Quick Navigation

Report Overview

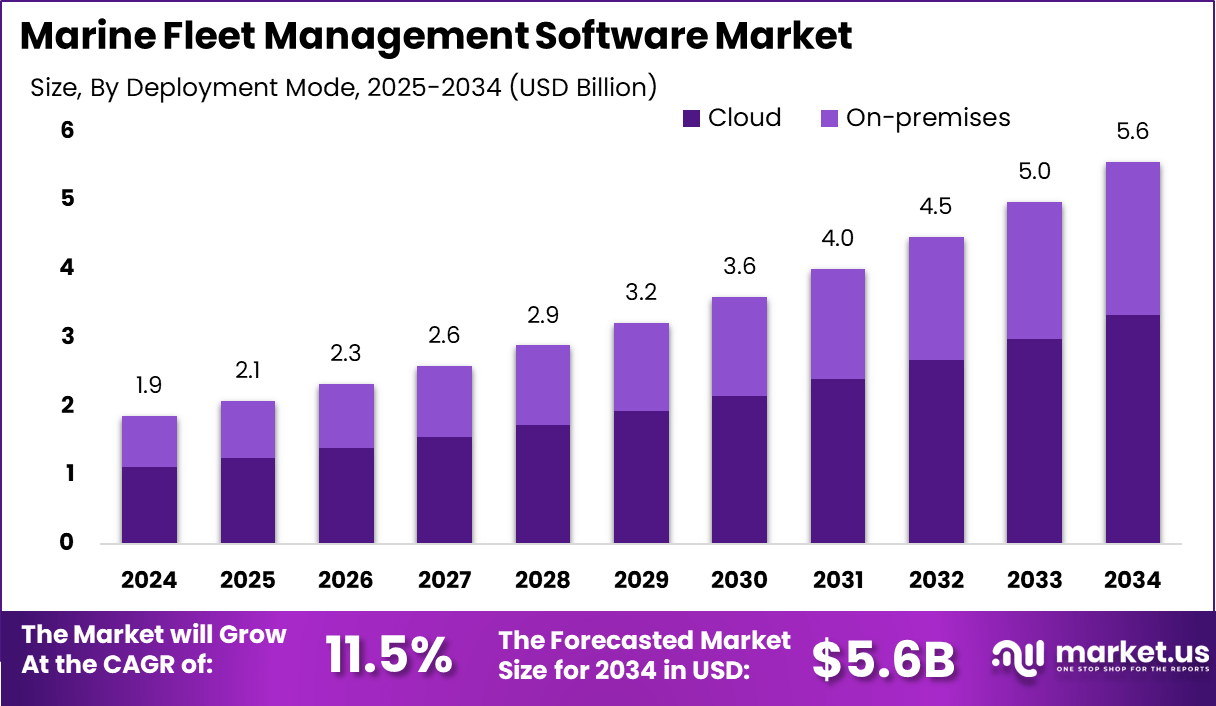

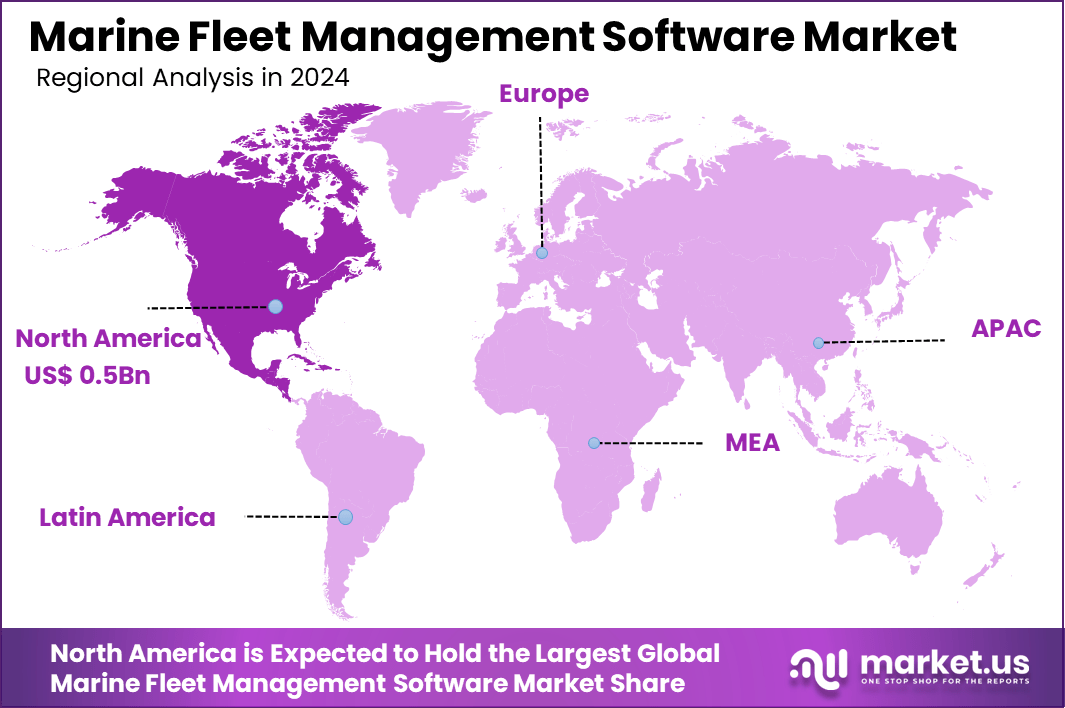

The Global Marine Fleet Management Software Market size is expected to be worth around USD 5.6 Billion By 2034, from USD 1.9 billion in 2024, growing at a CAGR of 11.5% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 31% share, holding USD 0.5 Billion revenue.

Marine Fleet Management Software refers to a centralized digital platform designed to oversee and optimize maritime vessel operations. It integrates a wide array of functionalities such as real‑time vessel tracking via AIS/GPS, fuel usage and emission monitoring, maintenance scheduling, crew and safety management, procurement, compliance with international regulations (e.g., MARPOL, SOLAS, E‑Navigation), and performance analytics.

The Marine Fleet Management Software Market represents the global industry of these digital solutions, driving factors include mounting operational cost pressures in maritime transport, the expansion of global trade, and the urgency to comply with tighter environmental and safety regulations. The need to standardize maintenance, procurement and quality systems across fleets has further accelerated adoption.

Increasing adoption of technologies such as Internet of Things (IoT) sensors, Artificial Intelligence (AI) and cloud computing is notable. Real‑time monitoring of fuel consumption and vessel performance is enabled via IoT, while AI algorithms support predictive maintenance and optimized routing. Cloud platforms offer on‑demand access across global fleets.

Key reasons for adopting this software include enhanced operational efficiency, lower fuel use, minimization of downtime through proactive maintenance, safety compliance, and reduction of carbon emissions. These systems also deliver visibility into vessel behavior and performance metrics, assisting in environmental stewardship and regulatory adherence.

Investment opportunities lie in emerging technologies such as autonomous vessels, smart ports, and integrated supply‑chain platforms. Vendors offering modular cloud solutions, AI‑driven analytics, and IoT connectivity stand to benefit from increasing demand across both developed and developing maritime markets.

Business benefits reported include optimized fleet deployment, improved crew and asset management, reduced unplanned maintenance, and data‑backed decision making. These outcomes support overall profitability and resilience, especially in operations spanning multiple regulatory environments.

Key Takeaways

- The Global Marine Fleet Management Software Market is projected to reach USD 5.6 billion by 2034, growing from USD 1.9 billion in 2024, with a strong CAGR of 11.5% between 2025 and 2034, driven by increasing automation in maritime logistics and rising fuel optimization needs.

- In 2024, North America led the global market with a 31% share, generating approximately USD 0.5 billion in revenue, supported by early adoption of digital maritime technologies and well-established shipping infrastructure.

- By component, software solutions held the majority in 2024, contributing to 68% of the global revenue, as demand surged for route planning, fuel management, and regulatory compliance systems.

- In terms of deployment, cloud-based platforms dominated the market with a 60% share in 2024, reflecting a growing shift towards scalable, real-time, and remotely accessible fleet operations.

- Among end users, the shipping industry emerged as the leading segment, accounting for 45% of total market share in 2024, due to increased reliance on integrated software tools for asset tracking, maintenance scheduling, and regulatory reporting.

Role of AI

The integration of artificial intelligence into marine fleet management software has initiated a significant transformation within maritime operations. AI-driven systems now enable real-time vessel performance monitoring, predictive maintenance using sensor and IoT data, and optimized route planning that reduces fuel consumption and emissions.

According to Orca AI, such navigation‑focused AI can reduce route deviations by 38 million nautical miles annually and cut fuel costs by about $100,000 per vessel, translating to a 47 million tonne reduction in carbon emissions globally per year. A case study in maritime fleet management software reported a 15% reduction in fuel consumption for a 50‑vessel fleet over six months, generating approximately $5 million in annual savings.

AI‑driven predictive maintenance is transforming vessel upkeep by forecasting equipment failures and scheduling maintenance before issues arise. Maersk’s use of engine‑monitoring AI and similar platforms like Wärtsilä’s and Shell’s have led to up to 15% savings in fuel and reduced downtime. Additionally, naval-grade AI systems such as Fathom5’s Enterprise Remote Monitoring (ERM v4) have been deployed on warships, reading 10,000 sensor data points per second to avert critical failures ahead of time.

AI is also foundational to compliance tracking, environmental management, and the development of autonomous maritime systems. Fleet management platforms now automatically benchmark against historic performance, monitor emissions and ESG metrics, and deliver timely regulatory reports. Environmental AI systems like hull‑cleaning robots have demonstrated up to 13% reductions in ferry fuel use, improving efficiency and lowering emissions without reliance on antifouling chemicals.

North America Growth

In 2024, North America held a dominant market position, capturing more than a 31% share and generating revenue of approximately USD 0.5 billion in the global marine fleet management software market. This regional leadership can be largely attributed to the region’s early adoption of digitalization across maritime operations, particularly in the United States and Canada.

The presence of advanced shipping infrastructure, stringent regulatory requirements for fleet compliance, and a high concentration of commercial and defense marine operators have collectively driven the demand for robust software platforms to manage, monitor, and optimize marine fleets efficiently.

Furthermore, the increasing use of AI-driven analytics, predictive maintenance tools, and integrated IoT systems across North American ports and shipping lines has strengthened the need for advanced fleet management solutions. Leading maritime software providers in the region have also been actively engaged in product upgrades and strategic collaborations with logistics and naval organizations, encouraging wider deployment.

By Component Analysis

In 2024, Software segment held a dominant market position, capturing more than a 68 % share of the global marine fleet management software market. This dominance can be attributed to the core value that software delivers – enabling real-time vessel tracking, route optimisation, compliance reporting, and predictive maintenance through intuitive dashboards and analytics tools.

The Software segment leads because it provides the essential capabilities that directly address operators’ needs. These solutions enable remote monitoring, performance insights, and automation of critical tasks such as fuel shift analysis and safety management – functions that create immediate operational efficiency. As shipping companies strive to reduce costs and improve reliability, they increasingly prioritise robust, scalable software platforms over standalone service packages.

By Deployment Analysis

In 2024, Cloud segment held a dominant market position, capturing more than 60 % share of the global marine fleet management software market. This commanding lead is supported by the segment’s scalable infrastructure, minimal upfront investment, and ease of access across dispersed maritime operations.

Operators are increasingly embracing cloud platforms to gain real-time access to vessel data and analytics from any location, eliminating the need for complex on-premises systems while ensuring seamless upgrades and regulatory compliance. The Cloud segment’s leadership is also driven by cost efficiency and operational flexibility.

By leveraging cloud services, maritime firms have been able to reduce IT expenses by approximately 22 % compared to on‑premise alternatives. Pay‑as‑you‑go pricing models have democratized access to advanced fleet software, enabling small‑ and medium‑sized enterprises to adopt digital tools without heavy capital expenditure.

By End-User Analysis

In 2024, Shipping Industries segment held a dominant market position, capturing more than 45 % share of the global marine fleet management software market. This leadership is rooted in the extensive fleet sizes maintained by commercial shipping companies that demand comprehensive solutions for fleet operations, including route optimization, fuel management, maintenance scheduling, and regulatory compliance.

The deep integration of digital platforms into shipping operations has allowed businesses to streamline workflows and reduce operational costs – key drivers behind this segment’s dominant share. Leading shipping enterprises have placed high priority on platforms capable of delivering real-time insights.

These systems support large-scale fleet oversight, predictive maintenance to minimize unplanned downtime, and emissions tracking to satisfy strict environmental mandates such as IMO regulations. The importance of these capabilities has encouraged heavy investment from shipping companies, maintaining the segment’s strong position in the market.

Key Market Segments

By Component

- Software

- Services

By Deployment

- Cloud

- On-premises

By End-User

- Ports & Terminals

- Shipping Industries

- Maritime Freight Forwarders

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Emerging Trends

AI‑Driven Predictive Maintenance & Digital Twins

The integration of AI with real‑time sensor data has enabled predictive maintenance across maritime fleets. Vessel operators are adopting AI‑powered analytics to forecast equipment failures before they occur, thereby reducing downtime and maintenance costs.

IoT sensors combined with machine learning models offer continuous performance insights – these capabilities are reshaping fleet operations by enabling proactive lifecycle management. Complementing predictive maintenance, Digital Twin platforms are gaining momentum in maritime operations.

These virtual replicas of vessels integrate sensor data to simulate operations, enabling scenario analysis for route planning, maintenance, and risk assessment. Although still in early adoption phases, digital twins are poised to become a strategic layer atop fleet management software, offering vessel-level insight and optimization.

Driver

Stricter Environmental & Emissions Regulations

Global maritime regulations – such as IMO’s MARPOL Annex VI, EEXI, and Carbon Intensity Indicator (CII)- have significantly increased pressure on shipowners to monitor and reduce greenhouse gas emissions. This creates strong demand for fleet management solutions capable of delivering granular fuel consumption analytics and compliance reporting.

In many instances, the adoption of such software is driven directly by the need to avoid financial penalties and to adhere to international standards. The urgency around sustainability goals has made operational transparency essential.

Fleet operators increasingly rely on digital systems for data collection and reporting tied to carbon tracking, emissions accounting, and optimization of engine performance. The result has been a marked shift towards specialized software that seamlessly integrates compliance and performance metrics – a pattern observed across regional adoption stats.

Restraint

High Initial Investment & Integration Complexity

Despite clear advantages, adoption of modern marine fleet management platforms is often hindered by significant upfront expenses, particularly for small and medium‑sized fleet operators. Costs include subscription/licensing fees, installation of onboard sensors, satellite communication infrastructure, staff training, and ongoing maintenance. For organizations with limited capital, these barriers may delay or limit full implementation.

Moreover, many maritime operators face integration complexities when linking legacy systems – such as maintenance logs, crew scheduling tools, or in‑house ERP – with new cloud-based platforms. The absence of standardized APIs and different data formats often results in siloed solutions, undermining efficiency gains. As a result, pilots and phased rollouts are common, but full-scale deployments may be slowed or abandoned.

Opportunity

Expansion in Asia‑Pacific & Mid‑Size Fleet Segments

The Asia-Pacific region, including emerging economies such as India and Southeast Asia, holds high growth potential. This region’s extensive maritime trade and port modernization efforts are driving both new fleet acquisitions and the upgrade of existing vessels.

Many mid-scale operators in this region are now seeking scalable, cloud-based software solutions that avoid substantial capital outlays while delivering real-time monitoring and compliance functionality. Additionally, cloud-based subscription models are lowering entry barriers and enabling fleet owners to gradually scale their capabilities.

These platforms allow flexible deployment without major IT investments, appealing especially to operators in high-growth but cost-sensitive markets. Adoption is expected to accelerate as digital transformation continues across Asia-Pacific maritime sectors .

Challenge

Cybersecurity & Data Sovereignty Risks

The increasing interconnectedness of maritime systems is amplifying cybersecurity vulnerabilities. As vessels rely more on connected platforms for navigation, fuel analytics, and communication, they also become targets for cyber-attacks.

Intrusions or ransomware incidents could disrupt navigation or compromise sensitive data, posing safety and compliance threats. Consequently, cybersecurity protocols have become critical yet challenging components to build and maintain.

Another emerging obstacle relates to data sovereignty and vendor lock‑in. Consolidation trends – such as acquisitions of key satellite data providers (e.g., Kpler’s purchase of Spire) – raise fears over data access restrictions, pricing power, and reduced interoperability. If operators lose access to critical AIS or satellite feeds due to commercial consolidation, fleet management platforms may become unreliable or overly expensive.

Key Player Analysis

ABS Group of Companies Inc. has emerged as a leading provider in maritime fleet management software through its ABS Wavesight platform, deployed on more than 5,000 vessels globally. Its integration with ABS’s longstanding classification services offers clients confidence in compliance and technical support. ABS’s position is reinforced by its affiliation with a classification society established in 1862, providing institutional depth and market trust.

BASS Software Ltd. and ConnectShip Inc. (sometimes ConnectShip has become part of BASSnet offerings) are recognized for modular, cloud‑based platforms that support cargo, tracking, and logistics workflows. These offerings cater especially to mid‑sized fleets seeking scalable, cost‑efficient digital solutions .

DNV GL (recently DNV) is prominent thanks to its broad suite of analytic and safety‑focused tools. Investment in R&D and acquisitions has allowed DNV to lead in compliance, AI‑enabled predictive maintenance, and integrated vessel-to-shore data systems .

Top Key Players Covered

- ABS Group of Companies Inc.

- BASS Software Ltd.

- ConnectShip Inc.

- DNV GL

- Hanseaticsoft GmbH

- JiBe ERP

- Kongsberg Maritime

- MariApps Marine Solutions Pte Ltd

- Matrid Technologies

- Micromarin

- Norcomms

- SBN TechnoLogics Private Limited

- Seaspeed Marine Management LLC.

- SERTICA

- Shipamax Ltd.

- ShipNet

- Softcom Solutions (UK) Ltd.

- SpecTec

- Star Information System

- Tero Marine

- Veson Nautical LLC

- Other Key Players

Recent Developments

- In July 2024, Union Marine Management Services (UMMS) began deploying CII Simulator digital systems and NAPA’s Voyage Optimization on an initial 55 bulk carriers, under a new agreement with Finnish software provider NAPA. These vessels, ranging from 25,000 to 180,000 DWT, are expected to achieve an average 5-10% reduction in greenhouse gas emissions, supporting global decarbonization goals through advanced digital navigation.

- In January 2024, ABB acquired DTN Shipping’s European and Philippine operations, significantly expanding its maritime software capabilities. This move strengthens ABB’s position in ship route optimization, enabling it to offer integrated digital, electric, and automated marine solutions. The acquisition is set to enhance operational efficiency, fuel performance, and emission control for DTN’s existing customer base.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 1.9 Bn |

| Forecast Revenue (2034) | USD 5.6 Bn |

| CAGR (2025-2034) | 11.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Component (Software, Services), By Deployment (Cloud, On-premises), By End-User (Ports & Terminals, Shipping Industries, Maritime Freight Forwarders) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | ABS Group of Companies Inc., BASS Software Ltd., ConnectShip Inc., DNV GL, Hanseaticsoft GmbH, JiBe ERP, Kongsberg Maritime, MariApps Marine Solutions Pte Ltd, Matrid Technologies, Micromarin, Norcomms, SBN TechnoLogics Private Limited, Seaspeed Marine Management LLC., SERTICA, Shipamax Ltd., ShipNet, Softcom Solutions (UK) Ltd., SpecTec, Star Information System, Tero Marine, Veson Nautical LLC, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |