Quick Navigation

Report Overview

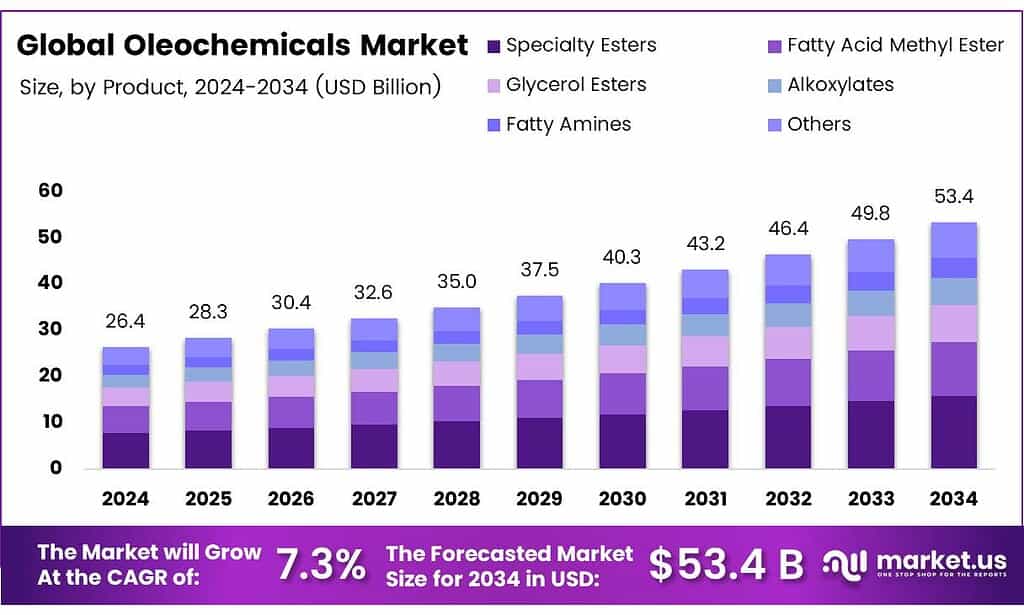

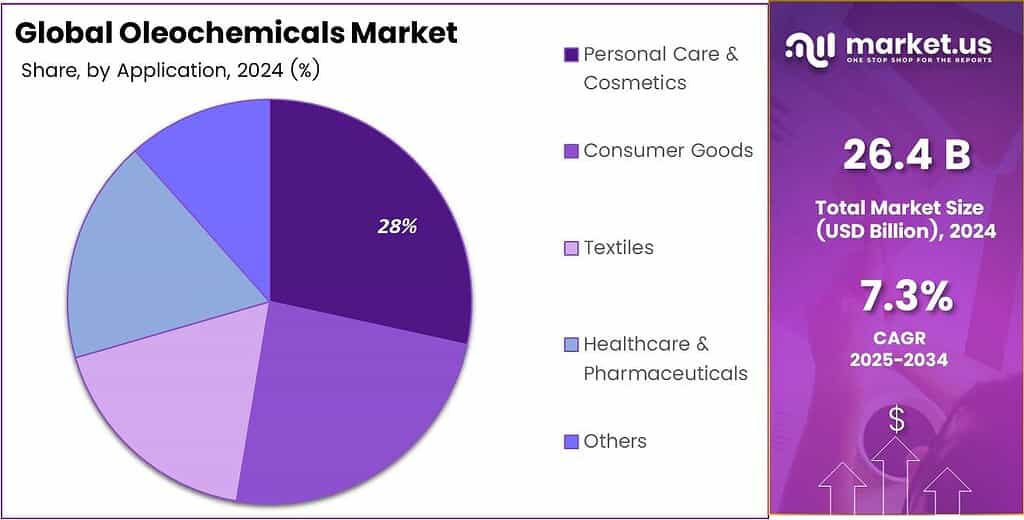

The Global Oleochemicals Market size is expected to be worth around USD 53.4 billion by 2034, from USD 26.4 billion in 2024, growing at a CAGR of 7.3% during the forecast period from 2025 to 2034.

