation

- VMware, Inc. (a Broadcom company)

- SUSE Software Solutions Germany GmbH

- Cisco Systems, Inc.

- Siemens AG

- Wind River Systems, Inc.

- BlackBerry, Ltd.

- Others

Recent Developments

- In July 2025, Canonical advanced Ubuntu’s role in cloud and edge deployments by refining long-term-support releases with lighter footprints and real-time kernel options. With Linux powering a growing share of AI, container, and edge workloads, Ubuntu remains a default choice for enterprises standardising on open-source operating environments.

- In October 2025, Oracle updated Oracle Linux and its engineered systems stack to better support database workloads, cloud migrations, and autonomous operations. By tightly coupling its OS, virtualisation, and database tools, Oracle positions its Linux distribution as a performance-optimised platform for mission-critical enterprise applications running on-premises and in Oracle Cloud.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 68.3 Billion |

| Forecast Revenue (2035) | USD 112.3 Billion |

| CAGR (2026-2035) | 5.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Desktop Operating Systems, Mobile Operating Systems, Server Operating Systems, Others), By License Type (Proprietary/Commercial, Open Source), By Deployment (On-premises, Cloud-based), By End-User (Individual Consumers, Enterprises) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Microsoft Corporation, Google LLC, Apple, Inc., Canonical, Ltd., Red Hat, Inc. (an IBM company), Amazon Web Services, Inc., Huawei Technologies Co., Ltd., Samsung Electronics Co., Ltd., Oracle Corporation, VMware, Inc. (a Broadcom company), SUSE Software Solutions Germany GmbH, Cisco Systems, Inc., Siemens AG, Wind River Systems, Inc., BlackBerry, Ltd., Others |

| Customization Scope | Customization at the segment and region/country levels will be provided. Moreover, customization can be tailored to the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |