Global K-12 Blended E-Learning Market Size, Share, Industry Analysis Report By Component (Hardware, Software, Content), By Learning Model (Flipped Classroom, Station Rotation, Flex Model), By End-User (Public Schools, Private Schools, Homeschooling), By Regional Analysis, Global Trends and Opportunity, Future Outlook by 2025-2034

- Published date: Oct. 2025

- Report ID: 160412

- Number of Pages: 389

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Top Market Takeaways

- Investment and Business Benefits

- US Market Size

- By Component: Content

- By Learning Model: Flipped Classroom

- By End-User: Public Schools

- Emerging Trends

- Growth Factors

- Key Market Segments

- Driver Analysis

- Restraint Analysis

- Opportunity Analysis

- Challenge Analysis

- Competitive Analysis

- Recent Developments

- Report Scope

Report Overview

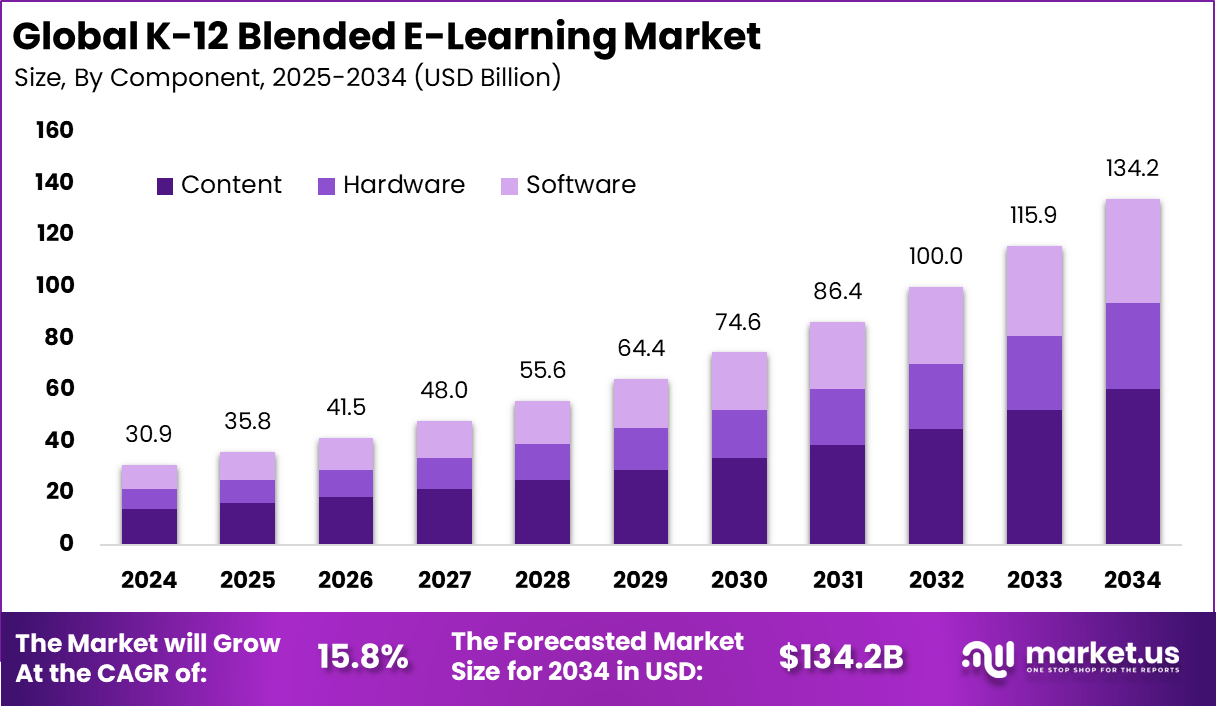

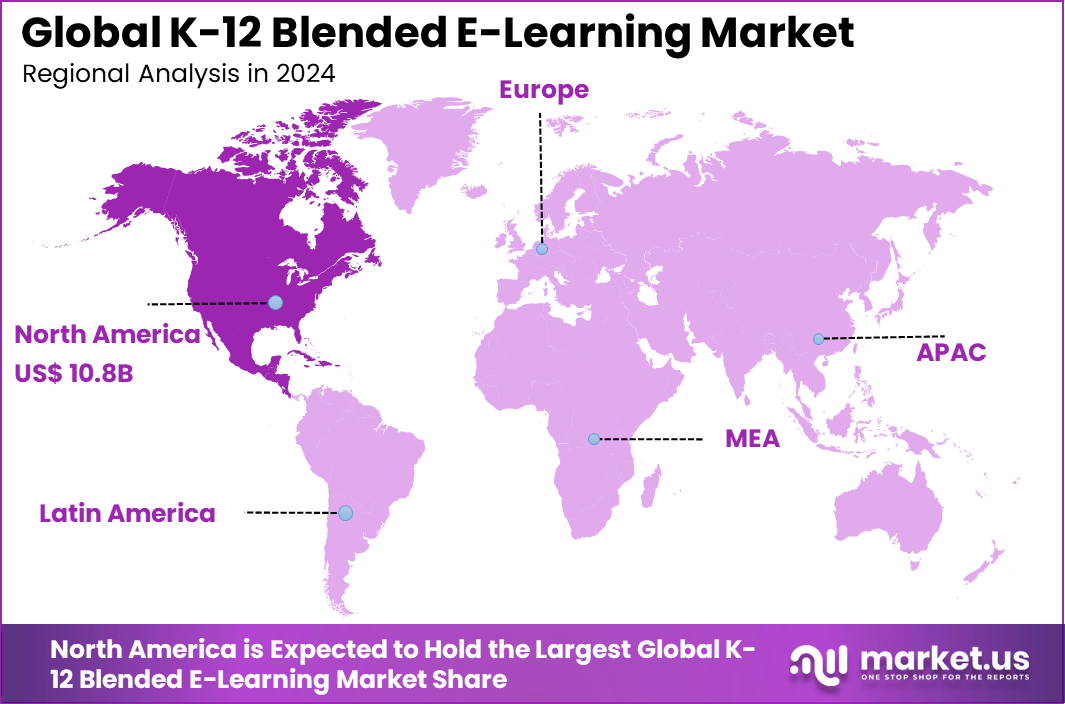

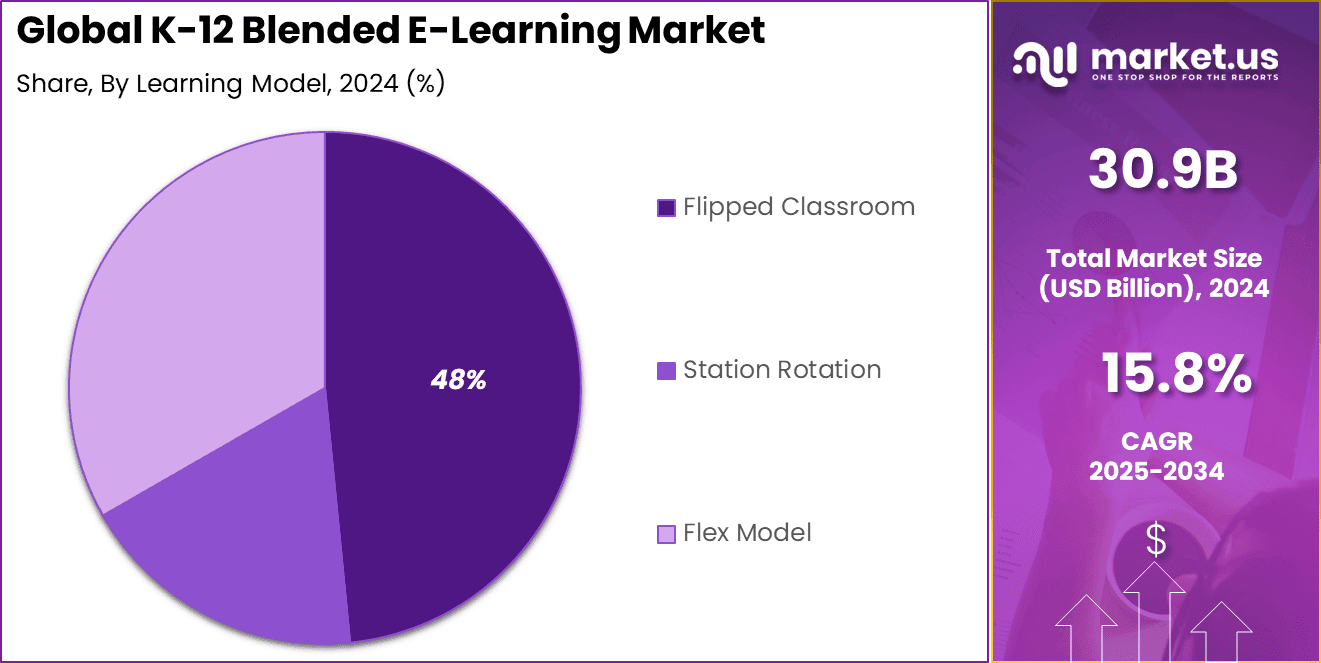

The Global K-12 Blended E-Learning Market generated USD 30.9 billion in 2024 and is predicted to register growth from USD 35.8 billion in 2025 to about USD 134.2 billion by 2034, recording a CAGR of 15.8% throughout the forecast span. In 2024, North America held a dominan market position, capturing more than a 35% share, holding USD 10.8 Billion revenue.

The K-12 Blended E-Learning Market refers to systems, platforms, content, devices, and services that combine online digital instruction with in-person teaching for primary and secondary school students. In such models, students spend some portion of their learning time in online modules (self-paced lessons, digital assessments, interactive media) and the remainder in classroom or teacher-facilitated sessions.

Key driving factors behind the growth of this market include rapid technological advancements, increased availability of digital devices, and high-speed internet. A major influence has been the COVID-19 pandemic, which accelerated the adoption of digital learning by highlighting the need for resilient and adaptable education systems. There is also growing demand for personalized and flexible learning that meets diverse student needs.

According to Market.us, The Global AI in K-12 Education Market is projected to reach USD 9,178.5 Million by 2034, rising from USD 391.2 Million in 2024 at a CAGR of 37.1% from 2025 to 2034, with North America leading in 2024 by securing over 40.5% share and USD 158.4 Million in revenue. For instance, India allocated over $13 billion recently to enhance digital classrooms and integrate coding and AI modules into the K-12 curriculum.

Meanwhile, the Global K-12 Online Tutoring Market is anticipated to attain USD 26.2 Billion by 2034, increasing from USD 7.8 Billion in 2024 at a CAGR of 12.9%, where Asia-Pacific dominated in 2024 with more than 40% share and USD 3.1 Billion revenue. Schools and governments are investing heavily in digital infrastructure and educational policies supportive of blended learning, fueling steady expansion.

Top Market Takeaways

- Content segment leads with 45%, driven by demand for digital curricula and interactive learning resources.

- Flipped classroom model holds 48%, reflecting its effectiveness in engaging students through pre-class digital learning.

- Public schools dominate with 60%, supported by government funding and district-wide digital learning initiatives.

- North America accounts for 35%, benefiting from strong EdTech infrastructure and adoption in schools.

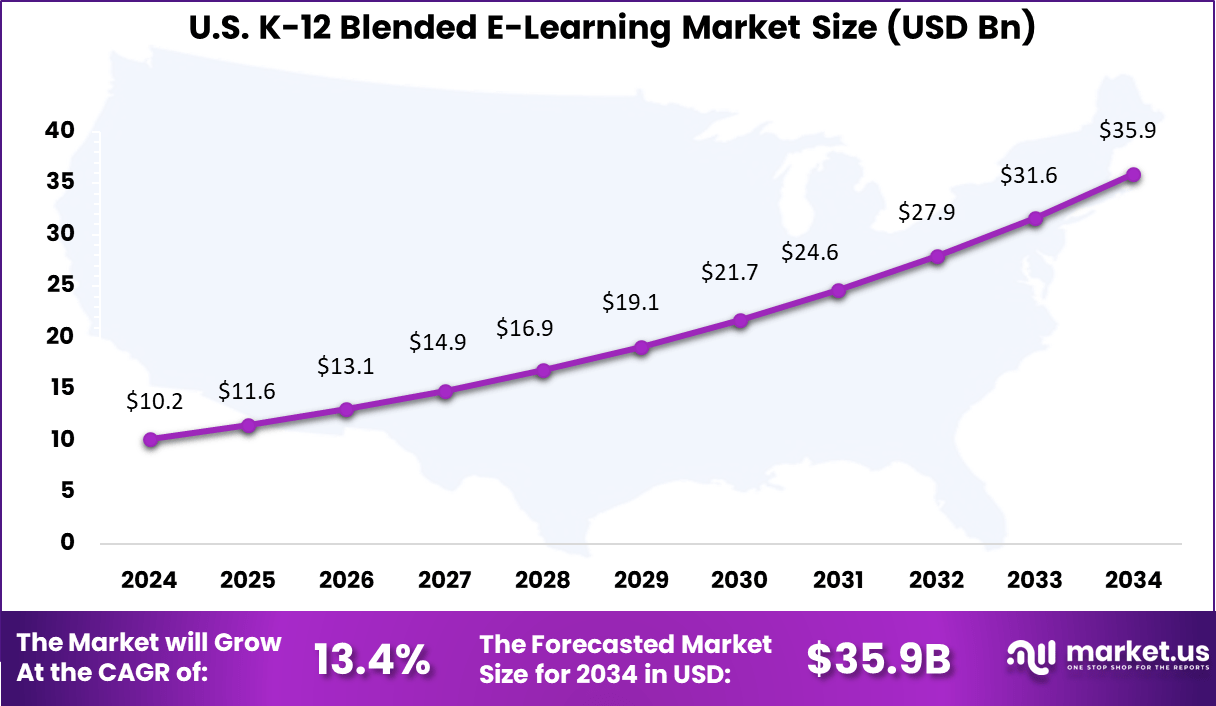

- The US market reached USD 10.2 billion and is expanding at a CAGR of 13.4%, highlighting sustained investment in blended education models.

Investment and Business Benefits

Investment opportunities in the K-12 blended e-learning sector are significant, driven by the rising interest in personalized learning solutions and the global push for digital education equity. Emerging markets with expanding digital infrastructure offer promising growth potential. Additionally, incorporating AI, ML and data analytics enables new adaptive educational tools, opening avenues for investors aiming to develop cutting-edge platforms and tools for K-12 education.

Recent studies show that AI adoption in education sectors is growing rapidly, with an adoption rate rising by over 38% annually. This suggests that generative AI is significantly reshaping how educational content is delivered to K-12 students, improving engagement and learning outcomes. Governments and private sectors are increasingly funding efforts to bridge the digital divide, presenting further investment appeal.

The business benefits from adopting blended e-learning include improved student engagement and outcomes, cost savings compared to purely in-person models, and enhanced communication among teachers, students, and parents. Blended learning fosters learner autonomy, enabling students to build discipline and problem-solving skills. Schools gain better insights through data-driven approaches to monitor student progress and tailor instructional support.

US Market Size

In 2024, the United States accounts for a substantial portion of the North American market, with a market size of around USD 10.2 billion and a strong growth rate of 13.4% CAGR. The US education system is at the forefront of adopting blended learning models, thanks to federal and state funding programs promoting digital equity and educational technology.

In 2024, North America holds a major 35% share of the K-12 blended e-learning market, driven by its advanced infrastructure, high digital literacy, and strong policy support. The region has witnessed widespread integration of blended models in both public and private educational settings. Technologies like data analytics, AI, and virtual reality are increasingly used to enhance personalized learning and improve assessment methods.

The market benefits from significant investments in innovative EdTech solutions that support flexible, hybrid learning environments. Schools focus on career readiness, STEM integration, and inclusive education, all supported by robust digital platforms that facilitate blended learning at scale.

By Component: Content

In 2024, Content is the backbone of the K-12 blended e-learning market, accounting for a significant 45% share. The richness and quality of digital content directly impact student engagement and learning outcomes. Interactive lessons, multimedia resources, and adaptive learning materials make content an essential component that helps educators tailor lessons to individual student needs.

Well-structured content facilitates seamless integration between online and face-to-face instruction, enriching the overall learning experience. The importance of content is also seen in ongoing investments in digital courseware that aligns with curriculum standards and supports differentiated learning styles.

Schools increasingly rely on cloud-based platforms to deliver content that can be continually updated and personalized. This ensures that students not only access relevant information but also benefit from a dynamic and interactive educational environment.

By Learning Model: Flipped Classroom

In 2024, the flipped classroom model dominates the learning approach segment with 48% share. This model reverses traditional teaching by assigning video lectures and study materials as homework, reserving classroom time for exercises, discussions, and hands-on activities.

The model encourages active student participation and facilitates personalized teacher support during class, creating a more engaging and effective learning environment. Studies show that students appreciate the flipped classroom because it allows them to learn at their own pace outside class and better prepare for in-class interaction.

While implementation challenges exist, particularly related to technology access and teacher readiness, the flipped classroom has gained traction for promoting deeper understanding and improving academic performance, especially in K-12 settings.

By End-User: Public Schools

In 2024, Public schools hold a commanding 60% share of the K-12 blended e-learning market end-user segment. They represent the largest adopters owing to increased government initiatives and funding geared towards digital education transformation, especially post-pandemic.

Blended learning helps public schools manage diverse student populations, providing flexible learning options that address different learning speeds and styles. Despite the progress, public schools often face challenges such as infrastructure gaps, limited teacher training, and resistance to change.

Overcoming these barriers is critical for maximizing the benefits of blended e-learning. Improvements in digital equity and professional development are key focus areas for enhancing effective adoption across public institutions.

Emerging Trends

Emerging trends in K-12 blended learning show a strong move towards AI-driven adaptive platforms, where learning content adjusts dynamically based on students’ performance. Schools are increasingly using AI-powered virtual tutors and immersive tools like VR simulations and real-time collaboration, which create interactive and dynamic learning environments.

Around 60% of educators now report enhanced student engagement when such technologies are used. Multilingual and culturally adaptive platforms continue to expand, ensuring inclusivity in diverse classrooms.

Growth Factors

Growth factors are closely tied to the increasing demand for personalized education, flexibility in learning, and wider availability of internet and mobile devices. The ability of blended models to allow students to learn anytime and anywhere enhances their appeal.

Data reveals that 74% of educators believe blended learning significantly increases student retention compared to traditional methods. Additionally, the expansion of 4G and 5G networks in urban and rural areas supports growth by connecting more learners to digital platforms.

Key Market Segments

By Component

- Hardware

- Software

- Content

By Learning Model

- Flipped Classroom

- Station Rotation

- Flex Model

By End-User

- Public Schools

- Private Schools

- Homeschooling

Regional Analysis and Coverage

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver Analysis

Flexible Personalized Learning

Blended K-12 e-learning drives growth by offering flexible, personalized learning experiences. Students benefit from a combination of face-to-face instruction with self-paced digital resources, which adapts to individual learning speeds and styles. This customization allows fast learners to deepen knowledge and slower learners to revisit materials, improving overall understanding and engagement.

Such an approach boosts academic performance by catering to diverse learning needs while making education more accessible beyond traditional classroom hours. The ability to learn anytime and anywhere enhances student motivation and participation, making blended learning a powerful educational tool in K-12 settings.

Restraint Analysis

Educator Adaptation and Training

A key restraint in K-12 blended e-learning adoption is the challenge of educator readiness and comfort with technology. Many teachers are accustomed to conventional teaching methods and may struggle to integrate digital tools effectively. The shift demands new skills in managing online platforms and combining remote with in-person teaching, which can cause resistance or slow adoption.

Additionally, lack of adequate training and professional development limits teachers’ ability to deliver high-quality blended lessons. Without sufficient support, educators may feel overwhelmed, affecting student engagement and learning outcomes.

Opportunity Analysis

Advanced Learning Technologies

The K-12 blended learning market holds significant opportunity through the integration of advanced technologies like artificial intelligence, machine learning, and data analytics. These tools can offer highly adaptive learning experiences by personalizing content based on real-time student performance and feedback.

As these technologies evolve, they promise to enhance educational effectiveness, providing detailed insights to educators and tailoring instruction to individual needs. Furthermore, expanding internet access and digital infrastructure worldwide create pathways to reach underserved regions, reducing educational disparities and opening new markets for blended learning solutions.

Challenge Analysis

Digital Divide and Accessibility

A major challenge facing K-12 blended e-learning is the digital divide, where unequal access to reliable technology and internet limits participation for some students. In low-income or rural areas, students often lack devices or consistent connectivity, preventing them from benefiting fully from blended models.

This gap exacerbates educational inequities and undermines the goal of inclusive learning. Closing this divide requires coordinated efforts by governments, schools, and technology providers to ensure affordable and widespread access to digital tools, along with robust infrastructure improvements to support blended learning environments

Competitive Analysis

The K-12 Blended E-Learning Market is supported by major technology providers such as Cisco Systems, Inc., Adobe Inc., and Blackboard, Inc. These companies deliver digital infrastructure for virtual classrooms, content management, and collaboration tools that integrate seamlessly with in-person learning environments. Their platforms are widely adopted by schools to support video instruction, secure communication, and real-time student engagement.

Content and curriculum specialists including Carnegie Learning, Inc., Cengage Learning, Inc., BYJU’S, and Allen Communication Learning Services offer AI-driven learning modules, interactive assignments, and adaptive assessments. These solutions help schools personalize education across subjects like mathematics, science, and language arts. Allen Interactions, Inc. and Atomi Systems, Inc. further strengthen the market through custom e-learning development and interactive authoring tools.

Emerging edu-tech providers such as Cegos, Acadecraft Inc, BetterLesson, Camp K12, and BlueApple Technologies focus on teacher enablement, project-based learning, and live group coaching. Their tools emphasize collaboration, creativity, and soft-skill development within blended formats. A diverse pool of other participants continues to broaden access to quality education through multilingual content, gamification, and cross-platform compatibility.

Top Key Players in the Market

- Cisco Systems, Inc.

- Adobe Inc.

- Blackboard, Inc.

- Allen Communication Learning Services

- Allen Interactions, Inc.

- Carnegie Learning, Inc.

- Cengage Learning, Inc.

- BYJU’S

- Atomi Systems, Inc.

- Cegos

- Acadecraft Inc

- BetterLesson

- Camp K12

- BlueApple Technologies

- Others

Recent Developments

- August 2025: Cengage Learning made significant strides by expanding its AI-powered learning product suite across higher education, K-12, and workforce segments. With the introduction of AI-driven tools like a student assistant supporting over 1 million students and a pilot AI content leveler for K-12, Cengage aims to deliver personalized, adaptive learning experiences and actionable analytics for educators.

- June 2025: Adobe Inc. launched enhanced Adobe Express for Education featuring generative AI tools designed to foster creativity and engagement among K-12 students. The 2025-2026 academic year saw Adobe introduce features like multi-step guided activities, animated characters, and standards-aligned templates to improve critical thinking and save teacher time. Notably, Adobe Express remains free for K-12 schools, helping promote accessible creative learning.

- ebruary 2025: Cisco Systems continues to emphasize hybrid learning in K-12 education, focusing on integrating virtual learning with on-campus teaching to address educational challenges and improve engagement. Cisco’s ongoing efforts highlight the growing demand for flexible digital classrooms and robust network infrastructure supporting blended models.

Report Scope

Report Features Description Market Value (2024) USD 30.9 Bn Forecast Revenue (2034) USD 134.2 Bn CAGR(2025-2034) 15.8% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Component (Hardware, Software, Content), By Learning Model (Flipped Classroom, Station Rotation, Flex Model), By End-User (Public Schools, Private Schools, Homeschooling) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Cisco Systems, Inc., Adobe Inc., Blackboard, Inc., Allen Communication Learning Services, Allen Interactions, Inc., Carnegie Learning, Inc., Cengage Learning, Inc., BYJU’S, Atomi Systems, Inc., Cegos, Acadecraft Inc, BetterLesson, Camp K12, BlueApple Technologies, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  K-12 Blended E-Learning MarketPublished date: Oct. 2025add_shopping_cartBuy Now get_appDownload Sample

K-12 Blended E-Learning MarketPublished date: Oct. 2025add_shopping_cartBuy Now get_appDownload Sample -

-

- Cisco Systems, Inc.

- Adobe Inc.

- Blackboard, Inc.

- Allen Communication Learning Services

- Allen Interactions, Inc.

- Carnegie Learning, Inc.

- Cengage Learning, Inc.

- BYJU'S

- Atomi Systems, Inc.

- Cegos

- Acadecraft Inc

- BetterLesson

- Camp K12

- BlueApple Technologies

- Others

Our Clients

- 160412

- Oct. 2025