Global Magnetic Resonance Imaging Coils Market By Product Type (Radiofrequency Coils and Gradient Coils), By Application (Brain and Neurology, Spine and Musculoskeletal, Cardiac and Vascular, Abdominal and Pelvic, Breast Imaging, Pediatric Imaging and Others), By End User (Hospitals, Diagnostic Imaging Centers, Ambulatory Surgical Centers and Research and Academic Institutes), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 181991

- Number of Pages: 251

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

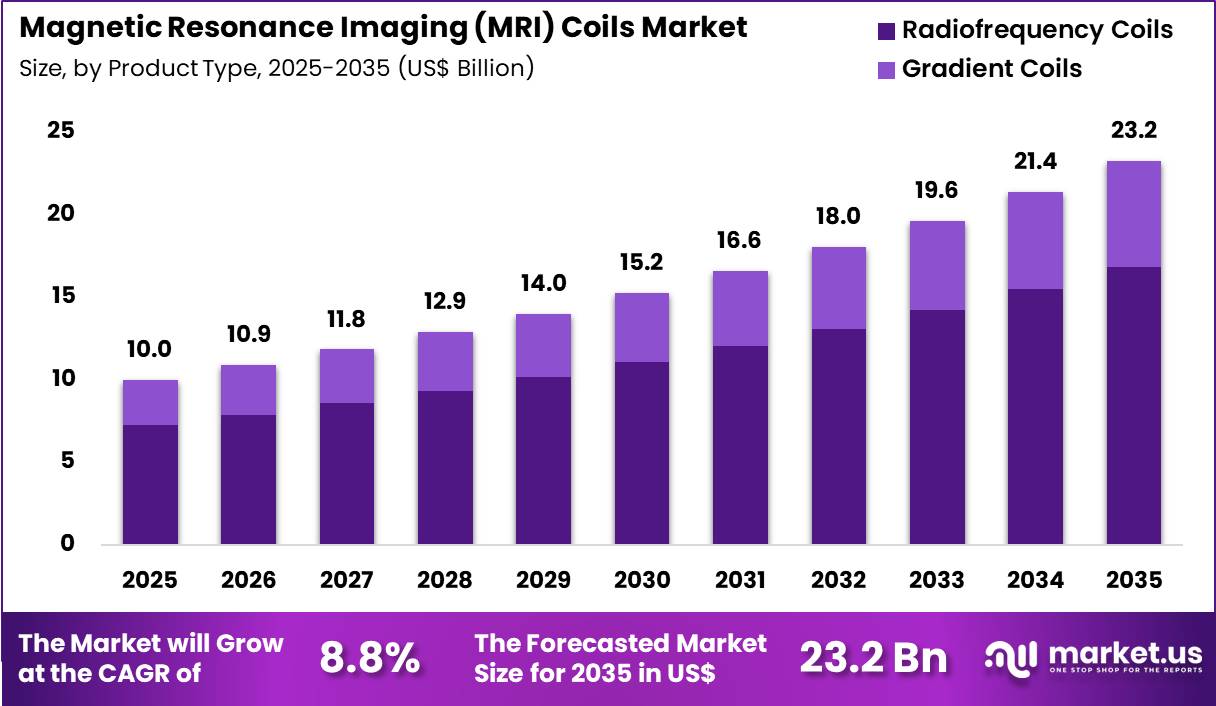

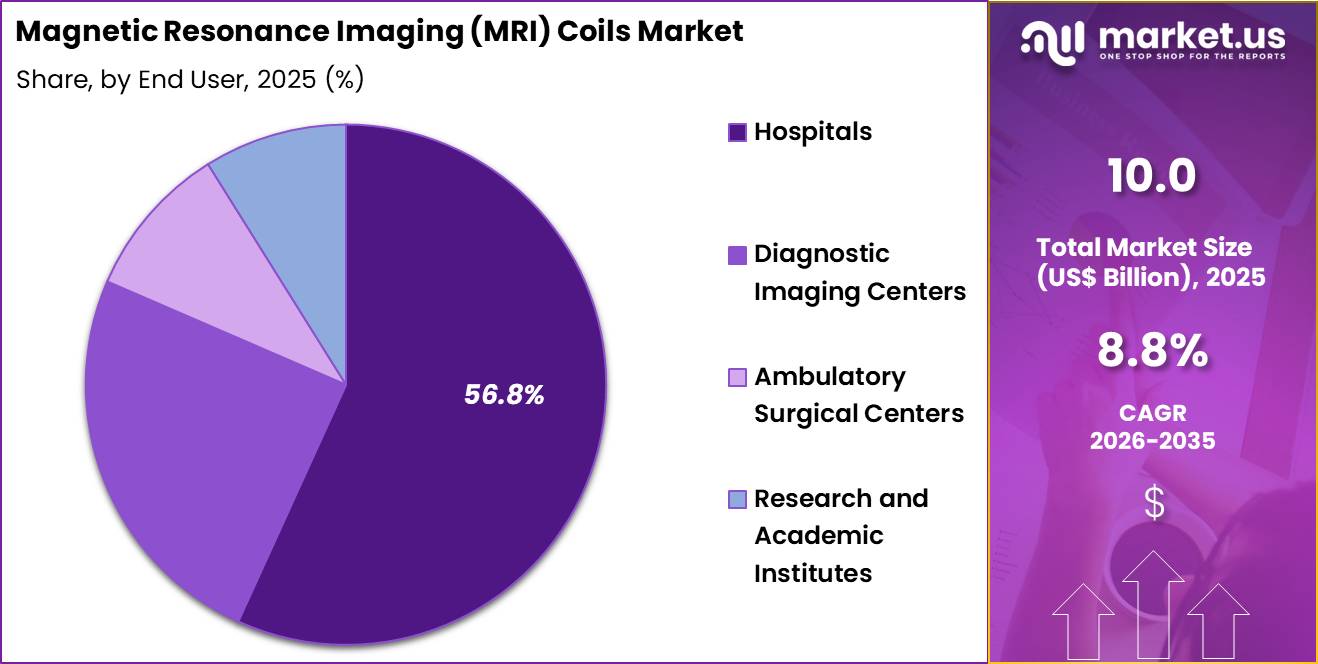

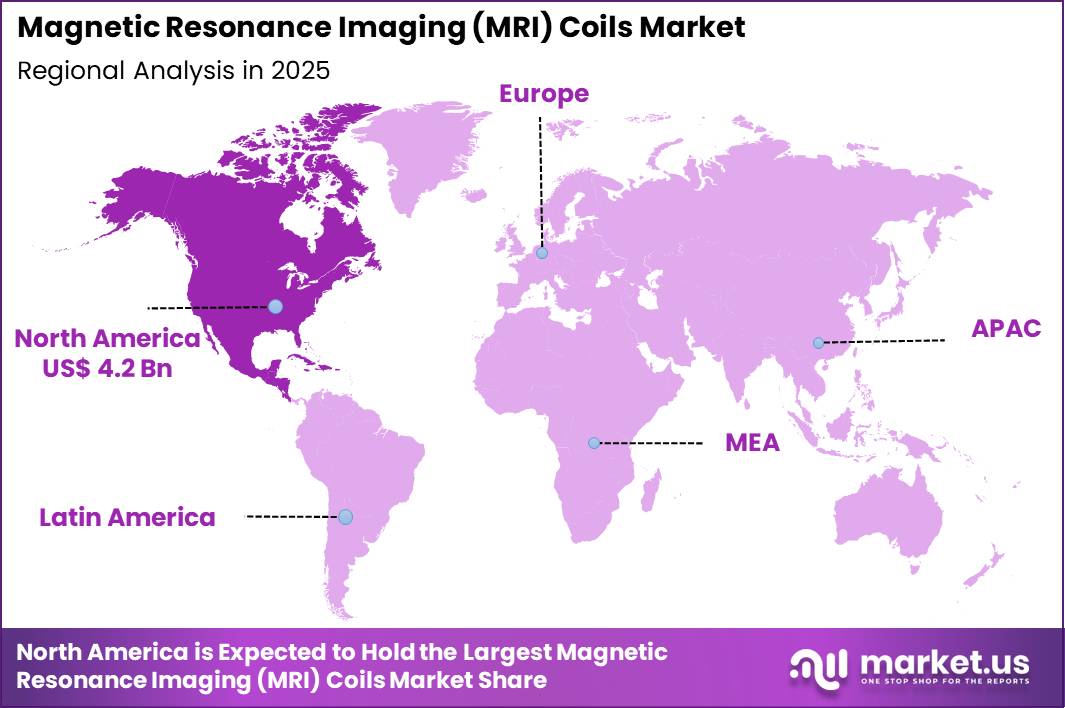

The Global Magnetic Resonance Imaging Coils Market size is expected to be worth around US$ 23.2 Billion by 2035 from US$ 10.0 Billion in 2025, growing at a CAGR of 8.8% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 42.6% share with a revenue of US$ 4.2 Billion.

Increasing adoption of advanced magnetic resonance imaging techniques propels the MRI Coils market as healthcare providers require specialized radiofrequency coils that maximize signal-to-noise ratio, anatomical coverage, and image quality for precise diagnostic and therapeutic planning.

Radiologists increasingly deploy dedicated neurovascular coils for comprehensive brain and cervical spine examinations, capturing high-resolution images of ischemic strokes, multiple sclerosis plaques, and intracranial vascular malformations to guide acute stroke interventions and long-term disease monitoring.

These coils support musculoskeletal applications through high-channel knee, shoulder, and wrist coils that reveal subtle cartilage defects, ligament tears, and bone marrow edema in sports injuries and degenerative joint disorders. Breast imaging specialists utilize multi-channel breast coils for dynamic contrast-enhanced MRI, detecting and characterizing malignant lesions in dense breast tissue while supporting preoperative staging and post-treatment surveillance.

Cardiac coils enable functional and perfusion imaging that assesses myocardial viability and ischemia in coronary artery disease patients, providing critical data for revascularization planning. Whole-body coils with integrated spine arrays facilitate detailed spinal cord evaluations in trauma and degenerative myelopathy, while extremity coils enhance peripheral joint assessments in rheumatoid arthritis and osteoarthritis.

Manufacturers pursue opportunities to integrate lightweight, flexible coil arrays with advanced parallel imaging acceleration, expanding applications in pediatric and claustrophobic patients where reduced scan times and open designs improve compliance and diagnostic yield. These advancements support ultra-high-field MRI systems that demand high-density coils for superior resolution in metabolic imaging of tumors and neurodegenerative disorders.

Opportunities emerge in modular, interchangeable coil designs that streamline workflows across multi-specialty imaging centers. Companies invest in automated coil selection, patient positioning sensors, and AI-assisted shimming to optimize image uniformity and reduce setup time.

In February 2026, GE HealthCare received FDA clearance for its SIGNA Sprint and SIGNA Bolt MRI systems. These platforms incorporate the latest AIR Coil technology and AIR Recon DL image reconstruction software, enabling improved image quality while using 1.5T magnetic field systems that are more widely accessible in clinical settings.

In January 2026, Siemens Healthineers obtained FDA approval for the Magnetom Flow MRI system with a 70 cm bore design. The system uses a nearly helium-free cooling architecture and BioMatrix Contour XL coils equipped with positioning sensors that help automate patient setup and lower overall energy consumption.

Recent trends emphasize high-channel, flexible coils with energy-efficient designs and AI-driven optimization, positioning the market for growth in faster, higher-quality MRI examinations that advance precision diagnostics across neurology, orthopedics, oncology, and cardiology.

Key Takeaways

- In 2025, the market generated a revenue of US$ 10.0 Billion, with a CAGR of 8.8%, and is expected to reach US$ 23.2 Billion by the year 2035.

- The product type segment is divided into radiofrequency coils and gradient coils, with radiofrequency coils taking the lead with a market share of 72.5%.

- Considering application, the market is divided into brain and neurology, spine and musculoskeletal, cardiac and vascular, abdominal and pelvic, breast imaging, pediatric imaging and others. Among these, brain and neurology held a significant share of 32.7%.

- Furthermore, concerning the end user segment, the market is segregated into hospitals, diagnostic imaging centers, ambulatory surgical centers and research and academic institutes. The hospitals sector stands out as the dominant player, holding the largest revenue share of 56.8% in the market.

- North America led the market by securing a market share of 42.6%.

Product Type Analysis

Radiofrequency coils accounted for 72.5% of growth within product type and dominate the magnetic resonance imaging coils market due to their direct role in signal reception and image quality improvement during MRI scans. FDA guidance describes MR receive-only coils as devices intended to produce images of human anatomy for general diagnostic use, which reflects their core importance in routine imaging workflows.

Hospitals and imaging providers increasingly prefer advanced radiofrequency coils because higher signal-to-noise performance supports clearer anatomical visualization and faster scan protocols. This segment is expected to strengthen as MRI systems continue shifting toward specialized coils for neurology, musculoskeletal, breast, and cardiac imaging.

Manufacturers also invest heavily in lightweight, anatomically contoured, and multi-channel coil designs that improve patient comfort and support parallel imaging. Demand is likely to rise further as diagnostic centers pursue better throughput, higher-resolution imaging, and stronger compatibility with modern MRI platforms.

Application Analysis

Brain and neurology accounted for 32.7% of growth within application and dominate the MRI coils market due to the high clinical dependence on MRI for evaluating neurological anatomy and disease. WHO reported that in 2021 more than 3 billion people worldwide were living with a neurological condition, which highlights the enormous global diagnostic burden tied to brain and nerve disorders.

NIH-linked literature also describes magnetic resonance imaging as the modality of choice for studying brain anatomy because of its high resolution and excellent soft-tissue contrast. This segment is projected to expand as providers increase MRI use for stroke assessment, neurodegenerative disease follow-up, epilepsy workups, and structural brain evaluation.

Dedicated brain coils are anticipated to see continued demand because neurologic imaging requires high precision, broad coverage, and reliable image uniformity for diagnosis and monitoring.

End-User Analysis

Hospitals accounted for 56.8% of growth within end user and dominate the MRI coils market due to their concentration of advanced imaging infrastructure, specialist staff, and high patient volumes. Hospital settings manage a large share of complex neurological, orthopedic, abdominal, and emergency imaging cases, which supports frequent use of dedicated MRI coil systems.

AHA materials also show hospitals continue to expand MRI access and specialized MRI programs, including mobile and advanced-site deployment, which reinforces their leadership in imaging adoption. This segment is expected to strengthen as hospitals modernize radiology departments, replace aging hardware, and expand specialty imaging pathways.

Hospitals are likely to remain the dominant buyers because they require a wide portfolio of coils across multiple anatomical applications and maintain the capital capacity to invest in premium MRI accessories and upgrades.

Key Market Segments

By Product Type

- Radiofrequency Coils

- Gradient Coils

By Application

- Brain and Neurology

- Spine and Musculoskeletal

- Cardiac and Vascular

- Abdominal and Pelvic

- Breast Imaging

- Pediatric Imaging

- Others

By End User

- Hospitals

- Diagnostic Imaging Centers

- Ambulatory Surgical Centers

- Research and Academic Institutes

Drivers

Increasing installation of high-field MRI systems is driving the market.

Healthcare facilities continue to upgrade to high-field MRI scanners that require advanced radiofrequency coils for optimal signal reception and image quality. These systems demand phased-array coil designs to support parallel imaging techniques and reduce scan times. The driver aligns with clinical preferences for superior soft-tissue contrast in neurology, oncology, and musculoskeletal applications.

Providers prioritize multi-channel coils to enhance spatial resolution in routine diagnostic protocols. The expansion reflects ongoing capital investment in imaging infrastructure within hospitals and diagnostic centers. Coil manufacturers respond with modular configurations compatible with 1.5T and 3T platforms. The trend supports higher throughput in busy radiology departments.

Enhanced coil sensitivity improves detection of subtle pathologies. Facilities achieve better patient throughput through faster acquisition sequences. This factor sustains consistent procurement of specialized coil hardware.

Restraints

High replacement costs for specialized multi-channel coils are restraining the market.

Multi-element phased-array coils represent significant capital outlays, often exceeding several hundred thousand dollars per unit depending on channel count and anatomical coverage. Facilities face challenges justifying replacement of functional legacy coils amid constrained capital budgets.

The restraint moderates upgrade cycles in community hospitals and outpatient imaging centers. Ongoing service agreements for coil calibration and maintenance add recurring financial commitments. The factor limits rapid adoption of higher-channel-count designs in cost-sensitive environments. Providers prioritize essential system maintenance over elective coil enhancements.

The dynamic influences purchasing decisions toward more economical single-anatomy coils. This constraint tempers penetration of premium coil technologies across diverse provider types. The limitation persists in constraining overall market velocity in non-academic settings. Budgetary pressures continue to affect procurement patterns during recent years.

Opportunities

Development of lightweight flexible coil arrays is creating growth opportunities.

Recent coil designs incorporate flexible materials and lightweight construction to improve patient comfort during extended examinations. These arrays conform closely to anatomical contours for enhanced signal-to-noise ratio in challenging body regions. Opportunities arise for improved image quality in pediatric and bariatric imaging applications.

The framework supports reduced motion artifacts through better coil-to-patient coupling. Manufacturers gain capacity to address comfort-related complaints associated with rigid traditional coils. The development facilitates expansion into outpatient and ambulatory imaging centers. Such advancements promote differentiation through superior patient experience metrics.

The opportunity fosters partnerships with MRI system vendors for integrated coil-system offerings. Stakeholders anticipate increased utilization in high-throughput environments. This innovation positions providers for enhanced clinical acceptance in diverse patient populations.

Impact of Macroeconomic / Geopolitical Factors

Hospitals and imaging centers continue to upgrade diagnostic capabilities, yet broader economic forces influence purchasing decisions in the MRI coils market. Rising material and manufacturing costs increase the price of specialized coil components, which can slow equipment replacement cycles for healthcare providers.

Higher borrowing costs also make large imaging investments harder for smaller hospitals and diagnostic clinics to justify. Global political tensions affect the availability of electronic parts, sensors, and high-precision materials used in coil manufacturing.

US tariffs on imported electronic components and imaging hardware add further cost pressure for device suppliers and healthcare buyers. These factors may delay short-term procurement plans and extend upgrade timelines.

At the same time, manufacturers strengthen domestic sourcing and improve supply resilience to manage risk. Continued demand for higher image quality and advanced diagnostic capability supports stable long-term growth in the MRI coils market.

Latest Trends

Introduction of higher-channel-count receive coils is driving the market.

Manufacturers launched multi-channel receive coil arrays exceeding 64 elements in 2025 for ultra-high-field and advanced clinical applications. These coils support accelerated parallel imaging techniques with reduced aliasing artifacts. The 2025 introduction aligns with demand for faster scans in time-sensitive protocols such as cardiac and abdominal imaging.

Radiologists benefit from improved temporal resolution and volumetric coverage. The development addresses requirements for whole-body imaging in oncology staging. Facilities report potential reductions in breath-hold durations through higher acceleration factors.

The innovation stimulates replacement demand for legacy lower-channel systems. Early clinical evaluations demonstrate consistent performance gains in signal homogeneity. The advancement supports integration with emerging compressed sensing reconstructions. Overall, this technological progression elevates diagnostic capabilities in high-end MRI environments.

Regional Analysis

North America is leading the Magnetic Resonance Imaging Coils Market

North America accounted for 42.6% of the magnetic resonance imaging (MRI) coils market in 2025 as hospitals and diagnostic imaging centers expanded use of advanced MRI systems for neurological, orthopedic, and cardiovascular diagnostics. Healthcare providers across the United States and Canada are upgrading imaging infrastructure to support higher resolution scanning and faster diagnostic workflows.

According to the Organisation for Economic Co-operation and Development, the United States had about 40 MRI units per million population in recent years, reflecting one of the highest imaging system densities globally and supporting strong demand for advanced coil components.

Rising prevalence of chronic diseases such as neurological disorders, musculoskeletal conditions, and cardiovascular diseases has increased the number of MRI examinations performed across major healthcare facilities. Imaging centers are investing in specialized coils designed for brain, breast, spine, and cardiac imaging to improve signal quality and diagnostic accuracy.

Technological advances such as multi-channel phased-array coils and lightweight flexible coil designs are enhancing patient comfort and image clarity. Hospitals are also integrating MRI systems with artificial intelligence software that improves image reconstruction and workflow efficiency.

Academic medical centers and research institutions across the region are collaborating with equipment manufacturers to develop advanced imaging technologies. These developments collectively supported strong growth of MRI coil technologies across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to experience significant expansion during the forecast period as healthcare infrastructure improves and diagnostic imaging capacity increases across rapidly developing economies. Countries such as China, India, Japan, and South Korea are expanding hospital networks and investing heavily in advanced medical imaging technologies to improve early disease detection.

The World Health Organization has reported that noncommunicable diseases account for nearly 71% of global deaths, increasing the importance of advanced diagnostic imaging tools used to detect conditions affecting the brain, heart, and musculoskeletal system. Hospitals across the region are increasing procurement of MRI scanners and related components to address rising demand for diagnostic services.

Medical imaging centers are adopting specialized coil systems that improve imaging quality for neurological, orthopedic, and oncological evaluations. Governments are also investing in healthcare modernization programs that support installation of advanced imaging technologies in both public and private hospitals.

Regional medical device manufacturers are expanding production capabilities to support local demand for imaging equipment components. Universities and research institutes are strengthening biomedical engineering programs focused on imaging technologies. These developments are expected to accelerate adoption of advanced MRI coil technologies throughout Asia Pacific in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the Magnetic Resonance Imaging (MRI) Coils Market expand their presence by developing advanced radiofrequency coil technologies, improving signal-to-noise performance, and integrating flexible coil designs that enhance patient comfort during diagnostic imaging procedures. Companies collaborate with hospitals and imaging centers to introduce specialized coil systems tailored for neurological, musculoskeletal, cardiac, and pediatric imaging applications.

They also invest in research initiatives and digital imaging software that improve image clarity and scanning efficiency in modern MRI systems. Siemens Healthineers represents a major participant in the Magnetic Resonance Imaging (MRI) Coils Market and operates as a global medical technology company headquartered in Germany that develops diagnostic imaging systems, laboratory diagnostics, and healthcare digital solutions.

The company designs advanced coil architectures and imaging technologies that support high-resolution MRI examinations across healthcare facilities worldwide. Industry competitors continue to introduce next-generation coil systems, strengthen clinical partnerships, and expand imaging technology portfolios to advance diagnostic accuracy and operational efficiency in medical imaging.

Top Key Players

- GE Healthcare

- Koninklijke Philips N.V.

- Siemens Healthineers AG

- Canon Medical Systems Corporation

- Esaote S.p.A.

- MR Instruments, Inc. (MRIi)

- Rapid MR International, LLC.

- ScanMed, LLC.

- Noras MRI Products GmbH

Recent Developments

- In February 2026, Philips introduced the InkSpace Imaging Snuggle pediatric body array coil for its 3.0T MRI platforms. The wearable and flexible coil design is intended to improve comfort during pediatric scans while maintaining strong signal quality needed for accurate diagnostic imaging.

- During RSNA 2025, Canon Medical Systems highlighted its vertical integration strategy for MRI technology. The approach focuses on producing RF coils and magnet components internally while combining them with its PIQE deep-learning image reconstruction technology to support higher scanning efficiency in clinical environments.

- In early 2026, Noras MRI Products marked its 40th anniversary by highlighting the role of its LUCY OR Head Holder and 8-channel coil system in a clinical brain-computer interface trial conducted in China. The technology demonstrates how specialized MRI coil systems support advanced neurosurgical and neurotechnology research.

- Throughout 2025, MRI manufacturers also expanded the development of coil systems designed for ultra-low-field scanners such as 0.55T platforms. These coil designs support imaging for interventional procedures and help improve accessibility for patients who may face challenges undergoing scans in higher-field MRI systems.

Report Scope

Report Features Description Market Value (2025) US$ 10.0 Billion Forecast Revenue (2035) US$ 23.2 Billion CAGR (2026-2035) 8.8% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Radiofrequency Coils and Gradient Coils), By Application (Brain and Neurology, Spine and Musculoskeletal, Cardiac and Vascular, Abdominal and Pelvic, Breast Imaging, Pediatric Imaging and Others), By End User (Hospitals, Diagnostic Imaging Centers, Ambulatory Surgical Centers and Research and Academic Institutes) Regional Analysis North America – The US, Canada; Europe – Germany, France, The U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape GE Healthcare, Koninklijke Philips N.V., Siemens Healthineers AG, Canon Medical Systems Corporation, Esaote S.p.A., MR Instruments, Inc. (MRIi), Rapid MR International, LLC., ScanMed, LLC., Noras MRI Products GmbH. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Magnetic Resonance Imaging Coils MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Magnetic Resonance Imaging Coils MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- GE Healthcare

- Koninklijke Philips N.V.

- Siemens Healthineers AG

- Canon Medical Systems Corporation

- Esaote S.p.A.

- MR Instruments, Inc. (MRIi)

- Rapid MR International, LLC.

- ScanMed, LLC.

- Noras MRI Products GmbH

Our Clients

- 181991

- March 2026