Quick Navigation

Report Overview

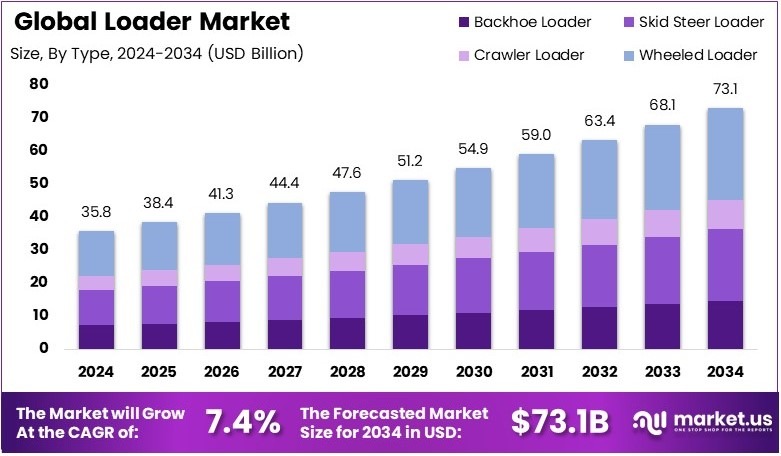

The Global Loader Market size is expected to be worth around USD 73.1 Billion by 2034, from USD 35.8 Billion in 2024, growing at a CAGR of 7.4% during the forecast period from 2025 to 2034.

A loader is a heavy construction machine used to move materials like soil, sand, and debris. It has a front-mounted bucket for lifting and transporting loads. Loaders are commonly used in construction, agriculture, and mining. They help speed up work by reducing manual labor and improving efficiency.

The loader market includes the sale, production, and demand for loaders worldwide. Growth is driven by construction, mining, and infrastructure projects. Companies invest in new technologies like automation and fuel efficiency. Key players focus on innovation to meet industry needs. Market trends include electric loaders and smart control systems.

With urban expansion, loaders are essential for road building, land clearing, and material handling. Moreover, they enhance operational efficiency in large infrastructure projects and industrial applications.

According to the Indian government’s Sagarmala Programme, 839 projects are planned with an investment of ₹5.48 lakh crore by 2035. As of 2023, 241 projects worth ₹2.32 lakh crore have been completed, while 234 projects worth ₹2.22 lakh crore are under development. This large-scale investment increases demand for loaders, as construction companies require advanced equipment to meet project deadlines and efficiency standards.

Consequently, the loader market is experiencing steady growth. Countries investing in infrastructure, such as India and China, drive demand for construction machinery. Moreover, urbanization fuels the need for loaders in real estate and road development. Manufacturers are focusing on technological advancements, such as automation and electric-powered loaders, to meet environmental regulations and efficiency demands.

Furthermore, competition in the loader market is rising as both established and new players seek market share. Leading companies invest in research and development to introduce energy-efficient and high-performance loaders. Meanwhile, price-sensitive buyers in developing economies create opportunities for budget-friendly models. The market remains unsaturated, providing room for growth and innovation.

Key Takeaways

- The Loader Market was valued at USD 35.8 billion in 2024 and is expected to reach USD 73.1 billion by 2034, with a CAGR of 7.4%.

- In 2024, Wheeled Loader dominated the type segment with 37.7%, driven by its versatility across construction and industrial applications.

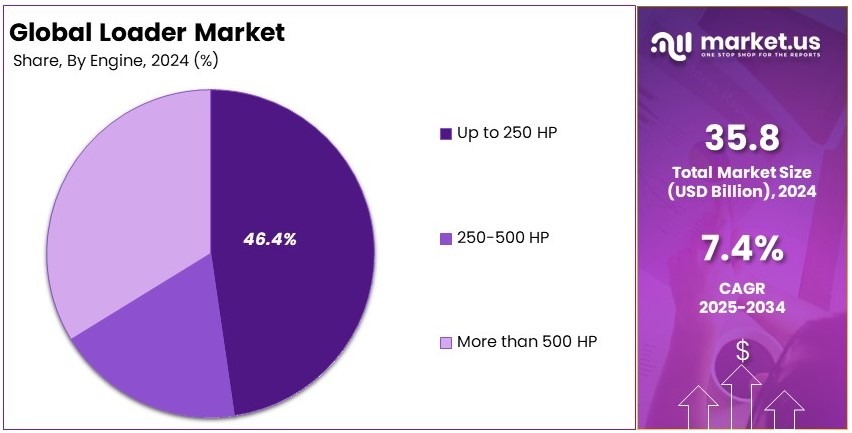

- In 2024, Up to 250 HP engines led the market with 46.4%, offering a balance of power and fuel efficiency.

- In 2024, ICE-powered loaders accounted for 77.2%, owing to their higher power output and widespread availability of fuel infrastructure.

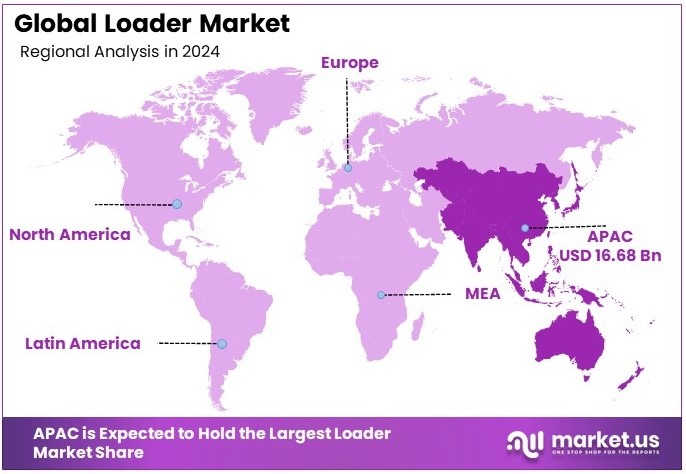

- In 2024, Asia Pacific held the largest market share at 46.6% (USD 16.68 billion), supported by increasing construction and mining activities.

Type Analysis

Wheeled Loader dominates with 37.7% due to its versatility and efficiency in operations.

In the Loader Market segmented by type, the Wheeled Loader emerges as the dominant sub-segment, capturing 37.7% of the market. This dominance stems from their ability to operate across various terrains and undertake multiple tasks efficiently, making them indispensable in construction and mining operations. Their lower maintenance and operational costs further bolster their preference among users, driving their significant market share.

Furthermore, Backhoe Loaders, while versatile, primarily serve smaller construction and utility projects. Their dual functionality for excavation and loading, though valuable, positions them behind Wheeled Loaders in market prominence.

Moreover, Skid Steer Loaders, known for their compact design, are ideal for urban construction sites where space is limited. Their maneuverability and the ability to operate in confined spaces enhance their utility, contributing distinctly to the market’s diversity.

Conversely, Crawler Loaders are tailored for challenging terrains where typical loaders falter. Despite their lesser prevalence compared to wheeled variants, their robustness in harsh conditions underscores their critical role in specific construction and mining applications, thus supporting overall market growth.

Engine Analysis

Up to 250 HP leads with 46.4% owing to its widespread application in varied operational environments.

In the engine power segment, loaders equipped with up to 250 HP engines dominate, holding a 46.4% share. This segment’s predominance is primarily due to the perfect balance these engines strike between delivering sufficient power and maintaining fuel efficiency, making them suitable for a wide array of loading tasks. Additionally, their lower operational costs and minimal environmental impact align well with the increasing global focus on sustainability.

Subsequently, engines in the 250-500 HP range are tailored for more demanding tasks, finding their niche in larger-scale operations that require additional power. Although they cater to a more specialized market segment, their capability to handle intensive loading tasks is indispensable.

On the other hand, engines with more than 500 HP are essential for the most demanding applications, such as large-scale mining and earthmoving. Their smaller market share does not diminish their importance; rather, it highlights their specialized role in supporting high-capacity operations where extreme power is a necessity.

Fuel Analysis

ICE dominates with 77.2% due to its reliability and established presence in the market.

Regarding fuel types, Internal Combustion Engines (ICE) hold a commanding lead, constituting 77.2% of the market. This significant share is largely due to the proven reliability and efficiency of ICE in heavy-duty machinery. The extensive availability of diesel and the robust performance of ICE loaders under rigorous conditions continue to make them the preferred choice in the market.

Nevertheless, the role of Electric loaders is rapidly expanding as environmental regulations become stricter and technological advancements improve their performance. Currently, they represent a smaller portion of the market but are poised for growth. This shift is driven by the industry’s movement towards sustainable practices and lower emissions, marking Electric loaders as integral to the future of the loader market, where they are expected to play an increasingly prominent role.

Key Market Segments

By Type

- Backhoe Loader

- Skid Steer Loader

- Crawler Loader

- Wheeled Loader

By Engine

- Up to 250 HP

- 250-500 HP

- More than 500 HP

By Fuel

- Electric

- ICE

Driving Factors

Infrastructure Expansion and Technological Advancements Drive Market Growth

The rapid growth of infrastructure projects worldwide is boosting the demand for loaders. Urbanization and industrialization are leading to the construction of new roads, highways, and residential complexes. This requires efficient machinery to handle materials and speed up operations.

Additionally, governments are investing heavily in smart infrastructure, which increases the need for advanced loaders with automation capabilities. Another major driver is the rise of autonomous and AI-powered loaders. These machines improve productivity by reducing human effort and errors. They also enhance safety by minimizing accidents on construction sites.

The mining industry is another key factor pushing the loader market forward. As demand for minerals rises, mining companies require high-capacity loaders to move large quantities of materials efficiently. Many companies are also focusing on energy-efficient loaders to meet sustainability goals.

In this context, manufacturers are developing smart loaders equipped with IoT technology. These machines provide real-time data to operators, improving performance and reducing downtime. With ongoing technological advancements and increased investments in infrastructure, the loader market is set to experience steady growth.

Restraining Factors

High Costs and Regulatory Constraints Restrain Market Growth

The high cost of loaders, including their initial investment and maintenance, is a significant challenge for buyers. Small and medium-sized construction firms struggle to afford these machines, limiting their adoption. Additionally, the operational costs of loaders are rising due to fuel consumption and spare parts expenses.

Another barrier is the stringent emission regulations placed on diesel-powered loaders. Governments worldwide are enforcing strict environmental policies to reduce carbon emissions. As a result, manufacturers must invest in cleaner technologies, increasing production costs.

The market is also highly competitive, with established players offering advanced models at competitive prices. This makes it difficult for new entrants to gain a foothold. Moreover, price fluctuations in raw materials, such as steel and rubber, impact manufacturing costs.

Sudden increases in material costs can force companies to raise prices, affecting sales. These challenges create pressure on both manufacturers and buyers. However, with a shift toward electric loaders and better financing options, some of these concerns may be addressed in the coming years.

Growth Opportunities

Electric and Smart Loaders Provide Opportunities for Growth

The shift toward electric and hybrid loaders is creating new opportunities in the market. Companies are focusing on reducing their carbon footprint, and electric loaders help in achieving this goal. These machines produce lower emissions and have lower operating costs compared to traditional diesel-powered models.

Another promising area is the integration of IoT and AI in loaders. Smart loaders equipped with real-time monitoring systems help in improving efficiency and reducing breakdowns. Construction firms are adopting these advanced machines to enhance project timelines and cut costs.

Compact loaders are also gaining popularity, especially in urban areas where space is limited. Small-scale construction projects require versatile and easy-to-maneuver equipment, driving demand for these models. Emerging markets offer another growth avenue.

Countries investing in infrastructure development, such as India and Brazil, are increasing their spending on heavy machinery. As a result, global manufacturers have opportunities to expand their reach in these regions. These trends indicate that the loader market will continue to evolve, with technology and sustainability playing key roles in future growth.

Emerging Trends

Rental Services and Automation Are Latest Trending Factors

The rise of rental and leasing services is changing the way companies acquire loaders. Many businesses prefer renting instead of purchasing to save on upfront costs and maintenance expenses. This trend is especially strong among small construction firms and contractors.

Another major shift is the increasing use of automation in loader operations. Remote-controlled and autonomous loaders are becoming more common, enhancing efficiency and safety. These machines reduce human labor and improve precision in material handling.

Additionally, 3D printing is gaining traction in loader manufacturing. Companies are using this technology to create durable and lightweight components, reducing production costs and material waste.

Loader manufacturers are also focusing on operator safety and comfort. New models come with ergonomic cabin designs, better visibility, and improved control systems. These advancements ensure that operators work efficiently without fatigue. With automation, digitalization, and sustainability at the forefront, the loader market is set to experience significant transformations in the coming years.

Regional Analysis

Asia Pacific Dominates with 46.6% Market Share

Asia Pacific leads the Loader Market with a 46.6% share, representing a value of USD 16.68 billion. This dominant position is fueled by rapid urbanization, significant infrastructure developments, and increasing investments in construction and mining sectors across the region.

The region’s vast manufacturing base and growing adoption of technologically advanced machinery drive demand. Countries like China, India, and Japan are key players, with their large-scale infrastructure projects and increasing technological integration in construction practices.

The future of the Asia Pacific in the Loader Market looks promising, with expected continued growth driven by urban expansion and increased governmental focus on infrastructure. The region’s influence is projected to expand, solidifying its position as a critical market for loaders globally.

Regional Mentions:

- North America: North America maintains a strong presence in the Loader Market, backed by advanced technological adoption and sustained investments in construction and mining. The region’s robust economic policies support the growth of loader manufacturing and deployment.

- Europe: Europe’s loader market is propelled by stringent safety regulations, environmental concerns, and the adoption of cutting-edge technology in machinery. The region focuses on energy-efficient and environmentally friendly loaders, reflecting its commitment to sustainability.

- Middle East & Africa: The Middle East and Africa are witnessing gradual growth in the Loader Market due to increased construction activities and infrastructure development, particularly in countries like Saudi Arabia and the UAE, which are investing heavily in transforming their urban landscapes.

- Latin America: Latin America shows growth potential in the Loader Market, driven by urbanization and industrialization, especially in major economies such as Brazil and Mexico. The region’s focus on improving infrastructure and construction capacities supports the demand for advanced loaders.

Key Regions and Countries Covered in the Report

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Landscape

In the Loader Market, the top four companies—Caterpillar, CNH Industrial N.V., Doosan Bobcat, and Hitachi Construction Machinery Co., Ltd.—play pivotal roles. Caterpillar, leading the pack, is renowned for its extensive range of loaders, characterized by robust performance and innovative technology. This company’s strong global network and commitment to sustainability drive its market dominance.

Next, CNH Industrial N.V. stands out with its comprehensive portfolio and strategic focus on fuel efficiency and automation in machinery design. This approach meets the growing demand for environmentally friendly and cost-effective solutions.

Doosan Bobcat is known for its compact equipment, including skid steer loaders, which are favored in small construction and landscaping projects. Their machines are appreciated for their versatility and agility, catering to various market segments. Hitachi Construction Machinery Co., Ltd. complements the top players with its focus on reliability and advanced technologies. Hitachi has invested heavily in developing electric and hybrid models, responding to the industry’s push towards reducing carbon footprints.

These leaders shape the Loader Market through continuous innovation, strategic global expansions, and by driving trends toward automation and sustainability. Their efforts not only dominate the market landscape but also set competitive standards that influence overall market growth and technology adoption.

Major Companies in the Market

- Caterpillar

- CNH Industrial N.V.

- Doosan Bobcat

- Hitachi Construction Machinery Co., Ltd.

- Hyundai Construction Equipment Co., Ltd.

- J C Bamford Excavators Ltd.

- AB Volvo

- Kobelco Construction Machinery Co., Ltd.

- Komatsu

- Liebherr

- Others

Recent Developments

- Consolidated Equipment Group and Agile Manufacturing: On October 2024, Consolidated Equipment Group, LLC acquired Agile Manufacturing Group, LLC, known for its innovative agricultural, industrial, and construction material handling equipment. This strategic move aims to enhance Consolidated Equipment Group’s product offerings and expand its market presence.

- Bourque Logistics and Sixth Street: In February 2025, Bourque Logistics secured growth financing exceeding $100 million from Sixth Street. This capital infusion supports Bourque Logistics’ recent acquisition of AllTranstek, aiming to bolster its services in the logistics sector.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 35.8 Billion |

| Forecast Revenue (2034) | USD 73.1 Billion |

| CAGR (2025-2034) | 7.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Backhoe Loader, Skid Steer Loader, Crawler Loader, Wheeled Loader), By Engine (Up to 250 HP, 250-500 HP, More than 500 HP), By Fuel (Electric, ICE) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Caterpillar, CNH Industrial N.V., Doosan Bobcat, Hitachi Construction Machinery Co., Ltd., Hyundai Construction Equipment Co., Ltd., J C Bamford Excavators Ltd., AB Volvo, Kobelco Construction Machinery Co., Ltd., Komatsu, Liebherr, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |