IoT Certificate Management Market By Component (Software, Services), By Deployment Mode (On-Premises, Cloud), By Organization Size (Small and Medium Enterprises, Large Enterprises), By Application (Device Authentication, Secure Communications, Data Encryption, Others), By End-User (BFSI, Healthcare, Manufacturing, Energy & Utilities, Retail, IT & Telecom, Government, Others), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2026-2035

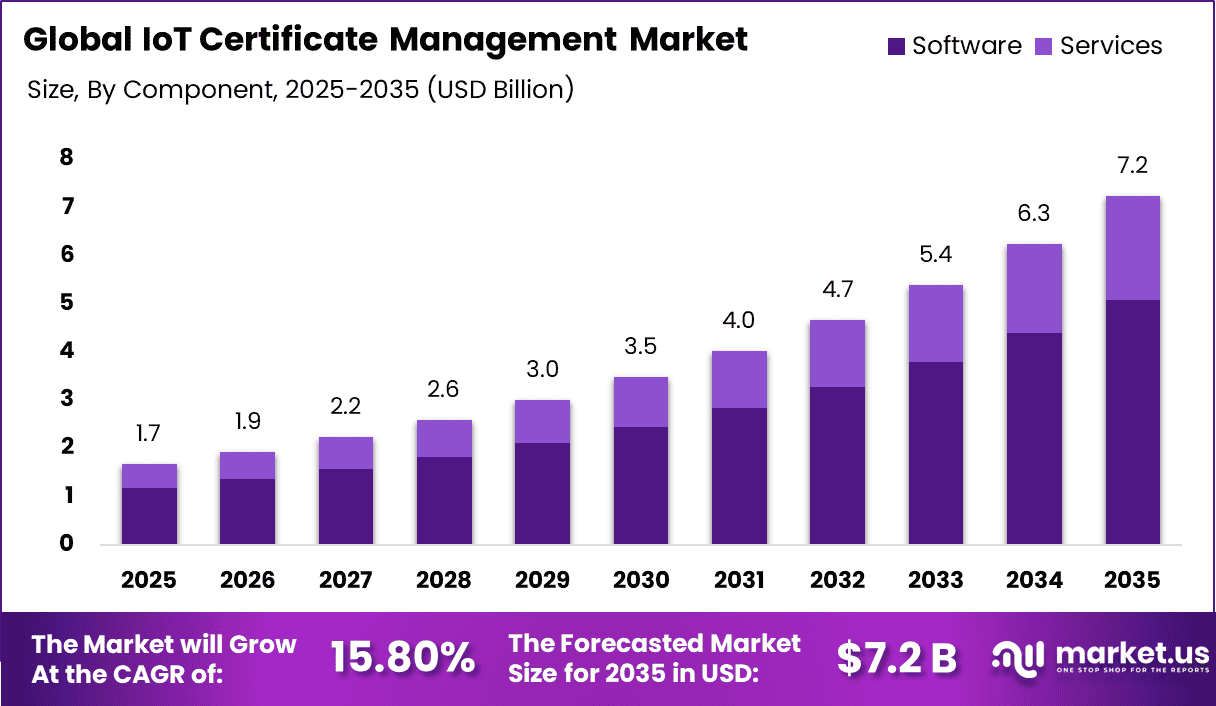

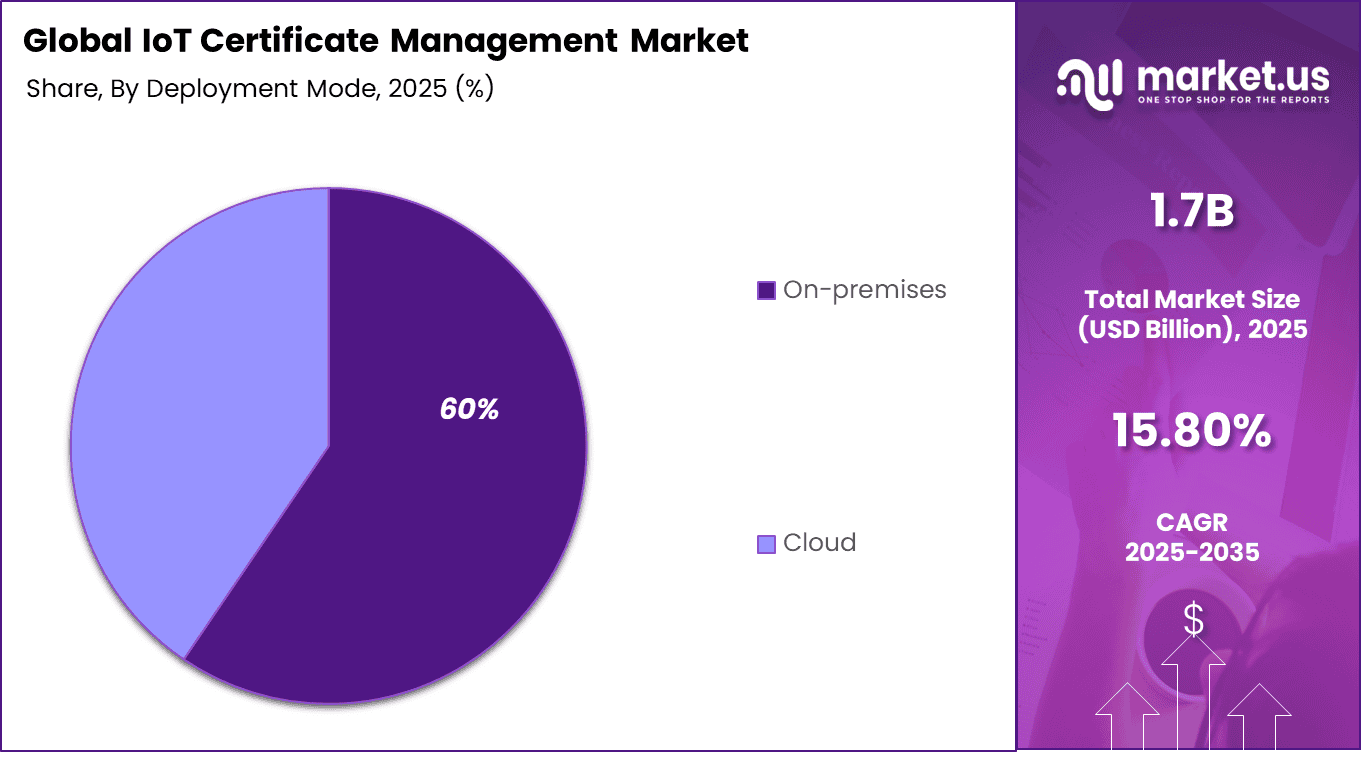

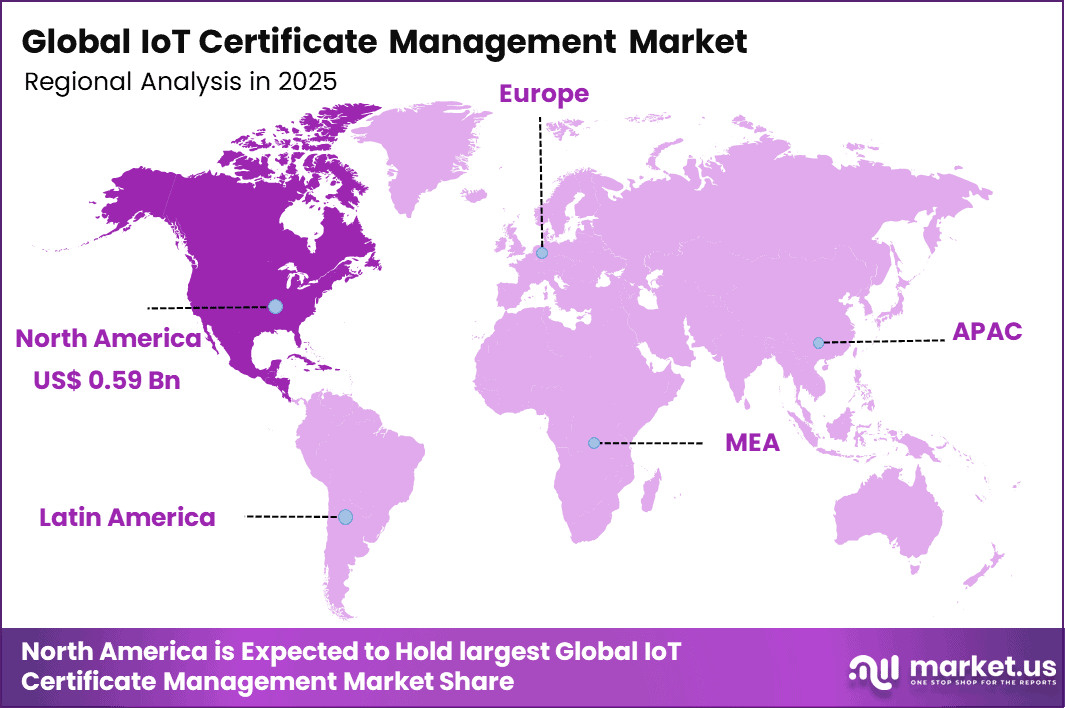

The Global IoT Certificate Management Market generated USD 1.7 billion in 2025 and is predicted to register growth from USD 1.9 billion in 2026 to about USD 7.2 billion by 2035, recording a CAGR of 15.30% throughout the forecast span. In 2025, North America held a dominant market position, capturing more than a 35.5% share, holding USD 0.59 Billion revenue.

Top Market Takeaways

Software commands 70.3% market share, delivering automated PKI orchestration, certificate lifecycle automation, and zero-touch provisioning for millions of IoT endpoints.

On-premises deployment captures 59.5%, ensuring data sovereignty, air-gapped security, and custom integration with enterprise-grade identity management systems.

Large enterprises hold 75.7%, leveraging scalable platforms for fleet-wide certificate monitoring, revocation, and compliance audit trails across hybrid environments.

Device authentication applications claim 40.6%, enabling mutual TLS, secure boot verification, and encrypted device-to-cloud communications at scale.

BFSI sector represents 35.4%, powering ATM security, branch IoT sensors, and digital banking endpoints with PCI-DSS compliant certificate governance.

