Quick Navigation

Report Overview

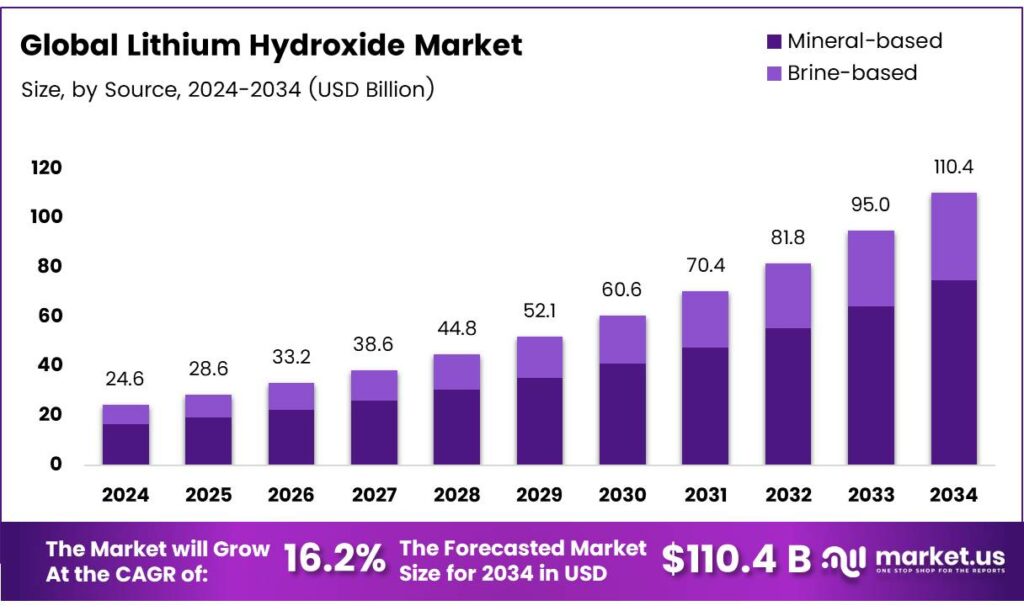

The Global Lithium Hydroxide Market size is expected to be worth around USD 110.4 billion by 2034, from USD 24.6 billion in 2024, growing at a CAGR of 16.2% during the forecast period from 2025 to 2034.

Lithium hydroxide is the chemical compound LiOH. It forms as an intermediate during the hydrolysis of lithium hydride (LiH) and reacts further with water to yield the monohydrate, LiOH·H₂O. The anhydrous form appears as a clear to water-white liquid with a possible pungent odor. It causes severe irritation to the skin, eyes, and mucous membranes and is toxic by ingestion, inhalation, or skin absorption. It serves primarily as a precursor for other lithium chemicals.

At room temperature, the stable form is the non-deliquescent monohydrate (LiOH·H₂O), produced by reacting lithium metal or LiH with H₂O. Heating above 423 K (150 °C) drives off the water of crystallization to form anhydrous LiOH, which melts at 735 K (462 °C), higher than the melting points of NaOH or KOH. Unlike other alkali hydroxides, LiOH decomposes upon further heating to Li₂O and H₂O. Overall, LiOH exhibits milder chemical behavior, resembling alkaline-earth hydroxides more than typical alkali hydroxides.

- In a representative procedure, LiOH (25 mL of 0.1 N aqueous solution) was added to compound 7 (1 g, 2.17 mmol) in aqueous THF (25 mL, 1:1 v/v). The mixture was stirred at 25 °C for 1 h. Acidification followed by extraction into CH₂Cl₂ (2 × 20 mL) and immediate treatment of the extracts with ethereal diazomethane yielded, after drying (MgSO₄), concentration in vacuo, and silica chromatography, methyl (5SR,6SR)-5-hydroxy-6-phenylselenyleicosa-cis, cis,cis-8,11,14-trienoate (8) (860 mg) as a colorless oil.

The electrolyte consists of a concentrated aqueous solution of KOH, NaOH, and LiOH (typically 5–9 mol L⁻¹). Composition is tailored to balance high-rate capability, low- and high-temperature performance, and cycle life. Higher concentrations promote the α/ γ nickel electrode reaction, boosting positive-electrode efficiency but increasing swelling and shortening life. Additions of NaOH and LiOH enhance high-temperature behavior at the positive electrode while impairing low-temperature and high-rate discharge at the cadmium negative electrode.

Key Takeaways

- The Global Lithium Hydroxide Market is projected to grow from USD 24.6 billion in 2024 to USD 110.4 billion by 2034 at a 16.2% CAGR.

- Mineral-based source dominated in 2024 with a 67.9% share due to abundant hard-rock deposits and consistent battery-grade quality.

- Battery Grade led in 2024 with 59.8% share, driven by high purity for NMC cathodes and EV energy storage innovation.

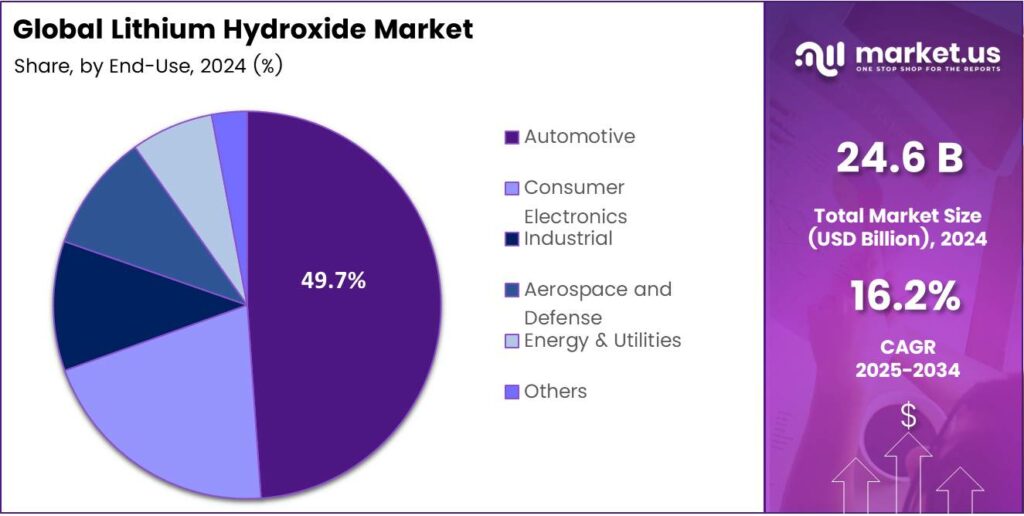

- Automotive end-use held a 49.7% share in 2024, fueled by superior energy density in EV batteries and supplier partnerships.

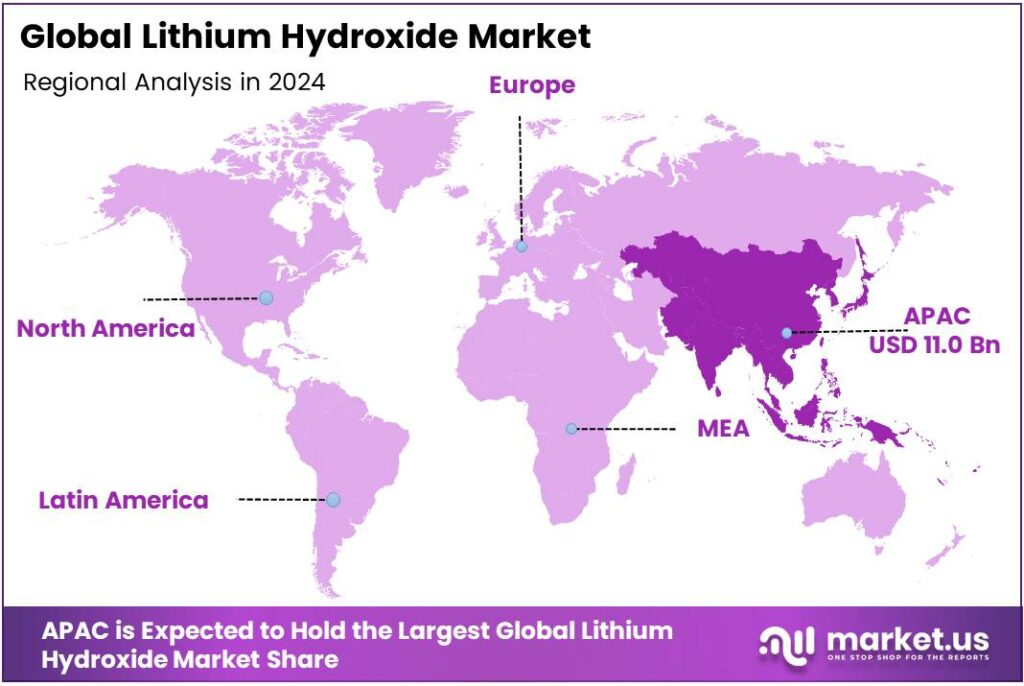

- Asia-Pacific commanded a 44.8% share (USD 11.0 billion) in 2024, propelled by EV adoption, battery production, and clean energy policies.

By Source

Mineral-based dominates with 67.9% due to its reliable supply from spodumene mining and established processing chains.

In 2024, Mineral-based held a dominant market position in the By Source Analysis segment of the Lithium Hydroxide Market, with a 67.9% share. This segment thrives because it draws from abundant hard-rock deposits, ensuring steady production. Manufacturers favor it for consistent quality in battery applications.

Moreover, advances in extraction techniques boost efficiency, making mineral-based lithium hydroxide a go-to choice. It supports the surging demand from electric vehicles effectively. Brine-based sources contribute significantly, leveraging evaporation ponds in salt flats for cost-effective recovery.

This method reduces energy use compared to mining, appealing to eco-conscious producers. Although it faces water scarcity issues, innovations in direct lithium extraction accelerate growth. Brine-based thus emerges as a vital alternative, enhancing supply diversity. It promises scalability for future market needs seamlessly.

By Grade

Battery Grade dominates with 59.8% due to its critical role in high-performance lithium-ion batteries for EVs.

In 2024, Battery Grade held a dominant market position in the By Grade Analysis segment of the Lithium Hydroxide Market, with a 59.8% share. High purity levels meet stringent requirements for advanced cathodes like NMC. This grade drives innovation in energy storage, powering longer-range vehicles. Producers invest heavily here, fueled by global electrification trends.

Battery Grade thus leads, propelling the sector forward dynamically. Technical Grade serves diverse applications with balanced purity and affordability. It excels in lubricants and greases, where reliability matters most. Industries adopt it for cost savings without compromising performance. This segment grows steadily, bridging high-end and basic needs effectively.

Technical Grade ensures broad accessibility across manufacturing lines. Industrial Grade focuses on bulk uses like glass and ceramics production. Its robust properties withstand harsh conditions, aiding durable materials. Factories rely on it for efficiency in large-scale operations. Though less pure, Industrial Grade sustains foundational industries reliably. It complements premium grades, maintaining market balance.

By End-Use

Automotive dominates with 49.7% due to the explosive growth in electric vehicle battery demands.

In 2024, Automotive held a dominant market position in the By End-Use Analysis segment of the Lithium Hydroxide Market, with a 49.7% share. EV manufacturers prioritize it for superior energy density in batteries. This fuels global transitions to sustainable transport swiftly. Partnerships with suppliers secure volumes, driving innovation.

Automotive thus anchors expansion, electrifying roads worldwide. Consumer Electronics utilizes lithium hydroxide in compact batteries for devices like smartphones. Portability demands high efficiency, which this end-use delivers consistently. Gadget makers integrate it for longer life cycles, boosting user satisfaction.

Consumer Electronics grows with tech advancements, keeping pace with daily connectivity needs. Industrial applications harness lithium hydroxide in energy storage and manufacturing processes. It supports grid stability and heavy machinery lubrication effectively. Factories value its versatility for uninterrupted operations. Industrial end-use expands with renewable integrations, fortifying infrastructure resilience steadily.

Key Market Segments

By Source

- Mineral-based

- Brine-based

By Grade

- Battery Grade

- Technical Grade

- Industrial Grade

By End-Use

- Automotive

- Consumer Electronics

- Industrial

- Aerospace and Defense

- Energy and Utilities

- Others

Emerging Trends

Policy-driven onshoring of battery-grade lithium hydroxide

A clear trend is the rapid onshoring and regional diversification of lithium hydroxide refining to cut supply risk and align with clean-energy policies. The EU’s Critical Raw Materials Act (CRMA) sets 2030 benchmarks of 10% domestic extraction, 40% processing, and 25% recycling of strategic raw materials.

In 2024, the U.S. Department of Energy announced USD 3 billion across 25 projects to build new domestic capacity across the battery materials chain, explicitly including lithium. These targets and funds are pushing mid-stream conversion capacity (spodumene/brine → lithium hydroxide) closer to end-markets. Australia illustrates how resource nations are moving up the value chain.

- Western Australia reports commercial production of lithium hydroxide at Kwinana 25,000 t/yr and Kemerton 50,000 t/yr, with a third plant under construction, evidence of a shift from exporting concentrate to exporting refined chemicals. Even as some expansions paused during the 2024–2025 price slump, state and federal strategies continue to position WA as a processing hub.

Drivers

Escalating electric-vehicle and energy-storage demand

- One of the most powerful factors driving growth in the market for lithium hydroxide is the surge in demand for batteries, especially for electric vehicles (EVs) and large-scale energy storage systems. According to the U.S. Geological Survey (USGS), global lithium consumption in 2023 was about 180,000 tons, a 27% increase over the 2022 figure of 142,000 tons — clearly showing strong growth tied to battery markets.

The International Energy Agency (IEA) further highlights that in the Stated Policies Scenario, battery demand for EVs is forecast to reach more than 3 terawatt-hours (TWh), up from roughly 1 TWh in 2024. Because lithium hydroxide is a preferred feedstock for high-nickel cathode chemistries used in long-range EVs, this rapid expansion of battery capacity directly raises demand for lithium hydroxide as opposed to other lithium compounds.

The leap in battery-related demand isn’t just incremental — it’s a structural shift. The USGS and IEA data show we’re not talking about maturity but about rapid scaling. Because lithium hydroxide is especially suitable for next-generation battery chemistries (nickel-rich NMC or NCA systems), the growth in battery demand is lifting its importance in the broader lithium portfolio.

Restraints

Price volatility and permitting squeeze investment

The biggest restraint on lithium hydroxide right now is simple: investment keeps getting whiplashed by prices and permitting. In 2024, spot lithium hydroxide prices in China fell from about USD 17,000/ton in January to about USD 9,900/ton in November, while spodumene also slid sharply. Those swings make bankers and boards pause on new conversion plants or expansions.

- At the same time, developers face a permitting reality that is slower and stricter, especially where water is scarce. In Chile’s Salar de Atacama, operators have committed to cutting freshwater use by 50%, and technical plans reference limiting brine extraction to 120 L/s. These measures protect fragile ecosystems, but they also raise compliance costs, add monitoring, and can cap output growth that would feed hydroxide refineries.

Policy uncertainty adds another brake. The U.S. Department of Energy terminated a USD 57.7 million grant tied to a proposed lithium hydroxide facility, underscoring that public funding can be revised mid-stream. For companies planning multi-billion-dollar supply chains, that kind of reversal forces contingency budgeting and slows final investment decisions.

Opportunity

Rising demand for high-purity battery chemicals

The Lithium Hydroxide market is the shift in battery chemistry toward high-nickel cathodes, which require ultra-high-purity lithium hydroxide rather than standard lithium carbonate. The International Energy Agency (IEA) reports that more than 80% of global lithium-chemical refining capacity for lithium hydroxide is concentrated in China, underlining how scarce and specialized this refining route has become.

IEA

This refinement bottleneck matters because automakers and battery manufacturers are accelerating production of long-range electric vehicles (EVs) and grid-storage systems, both of which increasingly rely on cathode chemistries like NCM 811 or NCA that favour lithium hydroxide for performance, stability, and longer cycle-life. That trend directly translates into growth in lithium hydroxide demand independent of overall lithium volumes.

Governments are backing this move. Under the Inflation Reduction Act (IRA) in the U.S., tax credits and incentives support battery manufacturing and chemical-processing facilities, indirectly lifting demand for battery-grade lithium hydroxide. Similarly, the European Critical Raw Materials Act (CRMA) sets processing-capacity targets to build domestic chemical value-chains — a signal that refined lithium chemicals will be strategically important.

Regional Analysis

Asia-Pacific leads with a 44.8% share and a USD 11.0 Billion market value.

In 2024, Asia-Pacific held a dominant 44.8% share, valued at USD 11.0 billion, leading the global lithium hydroxide market. The region’s leadership is driven by large-scale electric vehicle (EV) adoption, extensive lithium-ion battery production, and active government support for clean energy transition.

China, Japan, and South Korea remain at the core of battery manufacturing, hosting major players such as CATL, LG Energy Solution, and Panasonic, which collectively influence global lithium hydroxide demand. China’s National Energy Administration continues to push EV penetration, significantly boosting domestic lithium conversion capacity.

Australia contributes heavily as the largest lithium ore supplier, with companies such as Pilbara Minerals and Tianqi Lithium expanding spodumene production for downstream processing in Asia. Tianqi and IGO Ltd. announced capacity expansions at the Kwinana refinery, reinforcing the region’s integrated value chain.

Japan’s Ministry of Economy, Trade, and Industry (METI) introduced funding programs to secure strategic lithium supplies and recycling initiatives. These combined policy and industrial efforts strengthen Asia-Pacific’s role as the central hub for lithium refining and cathode production. With strong local manufacturing ecosystems and rising EV adoption, the Asia-Pacific is expected to maintain its dominant position.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Albemarle leverages its extensive, diversified lithium portfolio and strong foothold in key regions like North America. Its scale and vertical integration into both brine and hard rock resources provide a significant competitive edge. The company’s long-term contracts and major investments in expanding lithium hydroxide capacity position it to meet rising demand, particularly from the electric vehicle sector.

Ganfeng Lithium is a vertically integrated Chinese giant, controlling the supply chain from resources to battery production. Its aggressive global acquisition of mining assets ensures raw material security. The company is a key supplier to major battery manufacturers and automakers, fostering strong, long-term customer relationships. Continuous capacity expansion for high-purity lithium hydroxide solidifies.

Tianqi Lithium’s strength stems from its significant ownership in the world’s premier lithium resource, the Greenbushes mine in Australia. This strategic asset provides a low-cost, high-quality spodumene supply, which is crucial for producing lithium hydroxide. While financially leveraged, this resource backbone grants it immense influence over the raw material market.

Top Key Players in the Market

- Albemarle Corporation

- Ganfeng Lithium Co., Ltd

- Tianqi Lithium Corporation

- Mineral Resources Limited

- Pilbara Minerals Limited

- Yahua Group

- Chengxin Lithium Group

- AMG Lithium

- Nemaska Lithium

- Sichuan Energy Investment Development Co., Ltd.

Recent Developments

- In 2025, Albemarle expanded its specialties and began producing energy storage lithium salts, including battery-grade lithium hydroxide, at its integrated conversion facilities. The company achieved record output at its La Negra (Chile) and Meishan (China) plants.

- In 2025, Ganfeng completed Jiangxi Province’s first unsubsidized green certificate transaction, focusing on environmental protection and carbon footprint calculation for lithium carbonate and hydroxide. The company leads the Jiangxi Province lithium industry science and technology innovation consortium for clean extraction and recycling technologies.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 24.6 Billion |

| Forecast Revenue (2034) | USD 110.4 Billion |

| CAGR (2025-2034) | 16.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Source (Mineral-based, Brine-based), By Grade (Battery Grade, Technical Grade, Industrial Grade), By End-Use (Automotive, Consumer Electronics, Industrial, Aerospace and Defense, Energy and Utilities, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Albemarle Corporation, Ganfeng Lithium Co., Ltd, Tianqi Lithium Corporation, Mineral Resources Limited, Pilbara Minerals Limited, Yahua Group, Chengxin Lithium Group, AMG Lithium, Nemaska Lithium, Sichuan Energy Investment Development Co., Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |