Quick Navigation

Report Overview

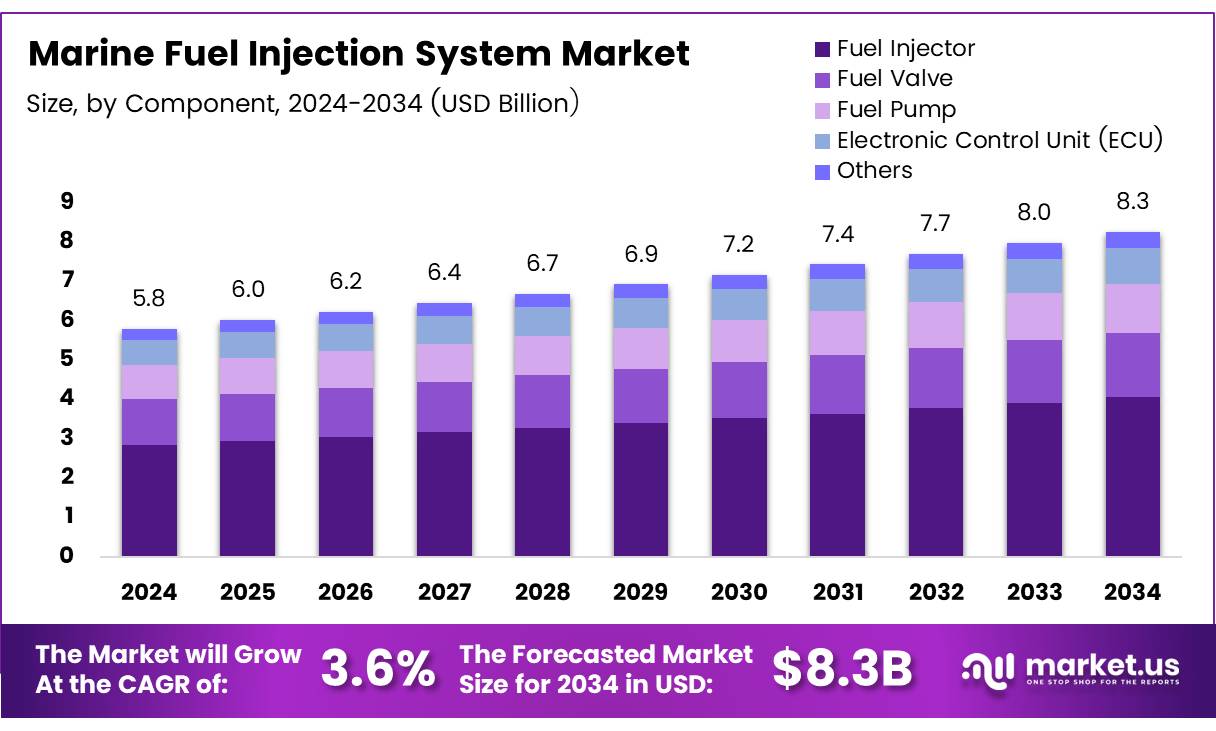

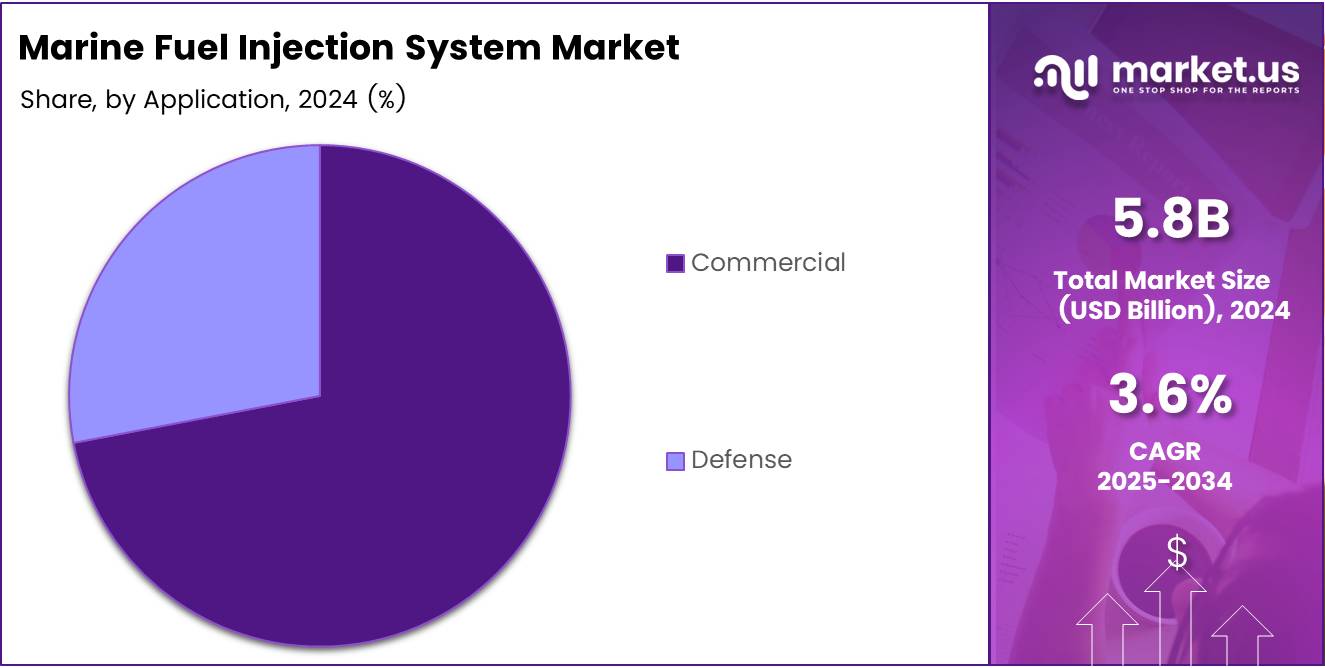

The Global Marine Fuel Injection System Market size is expected to be worth around USD 8.3 Billion by 2034, from USD 5.8 Billion in 2024, growing at a CAGR of 3.6% during the forecast period from 2025 to 2034.

The Marine Fuel Injection System plays a crucial role in ensuring the efficient operation of marine engines by delivering the correct amount of fuel into the combustion chamber under high pressure. These systems are integral to optimizing fuel consumption, reducing emissions, and enhancing engine performance.

The global push toward sustainability and regulatory compliance, driven by environmental concerns and government mandates, is fostering technological advancements in fuel injection systems. Furthermore, with increasing demand for energy-efficient shipping practices, the Marine Fuel Injection System market is witnessing an upsurge in adoption, particularly in regions focusing on decarbonizing the maritime industry.

The Marine Fuel Injection System market is poised for significant growth, driven by the maritime industry’s ongoing transition towards more environmentally sustainable practices.

One of the most notable drivers is the International Maritime Organization (IMO) strategy, which aims to reduce the carbon intensity of international shipping by at least 40% by 2030, compared to 2008 levels. This push for carbon reduction directly impacts the fuel injection systems, as operators increasingly turn to advanced technologies that optimize fuel efficiency and minimize emissions.

Additionally, market growth is being fueled by government investments and regulations targeting a cleaner and more sustainable maritime sector. For instance, according to safety4sea, data reported by 28,620 ships in 2023 showed a slight reduction in fuel consumption compared to 2022, with 211 million tonnes of fuel used in 2023 compared to 213 million tonnes in 2022. This indicates a growing focus on reducing fuel usage and enhancing fuel efficiency.

With the IMO aiming for a 40% reduction in carbon intensity by 2030 and a target of 70% by 2050, there is an increasing opportunity for manufacturers and suppliers of marine fuel injection systems to innovate. These advancements are expected to help shipping companies comply with emission reduction goals while improving operational efficiency.

Furthermore, governmental support in the form of regulations and financial incentives is likely to accelerate the adoption of advanced fuel injection technologies. The global market for these systems will continue to expand, particularly as both private and public sectors focus on improving environmental outcomes and reducing dependency on traditional marine fuels.

Key Takeaways

- The global Marine Fuel Injection System market is projected to reach USD 8.3 billion by 2034, growing at a 3.6% CAGR from 2025 to 2034.

- Fuel Injectors accounted for 31.1% of the market share in 2024, driving fuel efficiency and emission reductions.

- The Commercial segment led the market in 2024, encompassing vessels like cruise ships, bulk carriers, and tankers.

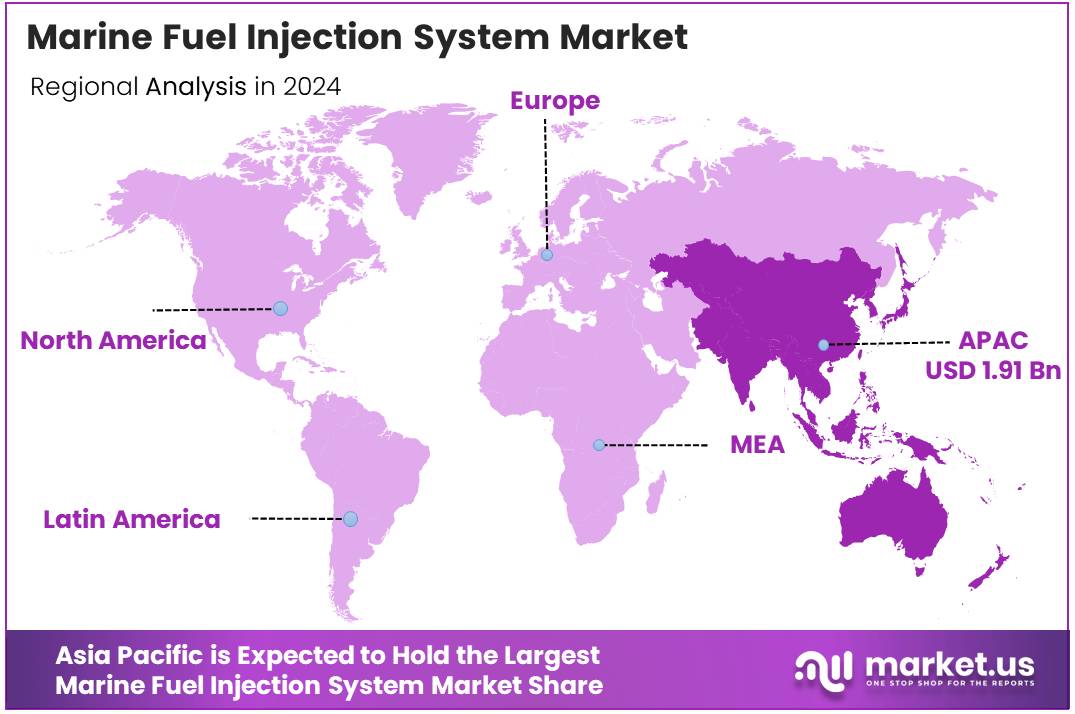

- Asia Pacific held the largest market share at 33.1% in 2024, valued at USD 1.91 billion, driven by shipbuilding industries in China, Japan, and South Korea.

Component Analysis

Fuel Injector Dominates Marine Fuel Injection System Market with 31.1% Share in 2024

In 2024, the Fuel Injector component held a dominant market position in the Marine Fuel Injection System Market, capturing a significant 31.1% share. The Fuel Injector plays a crucial role in optimizing fuel delivery to the engine, enhancing fuel efficiency, and reducing emissions, thereby driving its widespread adoption.

Following the Fuel Injector, the Fuel Valve segment accounted for a substantial portion of the market, contributing to the overall efficiency of fuel delivery. The Fuel Pump, essential for maintaining adequate fuel pressure, also holds a key share, further supporting engine performance and reliability.

The Electronic Control Unit (ECU), which oversees fuel injection timing and precision, is gaining traction due to advancements in automation and control technologies. While other components contribute to the market, their collective share remains smaller compared to the aforementioned parts, as their functionality is typically integrated with the more critical components like the Fuel Injector and ECU.

The growth of this market can be attributed to the increasing demand for high-performance, fuel-efficient marine engines, which continue to drive technological advancements in each of these segments. The consistent emphasis on regulatory compliance and eco-friendly fuel usage also supports this trend.

Application Analysis

Commercial Application Leads with Dominant Share in Marine Fuel Injection System Market in 2024

In 2024, the Commercial segment led the Marine Fuel Injection System market, capturing a dominant market share. This category includes a wide range of maritime vessels such as passenger cruise ships, bulk carriers, container ships, tankers, and others.

The growth of this segment can be attributed to the increasing demand for efficient and environmentally compliant fuel injection systems in large-scale commercial shipping operations. Passenger cruises and container ships, in particular, contribute to the high market share due to their expansive fleets and continuous operational requirements.

On the other hand, the Defense segment, which includes submarines, destroyers, frigates, aircraft carriers, and other military vessels, held a significant but smaller portion of the market.

The demand for marine fuel injection systems in the defense sector is driven by the specialized performance needs of military vessels and the increasing focus on advanced, reliable technologies for national security. However, the commercial segment’s sheer size, rapid technological advancements, and ongoing growth in global trade give it a competitive edge in the marine fuel injection system market.

Key Market Segments

By Component

- Fuel Injector

- Fuel Valve

- Fuel Pump

- Electronic Control Unit (ECU)

- Others

By Application

- Commercial

- Passenger Cruise

- Bulk Carrier & Container ships

- Tankers

- Others

- Defense

- Submarines

- Destroyers

- Frigates

- Aircraft Carriers

- Others

Drivers

Stringent Environmental Regulations Drive Demand for Advanced Marine Fuel Injection Systems

The growing stringency of environmental regulations, particularly the IMO 2020 guidelines, is significantly impacting the marine fuel injection system market. These regulations, which require a reduction in sulfur emissions from marine vessels, are pushing shipping companies to invest in more efficient and environmentally friendly fuel injection technologies.

The demand for advanced systems, such as common rail direct injection (CRDI), is increasing as they offer enhanced fuel efficiency, reduce harmful emissions, and improve overall engine performance. Additionally, the surge in global trade and maritime traffic has resulted in a greater need for improved fuel systems that can support higher engine demands while adhering to regulatory standards.

As shipping volumes rise, so does the need for more efficient fuel usage, leading to an increased focus on technological advancements in marine fuel injection systems. Furthermore, the rising cost of marine fuels is driving the adoption of fuel-efficient technologies to reduce operating expenses, making advanced fuel injection systems a more attractive investment for shipping companies.

These combined factors—regulatory pressures, global trade growth, technological advancements, and rising fuel costs—are shaping the market landscape and promoting the adoption of innovative fuel injection solutions.

Restraints

Shortage of Skilled Technicians Limits Market Expansion

One of the significant challenges facing the marine fuel injection system market is the lack of skilled technicians. The installation, maintenance, and repair of advanced fuel injection systems require highly trained professionals, yet there is a shortage of qualified workforce in the marine sector. This skills gap hampers the effective implementation and upkeep of these systems, limiting market growth.

As more vessels adopt technologically advanced engines and fuel systems, the demand for experienced professionals to manage these complex systems rises. Without sufficient technical expertise, vessel operators may face difficulties in ensuring optimal performance and efficiency, leading to higher operational costs and potential system failures.

Additionally, the lack of skilled labor may also deter ship owners from upgrading their existing fuel systems or investing in newer, more advanced technology, as the cost and effort required for training and maintenance become a burden. This can significantly slow the overall adoption of innovative fuel injection systems, creating a bottleneck in the market. As such, the shortage of qualified technicians poses a critical restraint, impacting the growth potential of the marine fuel injection system market.

Growth Factors

Expansion of LNG-Powered Vessels Drives Market Opportunities for Fuel Injection Systems

The growth of LNG-powered vessels represents a significant opportunity for the marine fuel injection system market. As the demand for LNG as a marine fuel rises due to its environmental benefits, including reduced emissions compared to traditional marine fuels, the need for specialized fuel injection systems designed to optimize LNG combustion is increasing. These systems must be tailored to handle the unique properties of LNG, such as its low density and cryogenic nature.

Moreover, the growing trend toward hybrid marine vessels—those that use both conventional marine fuels and alternative energy sources—creates another opportunity for fuel injection system development, as these systems must support the integration of multiple fuel types.

Additionally, there is an expanding market for retrofitting existing vessels with more efficient, modern fuel injection systems, enabling older ships to meet stricter emissions regulations while improving fuel economy.

Furthermore, the integration of fuel injection systems with digital technologies, such as IoT-enabled monitoring platforms, provides a promising growth area by allowing for real-time performance tracking, predictive maintenance, and optimization of fuel usage. As fleet operators seek to reduce operational costs and enhance fuel efficiency, the combination of advanced fuel injection systems with digital solutions will be a key driver for market expansion.

Emerging Trends

Low-Sulfur Fuel Adoption Boosts Demand for Advanced Marine Fuel Injection Systems

The growing adoption of low-sulfur fuel oils (LSFO) in response to stricter environmental regulations is a significant driver for the marine fuel injection system market. As shipping industries move towards cleaner fuels to comply with IMO 2020 standards, there is an increasing need for fuel injection systems that can optimize combustion efficiency and reduce emissions when using these low-sulfur fuels.

This trend is further complemented by the rise of hybrid propulsion systems, which integrate conventional marine engines with electric or alternative methods, creating demand for adaptable and flexible fuel injection technologies.

Additionally, digital twin technology, which simulates real-time engine performance, including fuel injection processes, is gaining traction in the industry. By providing accurate data to optimize engine efficiency and reduce downtime, digital twins play a pivotal role in improving overall operational costs.

Furthermore, the integration of automation and artificial intelligence (AI) into fuel injection systems is becoming more widespread. AI-powered systems can predict maintenance schedules, optimize fuel usage, and enhance overall fuel efficiency while minimizing harmful emissions. Collectively, these trends are pushing for more sophisticated, sustainable, and efficient fuel injection technologies in the maritime sector.

Regional Analysis

Asia Pacific leads the Marine Fuel Injection System market with 33.1% share, valued at USD 1.91 billion

The Marine Fuel Injection System market is experiencing significant growth across various regions, driven by advancements in technology, regulatory changes, and an increasing demand for efficient fuel systems in the maritime industry.

Asia Pacific is the dominating region, accounting for 33.1% of the global market share, with a market value of USD 1.91 billion. The region’s growth is primarily driven by the large number of shipbuilding industries in countries such as China, Japan, and South Korea.

Additionally, the increasing adoption of environmentally friendly regulations, such as the International Maritime Organization (IMO) 2020 sulfur cap, is boosting the demand for advanced fuel injection systems to comply with emissions standards. The rapidly growing maritime trade in the region also contributes to the high market share.

Regional Mentions:

In North America, the market is expected to witness steady growth, fueled by the stringent environmental regulations and the presence of key players in the marine industry. The U.S. and Canada are focusing on modernizing their fleets with fuel-efficient and low-emission technologies. North America is also investing in cleaner marine fuels, driving the demand for fuel injection systems designed for optimal performance.

Europe holds a significant market share due to its well-established maritime industry, particularly in the shipping and cruise sectors. Stringent environmental regulations in the region, such as the EU’s directive on reducing carbon emissions from shipping, are encouraging the adoption of more advanced marine fuel injection systems to ensure compliance with these regulations.

The Middle East & Africa region is witnessing gradual growth, largely driven by the expanding shipping activities in the Gulf countries and the region’s increasing investment in maritime infrastructure. Although the market share remains smaller, it is anticipated to grow as regional economies diversify and invest in cleaner fuel technologies.

In Latin America, market expansion is supported by rising international trade activities and government initiatives aimed at improving the energy efficiency of the shipping sector. However, the region’s growth remains moderate compared to other regions due to lower levels of technological adoption.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2024, the global Marine Fuel Injection System Market is expected to see continued growth, driven by technological advancements, regulatory compliance, and increasing demand for energy efficiency within the marine industry. Several key players are well-positioned to capitalize on these trends, with their diversified product offerings and innovative solutions.

NOVA WERKE AG stands out with its expertise in producing high-performance fuel injection systems for marine engines. The company’s commitment to optimizing fuel efficiency while reducing emissions aligns with the increasing regulatory pressure on the industry. Similarly, Caterpillar and Cummins Inc. remain dominant due to their extensive market presence and continuous investments in R&D. Both companies offer advanced, customizable marine fuel injection systems designed to enhance fuel efficiency and engine performance while meeting stringent environmental standards.

DENSO CORPORATION, known for its cutting-edge technologies in fuel injection systems, is strengthening its position through its focus on hybrid and electric marine solutions. YANMAR HOLDINGS CO., LTD., a leader in diesel engine technology, continues to develop marine-specific fuel injection systems that address both power and environmental concerns.

Woodward and LIEBHERR also play crucial roles by offering highly reliable fuel injection technologies, catering to diverse marine applications, from commercial shipping to offshore oil rigs. Marelli Holdings Co., Ltd., with its advanced electric fuel injection systems, is positioning itself as a forward-looking player amidst the growing trend of electrification.

Lastly, Rolls-Royce Plc, a global leader in marine propulsion systems, is leveraging its expertise in fuel-efficient systems to enhance the sustainability and performance of its marine engine solutions. Collectively, these companies are expected to drive significant innovation, contributing to the market’s expansion in the coming years.

Top Key Players in the Market

- NOVA WERKE AG

- Caterpillar

- Cummins Inc.

- DENSO CORPORATION

- YANMAR HOLDINGS CO., LTD.

- Woodward

- LIEBHERR

- Marelli Holdings Co., Ltd.

- Rolls-Royce Plc

Recent Developments

- In May 2023, Accelleron announced its acquisition of Officine Meccaniche Torino S.p.A. (OMT), aiming to strengthen its market position in providing cutting-edge technologies designed to decarbonize the marine industry.

- In September 2023, Alliant Power completed the acquisition of Everglades Diesel, significantly expanding its presence and capabilities within the marine sector to better serve the growing demand for power solutions.

- In October 2024, SRT secured a £31 million funding boost to support the successful $213 million contract award for its Maritime Domain Awareness (MDA) system, positioning the company for significant growth in global maritime security.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 5.8 Billion |

| Forecast Revenue (2034) | USD 8.3 Billion |

| CAGR (2025-2034) | 3.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Fuel Injector, Fuel Valve, Fuel Pump, Electronic Control Unit (ECU), Others), By Application (Commercial, Defense) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | NOVA WERKE AG, Caterpillar, Cummins Inc., DENSO CORPORATION, YANMAR HOLDINGS CO., LTD., Woodward, LIEBHERR, Marelli Holdings Co., Ltd., Rolls-Royce Plc |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |