Quick Navigation

Report Overview

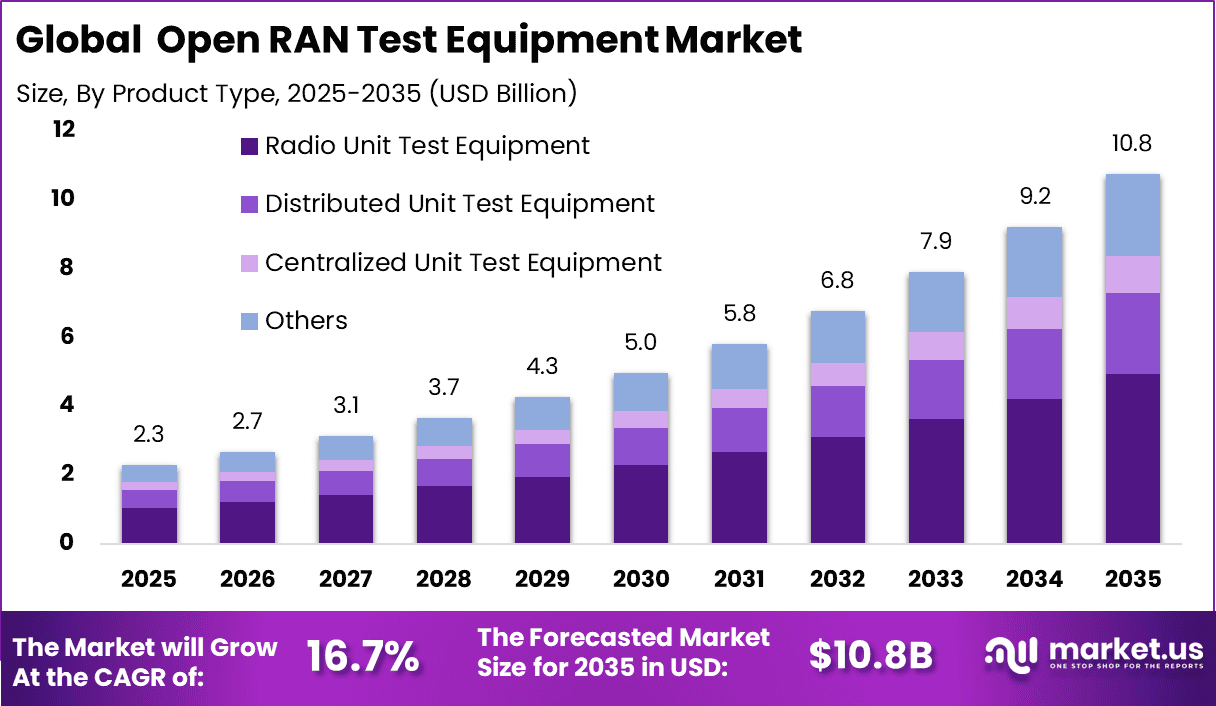

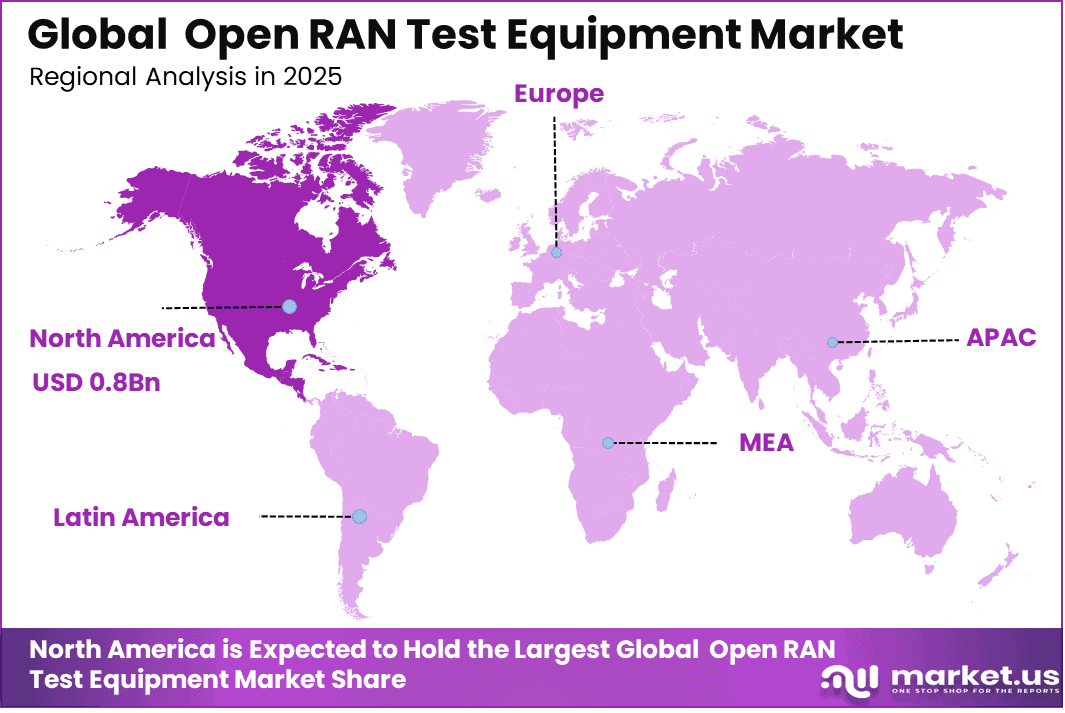

The Global Open RAN Test Equipment Market size is expected to be worth around USD 10.8 Billion By 2035, from USD 2.3 billion in 2025, growing at a CAGR of 16.7% during the forecast period from 2026 to 2035. North America held a dominant Market position, capturing more than a 39.1% share, holding USD 0.8 Billion revenue.

The Open RAN test equipment market refers to specialized testing solutions designed to validate, monitor, and optimize open radio access network architectures. These systems are essential for ensuring interoperability, performance, and security across disaggregated network components. Unlike traditional telecom networks, Open RAN separates hardware and software layers, which increases flexibility but also introduces complexity in testing.

Top driving factors for this market are strongly linked to the global transition toward 5G and open network architectures. Telecom operators are increasingly shifting to Open RAN to reduce costs and avoid vendor lock in, which has created a need for advanced testing solutions. The disaggregated nature of Open RAN requires each component to be tested individually as well as in integrated environments to ensure compliance and interoperability.

Based on data from market.us, The global Open RAN market is witnessing a significant transformation driven by the shift toward open and disaggregated network architectures. The market is projected to expand from USD 2,957 Million in 2024 to approximately USD 79,379 Million by 2034, reflecting a strong CAGR of 38.9% over the forecast period. This growth is driven by rising telecom demand for flexible, vendor neutral networks and expanding 5G deployment globally.

Increasing adoption technologies in this market are centered on virtualization, cloud native architectures, and artificial intelligence driven testing frameworks. Software defined testing tools are being widely used to simulate network conditions and automate validation processes. AI based testing platforms are also emerging, enabling faster identification of faults and reducing manual intervention. These technologies improve testing efficiency and support large scale deployments by enabling real time monitoring and automated troubleshooting.

Key reasons for adopting Open RAN test equipment include the need for interoperability assurance, network performance optimization, and security validation. In multi vendor environments, components must function cohesively despite being developed by different suppliers. Testing solutions ensure that these components meet standard specifications and operate without compatibility issues. In addition, the growing threat landscape in telecom networks has increased the need for robust security testing to identify vulnerabilities early in the deployment cycle.

Top Market Takeaways

- In the open RAN test equipment market, radio unit test equipment held a leading share of 45.8%.

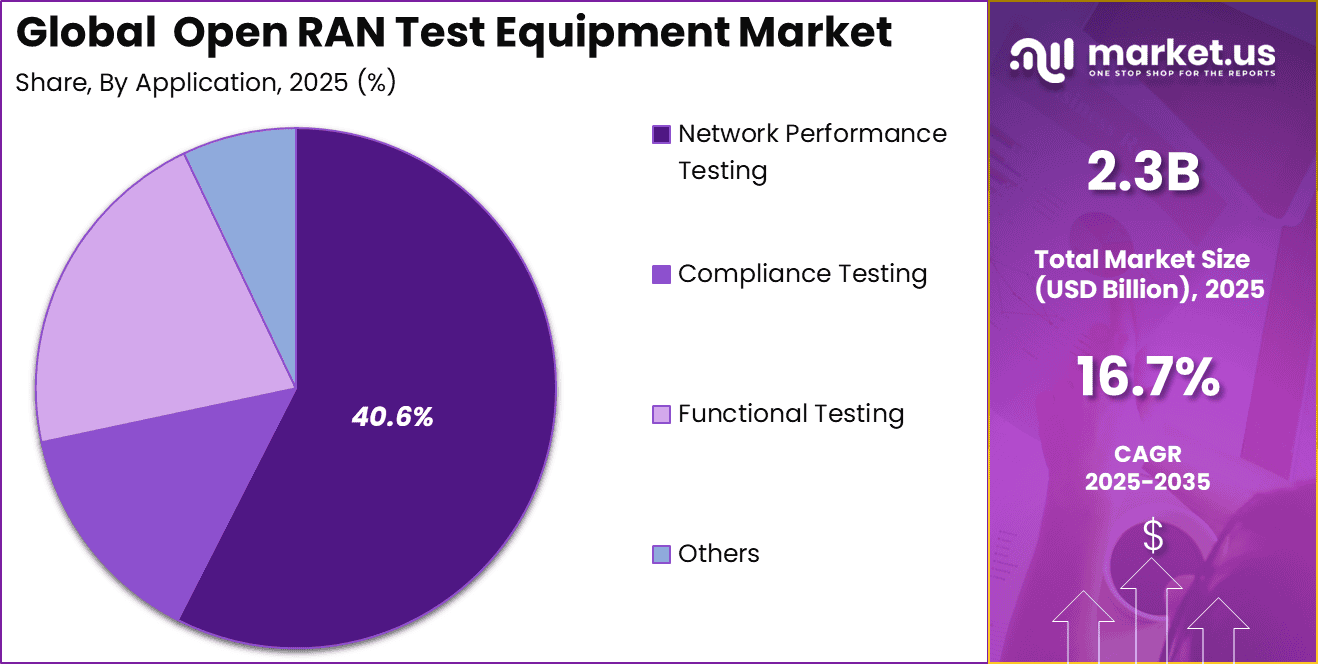

- Network performance testing accounted for 40.6%, reflecting strong demand for validating network efficiency and reliability.

- Telecom operators represented 58.4% of the market, making them the dominant end-user segment.

- Lab testing led deployment mode with a share of 60.7%, supported by the need for controlled testing environments before field rollout.

- North America held a dominant market share of 39.1%.

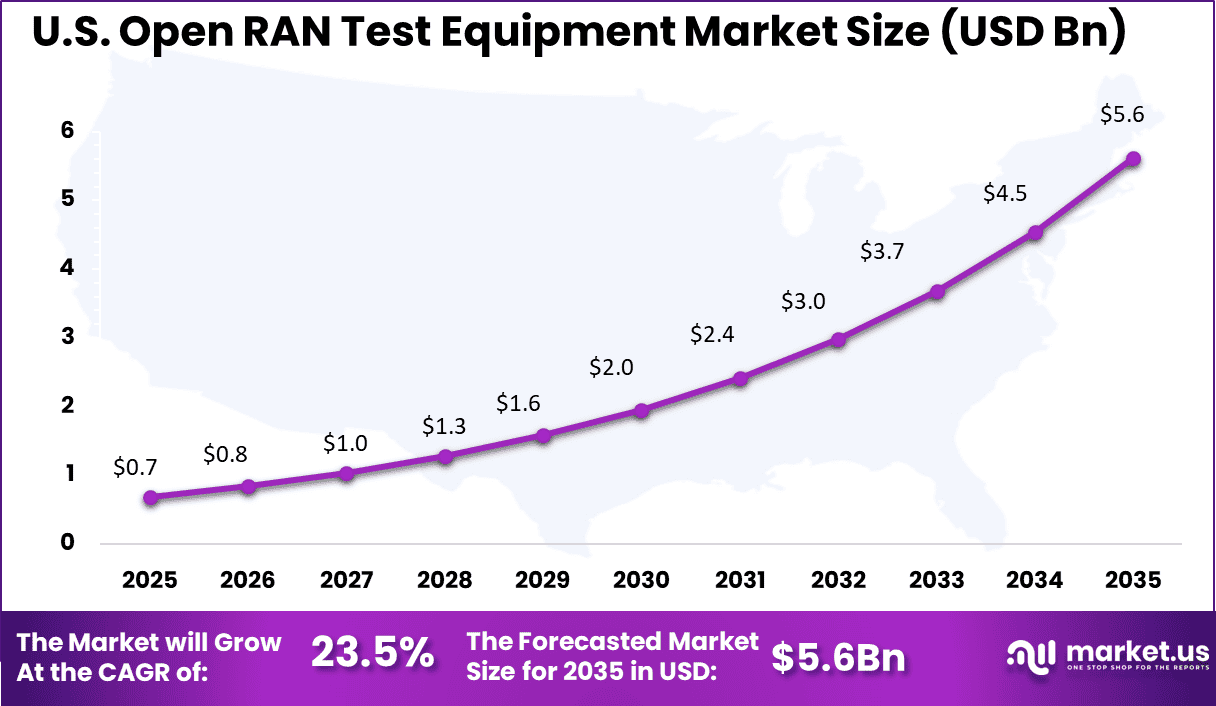

- The U.S. market was valued at USD 0.68 billion and is projected to grow at a CAGR of 23.5%

Key Insights Summary

- Open RAN has moved from early trials to broader rollout, with Open RAN revenue returning to double digit growth in 2025 after a sharp contraction between 2022 and 2024.

- Public or macrocell Open RAN deployments made up about 64% of the Open RAN market in 2025, showing that most commercial activity is in wide area coverage rather than only small cells or private networks.

- Open RAN is expected to account for around 10%+ of overall RAN revenue by 2025, signalling that a meaningful slice of new RAN spend is shifting to open architectures.

- Asia Pacific leads Open RAN deployment share in some recent estimates, with around 40%+ of Open RAN revenue linked to this region due to large scale 5G rollouts.

- Hybrid cloud is emerging as a common deployment model for Open RAN infrastructure, with about 50% share among deployment options as operators combine on premises and cloud resources for flexibility and latency control.

- Governments and ecosystem programs are expanding Open RAN testing capacity, for example with new 5G Open RAN testing labs in India and additional authorized labs in the US to support conformance and interoperability work.

By Product Type

In 2025, the radio unit test equipment segment held a dominant share of 45.8% in the Open RAN test equipment market, driven by the increasing deployment of disaggregated radio access networks. Radio units are critical components in Open RAN architecture, requiring precise testing to ensure interoperability and performance across multi-vendor environments.

As telecom operators transition toward open and flexible network models, the demand for specialized radio testing tools has increased. This has positioned radio unit testing as a key focus area in network validation. The segment’s growth is further supported by the rising complexity of 5G deployments and the need for continuous performance verification.

Testing equipment is essential to ensure signal quality, latency optimization, and compliance with network standards. Vendors are developing advanced testing solutions to support real-time analysis and scalability. This has reinforced the importance of radio unit test equipment within Open RAN ecosystems.

By Application

In 2025, the network performance testing segment accounted for 40.6% share, reflecting the critical need to maintain high-quality service in Open RAN environments. Telecom networks require continuous monitoring to ensure seamless connectivity, low latency, and efficient data transmission. Performance testing tools help identify bottlenecks, detect anomalies, and optimize network operations. This has driven strong adoption across telecom infrastructure projects.

The segment’s expansion is also influenced by increasing data traffic and growing demand for reliable connectivity. Operators are focusing on ensuring consistent network performance as they scale 5G and future network technologies. Advanced testing solutions provide real-time insights and predictive capabilities, enabling proactive network management. This has made performance testing a central application in the market.

By End-User

In 2025, the telecom operators segment held a dominant share of 58.4%, supported by their direct involvement in deploying and managing Open RAN networks. These operators require advanced testing equipment to ensure network reliability, interoperability, and compliance with standards. The shift toward multi-vendor ecosystems has increased the need for comprehensive testing solutions. As a result, telecom operators remain the primary end-users in the market.

The segment’s leadership is further driven by the rapid expansion of mobile networks and increasing demand for high-speed connectivity. Operators are investing in testing infrastructure to support network upgrades and maintain service quality. The adoption of Open RAN technologies also requires continuous validation of network components. This has strengthened the role of telecom operators in driving market demand.

By Deployment Mode

In 2025, the lab testing segment captured 60.7% share, reflecting the importance of controlled testing environments in validating Open RAN components. Lab testing allows organizations to simulate network conditions and identify potential issues before deployment. This approach reduces operational risks and ensures system compatibility across different vendors. As Open RAN architecture becomes more complex, lab-based validation has gained significant importance.

The segment’s growth is also supported by the need for early-stage testing during network development and integration. Lab environments provide a secure and controlled space for experimenting with new technologies and configurations. This enables faster troubleshooting and performance optimization. As a result, lab testing remains a critical step in the deployment of Open RAN solutions.

Regional Analysis

In 2025, North America accounted for 39.1% of the Open RAN test equipment market, supported by early adoption of Open RAN technologies and strong investment in 5G infrastructure. The region has a well-established telecommunications ecosystem that encourages innovation and deployment of advanced network solutions. Telecom operators are actively investing in testing equipment to support network transformation initiatives. This has positioned North America as a leading region in the market.

The regional dominance is further driven by collaboration between technology providers, telecom companies, and regulatory bodies. Continuous investment in research and development has accelerated the adoption of Open RAN frameworks. The presence of advanced infrastructure and skilled workforce also supports market growth. These factors collectively contribute to North America’s strong position.

Country Analysis

In 2025, the United States Open RAN test equipment market reached USD 0.68 billion and is expanding at a CAGR of 23.5%, reflecting rapid growth driven by network modernization efforts. The country’s telecom operators are actively adopting Open RAN technologies to enhance flexibility and reduce dependency on single vendors. This has increased the demand for advanced testing solutions to ensure network performance and interoperability. As a result, the U.S. market continues to expand steadily.

The growth in the U.S. is also supported by increasing investments in 5G and next-generation network technologies. Organizations are focusing on improving network efficiency and scalability through innovative testing approaches. Strong government support and industry initiatives further encourage adoption. This has positioned the United States as a key contributor to the global Open RAN test equipment market.

Key Market Segments

By Product Type

- Radio Unit Test Equipment

- Distributed Unit Test Equipment

- Centralized Unit Test Equipment

- Others

By Application

- Network Performance Testing

- Compliance Testing

- Functional Testing

- Others

By End-User

- Telecom Operators

- Network Equipment Manufacturers

- Others

By Deployment Mode

- Lab Testing

- Field Testing

Regional Analysis and Coverage

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Emerging Trends Analysis

The Open RAN test equipment market is evolving with the increasing shift toward open, disaggregated, and software-driven network architectures. Telecom networks are no longer built using a single vendor model, which has increased the need for flexible and interoperable testing solutions. Testing environments are becoming more automated and software-centric, enabling continuous validation of network components across cloud and edge infrastructure.

Another important trend is the rise of end-to-end testing frameworks that cover multiple layers of the network. Open RAN systems require validation of radio units, distributed units, centralized units, and cloud platforms simultaneously. As a result, integrated testing solutions are being adopted to ensure seamless interoperability and performance across all network elements. This is supporting faster deployment of next-generation networks and reducing integration risks.

Driver Analysis

The primary driver of the Open RAN test equipment market is the rapid expansion of 5G infrastructure. Telecom operators are adopting Open RAN to improve flexibility and reduce dependency on traditional network vendors. However, this multi-vendor environment increases complexity, making comprehensive testing essential to ensure network reliability and performance. This has significantly increased demand for advanced testing tools.

In addition, the need for cost-efficient and scalable network deployment is driving adoption. Open RAN allows operators to optimize capital and operational expenses, but it requires continuous validation of components and software updates. Testing equipment plays a critical role in ensuring that networks operate efficiently while maintaining service quality.

Restraint Analysis

One of the key restraints in the Open RAN test equipment market is the technical complexity associated with multi-vendor integration. Each component in an Open RAN environment must work seamlessly with others, which requires extensive testing and validation. This complexity can increase deployment timelines and require specialized expertise.

Another restraint is the high initial investment required for advanced testing infrastructure. Developing and deploying comprehensive testing systems involves significant costs, including software tools, hardware equipment, and skilled professionals. This can limit adoption among smaller telecom operators or new market entrants.

Opportunity Analysis

Significant opportunities are emerging from the global push toward open and interoperable telecom ecosystems. Governments and telecom operators are supporting Open RAN initiatives to promote competition and innovation. This is encouraging new network deployments, which in turn increases the demand for testing solutions to validate performance and compliance.

Additionally, the growth of private networks across industries such as manufacturing, logistics, and smart infrastructure is creating new opportunities. These networks require customized Open RAN deployments, which must be tested for performance, reliability, and security. This is expanding the application scope of Open RAN test equipment beyond traditional telecom operators.

Challenge Analysis

A major challenge in the Open RAN test equipment market is maintaining consistent performance across distributed and virtualized network environments. Open RAN systems operate across multiple layers, including cloud, edge, and physical infrastructure, making testing more complex. Ensuring stable performance across these layers requires advanced and continuously updated testing solutions.

Another challenge is the evolving nature of standards and specifications. Open RAN technologies are still developing, and frequent updates in protocols require constant adjustments in testing frameworks. Keeping pace with these changes while ensuring compatibility and accuracy remains a significant challenge for solution providers.

Competitive Analysis

The Open RAN Test Equipment Market is led by established test and measurement companies providing advanced validation and performance testing solutions. Keysight Technologies, VIAVI Solutions, Rohde & Schwarz, and Anritsu Corporation deliver high-precision tools for Open RAN compliance. Tektronix and National Instruments strengthen testing capabilities. These firms focus on 5G validation. Their solutions ensure interoperability and network reliability.

Network testing and performance solution providers play a key role in accelerating Open RAN deployment. Spirent Communications, EXFO Inc., and LitePoint offer solutions for performance benchmarking and protocol testing. CommScope and Radisys support Open RAN ecosystem integration. These companies enhance network efficiency. Their tools support faster rollout of next-generation networks.

Emerging and niche players contribute to innovation in Open RAN validation and optimization. Artiza Networks, Accuver, Polaris Networks, and Teradyne strengthen testing frameworks and automation. These companies focus on specialized testing requirements. Their solutions improve network performance and compliance. Other key players continue to expand capabilities. This competitive landscape supports steady growth in Open RAN technologies.

Top Key Players in the Market

- Keysight Technologies

- VIAVI Solutions

- Rohde & Schwarz

- Anritsu Corporation

- Spirent Communications

- EXFO Inc.

- LitePoint (Teradyne)

- National Instruments (NI)

- Tektronix

- Artiza Networks

- Accuver

- Polaris Networks

- CommScope

- Radisys

- Rohde & Schwarz

- Others

Recent Developments

- January, 2026 – Keysight expanded Open RAN Architect with end-to-end E2E testing suites covering O-RU, O-DU, and RIC components. Labs accelerated multi-vendor integration 40% via automated conformance campaigns.

- February, 2026 – VIAVI’s TM500 O-RU Tester validated Massive MIMO beamforming in OTA RF chambers. Field deployments cut fronthaul troubleshooting time 50% using T-BERD/MTS-5800 packet capture.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.3 Bn |

| Forecast Revenue (2035) | USD 10.8 Bn |

| CAGR (2026-2035) | 16.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Product Type (Radio Unit Test Equipment, Distributed Unit Test Equipment, Centralized Unit Test Equipment, Others), By Application (Network Performance Testing, Compliance Testing, Functional Testing, Others), By End-User (Telecom Operators, Network Equipment Manufacturers, Others), By Deployment Mode (Lab Testing, Field Testing) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Keysight Technologies, VIAVI Solutions, Rohde & Schwarz, Anritsu Corporation, Spirent Communications, EXFO Inc., LitePoint (Teradyne), National Instruments (NI), Tektronix, Artiza Networks, Accuver, Polaris Networks, CommScope, Radisys, Rohde & Schwarz, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |