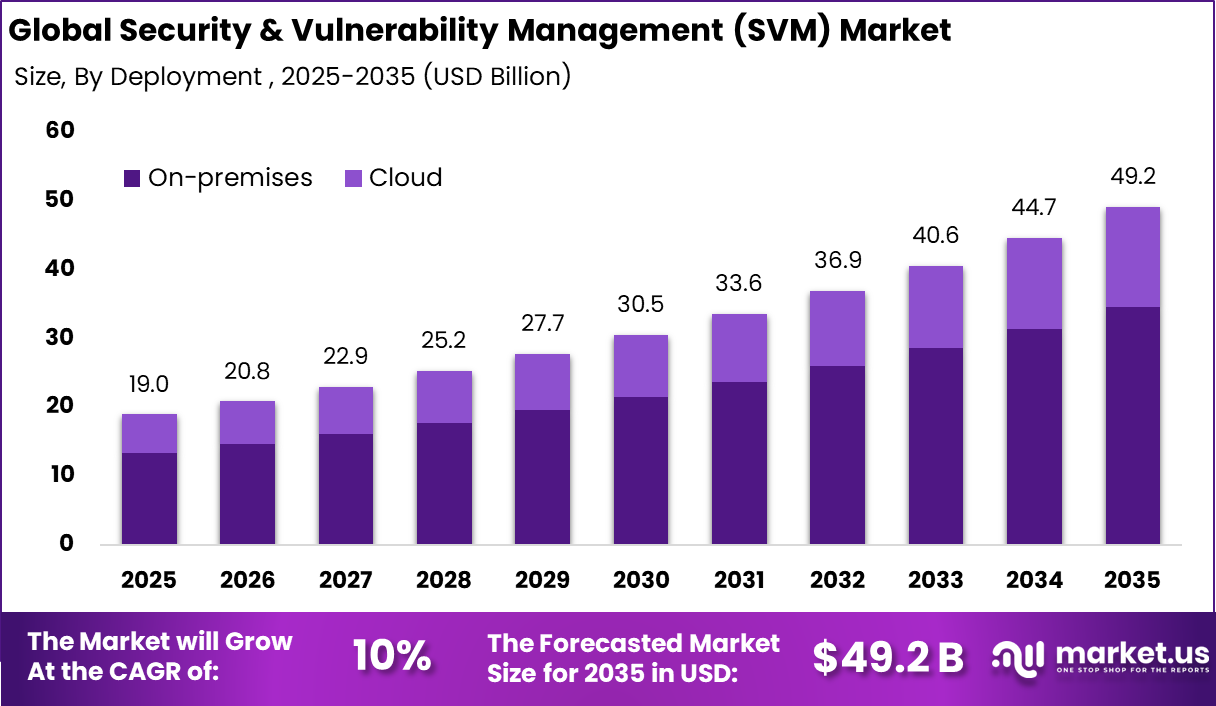

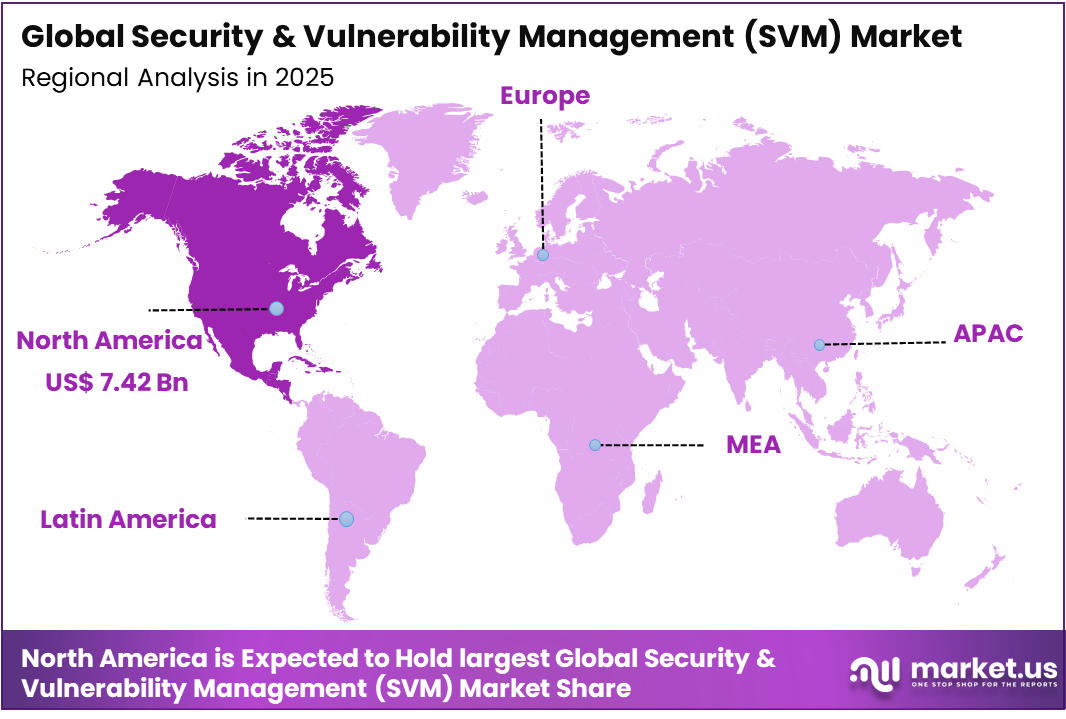

The Global Security & Vulnerability Management (SVM) Market generated USD 19 billion in 2025 and is predicted to register growth from USD 20.8 billion in 2026 to about USD 49.2 billion by 2035, recording a CAGR of 10% throughout the forecast span. In 2025, North America held a dominan market position, capturing more than a 39.2% share, holding USD 7.42 Billion revenue.

The Security and Vulnerability Management (SVM) Market represents a critical component of the global cybersecurity ecosystem. SVM solutions are designed to identify, assess, prioritize, and remediate vulnerabilities within IT infrastructure, applications, networks, and cloud environments. These solutions help organizations maintain strong cybersecurity posture by continuously monitoring potential security weaknesses and enabling proactive risk mitigation strategies.

The increasing digitalization of enterprises has significantly expanded the attack surface of modern organizations. Businesses are adopting cloud computing, remote work technologies, Internet of Things (IoT) devices, and interconnected systems that generate complex security environments. As a result, security and vulnerability management platforms have become essential tools for detecting and addressing security gaps before they can be exploited by cyber threats.

One of the primary drivers for the SVM market is the rapid increase in cyber threats and security vulnerabilities across digital systems. Organizations operate complex infrastructures that include cloud services, mobile devices, and interconnected applications, which significantly expand the potential attack surface. Continuous vulnerability monitoring enables security teams to detect weaknesses quickly and reduce the risk of exploitation by attackers.

Top Market Takeaways

By Component, software dominates with 74.8% share, delivering automated scanning, patch orchestration, and risk prioritization across sprawling attack surfaces.

By Type, endpoint security claims 35.6%, securing laptops, servers, and IoT devices against zero-days and privilege escalation exploits.

By Target, content management vulnerabilities lead at 43.4%, addressing CMS exploits, file upload weaknesses, and document workflow exposures.

By Deployment, on-premises captures 70.4%, ensuring sovereign scanning, air-gapped assessments, and integration with legacy enterprise stacks.

