Global K-12 Learning Management Systems (LMS) Market Size, Share Report By Component (Solutions, Services), By Deployment (Cloud-Based, On-Premise), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: July 2025

- Report ID: 153785

- Number of Pages: 233

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

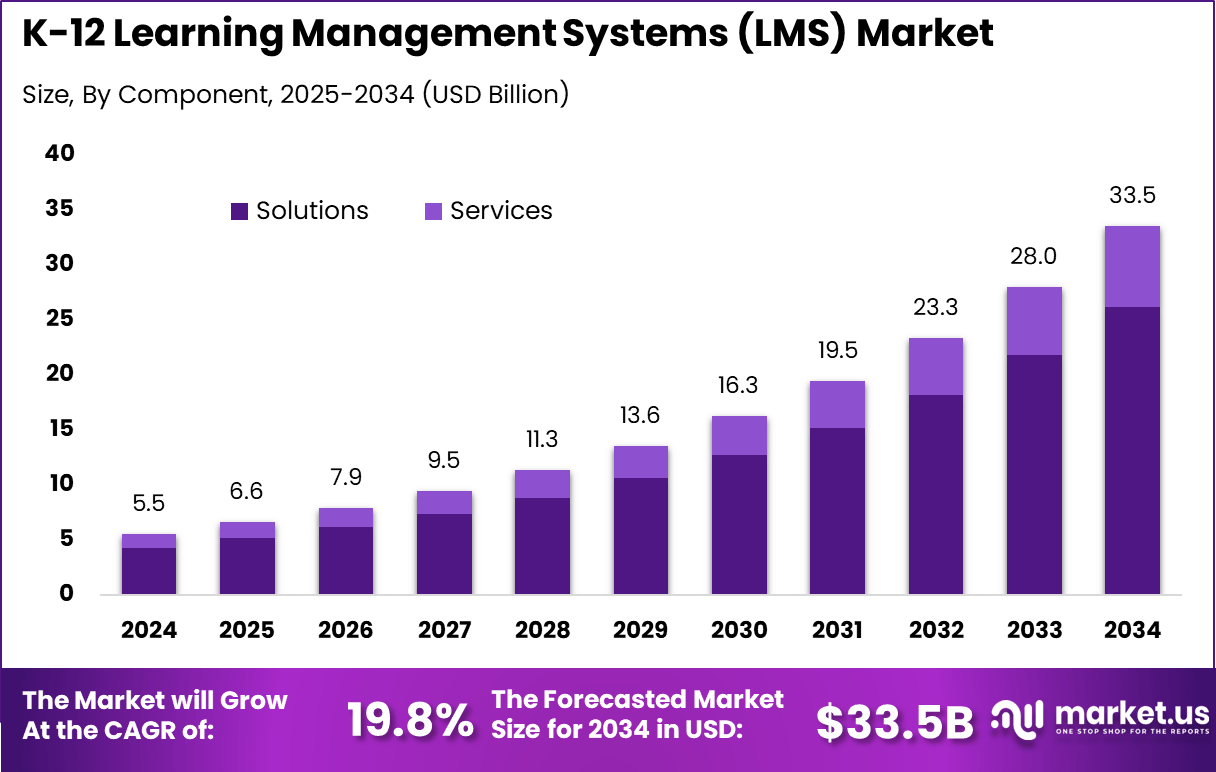

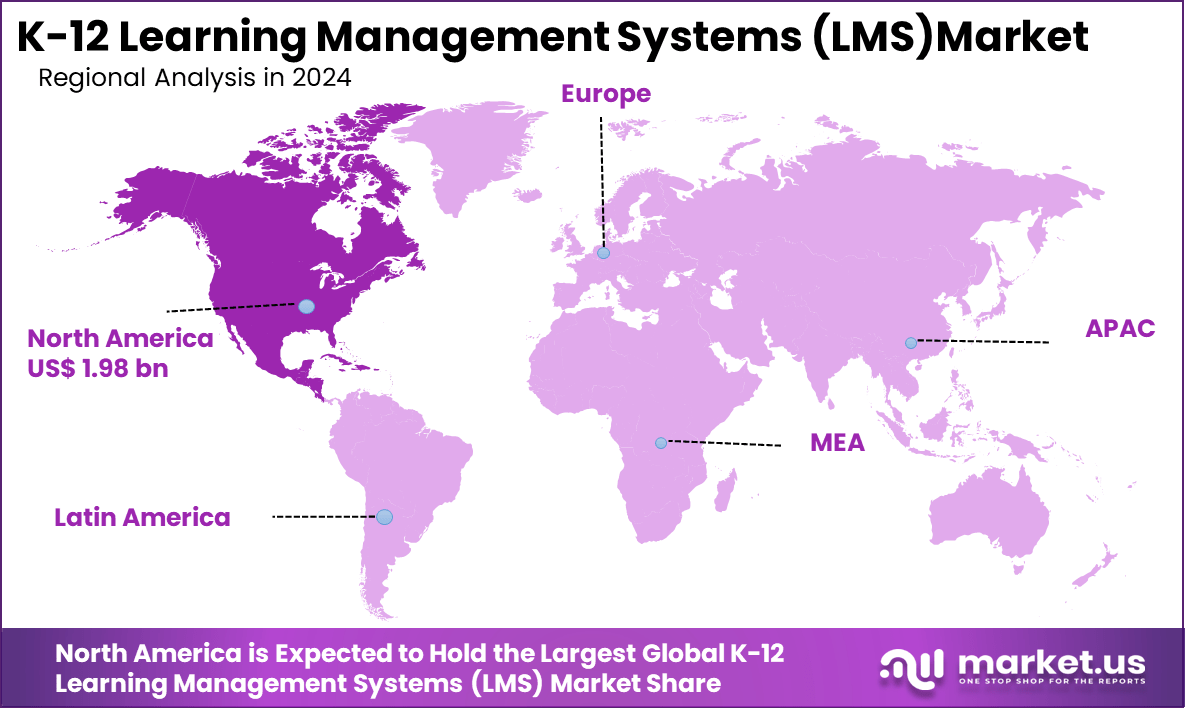

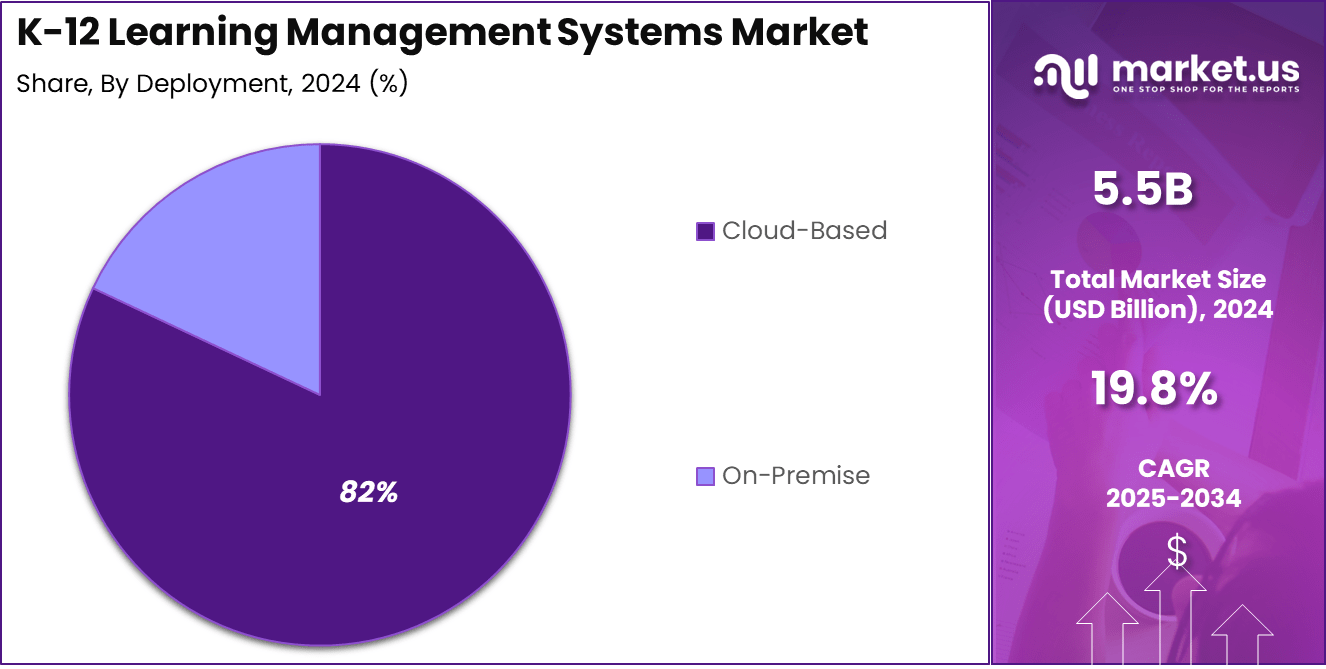

The Global K-12 Learning Management Systems (LMS) Market size is expected to be worth around USD 33.5 billion by 2034, from USD 5.5 billion in 2024, growing at a CAGR of 19.8% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 36% share, holding USD 1.98 billion in revenue.

The K-12 Learning Management Systems (LMS) market centers on digital platforms specially designed to manage, organize, and deliver educational content for students from kindergarten through twelfth grade. These platforms have reshaped the educational landscape by providing streamlined access to learning materials, tools to track student progress, and avenues for communication and collaboration between teachers, students, and parents.

One of the top driving factors behind this market’s rapid growth is the surge in digital integration within classrooms. Schools are embracing technology to create more engaging and interactive learning experiences, simplify resource management, and address the growing need for flexible and remote education. After the COVID-19 pandemic, the role of LMS became even more crucial, as institutions urgently shifted to online and hybrid learning models to maintain academic continuity.

For instance, in July 2025, Instructure announced a global partnership with OpenAI to embed advanced AI capabilities directly into its Canvas LMS platform. This collaboration aims to enhance teaching and learning through intelligent tutoring, automated feedback, and real-time content generation while maintaining strict data privacy controls. The integration is designed to support educators with personalized insights and reduce administrative workload.

Scope and Forecast

Report Features Description Market Value (2024) USD 5.5 Bn Forecast Revenue (2034) USD 33.5 Bn CAGR (2025-2034) 19.5% Leading Segment Cloud-Based : 82% Largest Market North America [36% market share] Largest Country US: 1.87 Billion, CAGR: 17.2% According to Market.us, the Global K-12 Education Technology (EdTech) Market is poised to grow significantly, reaching around USD 253.9 Billion by 2033, up from USD 78.2 Billion in 2023. This notable expansion reflects a steady compound annual growth rate of 12.5% between 2024 and 2033.

In parallel, the Global Learning Management System (LMS) Market is expected to witness exceptional momentum, rising from USD 24.5 Billion in 2024 to approximately USD 107.9 Billion by 2033. This surge represents an impressive 17.9% CAGR over the next decade, driven by the growing need for centralized learning platforms across schools, universities, and corporate training environments.

Key Takeaway

- The market is projected to reach USD 33.5 billion by 2034, expanding at a strong CAGR of 19.8%, reflecting the rapid digitization of the global education system.

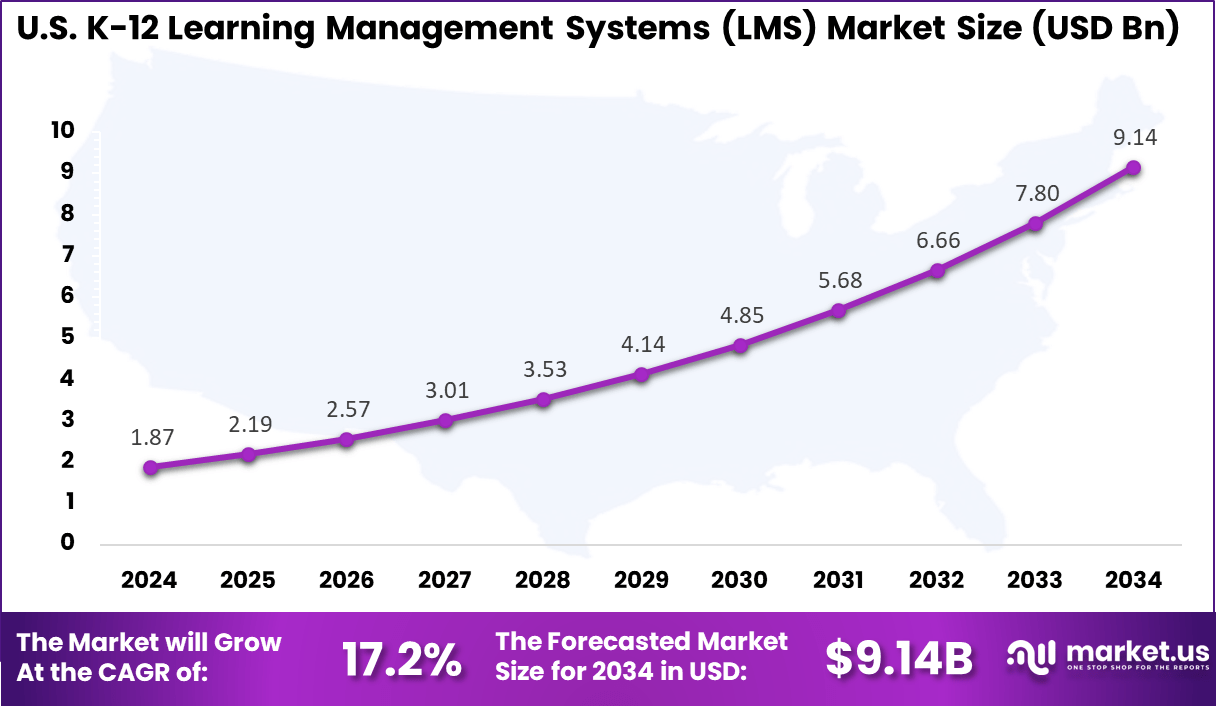

- In 2024, North America held a commanding 36% market share, contributing USD 1.98 billion in revenue, with the United States alone accounting for USD 1.87 billion and growing steadily at 17.2% CAGR.

- Cloud-based deployments made up 82% of all LMS installations in K-12 institutions, owing to their scalability, remote access, and minimal IT infrastructure requirements.

- The solutions segment led the market by component type, capturing 78% share, driven by rising demand for content management, curriculum planning, and real-time analytics.

- Demand is rising for platforms that support personalized learning, real-time feedback, and multilingual accessibility, aligning with diverse student needs across global school systems.

U.S. K-12 LMS Market Size

The market for K-12 Learning Management Systems (LMS) within the U.S. is growing tremendously and is currently valued at USD 1.87 billion, the market has a projected CAGR of 17.2%. The market is expanding rapidly, driven by growing adoption of digital learning tools, rising demand for personalized and flexible education, and the widespread use of blended and remote learning models.

Government initiatives, such as ESSER and EdTech funding, have accelerated technology integration in schools. Enhanced parental involvement and the adoption of advanced features like AI-powered learning, real-time analytics, and mobile accessibility further support this growth. These developments underscore a national focus on improving educational access, engagement, and outcomes through scalable, tech-enabled solutions.

For instance, In June 2025, Qubits Learning acquired U.S.-based Ellipsis Education to expand in the American K–12 market. This move underscores the U.S.’s key role in the global LMS space, drawing global firms seeking growth and collaboration. The deal lets Qubits add Ellipsis’s curriculum and tools to its LMS, improving personalized and standards-based learning.

In 2024, North America held a dominant market position in the Global K-12 Learning Management Systems (LMS) Market, capturing more than a 36% share, holding USD 1.98 billion in revenue. The market is in a dominant position, driven by high technology adoption and substantial investments in EdTech.

The region’s focus on digital learning tools, competency-based education, STEM/STEAM programs, and inclusive, emotionally supportive learning environments has strengthened its market presence. Emphasis on data-driven instruction, personalized learning, and scalable cloud-based LMS platforms has enhanced accessibility and cost efficiency.

For instance, In May 2025, ListedTech reported a rise in dual LMS adoption across North America, strengthening the region’s lead in the K–12 LMS market. Schools increasingly pair Google Classroom with systems like Canvas or Schoology to balance ease of use with advanced features. This approach improves flexibility, supports diverse learning needs, and enhances overall user experience.

Component Analysis

In 2024, the Solutions segment held a dominant market position, capturing a 78% share of the Global K-12 Learning Management Systems (LMS) Market. This dominance is due to the increasing demand for comprehensive, integrated platforms that support content delivery, performance tracking, communication, and collaboration.

Several educational institutions are seeking robust LMS alternatives that provide flexibility, simplicity, and compatibility with existing systems. The increased emphasis on personalized education, curriculum synchronization, and instant analytics has also led to an increase in demand for solution-based products over isolated services or tools.

For Instance, In December 2024, Britannica Education introduced NEP 2020-aligned digital learning tools for K–12 students in India. This move highlights rising demand for all-in-one solution-based platforms in the LMS market. With curriculum content, personalized learning, and teacher tools, Britannica’s launch reinforces the Solutions segment’s strong position in K–12 LMS offerings.

Deployment Analysis

In 2024, the Cloud-Based segment held a dominant market position, capturing an 82% share of the Global K-12 Learning Management Systems (LMS) Market. The growth of the cloud-based industry is mainly due to the increasing demand for affordable, flexible, and adaptable educational websites.

With the increasing popularity of remote and hybrid learning environments, these solutions offer instantaneous access through a range of devices. Educational institutions use service providers for infrastructure management, which leads to reduced IT upkeep and initial costs. The use of cloud-based LMS platforms also enhances the interaction and cooperation among teachers, learners, and families.

For instance, In July 2025, Uruguay advanced its digital education strategy by adopting PowerSchool’s Connected Intelligence K–12 solution and AI-powered PowerBuddy platform. This cloud-based system upgrades the national data infrastructure, allowing real-time insights, personalized learning, and centralized monitoring. The initiative reflects the global shift toward scalable, cloud-native LMS platforms that enable data-driven decisions and inclusive education.

Key Features and Trends

Feature/Trend Details Cloud-based Deployment Scalability, accessibility, and cost-effectiveness make cloud-based LMS dominant. Mobile & Multi-device Access Growing demand for learning on smartphones and tablets. AI & Personalization Adaptive learning paths, AI-driven recommendations, and automated assessments. Gamification & Engagement Use of interactive modules, badges, and rewards to boost student motivation. Data Analytics & Reporting Advanced dashboards for real-time student performance and progress tracking. Integration & Interoperability Seamless plug-ins with curriculum standards, school systems, and third-party tools. Mixed Reality & Immersive Learning Integration of AR/VR for enhanced interactivity and experiential learning. Focus on Microlearning Trend toward concise, modular, bite-sized content tailored for K–12 learners. Enhanced Parental Engagement Tools for progress monitoring, messaging, and at-home support. Key Market Segments

By Component

- Solutions

- Curriculum Management

- Content Authoring Tools

- Student Performance Tracking

- Assessment & Testing Solutions

- Communication & Collaboration Tools

- Services

- Implementation & Integration

- Training & Support

- Consulting

By Deployment

- Cloud-Based

- On-Premise

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Drivers

Increasing Digital Adoption in Learning

The landscape of K–12 education has been fundamentally changed by the swift adoption of digital and blended learning methods. A growing demand for flexible, scalable platforms in schools enables them to manage virtual classrooms, monitor students’ progress, and provide engaging content.

The use of Learning Management Systems (LMS) has become an essential component, enabling teachers to tailor instruction and improve learning outcomes. This structural necessity arises due to changing educational expectations and the ongoing policy emphasis on digital transformation in global educational systems.

For instance, in October 2024, Seesaw and D2L Brightspace announced a strategic partnership to deliver a unified learning experience spanning early elementary through high school. This integration aims to support educators with consistent tools, streamline workflows, and enhance student progression across grade levels. The partnership reflects a growing trend toward comprehensive, age-spanning digital learning ecosystems in K–12 education.

Restraint

Infrastructure & Digital Divide

Persistent digital infrastructure gaps hinder widespread LMS adoption, especially in rural or underserved regions. Insufficient broadband connectivity, insufficient hardware availability, and unstable connectivity hinder the efficiency of platforms and user participation.

These inequities lead to a fragmented market where technologically advanced institutions move quickly, while others face difficulties with fundamental implementation. To ensure equal access and the systemic integration of technology into K–12 education across all segments of society, it is imperative to close this digital divide.

for instance, In November 2024, India’s Ministry of Education revealed a 29% internet access gap between rural and urban schools, exposing critical digital infrastructure challenges. This divide limits the effective rollout of K–12 LMS platforms in underserved areas. Poor connectivity, lack of devices, and unreliable power supply remain key barriers to equitable digital education.

Opportunities

Integration with Advanced Technologies

The strategic integration of LMS platforms with advanced technologies such as artificial intelligence, learning analytics, and student information systems presents a significant market for growth and differentiation.

These improvements enable personalized learning, instant performance evaluation, and seamless curriculum integration. As schools prioritize data-driven teaching and enhancing their operational effectiveness, the K-12 educational sector is poised to benefit from platforms that offer modular, AI-integrated, and standards-compliant integration features.

For instance, in April 2025, Kira Learning unveiled a suite of AI agents designed to revolutionize digital instruction across K–12 education. These agents function as intelligent teaching assistants, supporting tasks such as grading, lesson planning, and personalized tutoring across subjects. Built with explainable AI, the platform aims to enhance educator efficiency and student engagement while maintaining transparency and trust.

Challenges

Competitive Landscape & Market Fragmentation

The K–12 LMS industry is fragmented and heavily reliant on established players such as Blackboard, Moodle, Instructure, PowerSchool, Edsby, and D2L. Every rival aims to outperform in terms of functionality, user-friendliness, scalability, and integration features.

The congested setting presents obstacles for recent graduates and ongoing differentiation, particularly as educational institutions strive to find solutions that accommodate changing educational and technological landscapes. Strategic alliances and consolidation within the ecosystem are necessary for long-term market dominance and expansion.

For instance, in July 2025, Anthology unveiled advanced AI and immersive learning innovations within its Blackboard platform, reinforcing its position as the fastest-evolving LMS for the fourth consecutive year. Key enhancements include the Anthology Virtual Assistant (AVA), designed to streamline workflows, improve student engagement, and reduce faculty administrative burden.

Key Players Analysis

One of the leading players in the market, in June 2024, PowerSchool announced its acquisition by Bain Capital in a landmark $5.6 billion take-private deal. The transaction aims to accelerate PowerSchool’s global expansion and innovation in areas such as AI-powered tools and personalized learning platforms. As a leading K–12 LMS provider, PowerSchool’s transition to private ownership is expected to provide greater strategic flexibility, enabling the company to deepen product development, scale digital infrastructure, and strengthen its role in shaping the future of educational technology.

Top Key Players in the Market

- PowerSchool

- Blackboard Inc. (Anthology)

- Google Classroom

- Instructure

- Moodle

- D2L Brightspace

- Edmodo

- Seesaw

- Knewton Alta/Pearson

- Others

Recent Developments

- In June 2025, Instructure released a LearnPlatform report revealing that K–12 districts are becoming more selective in adopting EdTech tools amid ongoing budget constraints. The report highlights a shift toward evidence-based decision-making, with schools prioritizing platforms that demonstrate clear instructional impact and cost-effectiveness.

- In October 2024, Anthology partnered with UK-based Obrizum to enhance AI-powered learning capabilities for Blackboard users worldwide. This collaboration aims to deliver hyper-personalized, adaptive learning experiences by leveraging Obrizum’s AI engine within the Blackboard LMS ecosystem.

- In July 2024, private equity giant KKR purchased Instructure, maker of the popular Canvas LMS, for a whopping $4.8 billion. This bold move is expected to accelerate innovation in cloud-based and personalized learning tools for schools globally.

Report Scope

Report Features Description Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Component (Solutions, Services), By Deployment (Cloud-Based, On-Premise) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape PowerSchool, Blackboard Inc. (Anthology), Google Classroom, Instructure, Moodle, D2L Brightspace, Edmodo, Seesaw, Knewton Alta/Pearson, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  K-12 Learning Management Systems MarketPublished date: July 2025add_shopping_cartBuy Now get_appDownload Sample

K-12 Learning Management Systems MarketPublished date: July 2025add_shopping_cartBuy Now get_appDownload Sample -

-

Our Clients

- 153785

- July 2025