North America drives 35.5% global value, with U.S. market at USD 0.50 billion and 13% CAGR, fueled by NIST cybersecurity frameworks and financial sector IoT mandates.

IoT Certificate Management market refers to software and security platforms that issue, provision, store, renew, rotate, and revoke digital certificates for connected devices throughout their operating life. These solutions help organizations establish trusted device identity, secure device to cloud communication, and manage certificate related tasks at scale across manufacturing, deployment, and field operations. The market is gaining importance as IoT deployments become larger and more complex, and as secure device identity becomes essential for reliable connected operations.

One of the main factors driving this market is the growing need to automate certificate lifecycle management. Manual handling of certificates becomes difficult and risky when organizations manage large device fleets, especially because certificates need renewal, rotation, and revocation over time.

Another important driver is the rising focus on stronger device authentication and encrypted communication, which is encouraging organizations to adopt certificate based security for long term IoT protection.

Demand for IoT certificate management solutions is increasing among industrial operators, connected device manufacturers, automotive systems, utilities, healthcare technology users, and smart infrastructure providers that need secure control over large device networks.

These buyers want practical tools that can support onboarding, certificate updates, policy enforcement, and secure device communication without heavy manual effort. Demand is also rising because many organizations now treat device identity management as a continuous operational requirement rather than a one time setup process.

Drivers Impact Analysis

Driver Factor

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Strategic Effect

Rapid growth of IoT device ecosystem

+2.0%

Global

Short to Mid Term

Increases demand for secure device authentication

Rising cybersecurity threats and data breaches

+1.8%

North America, Europe

Short Term

Drives adoption of certificate-based security

Expansion of connected infrastructure and smart devices

+1.5%

APAC, North America

Mid Term

Enhances need for scalable certificate lifecycle mgmt

Regulatory compliance and data protection requirements

+1.4%

Europe, North America

Mid to Long Term

Encourages adoption of standardized security solutions

Integration with cloud and edge computing environments

+1.3%

Global

Mid Term

Supports automated and distributed certificate mgmt

Restraints Impact Analysis

Restraint Factor

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Strategic Limitation

Complexity in managing large-scale certificate lifecycles

-1.3%

Global

Mid Term

Increases operational burden

High cost of implementation and maintenance

-1.1%

Global

Short Term

Limits adoption among smaller enterprises

Lack of standardized protocols across IoT ecosystems

-1.0%

Global

Mid to Long Term

Creates interoperability challenges

Limited awareness in emerging markets

-0.9%

APAC, Latin America

Mid Term

Slows adoption rate

Risk of certificate mismanagement or expiration failures

-0.8%

Global

Short to Mid Term

Leads to potential system vulnerabilities

By Component Analysis

Software accounted for 70.3% of the IoT Certificate Management Market. This segment leads because organizations rely on software platforms to issue, manage, and renew digital certificates for connected devices. These solutions ensure secure communication and help prevent unauthorized access across IoT ecosystems.

The segment is also supported by the growing number of connected devices. As IoT deployments expand, companies need scalable software tools to manage certificate lifecycles efficiently and maintain strong security across networks.

By Deployment Mode Analysis

On premises deployment held 60% of the market. This segment leads because organizations prefer to manage certificate systems within their own infrastructure to maintain control over sensitive security credentials. It allows direct oversight of certificate issuance and storage processes.

The segment is also driven by the need for data security and compliance. On premises systems help reduce exposure risks and ensure consistent control over device authentication frameworks, which supports adoption in security focused environments.

By Organization Size Analysis

Large enterprises accounted for 75.7% of the market. This segment dominates because large organizations deploy extensive IoT networks and require advanced certificate management solutions to secure a high volume of connected devices. They face greater security risks and need structured management systems.

The segment is supported by higher investment capacity and strong focus on cybersecurity. Large enterprises adopt certificate management platforms to ensure secure device communication and maintain operational reliability.

By Application Analysis

Device authentication represented 40.6% of the market. This segment leads because verifying the identity of connected devices is critical for preventing unauthorized access and ensuring secure data exchange. Certificate based authentication provides a reliable method for validating devices within IoT networks.

The segment is driven by increasing security concerns in connected environments. Organizations rely on authentication solutions to protect systems, maintain trust, and ensure safe operation of IoT infrastructure.

By End User Analysis

BFSI accounted for 35.4% of the market. This segment leads because financial institutions use IoT devices in secure environments such as ATMs, payment systems, and branch operations. Certificate management helps protect these systems and ensures secure communication.

The segment is also supported by strict regulatory requirements and the need for strong data protection. BFSI organizations invest in certificate management solutions to maintain security, reduce risks, and ensure compliance across their digital operations.

Investor Type Impact Analysis

Investor Type

Growth Sensitivity

Risk Exposure

Geographic Focus

Investment Outlook

Venture Capital Firms

High

High

North America, APAC

Focus on cybersecurity and IoT security startups

Private Equity Firms

Medium

Medium

Global

Invest in scalable security platforms

Corporate Investors

High

Low

Global

Strategic investments aligned with IoT ecosystem

Institutional Investors

Medium

Low

North America, Europe

Preference for stable cybersecurity infrastructure

Impact Investors

Medium

Medium

Europe, APAC

Interest in secure and resilient digital ecosystems

Technology Enablement Analysis

Technology Enabler

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Implementation Significance

Automated certificate lifecycle management tools

+1.9%

Global

Mid Term

Reduces manual errors and improves scalability

Cloud-based certificate management platforms

+1.6%

Global

Short to Mid Term

Enables centralized and flexible deployment

AI-driven threat detection and certificate monitoring

+1.5%

Global

Mid Term

Enhances proactive security management

Integration with IoT device management platforms

+1.3%

Global

Mid to Long Term

Streamlines security operations

Blockchain for secure identity and certificate validation

+1.2%

North America, Europe

Mid to Long Term

Strengthens trust and tamper-proof authentication

Key Challenges

Managing certificates across a large number of connected devices is a major challenge because IoT environments often include thousands or even millions of endpoints.

Certificate renewal and lifecycle management can be difficult because expired or mismanaged certificates may interrupt device communication and reduce system reliability.

Integration with different device types, platforms, and security systems is a challenge because many IoT deployments use mixed hardware and software environments.

Limited processing power and storage in some IoT devices can make certificate handling harder, especially in low cost or resource constrained equipment.

Security remains a serious concern because weak certificate management can increase the risk of device spoofing, unauthorized access, and data breaches.

Emerging Trends

A key trend in the IoT Certificate Management market is the increasing use of automated identity and credential management systems for connected devices. Organizations are adopting platforms that can issue, renew, and revoke digital certificates without manual intervention, ensuring secure communication across large device networks.

These systems are designed to handle device authentication at scale while maintaining consistent security policies. This trend reflects a shift toward lifecycle based certificate management where security is maintained continuously as devices are deployed, updated, and retired.

Growth Factors

The rapid expansion of connected devices is supporting the growth of IoT certificate management solutions. As more devices communicate across networks, ensuring secure identity verification becomes essential to prevent unauthorized access and data breaches.

Certificate management systems help organizations maintain trust between devices and networks by managing encryption and authentication processes efficiently. At the same time, increasing focus on device level security encourages adoption of solutions that provide structured and reliable management of digital credentials across large scale IoT environments.

Key Market Segments

By Component

Software

Services

By Deployment Mode

On-Premises

Cloud

By Organization Size

Small and Medium Enterprises

Large Enterprises

By Application

Device Authentication

Secure Communications

Data Encryption

Others

By End-User

BFSI

Healthcare

Manufacturing

Energy & Utilities

Retail

IT & Telecom

Government

Others

Regional Analysis

North America accounted for 35.5% of the IoT Certificate Management Market, reflecting strong adoption of security solutions for connected devices across industries. Organizations across the region increasingly deploy certificate management platforms to authenticate devices, encrypt communications, and ensure secure data exchange across IoT networks.

The rapid growth of connected devices in sectors such as manufacturing, healthcare, and smart infrastructure continues to drive the need for robust identity and certificate management systems across North America.

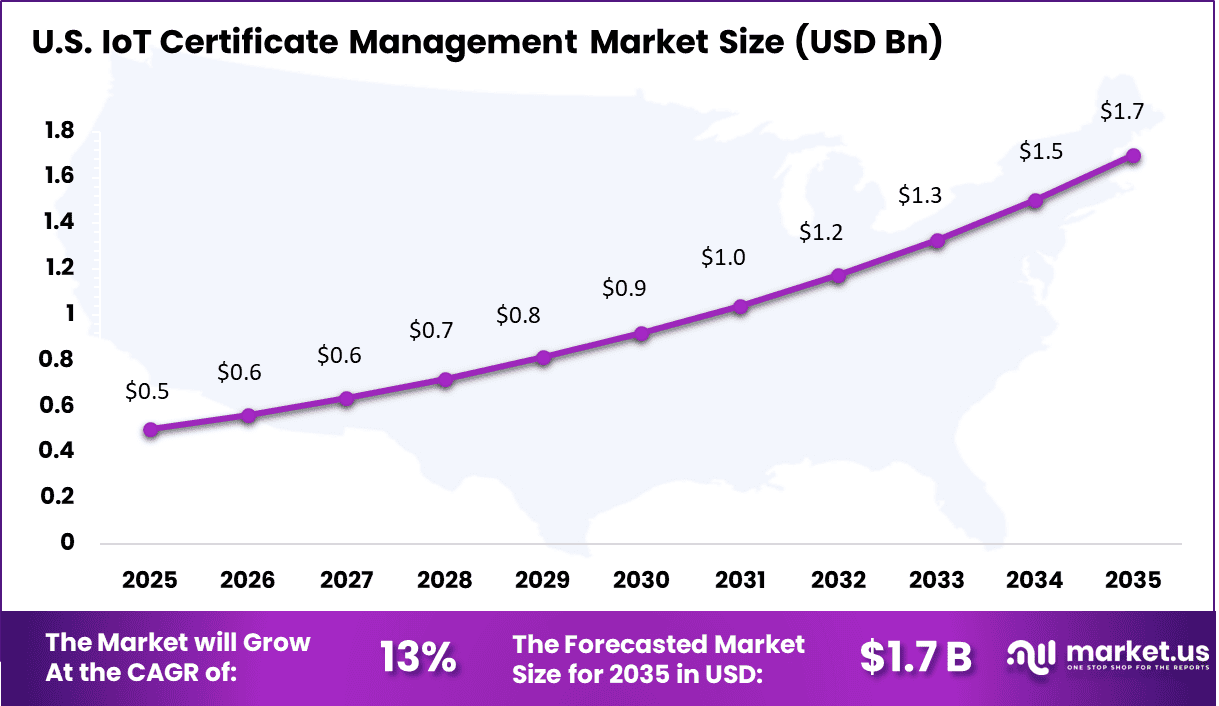

The U.S. generated about USD 0.50 Billion within the regional market and is projected to expand at a CAGR of 13%. Enterprises across the country continue to strengthen IoT security frameworks as device volumes increase and network environments become more complex.

Certificate management solutions help automate device authentication, manage digital identities, and reduce risks associated with unauthorized access. As businesses expand IoT deployments and prioritize data protection, demand for certificate management solutions continues to grow steadily across the US market.

Key Regions and Countries

North America

US

Canada

Europe

Germany

France

The UK

Spain

Italy

Russia

Netherlands

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Singapore

Thailand

Vietnam

Rest of APAC

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

South Africa

Saudi Arabia

UAE

Rest of MEA

Competitive Analysis

The competitive landscape of the IoT Certificate Management market includes major cybersecurity, cloud, and digital identity companies that provide certificate issuance, device authentication, and secure key management solutions.

IBM Corporation, Microsoft Corporation, DigiCert Inc., Entrust Datacard Corporation, Sectigo Limited, Verisign Inc., GlobalSign, Thales Group, Cisco Systems Inc., HID Global Corporation, Infineon Technologies AG, and Trend Micro Incorporated hold strong positions because they offer trusted security platforms that help protect connected devices and manage digital identities across large IoT networks.

Other players such as WISeKey SA, T-Systems International GmbH, Device Authority Ltd., Venafi Inc., Symantec Corporation, Globalscape Inc., Keyfactor Inc., and Comodo CA Limited add competition through certificate lifecycle management, encryption support, and device trust solutions.

The market is shaped by security reliability, automation capability, ease of integration, and the growing need to manage large volumes of certificates across connected industrial, enterprise, and consumer IoT environments.

The future outlook for the IoT Certificate Management Market looks strong as more connected devices need secure identity, authentication, and certificate lifecycle control at scale. Current guidance from Microsoft shows that managing PKI certificates in IoT environments becomes challenging and costly as device volumes and security needs grow, while AWS also highlights the importance of certificate rotation and fleet provisioning for device security. As businesses deploy larger IoT networks across factories, utilities, vehicles, and smart infrastructure, demand for automated certificate management solutions is expected to grow steadily in the coming years.

Recent Developments

March, 2026 – IBM Hyper Protect adds quantum-safe certs for IoT fleets with automated rotation and serves banks with mainframe-to-edge trust. Cuts breach risks 60% and partners AWS for hybrid PKI. Adds z15 mainframe support for legacy IoT bridges.

February, 2026 – Azure IoT DPS boosts device twin cert lifecycle with AI monitoring and handles 10M devices daily. Leads with Entra ID integration and zero-touch provisioning for factories. Scales to Azure Arc for on-prem edges.

Report Scope

Report Features

Description

Market Value (2025)

USD 1.7 Billion

Forecast Revenue (2035)

USD 7.2 Billion

CAGR(2025-2035)

15.80%

Base Year for Estimation

2024

Historic Period

2020-2024

Forecast Period

2026-2035

Report Coverage

Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends

Segments Covered

By Component (Software, Services), By Deployment Mode (On-Premises, Cloud), By Organization Size (Small and Medium Enterprises, Large Enterprises), By Application (Device Authentication, Secure Communications, Data Encryption, Others), By End-User (BFSI, Healthcare, Manufacturing, Energy & Utilities, Retail, IT & Telecom, Government, Others)

Regional Analysis

North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA

Competitive Landscape

IBM Corporation, Microsoft Corporation, DigiCert Inc., Entrust Datacard Corporation, Sectigo Limited, Verisign Inc., GlobalSign (GMO GlobalSign Ltd.), Comodo CA Limited, Thales Group (Gemalto NV), Cisco Systems Inc., HID Global Corporation, WISeKey SA, T-Systems International GmbH, Infineon Technologies AG, Trend Micro Incorporated, Device Authority Ltd., Venafi Inc., Symantec Corporation (Broadcom Inc.), Globalscape Inc., Keyfactor Inc., Others

Customization Scope

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Purchase Options

We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)