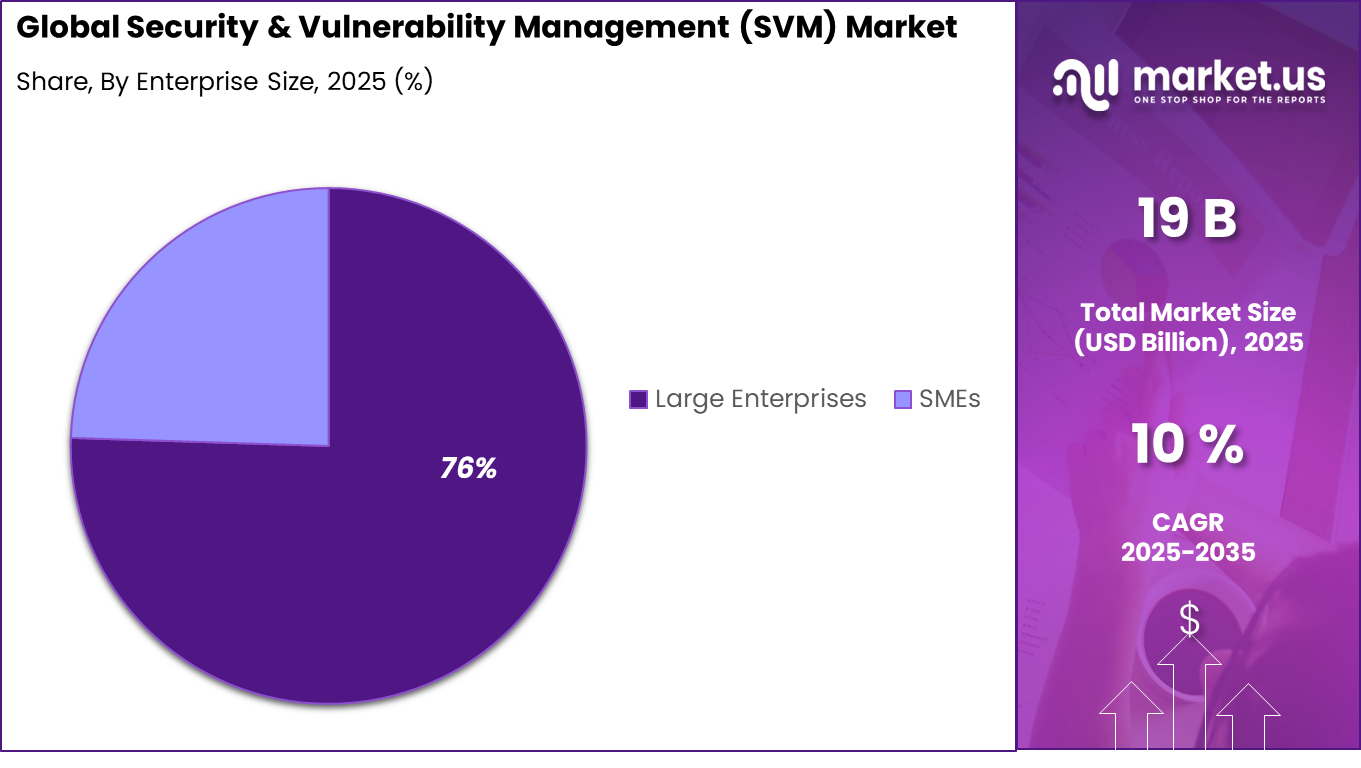

By Enterprise Size, large enterprises hold 75.5%, managing continuous vulnerability intelligence across global hybrid infrastructures.

By Vertical, BFSI commands 39.9%, prioritizing financial app hardening, transaction layer protection, and regulatory audit trails.

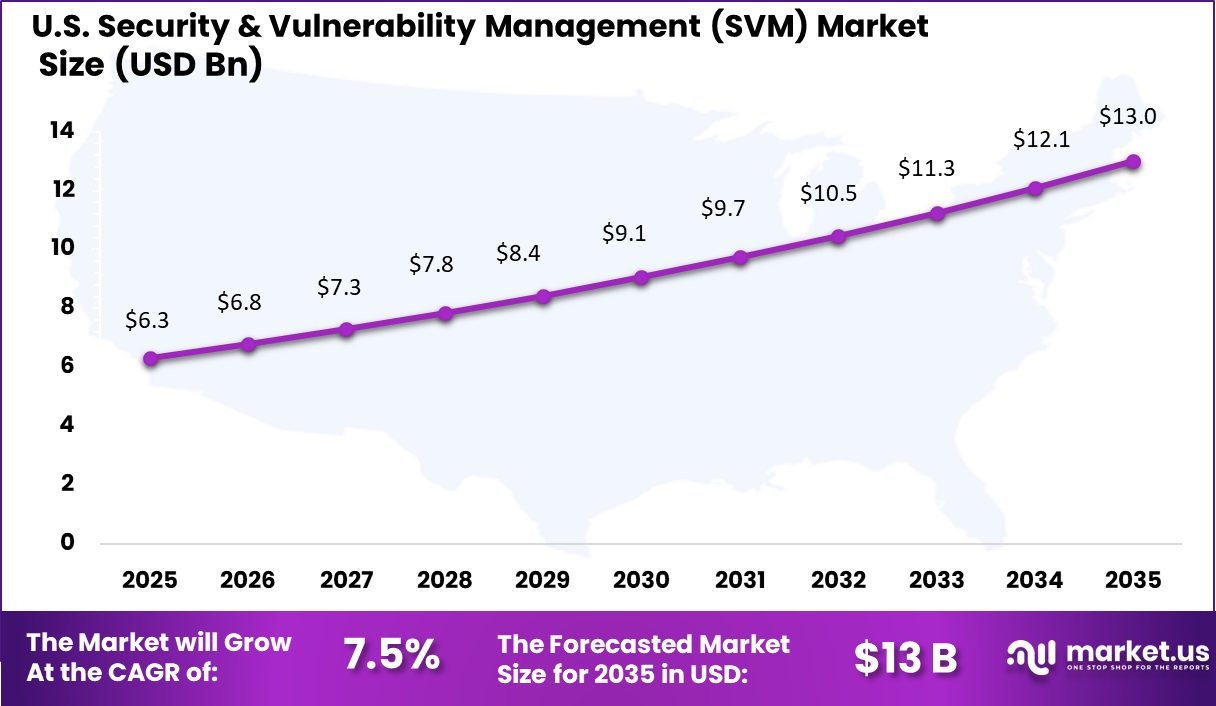

Regionally, North America accounts for 39.2% global share, with the U.S. market valued at USD 6.31 billion and a CAGR of 7.5%, driven by SEC cybersecurity rules and ransomware pressures.

Drivers Impact Analysis

Key Drivers

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Strategic Importance

Rising Frequency of Cyber Attacks and Data Breaches

+2.8%

Global

Short to Long Term

Drives continuous vulnerability monitoring

Increasing Adoption of Cloud and Hybrid Infrastructure

+2.3%

North America, Europe

Medium Term

Expands attack surface requiring management tools

Regulatory Compliance Requirements for Cybersecurity

+2.0%

North America, Europe

Medium Term

Encourages enterprise security assessments

Growth in IoT and Connected Devices

+1.6%

APAC, North America

Long Term

Increases vulnerability exposure points

Integration with Enterprise Risk Management Platforms

+1.3%

Global

Medium Term

Enhances organizational risk visibility

Restraints Impact Analysis

Key Restraints

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Market Constraint Level

Shortage of Skilled Cybersecurity Professionals

-1.9%

Global

Medium Term

Slows deployment and management

Complexity of Multi-cloud Security Environments

-1.6%

North America, Europe

Medium Term

Increases configuration challenges

High Implementation and Integration Costs

-1.3%

Emerging Markets

Short to Medium Term

Budget constraints for smaller organizations

False Positives in Vulnerability Detection Tools

-1.0%

Global

Medium Term

Reduces operational efficiency

By Component

Software represents 74.8% of the market, reflecting the growing reliance on automated security tools that continuously scan and assess enterprise systems. These platforms help organizations identify vulnerabilities across networks, applications, and operating environments before they can be exploited. Security software provides centralized dashboards that enable cybersecurity teams to monitor risk exposure and prioritize remediation actions.

The dominance of software solutions is also supported by their ability to integrate with security information and event management platforms and threat intelligence systems. Automated scanning and patch management capabilities allow organizations to maintain stronger system defenses. As cyber threats become more sophisticated, software based vulnerability management platforms continue to play a central role in enterprise security strategies.

By Type

Endpoint security accounts for 35.6% of the market, highlighting the importance of protecting devices that connect to enterprise networks. Laptops, mobile devices, servers, and industrial systems represent potential entry points for cyber attackers. Vulnerability management platforms are widely used to monitor these endpoints and ensure that security updates and patches are applied consistently.

The expansion of remote work and mobile device usage has increased the number of endpoints that organizations must secure. Continuous monitoring tools help identify weaknesses in operating systems and installed applications. As organizations expand distributed digital environments, endpoint vulnerability management remains a critical priority.

By Target

Content management vulnerabilities represent 43.4% of the market focus due to the widespread use of digital content platforms across enterprises. Websites, internal portals, and document management systems often store sensitive information and therefore require strong protection. Security solutions are deployed to detect configuration weaknesses, outdated software components, and unauthorized access risks.

Content management platforms are frequently targeted by cyber attackers seeking to exploit web application vulnerabilities. Automated scanning tools help identify potential threats before they affect operations or compromise data integrity. As organizations continue to expand digital content platforms, protecting these systems remains an essential security objective.

By Deployment

On premises deployment accounts for 70.4% of the market, reflecting the need for direct control over cybersecurity infrastructure. Many organizations manage sensitive corporate data and therefore prefer internal security monitoring systems that operate within controlled environments. On premises deployment enables customized security configurations aligned with internal governance policies.

Industries with strict regulatory requirements often maintain security platforms within internal data centers to strengthen data protection. This approach also allows organizations to integrate vulnerability management tools with legacy systems and proprietary applications. As security concerns remain a top priority, on premises deployment continues to dominate enterprise cybersecurity environments.

By Enterprise Size

Large enterprises represent 75.5% of the market share due to the complexity and scale of their IT infrastructures. These organizations manage multiple data centers, applications, and user networks that require continuous vulnerability monitoring. Dedicated cybersecurity teams implement structured security frameworks to protect enterprise systems from potential threats.

Large organizations also face significant regulatory and compliance obligations related to data protection and risk management. Vulnerability management platforms help ensure that security policies are consistently applied across business units. As enterprise digital ecosystems expand, large companies remain the primary adopters of advanced security management solutions.

By Vertical

The BFSI sector accounts for 39.9% of market adoption due to strict regulatory oversight and the sensitive nature of financial data. Financial institutions manage large volumes of transactional information and customer records that must be protected from cyber threats. Vulnerability management systems are used to monitor infrastructure, detect potential weaknesses, and ensure compliance with security regulations.

High exposure to digital financial transactions makes the sector a frequent target for cyber attacks. Continuous vulnerability scanning and patch management are essential for maintaining secure financial systems. As digital banking and online financial services expand, cybersecurity investment within the BFSI sector continues to increase.

Investor Type Impact Matrix

Investor Type

Growth Sensitivity

Risk Exposure

Geographic Focus

Investment Outlook

Venture Capital

High

Medium to High

North America, Israel

Focus on advanced cybersecurity analytics startups

Portfolio expansion through integrated security platforms

Institutional Investors

Medium

Medium

Developed Markets

Long-term cybersecurity infrastructure allocation

Government-backed Funds

Medium

Low

North America, Europe

National cybersecurity initiatives

Technology Enablement Analysis

Technology Enabler

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Adoption Momentum

AI-driven Threat Detection and Risk Scoring

+3.0%

North America, Europe

Medium to Long Term

Enhances predictive security monitoring

Automated Vulnerability Scanning Tools

+2.4%

Global

Short to Medium Term

Improves operational efficiency

Cloud-native Security Management Platforms

+1.9%

Global

Medium Term

Supports distributed infrastructure protection

Integration with DevSecOps Pipelines

+1.5%

North America, APAC

Medium to Long Term

Enables proactive vulnerability remediation

Continuous Attack Surface Management Systems

+1.2%

Global

Long Term

Expands enterprise visibility of risks

Key Challenges

Growing number of vulnerabilities making continuous monitoring difficult

High volume of security alerts creating alert fatigue for IT teams

Integration challenges with existing security tools and infrastructure

Shortage of skilled cybersecurity professionals to manage vulnerability programs

Difficulty in prioritizing critical vulnerabilities across large IT environments

Emerging Trends

In the Security and Vulnerability Management (SVM) market, a key trend is the growing adoption of continuous vulnerability monitoring across enterprise infrastructure. Organisations are moving beyond periodic security checks and are implementing systems that scan networks, applications, and endpoints on an ongoing basis to detect weaknesses as soon as they appear.

This approach improves visibility of security gaps and helps teams respond quickly before issues escalate into larger threats. Another trend is the growing use of risk-based prioritisation models that evaluate vulnerabilities according to system exposure, asset importance, and real operational impact. This helps security teams focus on the issues that matter most instead of managing long lists of alerts with equal urgency.

Growth Factors

A major growth factor in this market is the increasing complexity of digital infrastructure across organisations. Businesses rely on a wide range of cloud platforms, applications, connected devices, and remote systems, which expands the number of potential security entry points.

Managing vulnerabilities across such environments requires structured tools that help identify, track, and resolve weaknesses efficiently. Security and vulnerability management platforms provide a clear framework that supports faster remediation and better control over system integrity.

Key Market Segments

By Component

Software

Vulnerability Scanners

Patch Management

Security Incident & Event Management

Risk Assessment

Threat Intelligence

Others

Services

Professional Services

Consulting & Deployment

Pen Testing

Vulnerability Assessment

Incident Response

Support & Maintenance

Managed Services

By Type

Endpoint Security

Cloud Security

Network Security

Application Security

Infrastructure Protection

Data Security

Others (Wireless Security, Web & Content Security, etc.)

By Target

Content Management Vulnerabilities

IoT Vulnerabilities

API Vulnerabilities

Others

By Deployment

Cloud

On-premises

By Enterprise Size

Large Enterprises

SMEs

By Vertical

BFSI

Healthcare

Defense/Government

IT and Telecom

Energy

Retail

Manufacturing

Others

Regional Analysis

North America accounts for 39.2% of the security and vulnerability management (SVM) market, supported by strong cybersecurity investments and strict regulatory frameworks across financial services, healthcare, and government sectors.

Organizations in the region are increasingly deploying vulnerability management platforms to continuously identify, assess, and remediate security weaknesses across complex IT infrastructures. Demand is driven by rising cyber threats, expanding cloud environments, and the need to maintain compliance with evolving data protection and security standards.

The U.S. market is valued at USD 6.31 Bn and is growing at a CAGR of 7.5%, reflecting sustained focus on enterprise risk management and cyber resilience. Adoption is influenced by the increasing number of connected devices, frequent vulnerability disclosures, and growing pressure to strengthen defensive security strategies. Growth is further supported by integration of automated scanning, risk prioritization tools, and continuous monitoring solutions that help organizations manage security exposures more effectively.

Key Regions and Countries

North America

US

Canada

Europe

Germany

France

The UK

Spain

Italy

Russia

Netherlands

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Singapore

Thailand

Vietnam

Rest of APAC

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

South Africa

Saudi Arabia

UAE

Rest of MEA

Competitive Analysis

The Security and Vulnerability Management (SVM) Market is led by global cybersecurity and technology providers that deliver integrated threat detection and vulnerability assessment platforms. Microsoft, Cisco Systems, Inc., and IBM Corporation provide enterprise grade security frameworks combined with cloud security monitoring and endpoint protection tools. Their solutions are widely used across government, healthcare, and financial institutions where strong vulnerability management practices are required.

Dedicated cybersecurity firms contribute specialized vulnerability scanning and risk assessment capabilities. CrowdStrike, Qualys, Inc., Rapid7, and Tenable, Inc. offer advanced platforms for continuous vulnerability detection and threat prioritization. These vendors emphasize real time monitoring, automated remediation workflows, and risk based vulnerability scoring.

Security consulting firms and infrastructure providers further strengthen the ecosystem. AT&T Intellectual Property, Fortra, LLC, and RSI Security deliver managed security services and compliance driven vulnerability management solutions. These organizations support enterprises in implementing risk assessments, regulatory audits, and continuous security monitoring.

The future outlook for the Security & Vulnerability Management (SVM) Market is positive as organizations continue to strengthen their cybersecurity strategies. Demand for SVM solutions is expected to grow because these tools help identify security weaknesses, manage risks, and protect systems from cyber threats.

Increasing use of cloud computing, connected devices, and digital platforms is creating a greater need for continuous vulnerability monitoring and faster threat response. Overall, the market is expected to expand as businesses prioritize proactive security management and stronger protection of their digital infrastructure.

Recent Developments

In January 2025, Absolute Software Corporation expanded its Absolute Resilience Platform by adding integrated patch management, vulnerability scanning, remediation tools, workflow automation, and remote endpoint recovery. This integrated framework strengthens enterprise security operations while reducing endpoint management costs and improving system resilience. As a result, organizations can maintain continuous protection against cyber threats and operational disruptions.

In January 2025, Hackuity.io formed a partnership with cloud security provider Wiz, Inc. through the Wiz Integration Network (WIN) to strengthen risk-based vulnerability management. The collaboration supports seamless security workflows and prioritizes vulnerabilities using Hackuity’s True Risk Score (TRS) methodology. This capability allows IT teams to focus on the most critical threats and improve overall security response efficiency.

Report Scope

Report Features

Description

Market Value (2025)

USD 19 Billion

Forecast Revenue (2035)

USD 49.2 Billion

CAGR(2025-2035)

10%

Base Year for Estimation

2024

Historic Period

2020-2024

Forecast Period

2025-2035

Report Coverage

Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends

Segments Covered

By Component (Software (Vulnerability Scanners, Patch Management, Others), Services (Professional Services (Consulting & Deployment, Pen Testing), Managed Services)), By Type (Endpoint Security, Cloud Security, Others (Wireless Security, Web & Content Security. Etc.)), By Target (Content Management Vulnerabilities, IoT Vulnerabilities, Others), By Deployment (Cloud, On-premises), By Enterprise Size (Large Enterprises, SMEs), By Vertical (BFSI, Healthcare, Others)

Regional Analysis

North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA

Market")