Global Marine Grease Market Size, Share, And Industry Analysis Report By Thickeners (Metallic Soap Thickener, Non-soap Thickener), By Product Type (Synthetic, Mineral Based, Bio-Based), By Ship Type (Bulk Carrier and Cargo Ships, Passenger Ships, Tankers, Cruise and Ferries, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 179972

- Number of Pages: 282

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

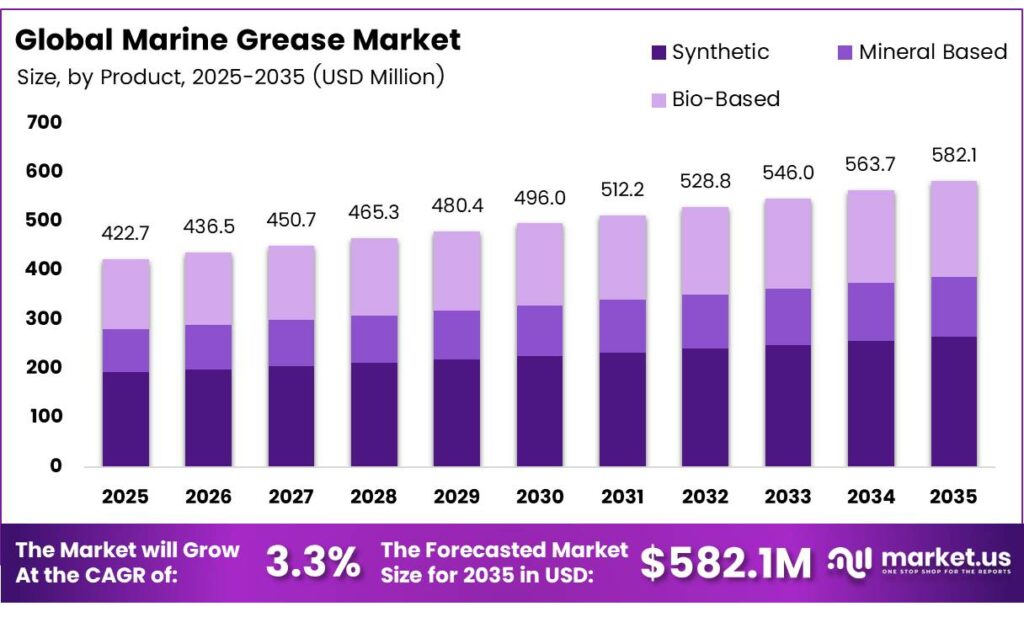

The Global Marine Grease Market size is expected to be worth around USD 582.1 million by 2035 from USD 422.7 million in 2025, growing at a CAGR of 3.3% during the forecast period 2026 to 2035.

Marine grease is a specialized lubricant that protects ship components from saltwater corrosion and heavy mechanical loads. It ensures smooth operation of deck machinery, steering gears, and underwater equipment in harsh marine conditions. Manufacturers formulate these greases to withstand high pressure and water washout.

Global seaborne trade expansion drives demand for reliable marine lubrication solutions. Moreover, increasing offshore oil and gas exploration activities require extreme-pressure greases for subsea equipment. Consequently, ship operators prioritize high-performance lubricants to reduce maintenance costs and extend vessel service life.

- Global grease production has averaged just over 1.14 billion kilograms per year over the past decade. Production recovered to 1.14 billion kilograms after a COVID-19-related dip. This recovery signals resilient demand from end-use industries, including maritime transport and shipbuilding sectors worldwide.

- China dominates global grease manufacturing, representing 38.1% of total reported grease production. The country produces more grease than Europe and North America combined, although Chinese grease output decreased 2.7% in the latest year. This production leadership positions Asia Pacific as the primary supply hub for marine greases globally.

Asia Pacific dominates the marine grease market with significant shipbuilding activities and port modernization projects. Additionally, naval defense fleet modernization programs in various countries boost product demand. Government investments in maritime infrastructure further support market growth across developing economies.

Key Takeaways

- The Global Marine Grease Market will reach USD 582.1 million by 2035 from USD 422.7 million in 2025, growing at a 3.3% CAGR from 2025 to 2035.

- Metallic Soap Thickener leads the thickeners segment with 57.8% market share.

- Synthetic grease dominates the product type segment, holding 48.2% of the market.

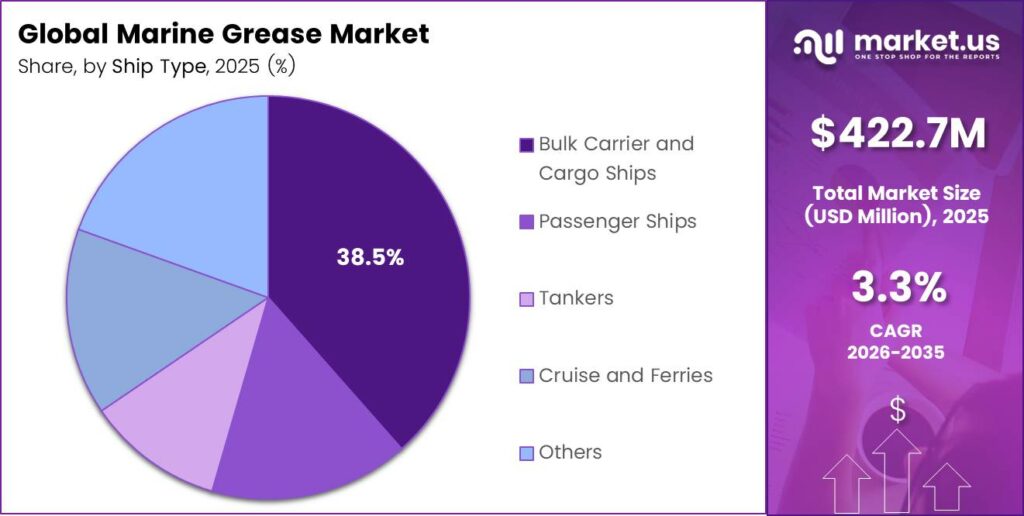

- Bulk carriers and Cargo Ships represent the largest ship type segment with 38.5% share.

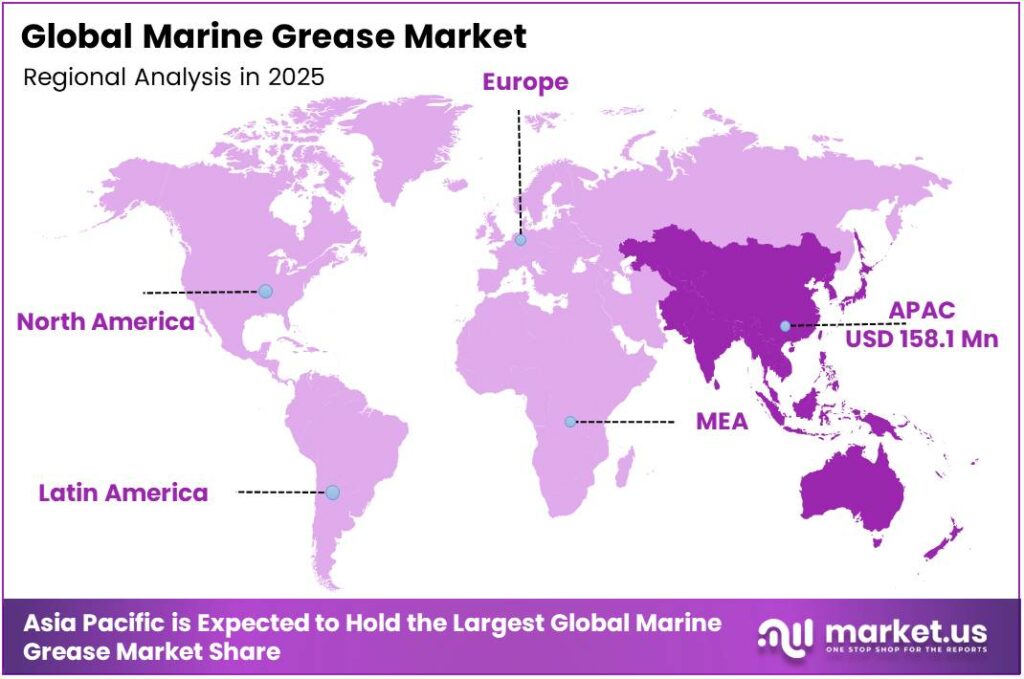

- Asia Pacific dominates with 37.4% market share, valued at USD 158.1 million in 2025.

By Thickeners Analysis

Metallic Soap Thickener dominates with 57.8% due to its cost-effectiveness and reliable performance in standard marine applications.

In 2025, Metallic Soap Thickener held a dominant market position in the By Thickeners segment of the Marine Grease Market, with a 57.8% share. Lithium-based greases within this category offer excellent water resistance and mechanical stability for general deck machinery. Moreover, calcium and sodium variants provide affordable solutions for less demanding onboard applications. Ship operators prefer these thickeners for routine maintenance schedules.

Lithium greases represent the most widely used metallic soap thickener due to their multi-purpose capabilities. They perform effectively across wide temperature ranges and resist saltwater corrosion. Additionally, aluminum-based thickeners offer smooth texture and good adhesion properties for specific equipment. These characteristics make metallic soaps the industry standard for conventional marine lubrication needs.

Non-soap Thickener formulations gain traction in specialized high-temperature and extreme-pressure applications. Inorganic thickeners like clay and silica provide superior performance where conventional soaps fail. They maintain consistency at high operating temperatures encountered in engine rooms and stern tubes. Consequently, manufacturers develop hybrid formulations combining soap and non-soap technologies for advanced protection.

By Product Type Analysis

Synthetic product type dominates with 48.2% due to superior performance in extreme marine conditions and longer service intervals.

In 2025, Synthetic held a dominant market position in the By Product Type segment of the Marine Grease Market, with a 48.2% share. These advanced formulations use chemically engineered base oils that resist breakdown under high pressure and temperature. They provide exceptional protection for critical equipment like thrusters and winches. Ship operators increasingly adopt synthetic greases to extend maintenance intervals and reduce lifecycle costs.

Mineral-based greases continue serving conventional marine applications where budget constraints outweigh performance requirements. They offer adequate lubrication for non-critical components under normal operating conditions. However, their lower resistance to water washout and temperature extremes limits the application scope. Many smaller vessels still rely on mineral-based products for routine maintenance needs.

Bio-Based greases emerge as environmentally responsible alternatives for vessels operating in ecologically sensitive waters. They biodegrade rapidly if accidental discharges occur, reducing marine pollution risks. Regulatory pressures and green shipping initiatives drive adoption in specific regions. Moreover, performance improvements in bio-based formulations expand their applicability beyond niche environmental applications.

By Ship Type Analysis

Bulk carriers and Cargo Ships dominate with 38.5% due to the sheer volume of global dry bulk trade and large vessel fleets.

In 2025, Bulk Carriers and Cargo Ships held a dominant market position in the By Ship Type segment of the Marine Grease Market, with a 38.5% share. These vessels operate continuously on major trade routes requiring regular lubrication maintenance. Their deck cranes, hatch covers, and steering systems demand consistent grease application. Moreover, fleet expansion in emerging economies sustains high demand from this segment.

Passenger Ships including ferries and cruise vessels, require specialized greases for passenger comfort equipment and safety systems. Stabilizers, propulsion units, and door mechanisms need reliable lubrication for uninterrupted operation. These vessels operate on strict schedules with minimal downtime for maintenance. Consequently, operators demand high-performance greases that ensure reliability between port calls.

Tankers transporting oil and chemicals require grease formulations resistant to cargo contamination and washout. Pump rooms, cargo handling equipment, and valve systems operate in potentially hazardous environments. Additionally, the Cruise and Ferries segment demands food-grade lubricants for galleys and public area equipment. The other category includes specialized vessels like dredgers and offshore supply ships with unique lubrication requirements.

Key Market Segments

By Thickeners

- Metallic Soap Thickener

- Lithium

- Calcium

- Sodium

- Aluminum

- Others

- Non-soap Thickener

- Inorganic

- Clay

- Silica

- Others

By Product Type

- Synthetic

- Mineral Based

- Bio-Based

By Ship Type

- Bulk Carrier and Cargo Ships

- Passenger Ships

- Tankers

- Cruise and Ferries

- Others

Emerging Trends

Shift Toward Calcium Sulfonate Complex Greases Offering Superior Water Resistance and Long Service Intervals

Calcium sulfonate complex greases gain preference for marine applications requiring exceptional water resistance. These formulations withstand direct seawater contact without emulsifying or losing protective properties. Ship operators appreciate their ability to protect equipment during harsh weather operations. Moreover, their extended service intervals reduce overall maintenance frequency and costs.

Integration of nanotechnology-enhanced additives provides superior corrosion protection in extreme marine conditions. Nanoparticles fill microscopic surface irregularities, creating durable protective barriers against saltwater. These advanced additives significantly extend equipment life in continuously wet environments. Additionally, they improve load-carrying capacity for heavy-duty applications like deck cranes and winches.

Adoption of digital IoT-based predictive maintenance systems enables real-time grease performance monitoring. Sensors track lubrication conditions and alert crews before equipment failures occur. This technology optimizes grease application schedules based on actual operating conditions. Consequently, vessels achieve higher operational reliability while reducing unnecessary grease consumption and waste.

Drivers

Booming Global Seaborne Trade Driven by Expanding Maritime Routes and International Commerce

Global seaborne trade volumes continue expanding as international commerce grows across all regions. Container shipping networks connect manufacturing hubs with consumer markets worldwide. At the world’s largest bunker hub in Singapore, marine fuel sales totaled 54.92 million metric tons in 2024, surpassing the previous annual record of 51.82 million metric tons set in 2023. This trade growth directly increases demand for marine greases across all vessel types.

Escalating offshore oil and gas exploration activities require extreme-pressure lubrication solutions for subsea equipment. Drilling rigs, production platforms, and support vessels operate in challenging marine environments. These applications demand specialized greases that maintain performance under high pressure and water exposure. Moreover, deepwater exploration pushes the need for advanced lubrication technologies.

Surge in naval defense fleets and recreational boating activities worldwide expands the marine grease customer base. Navies modernize aging fleets while emerging economies acquire new vessels for maritime security. Recreational boating continues to grow, particularly in North America and Europe. This diverse demand across military, commercial, and leisure segments ensures market stability.

Restraints

Volatility in Raw Material Prices Causes Fluctuations in Production and Procurement Costs

Raw material price volatility creates significant challenges for marine grease manufacturers and their customers. Base oil prices fluctuate with crude oil markets, while thickener costs vary with metal prices. These uncertainties make long-term contracting difficult for both producers and ship operators.

- Sudden price increases squeeze profit margins across the supply chain. Europe represents 18.7% of global grease production in the NLGI survey, with European grease production increasing steadily at a compound annual growth rate of +1.8% over the last 11 years despite regulatory challenges.

Stringent regulatory pressures on environmental footprint and marine pollution risks constrain formulation options. Regulations restrict certain additive chemistries that previously enhanced grease performance. Manufacturers must invest in research to develop compliant alternatives meeting performance standards.

Growth Factors

Development of Bio-Based and Biodegradable Environmentally Acceptable Lubricants for Regulatory Compliance

Bio-based marine greases represent a significant growth opportunity as environmental regulations tighten globally. Ship operators in ecologically sensitive areas increasingly adopt biodegradable lubricants. TotalEnergies Marine Fuels supplied a 700-metric-ton cargo of 100% used-cooking-oil-based B100 marine biofuel in Singapore in August 2024. The company estimated that annual marine biofuel demand in Singapore could reach nearly 1 million metric tons by 2025, indicating strong growth potential for bio-based lubricants.

Expansion of e-commerce fueled international container shipping drives demand for marine greases. Port modernization projects worldwide aim to accommodate larger container vessels with greater efficiency. These modern ports require advanced lubrication solutions for new handling equipment. Consequently, grease manufacturers develop specialized products for automated container terminals.

Technological innovations in synthetic hybrid thickeners enable better performance for deep-sea and high-load applications. The Asia-Pacific region accounts for more than 50% of global marine lubricants sales in the Lubmarine business. Their dedicated blending plant in Tuas, Singapore, has a marine and industrial lubricant production capacity of 310,000 metric tons per year, supporting regional growth.

Regional Analysis

Asia Pacific Dominates the Marine Grease Market with a Market Share of 37.4%, Valued at USD 158.1 Million

Asia Pacific holds the largest share of the marine grease market, accounting for 37.4% with a value of USD 158.1 million. This dominance is attributed to the region’s position as a global hub for shipbuilding and repair activities, particularly in countries like China, Japan, and South Korea, alongside increasing maritime trade volumes.

Europe represents a significant market for marine grease, driven by a strong presence of established shipping companies and a dense network of ports. The region’s focus on high-performance, environmentally acceptable lubricants for operations in environmentally sensitive areas like the Baltic and North Seas shapes market demand.

The North American market is characterized by steady demand from its robust commercial fishing industry, extensive inland waterway system, and naval defense operations. Stringent environmental regulations regarding lubricant biodegradability and toxicity continue to influence product development and adoption across the United States and Canada.

The Middle East and Africa region is experiencing growth supported by its strategic location for global oil shipments and expanding port infrastructure. Demand is primarily driven by the need for high-temperature resistant greases for vessels operating in the region’s warm climates and for the maintenance of port equipment.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BP p.l.c. continues to leverage its extensive global supply network and integrated value chain to maintain a strong market position. The company is actively investing in lower-carbon marine solutions, signaling a long-term strategic pivot. This dual focus on traditional product reliability and future energy transitions positions them as a resilient and forward-thinking partner for the global shipping industry.

Chevron Corporation utilizes its vast operational scale and technological expertise to deliver high-performance lubricants. Their strength lies in consistent product quality and a robust distribution framework that serves international maritime hubs. By maintaining a strong emphasis on research and development, Chevron ensures its formulations meet the evolving technical demands of modern, high-efficiency marine engines.

ENEOS Corporation stands out due to its dominant refining capacity and deep technical knowledge. The corporation provides a comprehensive portfolio of marine lubricants tailored to the specific needs of the Asian shipping fleet. Their strategy focuses on leveraging local manufacturing strength to ensure supply chain security and deliver specialized products that enhance engine performance and operational longevity for regional clients.

Gulf Oil Marine Ltd, which operates with a dedicated focus on the maritime sector. Their core strength is a customer-centric approach, offering bespoke technical services and a wide array of cylinder and system oils. This commitment to specialized support and a global network of ports allows them to build strong, lasting relationships with ship operators worldwide.

Top Key Players in the Market

- BP p.l.c.

- Chevron Corporation

- ENEOS Corporation

- Gulf Oil Marine Ltd

- Idemitsu Kosan Co. Ltd.

- Lucas Oil Products Inc.

- Lukoil Marine Lubricants DMCC

- Penrite Oil

- Royal Dutch Shell plc

- TotalEnergies SE

- Warren Oil Company LLC

Recent Developments

- In 2025, Chevron Corporation, the primary developer, announced updates to its marine grease portfolio. Chevron Marine Lubricants restructured and rebranded its grease products (classifying them by thickener type for easier selection) with new naming, packaging, improved labeling, and QR codes for technical details. This applies to marine supply regions and ports.

- In 2025, the official Gulf Marine confirms the ongoing supply of a full range of marine greases, oils, and EALs for shipboard use, with emphasis on OEM approvals and reliability. Castrol continues to offer high-performance marine greases (including Environmentally Acceptable Lubricants/EALs like BioTac MP2, which carries EU Ecolabel registration for multipurpose EP grease applications in sensitive marine environments).

Report Scope

Report Features Description Market Value (2025) USD 422.7 million Forecast Revenue (2035) USD 582.1 million CAGR (2026-2035) 3.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Thickeners (Metallic Soap Thickener, Non-soap Thickener), By Product Type (Synthetic, Mineral Based, Bio-Based), By Ship Type (Bulk Carrier and Cargo Ships, Passenger Ships, Tankers, Cruise and Ferries, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape BP p.l.c., Chevron Corporation, ENEOS Corporation, Gulf Oil Marine Ltd, Idemitsu Kosan Co. Ltd., Lucas Oil Products Inc., Lukoil Marine Lubricants DMCC, Penrite Oil, Royal Dutch Shell plc, TotalEnergies SE, Warren Oil Company LLC Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- BP p.l.c.

- Chevron Corporation

- ENEOS Corporation

- Gulf Oil Marine Ltd

- Idemitsu Kosan Co. Ltd.

- Lucas Oil Products Inc.

- Lukoil Marine Lubricants DMCC

- Penrite Oil

- Royal Dutch Shell plc

- TotalEnergies SE

- Warren Oil Company LLC

Our Clients

- 179972

- March 2026