Global Okra Seed Market Size, Share, And Industry Analysis Report By Seed Type (Hybrid Seeds, Open-Pollinated Seeds, Heirloom Seeds), By Seed Form (Untreated, Treated), By Growth Method (Conventional Farming, Organic Farming, Hydroponics), By Application (Commercial Cultivation, Home Gardening, Research and Development, Organic Farming), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: February 2026

- Report ID: 178378

- Number of Pages: 371

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

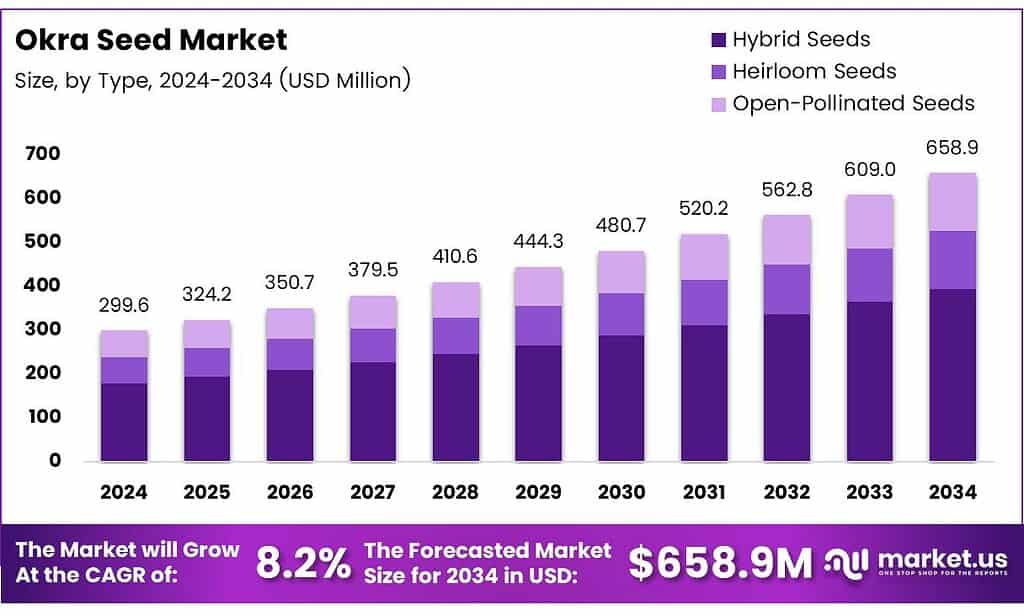

The Global Okra Seed Market size is expected to be worth around USD 658.9 million by 2034 from USD 299.6 million in 2024, growing at a CAGR of 8.2% during the forecast period 2025 to 2034.

The okra seed market covers the commercial production, distribution, and sale of seeds used to cultivate okra crops. These seeds serve commercial farmers, home gardeners, and research institutions globally. Demand spans both tropical and subtropical regions, where okra grows as a staple vegetable crop.

Okra, also known as lady’s finger, holds strong nutritional value. Farmers and food producers increasingly adopt it for its fiber, vitamins, and antioxidant content. Moreover, food processing industries source okra for value-added products, further widening the market base for quality seed varieties.

- Rising health awareness is boosting demand for okra, known for its gut health and anti-diabetic benefits, which increases pressure on seed producers to supply premium planting material. Okra seeds contain about 40% oil rich in oleic and linoleic acids, making them a potential edible oil source, while certain pretreatments can alter their nutrient profile.

Hybrid seed development drives significant transformation across this market. Seed companies invest heavily in developing disease-resistant, high-yield cultivars. Consequently, commercial growers shift away from traditional open-pollinated seeds toward premium hybrid options that deliver consistent performance across diverse agro-climatic zones.

Protected cultivation and urban farming further expand addressable demand. Greenhouse operators and rooftop farming practitioners require specialized seed types suited to controlled environments. However, the fragmented supply chain and limited cold-chain infrastructure in developing regions continue to create distribution challenges for premium seed manufacturers.

Key Takeaways

- The Global Okra Seed Market is valued at USD 299.6 million in 2024 and is projected to reach USD 658.9 million by 2034, at a CAGR of 8.2% during the forecast period 2025–2034.

- Hybrid Seeds dominate the market with a 59.1% share in 2025.

- Untreated Seeds hold the largest share at 67.2%.

- Conventional Farming leads with a 65.3% share.

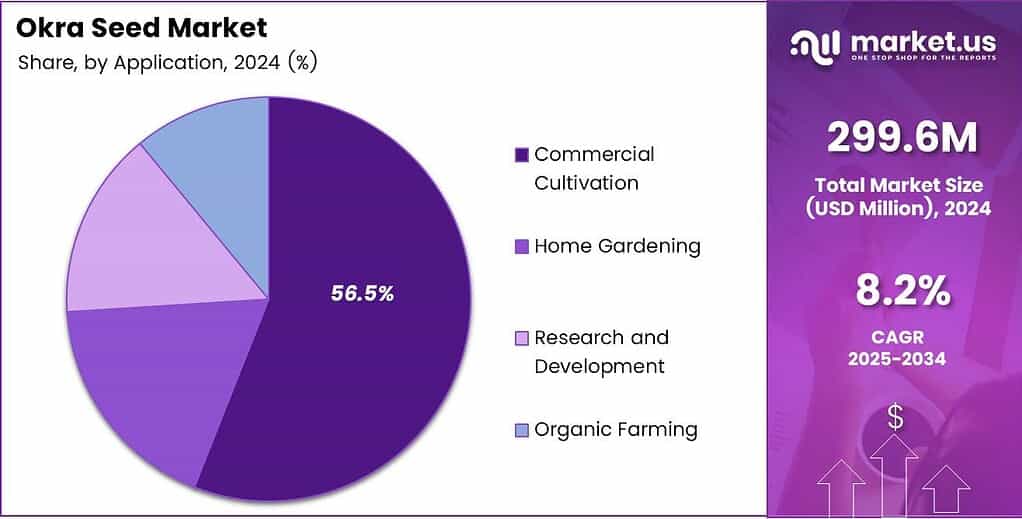

- Commercial Cultivation accounts for the largest share at 56.5%.

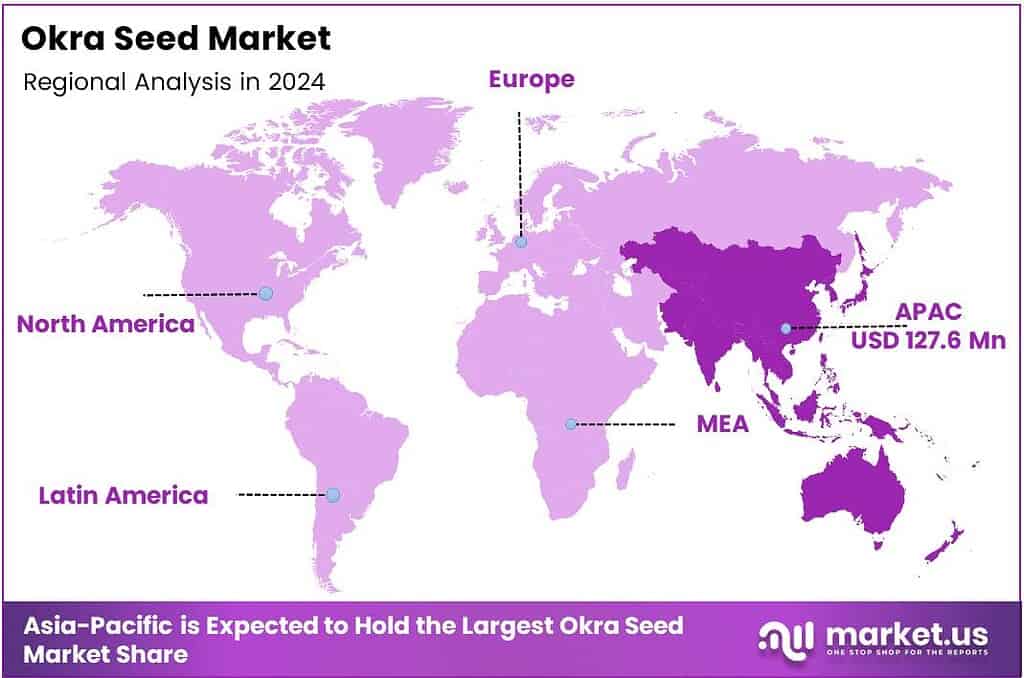

- Asia Pacific dominates regionally with a 42.6% market share, valued at USD 127.6 million.

By Seed Type Analysis

Hybrid Seeds dominate with 59.1% due to superior yield performance and disease resistance.

In 2025, Hybrid Seeds held a dominant market position in the By Seed Type segment of the Okra Seed Market, with a 59.1% share. Commercial growers prefer hybrid varieties because they deliver consistent yields, improved disease resistance, and better adaptation to variable climate conditions. Moreover, government-backed programs increasingly promote hybrid adoption among smallholder farmers to raise productivity.

Open-Pollinated Seeds continue to serve a significant segment of the market, particularly among smallholder and subsistence farmers. These seeds offer cost advantages and allow farmers to save seeds across seasons. However, their lower yield performance compared to hybrids gradually limits their market share as awareness of premium seed benefits grows.

Heirloom Seeds attract niche growers focused on heritage varieties, biodiversity conservation, and organic farming practices. Specialty food producers and research institutions drive demand for these traditional cultivars. Additionally, growing consumer interest in non-GMO and authentically sourced food products supports the continued relevance of heirloom okra varieties in premium markets.

By Seed Form Analysis

Untreated Seeds dominate with 67.2% due to cost-effectiveness and wide farmer acceptance.

In 2025, Untreated Seeds held a dominant market position in the By Seed Form segment of the Okra Seed Market, with a 67.2% share. Smallholder and conventional farmers widely prefer untreated seeds for their lower upfront cost and familiar handling. Moreover, in regions with limited access to agrochemical inputs, untreated seeds remain the default and practical choice for most growers.

Treated Seeds represent a fast-growing sub-segment driven by precision agriculture and commercial farming expansion. Seed treatment technologies, including fungicide and biological coatings, improve germination rates and early-stage crop health. Consequently, large-scale commercial producers increasingly adopt treated seeds to reduce crop losses and improve return on investment across intensive cultivation systems.

By Growth Method Analysis

Conventional Farming dominates with 65.3% due to established infrastructure and scale advantages.

In 2025, Conventional Farming held a dominant market position in the By Growth Method segment of the Okra Seed Market, with a 65.3% share. Traditional field cultivation remains the primary method for okra production across Asia, Africa, and Latin America. Farmers rely on established agronomic practices, and seed companies tailor product portfolios to support conventional growing systems at scale.

Organic Farming gains strong momentum as consumer demand for chemical-free produce rises globally. Certified organic okra commands price premiums in export markets, incentivizing farmers to transition. Additionally, several governments now offer subsidy programs and certification support to accelerate organic conversion among small and medium-scale okra producers.

Hydroponics represents an emerging and high-potential growth method within the okra seed market. Urban growers and controlled-environment agriculture operators adopt hydroponic systems to produce okra year-round. Therefore, seed companies develop specialized cultivars compatible with soilless growing environments, opening a distinct and premium product category within this segment.

By Application Analysis

Commercial Cultivation dominates with 56.5% due to large-scale demand from food processing and export sectors.

In 2025, Commercial Cultivation held a dominant market position in the By Application segment of the Okra Seed Market, with a 56.5% share. Export-oriented farming operations and food processing companies drive bulk seed procurement. Moreover, organized retail and supermarket supply chains require consistent okra quality, pushing commercial growers toward high-performance hybrid seed varieties.

Home Gardening emerges as a significant and rapidly growing application segment. Urban households and health-conscious consumers grow okra in kitchen gardens, raised beds, and container setups. Consequently, seed retailers and e-commerce platforms report rising demand for small, affordable okra seed packs suited to backyard and balcony cultivation.

Research and Development applications support the long-term innovation pipeline within the okra seed industry. Universities, public research institutes, and private breeding programs source diverse okra germplasm for varietal improvement. Additionally, Organic Farming as an application captures growers who require certified organic, untreated seed inputs specifically compliant with organic production standards and export certifications.

Key Market Segments

By Seed Type

- Hybrid Seeds

- Open-Pollinated Seeds

- Heirloom Seeds

By Seed Form

- Untreated

- Treated

By Growth Method

- Conventional Farming

- Organic Farming

- Hydroponics

By Application

- Commercial Cultivation

- Home Gardening

- Research and Development

- Organic Farming

Emerging Trends

Precision Breeding, Digital Platforms, and Urban Farming Reshape the Okra Seed Industry

Urban home gardening and rooftop farming movements strongly accelerate demand for specialty okra seed varieties. Consumers in tier-1 cities across Asia and Europe now cultivate okra in compact spaces. Consequently, seed producers develop compact, fast-maturing cultivars specifically tailored for container and small-plot urban farming applications.

- Seed companies rapidly integrate precision biological coatings and advanced treatment technologies into their okra seed product lines. These coatings enhance germination rates and early-crop resistance to soil-borne pathogens. Thailand’s okra export price reached USD 1,470 per metric ton in September 2025, reflecting how premium quality cultivation drives stronger price realization across global supply chains.

Digital agri-marketplaces and mobile apps transform how farmers discover and purchase okra seeds. E-commerce platforms now deliver premium seed varieties directly to rural doorsteps, bypassing traditional distribution intermediaries. Additionally, marker-assisted genomic breeding programs advance the development of climate-resilient, high-shelf-life okra varieties that better serve both tropical and temperate growing conditions.

Drivers

Hybrid Seed Adoption, Protected Cultivation, and Health Awareness Accelerate Okra Seed Market Growth

Commercial growers across Asia and Africa accelerate their shift to high-yielding, disease-resistant hybrid okra varieties. These cultivars deliver superior productivity per hectare and reduce crop loss from common viral and fungal threats. Moreover, organized agribusiness operations increasingly standardize on hybrid seed inputs to meet food processor and export market quality specifications consistently.

Protected cultivation systems, including greenhouses and polyhouses, enable year-round okra production in regions with seasonal limitations. Operators of these facilities create stable, high-volume demand for quality seed inputs. Consequently, seed companies develop purpose-built varieties optimized for controlled-environment performance, creating a new premium product tier within the broader okra seed category.

Government-backed seed replacement programs actively lower barriers for smallholder farmers to access certified, improved okra varieties. Subsidized seed distribution schemes operate across India, Nigeria, and other major producing nations. Additionally, rising global awareness of okra’s nutritional benefits fuels consumer demand, which in turn motivates farmers to plant more and procure better-quality seed inputs.

Restraints

High Hybrid Seed Costs and Climate Vulnerabilities Constrain Broader Market Penetration

Premium hybrid okra seed prices remain a significant barrier for small-scale producers in developing economies. Many smallholder farmers operate on thin margins and cannot justify the higher per-unit cost of hybrid varieties. Consequently, a large portion of the global farming base continues to rely on saved open-pollinated or low-quality informal seed sources despite available alternatives.

- Climatic vulnerabilities create persistent disruptions across the okra seed supply chain. Irregular rainfall, drought periods, and rising temperatures damage both seed production crops and commercial okra cultivation. China’s okra export price declined by 41% year-on-year to USD 843 per metric ton in September 2025, illustrating how supply shocks and climate-driven output fluctuations can severely compress price realization for producers.

Viral disease outbreaks, including Yellow Vein Mosaic Virus, periodically devastate okra crops across major growing regions. These outbreaks reduce seed demand in affected areas and erode farmer confidence in new variety adoption. Therefore, seed companies face ongoing pressure to accelerate breeding programs that deliver durable viral resistance traits in commercially viable okra cultivars.

Growth Factors

Organic Segments, Digital Commerce, and Dual-Purpose Cultivars Open New Revenue Pathways

Organic and non-GMO okra seed segments expand rapidly as health-focused buyers prioritize clean-label produce. Specialty retailers, organic food chains, and export markets pay significant premiums for certified organic okra. Moreover, seed producers who establish organic-compliant seed lines position themselves to capture a high-margin, fast-growing buyer segment across North America, Europe, and premium Asian markets.

Digital e-commerce platforms now enable seed companies to deliver premium okra seed varieties directly to farmers and home gardeners. Mobile-first agri-marketplaces reduce distribution costs and eliminate layers of intermediaries. Consequently, smaller and regional seed producers gain market access they previously lacked, expanding overall market participation and intensifying competitive innovation across the value chain.

Development of dual-purpose okra cultivars, valued for both vegetable pod production and nutraceutical oil extraction, unlocks new revenue streams for growers. Additionally, strategic breeding programs target temperate regions through climate-adaptive localized varieties. These efforts expand the geographic footprint of okra cultivation beyond traditional tropical zones, adding new national markets to the global demand base.

Regional Analysis

Asia Pacific Dominates the Okra Seed Market with a Market Share of 42.6%, Valued at USD 127.6 Million

Asia Pacific leads the global okra seed market with a 42.6% share, valued at USD 127.6 million in 2024. India, China, and Southeast Asian nations together drive this dominance through large-scale commercial cultivation and strong domestic consumption.

North America represents a growing market for specialty and organic okra seed varieties. Rising multicultural food preferences and health-conscious consumer behavior in the US drive retail and foodservice demand for fresh okra. Additionally, urban farming initiatives and farm-to-table movements create sustained demand for premium seed inputs among small-scale and specialty growers.

Europe shows increasing interest in okra, driven by immigrant communities and the broader expansion of ethnic food retail channels. The UK, France, and Germany lead import demand for fresh okra, which creates downstream interest in quality seed production. Furthermore, strict EU regulations on seed certification and GMO restrictions shape product development strategies for seed companies operating in this region.

Latin America presents strong growth potential, particularly in Brazil, where okra holds deep cultural and culinary significance. Smallholder farming communities across the region cultivate okra as both a subsistence and cash crop. Consequently, national seed programs and agronomic extension services actively promote improved hybrid varieties to raise productivity and reduce post-harvest losses among rural farming communities.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

UPL Limited brings scale and reach to okra seed distribution through its strong agri-input channels, helping varieties move quickly from breeders to smallholders. UPL’s advantage is bundling: seeds supported by crop protection advice and dealer networks. This improves adoption and repeat purchase, especially in price-sensitive regions. It also benefits from export-oriented supply chains and compliance capabilities.

Syngenta Group tends to compete on hybrid performance, uniformity, and field support, which matters for okra growers targeting fresh markets and processors. Syngenta’s trial infrastructure and agronomy teams translate local disease pressure into product positioning. Its brand trust helps premium pricing, while partnerships with distributors extend coverage into emerging vegetable belts, ensuring a consistent seasonal supply.

Bayer AG influences the okra seed landscape through R&D depth, quality standards, and a strong focus on integrated pest and disease solutions. Bayer’s strength is data-led product development and stewardship programs that protect farmer outcomes and brand reputation. Where it participates, it often targets higher-margin segments that reward reliability, shelf-life, and exportable grade at scale.

Sakata Seed Corporation is widely associated with vegetable seed specialization, and okra fits its portfolio strategy of dependable horticulture genetics. Sakata’s emphasis on stable germination, uniform pods, and traits aligned with retail presentation. Its global breeding footprint supports region-specific lines, while careful seed quality control reduces variability for professional growers and contract farming programs across seasons and geographies.

Top Key Players in the Market

- UPL Limited

- Syngenta Group

- Bayer AG

- Sakata Seed Corporation

- East-West Seed Group

- NR Seeds Pvt. Ltd.

- Nuziveedu Seeds Limited

- Limagrain

- Enza Zaden

- BASF AG

- Takii & Co., Ltd.

Recent Developments

- 2026 – Advanta Enterprises Ltd. contributed under India’s Access and Benefit-Sharing (ABS) framework to the National Biodiversity Authority for the commercial use of biological resources, including okra. This contribution specifically supported the development of improved and hybrid okra seed varieties, reinforcing India’s regulatory commitment to biodiversity-linked seed commercialization.

- 2025 – Sakata Seed Corporation launched the Niger F1 okra variety at Seed Connect Africa, targeting Nigerian and broader African market conditions. The variety features an extended harvesting season and improved yield performance, demonstrating Sakata’s strategic focus on developing Africa-specific okra cultivars for emerging regional seed markets.

Report Scope

Report Features Description Market Value (2024) USD 299.6 Million Forecast Revenue (2034) USD 658.9 Million CAGR (2025-2034) 8.2% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Seed Type (Hybrid Seeds, Open-Pollinated Seeds, Heirloom Seeds), By Seed Form (Untreated, Treated), By Growth Method (Conventional Farming, Organic Farming, Hydroponics), By Application (Commercial Cultivation, Home Gardening, Research and Development, Organic Farming) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape UPL Limited, Syngenta Group, Bayer AG, Sakata Seed Corporation, East-West Seed Group, NR Seeds Pvt. Ltd., Nuziveedu Seeds Limited, Limagrain, Enza Zaden, BASF AG, Takii & Co., Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- UPL Limited

- Syngenta Group

- Bayer AG

- Sakata Seed Corporation

- East-West Seed Group

- NR Seeds Pvt. Ltd.

- Nuziveedu Seeds Limited

- Limagrain

- Enza Zaden

- BASF AG

- Takii & Co., Ltd.

Our Clients

- 178378

- February 2026