Global Knee Reconstruction Devices Market By Product Type (Cemented Implants, Partial Implants, Cementless Implants and Revision Implants), By Indication (Osteoarthritis, Trauma, Rheumatoid Arthritis and Others), By End User (Hospitals, ASCs and Orthopedic Clinics), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179379

- Number of Pages: 332

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

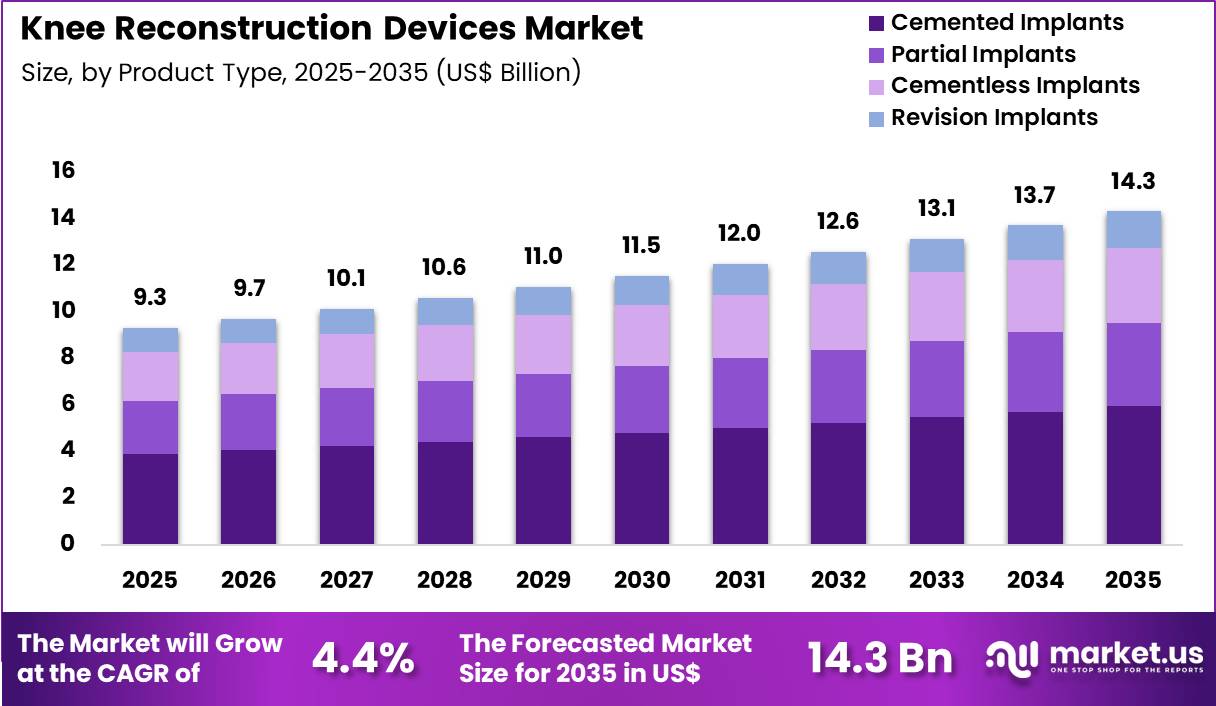

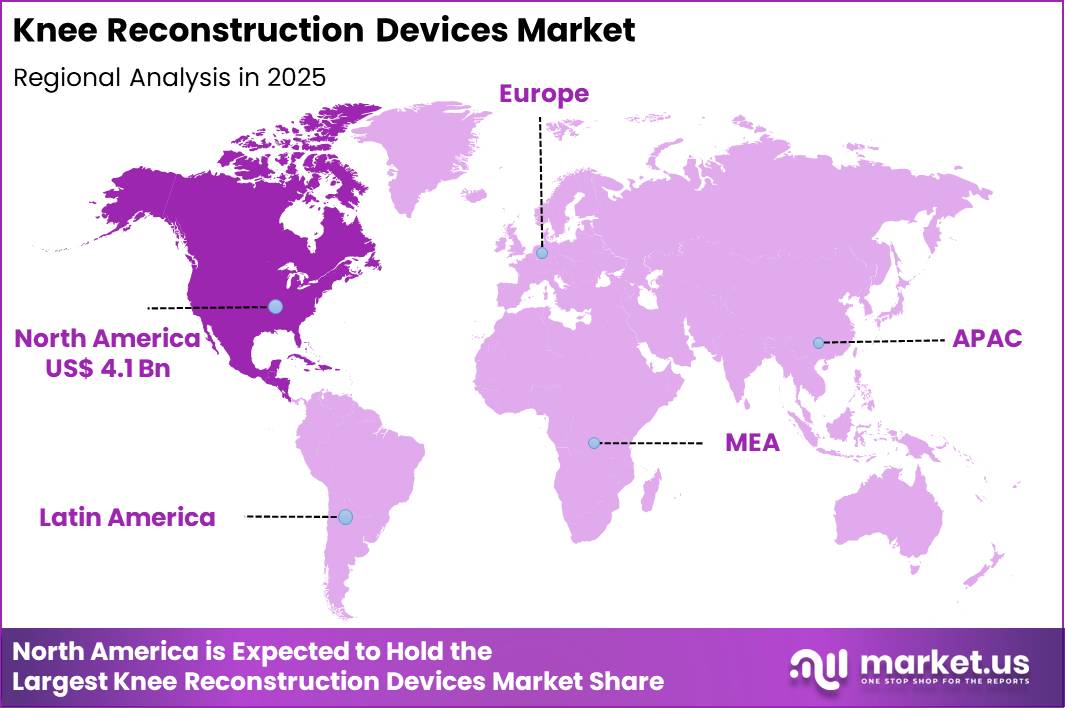

The Global Knee Reconstruction Devices Market size is expected to be worth around US$ 14.3 Billion by 2035 from US$ 9.3 Billion in 2025, growing at a CAGR of 4.4% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 43.7% share with a revenue of US$ 4.1 Billion.

Increasing prevalence of knee osteoarthritis and sports-related injuries accelerates the knee reconstruction devices market as orthopedic surgeons seek advanced implants that restore mobility, alleviate pain, and extend joint longevity.

Surgeons increasingly perform total knee arthroplasty using cemented and cementless femoral and tibial components to replace damaged articular surfaces in patients with end-stage degenerative arthritis, improving range of motion and daily function.

These devices support partial knee replacement for isolated compartment disease, preserving healthy bone and ligaments while addressing medial or lateral compartment wear. Revision knee systems enable complex reconstructions in patients with implant loosening, infection, or periprosthetic fractures, where modular stems and augments restore stability and bone stock.

Patellofemoral arthroplasty targets isolated patellofemoral degeneration, offering targeted resurfacing for younger patients with anterior knee pain. Surgeons also apply knee reconstruction devices in trauma cases to repair tibial plateau fractures or ligament avulsions, utilizing plates and screws to achieve anatomic reduction and early weight-bearing.

Manufacturers pursue opportunities to develop patient-specific implants through 3D printing and preoperative planning software, expanding applications in complex deformities and revision surgeries where standard components fail to address bone loss or malalignment.

Developers advance sensor-embedded smart implants that monitor load distribution and implant stability, broadening utility in postoperative rehabilitation and long-term outcome tracking. These innovations facilitate robotic-assisted knee arthroplasty, improving alignment accuracy and soft tissue balance in primary and revision procedures.

Opportunities emerge in bioactive coatings and porous metals that enhance osseointegration, reducing aseptic loosening risks. Companies invest in gender-specific and high-flexion designs that accommodate diverse anatomies and activity levels. Recent trends emphasize value-based models that prioritize implant longevity and reduced revision rates, positioning the market for growth in personalized, technology-enabled knee reconstruction solutions.

Key Takeaways

- In 2025, the market generated a revenue of US$ 9.3 Billion, with a CAGR of 4.4%, and is expected to reach US$ 14.3 Billion by the year 2035.

- The product type segment is divided into cemented implants, partial implants, cementless implants and revision implants, with cemented implants taking the lead with a market share of 41.7%.

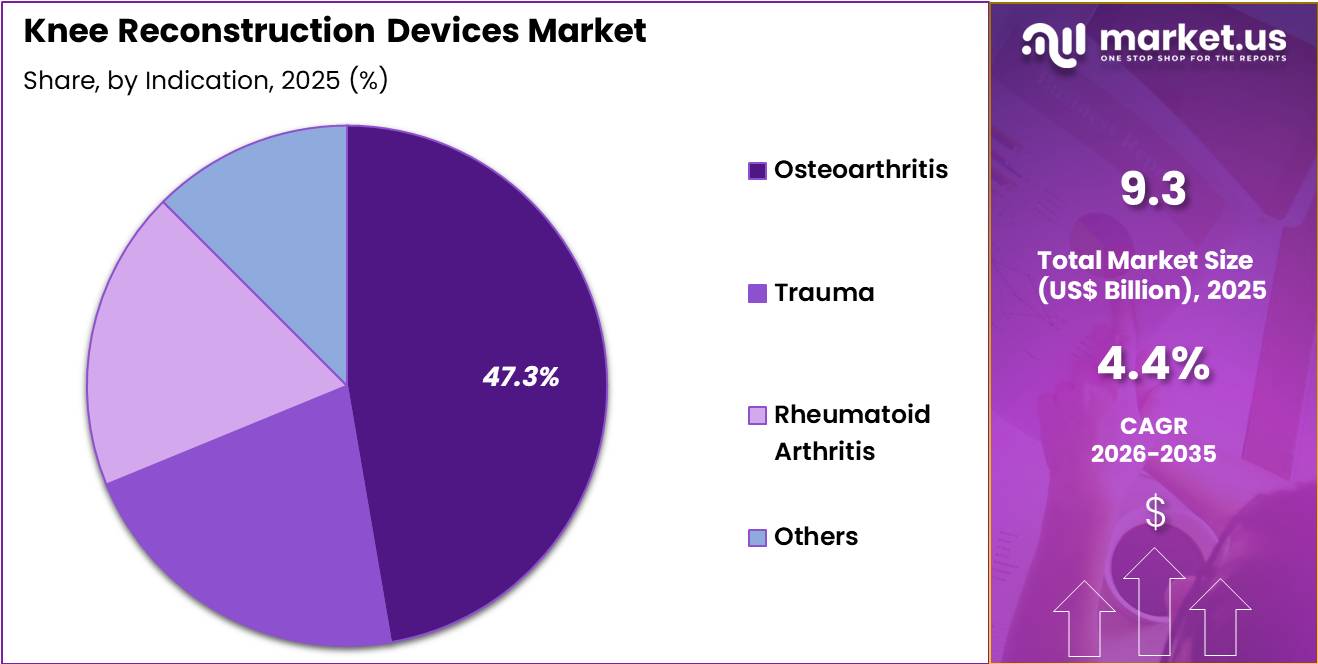

- Considering indication, the market is divided into osteoarthritis, trauma, rheumatoid arthritis and others. Among these, osteoarthritis held a significant share of 47.3%.

- Furthermore, concerning the end user segment, the market is segregated into hospitals, ASCs and orthopedic clinics. The hospitals sector stands out as the dominant player, holding the largest revenue share of 51.2% in the market.

- North America led the market by securing a market share of 43.7%.

Product Type Analysis

Cemented implants accounted for 41.7% of growth within product type and dominate the knee reconstruction devices market due to their long-term stability, proven clinical outcomes, and widespread surgeon familiarity.

The implants’ ability to provide immediate fixation and reduced post-operative complications supports high adoption rates. Advancements in cement formulations improve biocompatibility and handling during surgery, enhancing patient outcomes.

Hospitals and orthopedic centers increasingly use cemented implants for primary and complex knee reconstructions. The segment growth is projected to continue as aging populations and rising osteoarthritis prevalence drive surgical interventions. Enhanced training programs and growing orthopedic expertise further support adoption globally.

Indication Analysis

Osteoarthritis accounted for 47.3% of growth within indications and remains the leading driver of the market. The increasing prevalence of degenerative joint disorders among aging populations, combined with rising obesity rates, fuels demand for knee reconstruction surgeries.

Patients seek solutions for pain relief, mobility restoration, and improved quality of life, boosting device utilization. Hospitals and orthopedic centers implement early intervention programs to prevent disease progression.

Segment growth is expected to strengthen as technological innovations, including patient-specific implants and minimally invasive procedures, enhance surgical precision and recovery. Rising awareness and reimbursement support further drive adoption across developed and emerging regions.

End-User Analysis

Hospitals contributed 51.2% of growth within end-users and dominate due to their capacity for high-volume orthopedic procedures and comprehensive post-operative care. Hospitals provide access to specialized surgical teams, advanced imaging, and rehabilitation services, making them primary sites for knee reconstruction.

The increasing number of joint replacement surgeries and multidisciplinary care models strengthens demand for hospital-based implant services. Segment growth is anticipated to continue as hospitals expand orthopedic departments, adopt robotic-assisted surgery, and implement evidence-based clinical pathways. Collaborations with medical device manufacturers for training and device optimization further enhance adoption and outcomes.

Key Market Segments

By Product Type

- Cemented Implants

- Partial Implants

- Cementless Implants

- Revision Implants

By Indication

- Osteoarthritis

- Trauma

- Rheumatoid Arthritis

- Others

By End User

- Hospitals

- ASCs

- Orthopedic Clinics

Drivers

Increasing prevalence of knee osteoarthritis is driving the market.

The rising incidence of knee osteoarthritis has significantly boosted the demand for knee reconstruction devices, as more patients require surgical interventions to restore joint function and alleviate pain. Enhanced diagnostic tools and greater clinical awareness have led to earlier identification of degenerative joint conditions, expanding the patient pool eligible for reconstruction.

Healthcare providers are increasingly recommending knee replacements for individuals with advanced osteoarthritis that limits mobility. The correlation between obesity, aging, and joint deterioration further amplifies the need for durable implant solutions. Government health organizations emphasize preventive orthopedics to address this public health issue.

Knee reconstruction devices enable improved quality of life for patients with severe joint damage through partial or total replacements. National arthritis statistics document the growing burden of knee-related disabilities, prompting investment in surgical infrastructure.

Key manufacturers are refining implant materials to meet this escalating clinical requirement. This driver fosters innovation in cementless fixation and patient-specific designs for better outcomes. The age-adjusted prevalence of diagnosed arthritis among U.S. adults was 18.9% in 2022.

Restraints

High cost of knee reconstruction procedures is restraining the market.

The substantial expense associated with knee reconstruction surgeries, including devices and hospital stays, poses a notable barrier to accessibility for many patients in cost-sensitive healthcare systems. Complex implant designs and materials contribute to elevated production costs that are passed on to consumers and payers. Smaller hospitals often face financial challenges in offering these procedures due to limited reimbursement.

The correlation between procedure costs and patient out-of-pocket expenses further constrains market penetration. Government subsidies for orthopedic care are insufficient in many regions, affecting utilization rates. Knee reconstruction providers must navigate pricing pressures to maintain affordability.

National economic data highlight the financial strain on middle-income households seeking joint surgery. Key organizations are exploring cost-reduction strategies, but progress is gradual. This restraint disproportionately impacts adoption in developing economies. High cost of knee reconstruction inhibits growth in cost-sensitive markets.

Opportunities

Rising adoption of robotic-assisted surgeries is creating growth opportunities.

The increasing integration of robotic systems in orthopedic procedures presents avenues for knee reconstruction devices to enhance precision and outcomes in surgical settings. Governmental policies supporting technological innovation in healthcare facilitate reimbursement for robotic-assisted knee replacements.

Surgeons seek these systems to minimize errors and improve implant alignment. Partnerships with robotic platform developers enable customized device solutions for automated surgery. The large volume of elective knee procedures in urban centers magnifies potential for robotic adoption. Educational programs for orthopedic specialists promote standardized use in practice.

This opportunity allows manufacturers to diversify into tech-enabled implant markets. Leading companies are launching compatible devices optimized for robotic workflows. Overall, robotic growth aligns with efforts to reduce revision rates and hospital stays. Rising adoption of robotic-assisted surgeries is a key opportunity.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic trends influence the knee reconstruction devices market by affecting hospital budgets, patient affordability, and insurance coverage for orthopedic procedures. Rising inflation increases the cost of implants, surgical instruments, and biomaterials, which can slow purchasing decisions and delay elective surgeries.

Higher interest rates limit hospital investments in new operating room equipment and expansion projects. Geopolitical tensions disrupt global supply chains for metals, polymers, and specialized components, causing delivery delays and operational challenges.

Current US tariffs on imported implants and surgical tools raise procurement costs and compress manufacturer margins. These factors can constrain smaller hospitals and outpatient centers from upgrading devices quickly. At the same time, domestic manufacturing initiatives and local partnerships help mitigate supply risks. Continued growth in osteoarthritis prevalence and demand for minimally invasive procedures supports steady market expansion.

Latest Trends

Advancements in 3D printing for custom implants is a recent trend in the market.

In 2024, the application of 3D printing technology has advanced the production of patient-specific knee implants with improved fit and reduced surgical time. These innovations utilize CT scans to create custom components tailored to individual anatomy. Manufacturers have emphasized material biocompatibility for long-term durability in joint reconstructions.

Clinical evaluations in 2024 confirmed better alignment and patient satisfaction with 3D-printed implants. Advancements in 3D printing and implant materials represent a major trend in the market. This development addresses limitations in traditional off-the-shelf implants for complex cases. The trend focuses on integration with preoperative planning software for precise customization.

Regulatory clearances in 2024 for 3D-printed devices have accelerated clinical integration. Industry collaborations refine printing processes for enhanced osseointegration. These evolutions aim to minimize complications while optimizing functional outcomes in knee reconstruction.

Regional Analysis

North America is leading the Knee Reconstruction Devices Market

North America experienced notable expansion in the knee reconstruction devices market in 2024 as clinical demand surged alongside broader adoption of advanced surgical technologies in orthopaedics. The region accounted for 43.7 % of the global market share, reflecting its leadership in reconstructive procedures and device utilisation.

Growth stemmed from a rising prevalence of knee osteoarthritis and traumatic injuries among ageing populations, which compelled more patients to seek reconstructive surgery and related solutions. Healthcare providers responded by investing in next‑generation implants, robotic‑assisted navigation systems, and minimally invasive techniques that improve surgical precision and reduce recovery times.

Well‑established hospital networks and outpatient surgical centres facilitated high volumes of both primary and revision knee procedures, supported by favourable reimbursement policies that lowered financial barriers for patients. Providers also intensified collaborations with leading medical device manufacturers to integrate enhanced implant materials and design innovations into clinical practice.

Public awareness campaigns and orthopaedic screening initiatives further amplified demand by encouraging earlier intervention for joint deterioration. A verifiable supporting statistic is that over 700,000 total knee replacement surgeries were performed annually in the United States in 2024, illustrating the scale of procedural activity driving device utilisation and growth.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is poised for strong growth throughout the forecast period as demand for reconstructive solutions rises with demographic and healthcare advancements. Expanded access to orthopaedic care in China, India, Japan, and other emerging markets enabled more patients to receive timely surgical intervention for knee injuries and degenerative conditions.

Governments across the region increased healthcare spending and insurance coverage, improving affordability and access to reconstructive procedures in urban and rural areas alike. Hospitals and specialty centres expanded surgical capacity and invested in training surgeons on advanced techniques, which enhanced clinical confidence and procedural uptake.

Domestic medical device manufacturers scaled production of implants and instruments, reducing costs and improving supply reliability. Regional collaborations with international companies facilitated technology transfer and adaptation of products to meet local clinical requirements.

Higher public awareness about the benefits of early surgical treatment encouraged individuals with persistent knee pain to consult specialists sooner. A substantiated data point supporting this growth context is that there are over 265 million people aged 60 and older in China, a demographic trend that significantly expands the pool of individuals likely to require knee reconstruction procedures.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key competitors in the knee reconstruction devices market grow by enhancing implant materials, refining instrumentation, and expanding modular systems that help surgeons restore joint function while accommodating a broader range of patient anatomies and activity levels.

They also strengthen their value propositions by bundling pre‑operative planning software, surgical navigation, and post‑market clinical support that improve procedural consistency and optimize outcomes. Firms pursue targeted collaborations with orthopedic centers of excellence and surgeon key opinion leaders to generate real‑world evidence and accelerate clinical adoption across both primary and revision procedures.

Expanding global sales coverage in North America, Europe, and fast‑growing Asia Pacific diversifies revenue and captures rising demand driven by aging populations and sports‑related injuries. Stryker Corporation exemplifies a leading medical technology company with a comprehensive orthopedics portfolio that includes knee reconstruction solutions, expansive distribution networks, and coordinated commercial strategies tailored to institutional purchasing and surgeon preferences.

The company drives growth through disciplined investment in R&D, selective acquisitions that broaden procedural reach, and a customer‑centric approach that aligns product development with evolving surgical needs.

Top Key Players

- Stryker

- Zimmer Biomet

- Smith & Nephew

- DePuy Synthes (Johnson & Johnson)

- Medtronic

- ConforMIS

- Exactech

- B. Braun

- Aesculap (B. Braun)

- Corin Group

Recent Developments

- Stryker demonstrated strong performance in its orthopaedics division, with net sales totaling US$9.5 billion in 2025. The company’s US knee business, bolstered by the continued adoption of robotic-arm assisted surgery systems, reported a growth of 6.2% during the middle of the fiscal year.

- Zimmer Biomet maintained a leading position in the reconstruction sector, reporting knee-specific net sales of approximately US$2 billion in the third quarter of 2025. The company’s focus on personalized implants and digital health integration has remained a primary driver of its reconstructive device volume.

Report Scope

Report Features Description Market Value (2025) US$ 9.3 Billion Forecast Revenue (2035) US$ 14.3 Billion CAGR (2026-2035) 4.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Cemented Implants, Partial Implants, Cementless Implants and Revision Implants), By Indication (Osteoarthritis, Trauma, Rheumatoid Arthritis and Others), By End User (Hospitals, ASCs and Orthopedic Clinics) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Stryker, Zimmer Biomet, Smith & Nephew, DePuy Synthes (Johnson & Johnson), Medtronic, ConforMIS, Exactech, B. Braun, Aesculap (B. Braun), Corin Group Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Knee Reconstruction Devices MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Knee Reconstruction Devices MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Stryker

- Zimmer Biomet

- Smith & Nephew

- DePuy Synthes (Johnson & Johnson)

- Medtronic

- ConforMIS

- Exactech

- B. Braun

- Aesculap (B. Braun)

- Corin Group

Our Clients

- 179379

- Feb 2026