Global Land Drilling Rig Market Size, Share Analysis Report By Rig Type (Conventional, Mobile/Wheel-Mounted, Walking Super-Spec), By Drive System (Mechanical, Electric (SCR and AC), Hybrid/Compound), By Horsepower Rating (Up to 1,000 HP, 1,000 to 1,499 HP, Above 1,500 HP), By Application (Conventional Oil, Unconventional/Tight and Shale, Geothermal, Emerging Natural-Hydrogen) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: April 2026

- Report ID: 184074

- Number of Pages: 214

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

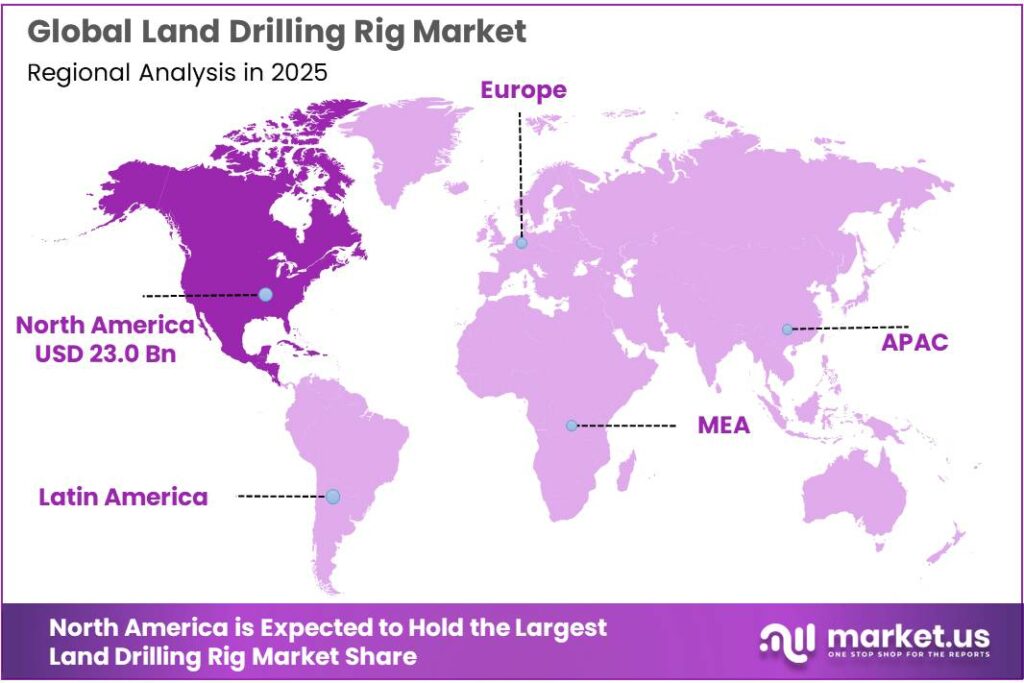

The Global Land Drilling Rig Market size is expected to be worth around USD 85.9 Billion by 2035, from USD 54.6 Billion in 2025, growing at a CAGR of 4.6% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 42.3% share, holding USD 23.0 Billion revenue.

The land drilling rig industry represents the onshore backbone of oil and gas field development, supplying the mechanical capacity needed for exploration, appraisal, development drilling, and workover activity across shale, tight oil, conventional, and gas-bearing basins. In practical terms, the sector is being shaped less by simple rig additions and more by the quality of super-spec assets, automation, pad efficiency, and drilling productivity per crew and per well.

- The United States, where crude oil production reached a record more than 13.6 million barrels per day in July 2025, while the U.S. Energy Information Administration still projected an average of 13.5 million barrels per day for full-year 2025 despite softer price assumptions of $69 per barrel Brent for the year.

From an industry scenario perspective, land drilling remains operationally resilient even when headline rig activity is restrained. Baker Hughes’ North America rig count data shows the market continued to be tracked weekly through April 2, 2026, underscoring the importance of active rig monitoring as a leading indicator for onshore capital deployment.

EIA reported that total U.S. crude oil production climbed from 5.0 million barrels per day in 2008 to 13.2 million barrels per day in 2024, while onshore crude production from federal lands alone reached a record 1.7 million barrels per day in 2024, or roughly 6 times the 2008 level. This indicates that operators are extracting more output from a more selective, efficiency-focused land rig fleet.

The main driving factors for the industry are therefore production optimization, energy security, technology-led cost reduction, and policy support for domestic resource development. On the demand side, the International Energy Agency stated that global oil demand increased by 830 kb/d in 2025, while global oil supply was still expected to rise by 3.0 mb/d in 2025 to 106.2 mb/d, preserving a need for disciplined onshore drilling investment in productive basins.

On the policy side, the U.S. Department of the Interior stated that its first-quarter 2025 oil and gas lease sales generated more than $39.0 million in receipts from 34 parcels covering 25,038 acres, and it added that the Bureau of Land Management planned 15 more lease sales in 2025. Such steps support future land drilling activity by extending acreage access and permitting visibility.

Government and national energy initiatives are also shaping future opportunity. ADNOC approved a USD 150 billion five-year business plan for 2026-2030, while Abu Dhabi’s unconventional resources are estimated at 160 tscf of gas and 22 billion stock tank barrels of oil. Saudi Aramco has stated that Jafurah contains 229 trillion standard cubic feet of raw gas and supports a plan to raise gas production capacity by 60% between 2021 and 2030.

Key Takeaways

- Land Drilling Rig Market size is expected to be worth around USD 85.9 Billion by 2035, from USD 54.6 Billion in 2025, growing at a CAGR of 4.6%.

- Conventional held a dominant market position, capturing more than a 45.8% share.

- Electric (SCR and AC) held a dominant market position, capturing more than a 39.9% share.

- Above 1,500 HP held a dominant market position, capturing more than a 49.2% share.

- Unconventional/Tight and Shale held a dominant market position, capturing more than a 43.7% share.

- North America emerged as the dominant regional market in the land drilling rig industry, accounting for 42.3% of the global market and reaching USD 23.0 billion.

By Rig Type Analysis

Conventional rigs lead the land drilling rig market with a 45.8% share in 2025, supported by their dependable performance across established onshore fields.

In 2025, Conventional held a dominant market position, capturing more than a 45.8% share in the land drilling rig market by rig type. This leadership was mainly supported by its continued use in mature onshore oil and gas fields where drilling conditions are well understood and operational risks are lower. Conventional rigs remain a practical choice for operators focused on steady field development, workover activity, and cost-controlled drilling programs. Their simpler setup, easier maintenance, and strong suitability for vertical and moderately complex wells make them widely preferred across long-established producing regions.

By Drive System Analysis

Electric (SCR and AC) drive systems dominate with a 39.9% share in 2025, driven by better efficiency and stronger control in modern land drilling operations.

In 2025, Electric (SCR and AC) held a dominant market position, capturing more than a 39.9% share in the land drilling rig market by drive system. This strong position was supported by the growing preference for efficient, high-performance rig operations across major onshore drilling programs. Electric drive systems are widely valued for delivering smoother power transmission, better torque control, and improved drilling precision, which are important in both conventional and increasingly complex well designs. Their ability to support consistent speed control and reduce mechanical stress on rig components makes them a preferred choice for contractors aiming to improve uptime and lower maintenance interruptions.

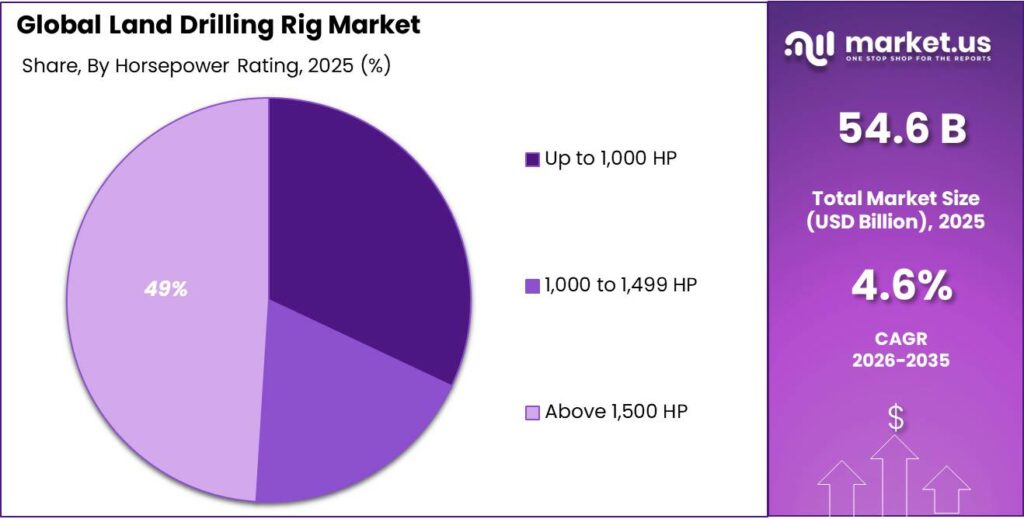

By Horsepower Rating Analysis

Above 1,500 HP rigs dominate with a 49.2% share in 2025, supported by strong demand for deeper and high-intensity onshore drilling programs.

In 2025, Above 1,500 HP held a dominant market position, capturing more than a 49.2% share in the land drilling rig market by horsepower rating. This segment remained in the lead because operators increasingly preferred high-horsepower rigs for deeper wells, longer lateral sections, and multi-well pad drilling projects that require stronger load-handling capacity. These rigs are well suited for demanding onshore environments where higher hook load, better mud pump support, and stronger top drive performance are essential for maintaining drilling speed and well control.

By Application Analysis

Unconventional, tight, and shale drilling leads with a 43.7% share in 2025, backed by continued focus on high-output onshore resource plays.

In 2025, Unconventional/Tight and Shale held a dominant market position, capturing more than a 43.7% share in the land drilling rig market by application. This segment remained the largest because onshore operators continued to prioritize shale and tight resource development for faster production growth and better recovery from established acreage. These drilling programs typically require high-spec land rigs capable of horizontal drilling, longer laterals, and repeated pad-based operations, which keeps rig demand strong in this application area

Key Market Segments

By Rig Type

- Conventional

- Mobile/Wheel-Mounted

- Walking Super-Spec

By Drive System

- Mechanical

- Electric (SCR and AC)

- Hybrid/Compound

By Horsepower Rating

- Up to 1,000 HP

- 1,000 to 1,499 HP

- Above 1,500 HP

By Application

- Conventional Oil

- Unconventional/Tight and Shale

- Geothermal

- Emerging Natural-Hydrogen

Emerging Trends

Rig Automation and Robotics Are Becoming the Defining Market Trend

One of the most important latest trends in the land drilling rig market is the fast shift toward automation, robotics, and digitally controlled rig floors. In 2025 and moving into 2026, operators are increasingly choosing rigs that can reduce manual intervention, improve repeatability, and make drilling safer in shale and long-lateral wells. This trend is no longer experimental—it is already active in field operations.

A strong example comes from Nabors, whose fully automated PACE®-R801 land rig has already demonstrated real horizontal well drilling capability, including a 19,917-foot measured depth well in the Permian. The company also stated that use of its automation suite helped reduce drilling time by 4 days per well in major basins. This matters because every day saved directly improves operator economics and raises the value of advanced rigs.

Retrofit Robotics on Existing Fleets Is Expanding Fast

Another major trend is the rise of retrofit-ready robotic systems on active land rig fleets, allowing contractors to modernize existing assets instead of replacing them fully. This is making advanced drilling technology more commercially practical in 2025. A strong recent example is Helmerich & Payne’s FlexRobotics™, which made its field debut in the Permian and completed a pad-to-pad rig move in just 44 hours while using fully automated pipe-handling systems.

The importance of this trend is that operators can now improve safety and flat-time performance without waiting for entirely new rig builds. Government-backed energy security programs and national oil companies are also favoring these efficient systems because faster rig moves and reduced red-zone exposure improve both production timelines and workforce safety standards. In simple terms, the market is moving toward smarter rigs that combine legacy fleet strength with modular robotics, digital workflows, and remote operational visibility.

Drivers

Rising Onshore Oil Production is the Core Demand Driver

One major driving factor for the land drilling rig market is the steady rise in onshore oil production, especially from highly productive shale and tight formations. When oil output continues to grow from land-based fields, operators need more reliable rigs for development drilling, infill wells, and longer horizontal sections. This keeps demand strong for high-performance land rigs across active basins.

A clear example comes from the U.S. Energy Information Administration, which reported that U.S. crude oil production reached a record 13.6 million barrels per day in 2025, with the Permian Basin alone contributing 6.6 million barrels per day, or almost half of total output. Even more importantly for land rig demand, EIA noted that onshore crude oil production from federal lands reached 1.7 million barrels per day in 2024, a record level, supported by rising lease approvals and drilling permits.

Government Leasing and Permit Support Strengthens Rig Activity

Another strong growth driver is continued government support for onshore leasing, drilling permits, and well-start approvals in major producing regions. Land drilling rigs depend heavily on how quickly operators can move from lease acquisition to active drilling, so policy support directly influences fleet utilization.

- According to EIA data based on the U.S. Department of the Interior, federal onshore production increased from 3.2 trillion cubic feet of natural gas in 2020 to 4.2 trillion cubic feet in 2024, while oil production on these lands also reached record highs.

The same source highlighted that the majority of drilling permit approvals and wellbore starts were concentrated in key onshore federal areas over recent fiscal years, showing how administrative support converts into actual rig movement. This matters because every new lease block, permit approval, and development plan creates follow-up demand for drilling contractors, rig crews, mud systems, and associated well services. In simple terms, when governments continue to open land acreage and speed up approvals, the land drilling rig market benefits through stronger utilization, better contract visibility, and longer-term deployment opportunities.

Restraints

Oil Price Volatility Remains the Biggest Restraining Factor

One of the biggest restraining factors for the land drilling rig market is oil price volatility, because drilling decisions are directly tied to expected well economics. When crude prices fall sharply or remain uncertain, operators usually delay new drilling programs, reduce rig contracts, and shift spending toward only the most productive acreage. This directly slows rig utilization. A clear example came from the U.S. Energy Information Administration, which forecast Brent crude prices to decline from $81 per barrel in 2024 to $74 in 2025 and further to $66 in 2026.

Lower price expectations like these make many onshore wells less attractive, especially outside top-tier shale zones. The effect can already be seen in field activity trends: EIA reported that the average Lower 48 active rig count dropped from 750 rigs in December 2022 to 517 rigs by October 2025. This kind of price-led spending discipline creates hesitation across exploration and production budgets, making oil price instability one of the most practical restraints on future land rig demand.

Capital Discipline and Fewer Active Rigs Limit Market Expansion

Another major restraint linked to the same issue is the growing focus on capital discipline by operators, even when production remains strong. Many oil and gas companies are now prioritizing shareholder returns, debt reduction, and operational efficiency over aggressive drilling expansion. This reduces the need for additional land rigs. According to EIA, even though U.S. crude oil production reached 13.6 million barrels per day in 2025, the number of active rigs in the Lower 48 was still 5% lower than 2024 levels.

This shows that companies are producing more with fewer rigs through longer laterals, faster drilling cycles, and better completion methods. While this is positive for operator margins, it acts as a restraint for the land drilling rig market because fleet growth does not move in line with production growth.

Opportunity

Rig Automation and High-Spec Upgrades Create the Biggest Growth Opportunity

One of the strongest growth opportunities for the land drilling rig market is the rapid shift toward rig automation, digital controls, and high-spec fleet upgrades. Operators are now looking for rigs that can drill faster, reduce non-productive time, and improve crew safety, especially in shale and long-lateral wells. A strong real-world sign of this opportunity comes from Helmerich & Payne, which reported that its total fleet reached 367 drilling rigs as of September 30, 2025, including 223 rigs in North America and 137 rigs internationally.

This larger modern fleet footprint shows where capital is moving—toward advanced rigs that can support multi-well pad drilling and faster walking times. The opportunity is even stronger in markets where national oil companies are pushing for drilling efficiency and lower well costs. As more operators replace older mechanical and SCR fleets with automated AC rigs, the market gains a clear long-term upgrade cycle that supports new contracts, retrofit demand, and digital drilling service revenue.

Government-Led Energy Expansion and International Newbuild Programs Open New Demand

A second major growth opportunity comes from government-backed onshore energy expansion and long-term international newbuild programs, which directly increase demand for new land rigs. National energy security plans are encouraging more domestic oil and gas development, and this gives drilling contractors better long-term visibility. A good example is Nabors’ 2025 international activity, where the company guided an average international rig count of 85–86 rigs in 2025, showing strong utilization outside North America.

In addition, large-scale programs such as SANAD’s Saudi newbuild rollout continue to support deployment of modern rigs built for long-cycle contracts. These government-linked developments create a major opening for contractors offering high-horsepower, automated, and walking rigs. The real opportunity is not just more wells, but longer contract tenures, better fleet utilization, and expansion into underpenetrated onshore gas basins.

Regional Insights

North America Dominates the Land Drilling Rig Market with 42.3% Share, Reaching USD 23.0 Billion

North America emerged as the dominant regional market in the land drilling rig industry, accounting for 42.3% of the global market and reaching USD 23.0 billion. The region’s leadership is strongly supported by large-scale shale development, strong contractor presence, and widespread deployment of high-horsepower AC and walking rigs across major unconventional basins.

The United States remains the core growth engine, led by the Permian, Eagle Ford, and Bakken plays, where continuous horizontal drilling and pad development sustain strong rig demand. According to the U.S. Energy Information Administration, U.S. crude oil production reached a record 13.6 million barrels per day in 2025, while the Permian Basin alone contributed 6.6 million barrels per day, equal to nearly 48% of total U.S. production. This scale of output directly supports sustained utilization of premium land rigs across the region.

The region also benefits from a highly developed oilfield services ecosystem, rapid rig mobilization capability, and continuous technological upgrades in automation and drilling analytics. Even with improved well productivity, the active drilling base remains substantial. Baker Hughes’ latest North America rotary rig data continued to show more than 700 active rigs in the region during 2025 reporting periods, reflecting resilient field activity across the U.S. and Canada.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Nabors Industries remains one of the strongest players in the land drilling rig market with a 2025 average of 158.3 working rigs globally, including 69.9 rigs in the U.S. and 88.4 rigs internationally. The company’s strength is further supported by its Saudi SANAD expansion and Parker Drilling acquisition completed at approximately $180.6 million in 2025.

Patterson-UTI Energy is a major U.S.-focused land drilling contractor with strong exposure to unconventional shale basins. For the three months ended December 31, 2025, the company averaged 93 active drilling rigs in the United States, showing solid operational scale in the Lower 48 market. The company remains highly competitive due to its super-spec rig fleet, integrated pressure pumping capabilities, and strong relationships with shale-focused E&P operators.

Helmerich & Payne continues to hold a strong market position through its premium FlexRig fleet and growing international footprint. In fiscal 2025, the company reported a global operating footprint of more than 200 rigs, reflecting its expanding role in both U.S. shale and Middle East drilling programs. Its technology-led model, especially in automation and FlexRobotics deployment, supports strong demand in long-lateral and pad drilling applications.

Top Key Players Outlook

- Nabors Industries Ltd

- Helmerich & Payne Inc

- Patterson-UTI Energy Inc

- Precision Drilling Corp

- Schlumberger Ltd

- Weatherford International PLC

- Ensign Energy Services Inc

- KCA Deutag

- ADNOC Drilling

- China Oilfield Services Ltd (COSL)

- Sinopec Zhongyuan Petroleum Eng.

- Borr Drilling Ltd

- Saipem SpA

- Kuwait Drilling Company

- Valaris Ltd

Recent Industry Developments

In 2025, Helmerich And Payne total drilling fleet reached 368 rigs, including 224 rigs in North America, 137 international land rigs, and 7 offshore platform rigs, showing its strong scale across both shale and international onshore markets.

Patterson-UTI Energy remains a major U.S. drilling contractor with strong exposure to shale and other onshore drilling programs. In December 2025, the company reported an average of 93 drilling rigs operating in the United States, and for the three months ended December 31, 2025, it also averaged 93 rigs, showing a stable activity base at year-end.

Report Scope

Report Features Description Market Value (2025) USD 54.6 Bn Forecast Revenue (2035) USD 85.9 Bn CAGR (2026-2035) 4.6% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Rig Type (Conventional, Mobile/Wheel-Mounted, Walking Super-Spec), By Drive System (Mechanical, Electric (SCR and AC), Hybrid/Compound), By Horsepower Rating (Up to 1,000 HP, 1,000 to 1,499 HP, Above 1,500 HP), By Application (Conventional Oil, Unconventional/Tight and Shale, Geothermal, Emerging Natural-Hydrogen) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Nabors Industries Ltd, Helmerich & Payne Inc, Patterson-UTI Energy Inc, Precision Drilling Corp, Schlumberger Ltd, Weatherford International PLC, Ensign Energy Services Inc, KCA Deutag, ADNOC Drilling, China Oilfield Services Ltd (COSL), Sinopec Zhongyuan Petroleum Eng., Borr Drilling Ltd, Saipem SpA, Kuwait Drilling Company, Valaris Ltd Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Nabors Industries Ltd

- Helmerich & Payne Inc

- Patterson-UTI Energy Inc

- Precision Drilling Corp

- Schlumberger Ltd

- Weatherford International PLC

- Ensign Energy Services Inc

- KCA Deutag

- ADNOC Drilling

- China Oilfield Services Ltd (COSL)

- Sinopec Zhongyuan Petroleum Eng.

- Borr Drilling Ltd

- Saipem SpA

- Kuwait Drilling Company

- Valaris Ltd

Our Clients

- 184074

- April 2026