Oleochemicals are aliphatic molecules derived from lipids, primarily vegetable oils and animal fats. They are widely used in transportation fuels, consumer products, and industrial applications. Common oleochemicals include surfactants and biodiesel, valued for their versatility. Their chemical properties, such as chain length and modifications, determine their specific uses. Long-chain fatty acids (C16-C18) are used in soaps, while medium-chain fatty acids (C8-C12) serve as herbicides and lubricant precursors.

Global vegetable oil production surged over 20%, driven by oleochemical demand. Most high-volume oils contain long-chain fatty acids (≥C16), making them abundant. Medium-chain lipids (C6-C14) are less common, except for dodecanoic acid found in coconut and palm kernel oils. Oleochemicals are cost-competitive with sugar feedstocks, emphasizing yield as a critical factor. Efficient production relies on optimizing microbial strains for high yields.

- Most oleochemicals, except triacylglycerols (TAGs), are not naturally produced in large quantities by microbes. Achieving industrially relevant titers with high yields (>90% of theoretical) is difficult. Natural microbes lack the metabolic pathways for such output, necessitating genetic engineering. Engineered strains of Y. lipolytica have achieved significant titers: 100 g/L TAGs, 10 g/L free fatty acids, and 2 g/L fatty alcohols. In contrast, unengineered E. coli and S. cerevisiae produce far lower yields, at 27 mg/L and 42.7 mg/L, respectively.

Lipase-catalyzed esterification for wax ester production consumes 34% less energy than chemical esterification. This method also generates less waste, improving sustainability. Chemical esterification relies on strong acids, which increase energy and environmental costs. Advances in microbial engineering have enabled up to 100-fold improvements in oleochemical titers. Ongoing research focuses on understanding lipogenesis to further enhance production efficiency.

The growing demand for oleochemicals drives innovation in microbial engineering and production processes. Optimizing strains for medium-chain lipid production remains a key challenge. Advances in metabolic engineering could unlock higher yields and new applications. Sustainable production methods, like lipase-catalyzed processes, are critical for reducing environmental impact. Continued research into lipogenesis will support the scalability of oleochemical industries.

Key Takeaways

- The Global Oleochemicals Market is projected to grow from USD 26.4 billion in 2024 to USD 53.4 billion by 2034, at a CAGR of 7.3%.

- Specialty Esters dominated the market in 2024, holding a 29.5% share due to their use in personal care, lubricants, and food processing.

- Personal Care and Cosmetics led application segments in 2024 with a 27.3% share, driven by demand for sustainable, plant-based ingredients.

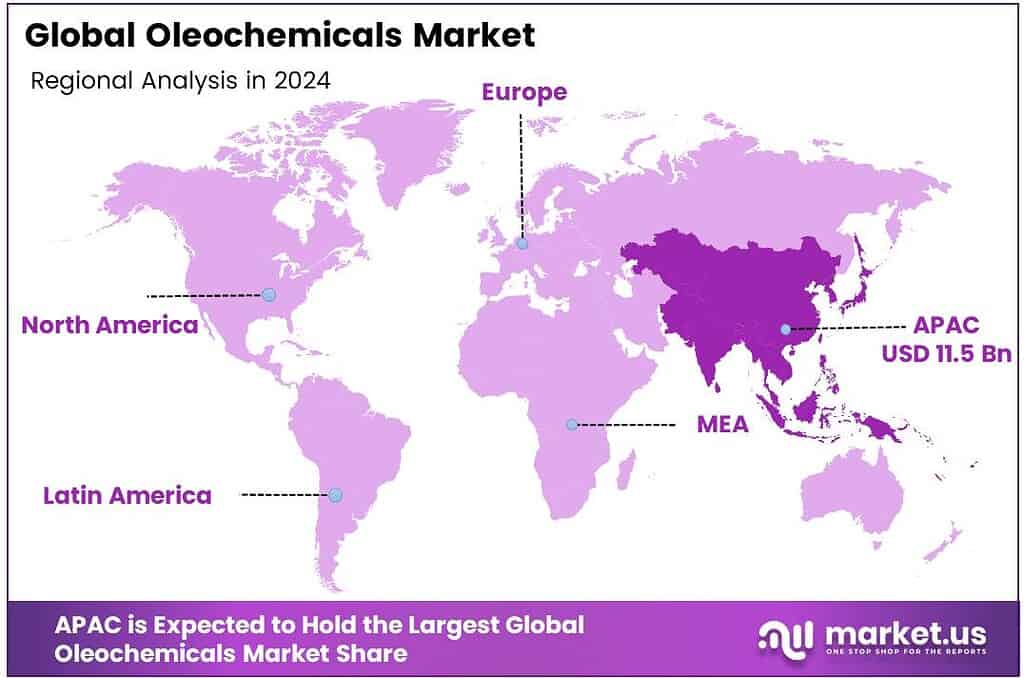

- The Asia-Pacific region held a 43.8% market share in 2024, valued at USD 11.5 billion, led by Malaysia, Indonesia, India, and China.

By Product

Specialty Esters Lead the Oleochemicals Market with 29.5% Share

In 2024, Specialty Esters held a dominant market position in the Oleochemicals Market, capturing more than a 29.5% share. These esters are widely used in personal care, lubricants, and food processing due to their high performance, biodegradability, and stable properties under extreme conditions.

The segment is largely supported by increasing demand for natural and sustainable ingredients in cosmetics and industrial lubricants. Companies across Europe and Asia-Pacific focused on formulating tailor-made esters derived from renewable feedstocks like palm and rapeseed oil, boosting market expansion. Specialty Esters continue to maintain their dominance as industries transition toward eco-friendly chemical substitutes.

The rise of bio-based lubricants, coupled with the growing adoption of green formulations in cosmetics and pharmaceuticals, further enhances the segment’s importance. This evolution positions Specialty Esters as a preferred choice for manufacturers aiming to balance performance with environmental responsibility, ensuring steady demand growth and reinforcing their leadership in the oleochemicals industry.

By Application

Personal Care and Cosmetics Dominate Oleochemicals Market with 27.3% Share

In 2024, Personal Care and Cosmetics held a dominant market position in the Oleochemicals Market, capturing more than a 27.3% share. The segment’s strong presence was driven by the rising use of plant-based and sustainable ingredients in skincare, haircare, and hygiene products.

Consumers increasingly preferred natural formulations over synthetic chemicals, pushing manufacturers to use oleochemicals such as fatty acids, glycerol, and esters derived from renewable oils. Companies also emphasized transparency and environmental responsibility, aligning with global sustainability goals and boosting oleochemical adoption in cosmetic formulations.

The Personal Care and Cosmetics segment continues to expand steadily, supported by clean beauty trends and growing demand for eco-certified ingredients. Major cosmetic brands are shifting toward biodegradable and non-toxic materials, strengthening the market’s focus on natural oleochemical derivatives. Innovations in emollients, surfactants, and specialty esters further enhance product texture and performance.

Key Market Segments

By Product

- Specialty Esters

- Fatty Acid Methyl Ester

- Glycerol Esters

- Alkoxylates

- Fatty Amines

- Others

By Application

- Personal Care and Cosmetics

- Consumer Goods

- Textiles

- Healthcare and Pharmaceuticals

- Others

Emerging Trends

Transition to Bio-based Feedstocks in the Oleochemicals Industry

One of the most significant emerging trends in the oleochemicals industry is the steady shift from conventional petrochemical feedstocks to bio-based and sustainably sourced oils and fats. This shift is not just a matter of marketing—it’s being driven by real regulatory changes and measurable progress in certified sustainable raw materials.

- The Roundtable on Sustainable Palm Oil (RSPO) reports that as of its 2024 Impact Report, the certified sustainable palm oil plantation area now spans 5.2 million hectares across 23 countries. At the same time, major chemical players such as BASF SE note that in 2024, they sourced 98.1% of their palm oil as RSPO-certified, and were able to trace 96.7% of their global palm footprint back to the oil mill level.

At the same time, regulatory frameworks are tightening. In the European Union, for instance, the revised Renewable Energy Directive II caps the contribution of biofuels from waste oils and fats (including used cooking oil) at 1.7% of transport-energy consumption, which forces industry players to look for more advanced feedstocks.

Drivers

Rising Demand for Sustainable and Biodegradable Products

The oleochemicals industry is experiencing an increasing demand for sustainable and biodegradable chemical alternatives. Simply put, manufacturers and consumers alike are pushing away from traditional petrochemical-derived materials and are embracing oleochemicals because they are derived from natural fats and oils, are often more eco-friendly, and support the broader goals of circular and green chemistry.

The market for oleochemicals is said to be growing because companies recognise that these substances from renewable feedstocks offer a lower carbon footprint, and because regulatory as well as consumer pressure is mounting. The demand for oil crops (the primary raw material for many oleochemicals) grew by 25% over five years, and the industry saw both opportunity and pressure to refine the sustainability story.

In India, for instance, the push for biofuels and renewable feedstocks is very strong, which indirectly benefits the oleochemicals industry because similar supply chains, oils, and fats are involved. One estimate says the programme to blend ethanol into petrol could reduce crude oil imports by nearly 86 million barrels annually and cut carbon dioxide emissions by about 10 million tonnes every year in India.

Restraints

Feed Stock Volatility and Supply Chain Challenges

A major restraint facing the oleochemicals industry is the ongoing challenge of securing stable, sustainable feedstocks and functioning supply chains. In particular, a heavy reliance on oils like palm oil and palm kernel oil creates vulnerability because supply disruptions or regulatory shifts can ripple through production and raise costs.

Swiss Re Corporate Solutions notes that more than 80% of the world’s palm oil production comes from just two countries — Malaysia and Indonesia. What this means is that any event—be it weather disruption, export curbs, labour issues, or disease outbreaks—in one of those regions can immediately tighten supply for the downstream oleochemical producers. Further, while palm and palm kernel oils are the backbone of many oleochemical processes.

- Henkel AG reports that in 2024, it was able to trace 95% of its palm and palm-kernel oil purchases back to the refinery level, 94% back to the oil mill, but only 65% back to the plantation. This gap underscores the complexity of the supply chain and the risk of non-compliance with upcoming regulations or certifications, which can delay product launch or limit which markets ingredients can serve.

Opportunity

Growing Demand for Bio-based and Renewable Feedstocks

One of the strongest growth drivers for the oleochemicals industry is the rising demand for bio-based and renewable feedstocks, which helps manufacturers meet sustainability goals and regulatory requirements. The Roundtable on Sustainable Palm Oil (RSPO) reported that in 2024 its members produced 16.2 million metric tons of Certified Sustainable Palm Oil (CSPO), equivalent to about 20.1% of their total palm oil output.

This increase reflects growing pressure from both consumers and brand-owners to switch to responsibly sourced oils. At the same time, leading feedstock suppliers are investing in supply-chain sustainability. For instance, Cargill’s 2024 impact report notes that they engage 26,400 small-holder farmers across 51,500 hectares of land in their palm oil supply chain, helping build a more resilient and renewable raw-material base.

Governments and regulatory programmes are also working to support this shift. The European Union’s revised renewable energy and deforestation-regulation frameworks push for traceable, low-carbon feedstocks in chemicals and fuels, effectively boosting demand for oleochemicals derived from renewable oils. See discussion of traceability in RSPO commentary.

Regional Analysis

Asia-Pacific leads with a 43.8% share and a USD 11.5 Billion market value.

In 2024, the Asia-Pacific region held a dominant position in the global oleochemicals market, capturing a 43.8% share, valued at around USD 11.5 billion. This leadership stems from its strong production base, abundant natural resources, and expanding industrial network. Countries like Malaysia, Indonesia, India, and China serve as major hubs for palm oil and coconut oil, the primary feedstocks for oleochemical production.

The region’s well-established refining and downstream processing industries also contribute significantly to cost efficiency and global supply reliability. The Asia-Pacific market continues to expand due to rising demand for bio-based products across personal care, food, pharmaceuticals, and lubricants. Government initiatives supporting renewable materials and low-carbon production are reinforcing this growth.

Malaysia’s National Agri-Commodity Policy and India’s Biofuel Policy 2025 encourage the sustainable use of vegetable oils for high-value derivatives, including fatty acids, glycerine, and esters. Additionally, regional manufacturers are investing in advanced processing technologies and certification programs to meet international sustainability standards such as RSPO and ISCC.

Rapid industrialization, urban population growth, and the shift toward green chemistry are further driving the oleochemicals market in Asia-Pacific. With strong export capabilities, expanding domestic consumption, and increasing global preference for eco-friendly ingredients, the region remains the largest and most dynamic contributor to the global oleochemicals landscape, setting the benchmark for future industry expansion.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Emery Oleochemicals strength lies in its extensive portfolio of oleochemical derivatives, including biodegradable lubricants, polymer additives, and agrochemical solutions. The company focuses on innovation and sustainability, catering to industries seeking environmentally friendly alternatives to petroleum-based products. Its strategic focus on R&D and custom solutions solidifies its position as a key technical partner in the global oleochemicals market, driving the bio-economy forward.

Evonik Industries AG is a dominant force in the oleochemicals market, particularly through its expertise in derivatives like fatty alcohols and methyl esters. The company leverages its strong R&D capabilities to produce high-value ingredients for cosmetics, detergents, and plastics. Evonik’s strategy emphasizes sustainability and creating innovative, performance-driven solutions for its customers.

Wilmar International Ltd. is a vertically integrated powerhouse in the oleochemicals market. Its unparalleled strength is its massive, integrated production of palm and oilseed-based raw materials. This control over the entire supply chain, from plantations to refineries, ensures cost efficiency and a consistent supply of feedstocks. Wilmar primarily focuses on basic oleochemicals like fatty acids and glycerine, supplying bulk quantities globally and making it a foundational and influential player in the industry’s landscape.

Top Key Players in the Market

- Emery Oleochemicals

- Evonik Industries AG

- Wilmar International Ltd.

- Kao Chemicals Global

- Ecogreen Oleochemicals

- Corbion N.V

- Cargill, Incorporated

- Oleon NV

- Godrej Industries

- IOI Corporation Berhad

- KLK OLEO

Recent Developments

- In 2024, Emery achieved ISO 50001 Energy Management Systems certification for its Cincinnati plant, alongside an Award for Excellence in Environmental Performance from the Ohio Chemistry Technology Council at its 36th Annual Conference. Emery added four pelargonic acid products to its 100% USDA BioPreferred certified biobased portfolio.

- In 2024, Evonik expanded sodium methylate production in Rosario, Argentina, to support rising biodiesel demand, aligning with Brazil’s B15 blending mandate. It launched the Purocel series for purifying pyrolysis oil from plastics, enhancing circular economy applications for oleochemical feedstocks.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 26.4 Billion |

| Forecast Revenue (2034) | USD 53.4 Billion |

| CAGR (2025-2034) | 7.3% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Specialty Esters, Fatty Acid Methyl Ester, Glycerol Esters, Alkoxylates, Fatty Amines, Others), By Application (Personal Care and Cosmetics, Consumer Goods, Textiles, Healthcare and Pharmaceuticals, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Emery Oleochemicals, Evonik Industries AG, Wilmar International Ltd., Kao Chemicals Global, Ecogreen Oleochemicals, Corbion N.V, Cargill, Incorporated, Oleon NV, Godrej Industries, IOI Corporation Berhad, KLK OLEO |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |