Quick Navigation

- Report Overview

- Top Market Takeaways

- Drivers Impact Analysis

- Restraints Impact Analysis

- By Platform Analysis

- By Component Analysis

- By Technology Analysis

- By Grade Analysis

- By End-User Analysis

- Investor Type Impact Analysis

- Technology Enablement Analysis

- Key Challenges

- Emerging Trends

- Growth Factors

- Key Market Segments

- Regional Analysis

- Competitive Analysis

- Future Outlook

- Recent Developments

- Report Scope

Report Overview

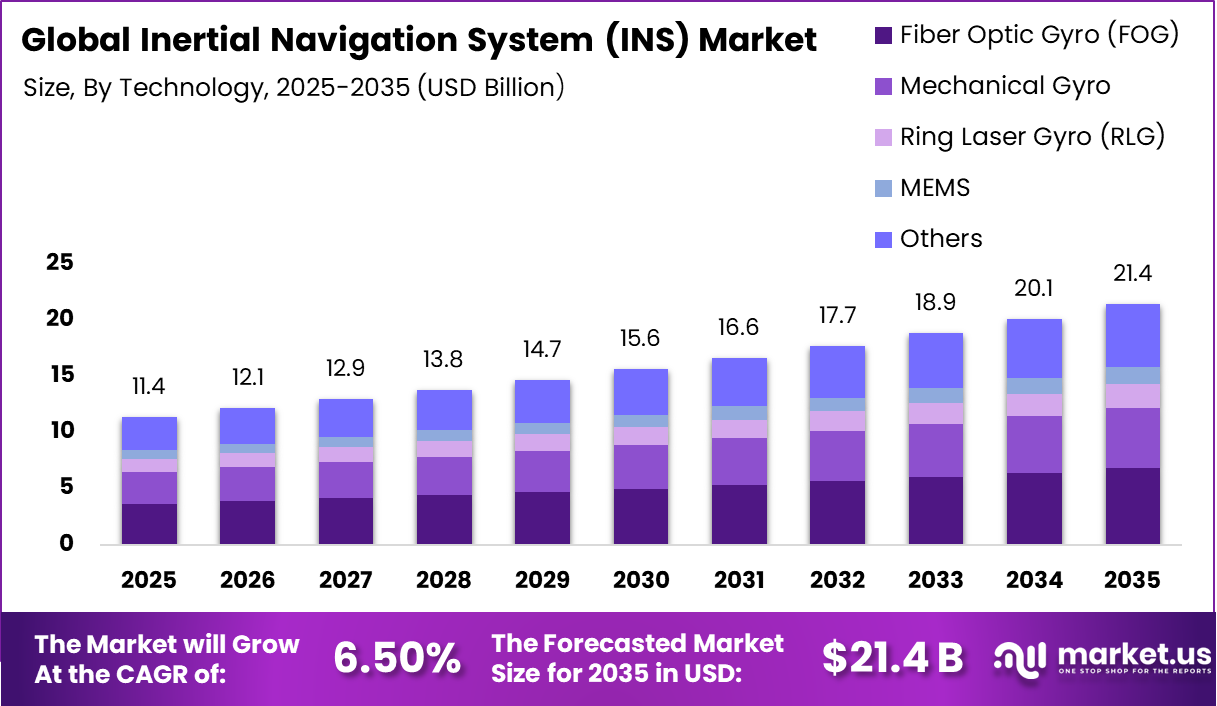

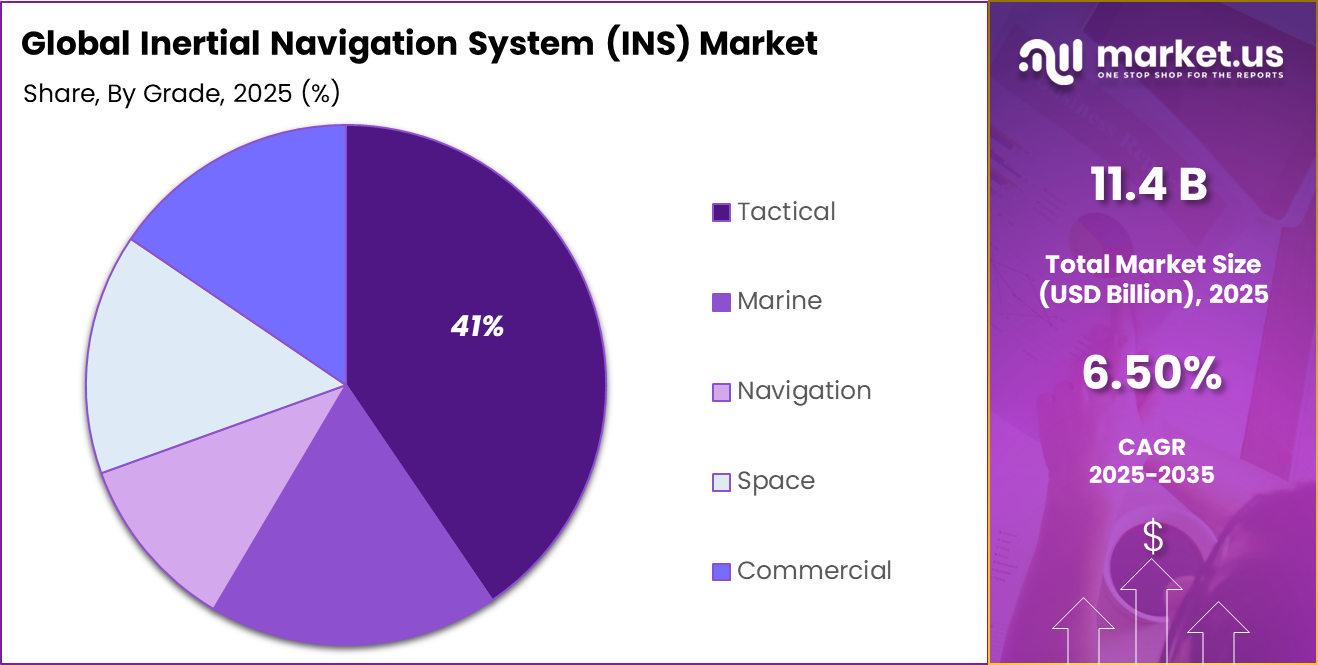

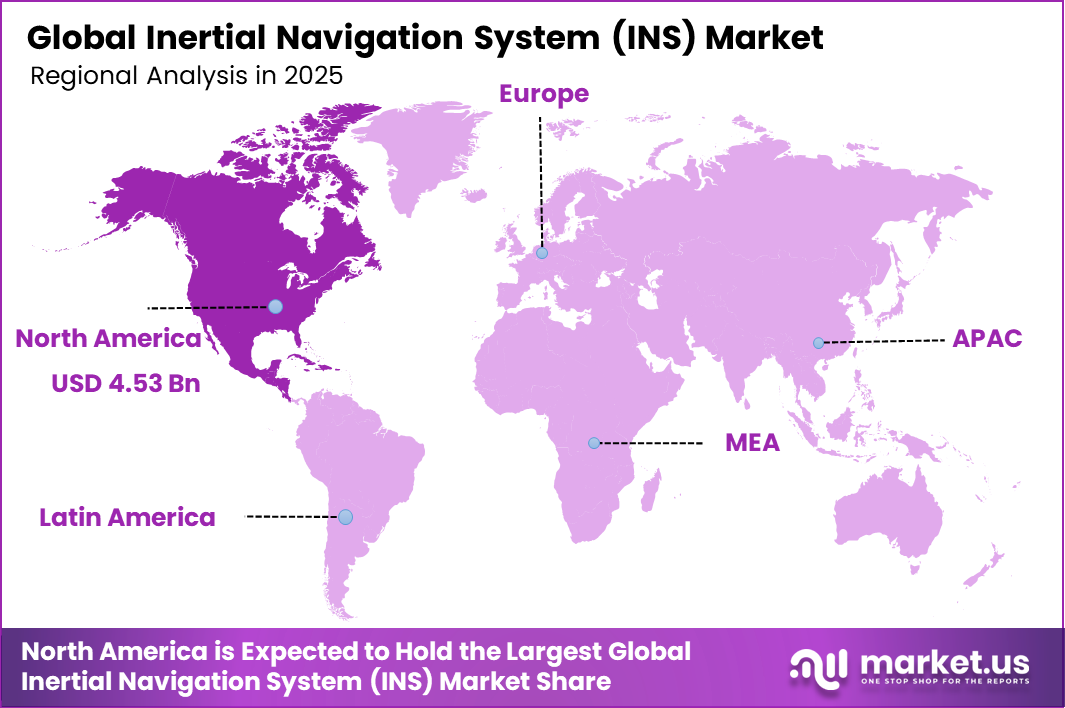

The Global Inertial Navigation System (INS) Market generated USD 11.4 billion in 2025 and is predicted to register growth from USD 12.1 billion in 2026 to about USD 21.4 billion by 2035, recording a CAGR of 6.50% throughout the forecast span. In 2025, North America held a dominant market position, capturing more than a 39.8% share, holding USD 4.53 Billion revenue.

Inertial navigation systems are self contained navigation solutions that determine position, speed, and direction by using motion sensors such as accelerometers and gyroscopes. These systems calculate movement without relying on external signals, which makes them valuable in environments where satellite navigation is weak, blocked, or unavailable.

They are widely used in aircraft, ships, defense platforms, autonomous vehicles, industrial equipment, and guided systems where continuous navigation accuracy is important. As mobility platforms become smarter and more automated, inertial navigation systems are becoming a core technology for reliable positioning and control.

One of the main driving factors is the increasing need for dependable navigation in challenging environments. Aircraft, submarines, missiles, mining vehicles, and autonomous machines often operate where external positioning signals cannot be trusted or consistently received.

In addition, rising investments in defense modernization are supporting demand for precision guidance and mission critical navigation systems. The growth of autonomous transportation and robotics is also encouraging adoption, as these platforms require constant motion sensing and accurate orientation data. Continuous improvements in sensor miniaturization, calibration, and processing capability are further expanding the range of commercial and industrial applications.

Demand for inertial navigation systems is rising as organizations seek accurate and uninterrupted navigation performance. There is a strong preference for systems that offer compact size, low drift error, durability, and smooth integration with satellite navigation and control platforms.

Users are also looking for solutions that can perform under vibration, temperature variation, and harsh operating conditions. The demand is particularly strong in aerospace, defense, marine, automotive, and industrial sectors where reliability is essential. As autonomous operations and precision movement continue to expand, the need for advanced inertial navigation solutions is expected to grow steadily.

Top Market Takeaways

- Platform (Aircraft) Aircraft account for 28.6% of the INS market as they widely use navigation systems for accurate flight control and positioning.

- Component (Gyroscopes) Gyroscopes hold a 42.7% share as they are essential for measuring rotation and maintaining direction.

- Technology (Fiber Optic Gyro – FOG) Fiber Optic Gyro technology leads with 31.9% due to its high precision, low drift, and reliability.

- Grade (Tactical Grade) Tactical-grade systems make up 40.5% of the market offering a good balance between performance and cost.

- End-User (Defense) The defense sector dominates with 73.4% driven by strong demand for military navigation and guidance systems.

- Region (North America) North America holds 39.8% of the market supported by advanced defense and aerospace industries.

- Country (United States) The U.S. market is valued at USD 4.13 billion and is expected to grow at a CAGR of 4.3%.

Drivers Impact Analysis

| Key Driver | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| Rising defense modernization and military spending | +2.6% | North America, Europe, Asia Pacific | Medium to long term | Defense demand supports INS adoption |

| Growing use of autonomous vehicles and drones | +2.3% | Global | Medium term | Autonomous systems need precise navigation |

| Increasing aircraft fleet expansion and upgrades | +2.1% | North America, Asia Pacific | Medium to long term | Aviation growth boosts system demand |

| Higher demand for navigation in marine applications | +1.9% | Global | Medium term | Ships require reliable positioning systems |

| Need for GPS-independent navigation solutions | +1.7% | Global | Long term | INS ensures operation in denied environments |

Restraints Impact Analysis

| Key Restraint | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| High cost of advanced INS components | -2.4% | Emerging markets | Short to medium term | Costs limit wider adoption |

| Sensor drift and calibration challenges | -2.1% | Global | Medium term | Accuracy issues need correction |

| Complex integration with existing platforms | -1.8% | Global | Medium term | Integration delays deployments |

| Dependence on specialized manufacturing | -1.5% | Global | Medium to long term | Supply constraints affect growth |

| Export controls and regulatory barriers | -1.3% | North America, Europe | Long term | Regulations restrict trade flows |

By Platform Analysis

The aircraft segment accounted for 28.6% of the market share, reflecting its strong role in supporting accurate navigation, positioning, and flight stability. This dominance is supported by the growing need for dependable navigation systems that can operate independently of external signals. Aircraft operators rely on inertial navigation systems to maintain route accuracy, especially during long-distance flights and challenging operating conditions.

Another factor driving this segment is the increasing use of advanced avionics and autonomous flight support technologies. INS solutions help improve operational safety and ensure continuous navigation performance during signal disruptions. Their importance in both military and commercial aviation continues to support segment growth.

By Component Analysis

The gyroscopes segment held 42.7% share, driven by their critical function in measuring angular motion and maintaining orientation accuracy. Gyroscopes are a core component of inertial navigation systems, helping platforms determine direction and movement in real time. Their reliability and precision make them essential across air, land, and marine applications.

In addition, advances in sensor design and miniaturization have improved gyroscope performance while reducing size and weight. These improvements have expanded adoption in modern navigation systems that require compact and highly accurate components.

By Technology Analysis

The fiber optic gyro segment captured 31.9% of the market, reflecting strong demand for high-precision and low-maintenance navigation technology. FOG systems are valued for their accuracy, durability, and resistance to mechanical wear since they have no moving parts. These features make them highly suitable for mission-critical applications.

Furthermore, fiber optic gyro technology performs well in harsh environments and under continuous operation. Its ability to deliver stable navigation data with low drift has encouraged wider use in aerospace, defense, and industrial platforms requiring dependable guidance systems.

By Grade Analysis

The tactical grade segment accounted for 41% of the market share, driven by the need for a balance between performance, cost efficiency, and operational durability. Tactical grade INS solutions are widely used in defense vehicles, unmanned systems, and guided platforms where reliable navigation is essential. They offer strong accuracy levels suitable for demanding field conditions.

Moreover, defense organizations prefer tactical grade systems for applications requiring rugged performance without the higher cost of strategic-grade units. Their versatility and practical deployment benefits continue to strengthen adoption across multiple mission environments.

By End-User Analysis

The defense segment held 73.4% share, reflecting its dominant role in the adoption of inertial navigation systems for military operations. Defense forces rely on INS technology for aircraft, missiles, naval vessels, armored vehicles, and unmanned systems where precise navigation is mission critical. These systems remain effective even when external positioning signals are unavailable.

In addition, rising focus on modern warfare capabilities and secure navigation technologies has increased investment in advanced INS platforms. Defense users prioritize resilience, accuracy, and continuous performance, which has reinforced strong demand for inertial navigation systems in this segment.

Investor Type Impact Analysis

| Investor Type | Growth Sensitivity | Risk Exposure | Geographic Focus | Investment Outlook |

|---|---|---|---|---|

| Venture capital firms | Moderate | High | US, Europe | Investing in autonomous navigation startups |

| Private equity firms | Moderate | Moderate | North America and Europe | Scaling aerospace component providers |

| Corporate investors | High | Moderate | Global | Strategic investments in defense and mobility |

| Institutional investors | Moderate | Low to moderate | Developed markets | Prefer stable aerospace technology firms |

| Government and public funding bodies | Very high | Low | Global | Supporting defense and transport programs |

Technology Enablement Analysis

| Technology | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| MEMS-based inertial sensors | +2.8% | Global | Medium to long term | Reduces size and cost |

| AI-assisted navigation correction systems | +2.5% | US, Europe | Medium term | Improves accuracy over time |

| Integration with GNSS hybrid navigation | +2.3% | Global | Medium term | Enhances positioning reliability |

| Fiber optic and ring laser gyroscopes | +2.0% | Developed markets | Long term | Supports high-precision use cases |

| Edge computing for real-time navigation | +1.8% | Global | Medium to long term | Speeds onboard decision-making |

Key Challenges

- High cost of advanced INS components and systems.

- Complex design and integration with existing platforms.

- Accuracy drift over time without external correction signals.

- Need for regular calibration and maintenance.

- High dependence on quality sensors and components.

- Size and weight constraints in compact devices.

- Power consumption can reduce battery life in mobile systems.

- Limited skilled professionals for installation and operation.

- Performance issues in harsh environments such as vibration or heat.

- Strict regulatory and certification requirements in defense and aviation.

Emerging Trends

The inertial navigation system market is evolving toward smaller, smarter, and more precise navigation solutions designed for demanding environments. One of the key emerging trends is the shift toward miniaturized sensors based on MEMS technology, which allows inertial systems to be integrated into compact platforms such as drones, autonomous vehicles, and portable defense equipment.

Another important trend is the growing use of hybrid navigation systems that combine inertial sensors with satellite positioning, vision systems, and real time mapping to improve accuracy when external signals are weak or unavailable. There is also increasing focus on AI assisted calibration and error correction, helping systems maintain stable performance over long operating periods. In addition, ruggedized INS units are gaining traction for harsh environments such as marine, aerospace, and industrial operations where vibration and temperature changes are common. Edge processing capabilities are also being added, allowing faster onboard decision making without relying on constant connectivity.

Growth Factors

The growth of this market is driven by the rising demand for reliable positioning and guidance in applications where continuous navigation is critical. Defense modernization programs, commercial aviation upgrades, and the expansion of autonomous mobility are creating strong need for systems that can operate independently of external signals. The increasing use of drones for surveying, inspection, logistics, and security is also supporting adoption, as these platforms require stable motion sensing and route control.

Another major factor is the need for resilient navigation in areas where satellite signals may be blocked, jammed, or degraded. Industries are also focusing on higher safety standards and operational precision, which encourages investment in advanced inertial solutions. Furthermore, ongoing improvements in sensor accuracy, power efficiency, and manufacturing techniques are making inertial navigation systems more accessible across a wider range of commercial and industrial uses.

Key Market Segments

By Platform

- Aircraft

- Fixed-Wing

- Rotary-Wing

- Missiles

- Space Launch Vehicles

- Marine Vessels

- Military Armored Vehicles

- Unmanned Aerial Vehicles

- Unmanned Ground Vehicles

- Unmanned Maritime Vehicles

- By Component

- Accelerometers

- Gyroscopes

- Algorithms & Processors

By Technology

- Mechanical Gyro

- Ring Laser Gyro (RLG)

- Fiber Optic Gyro (FOG)

- Microelectromechanical Systems (MEMS)

- Others

By Grade

- Marine

- Navigation

- Tactical

- Space

- Commercial

By End-User

- Commercial & Government

- Defense

Regional Analysis

North America accounted for 39.8% of the Inertial Navigation System (INS) market, supported by strong demand from aerospace, defense, marine, and autonomous mobility sectors. The region has advanced technological capabilities and a high concentration of navigation system developers, which has encouraged continuous adoption of precision guidance solutions.

INS technology is widely used where reliable positioning is required even when satellite signals are weak or unavailable. Growing investments in aircraft modernization, defense platforms, unmanned systems, and smart transportation are further strengthening demand across the region.

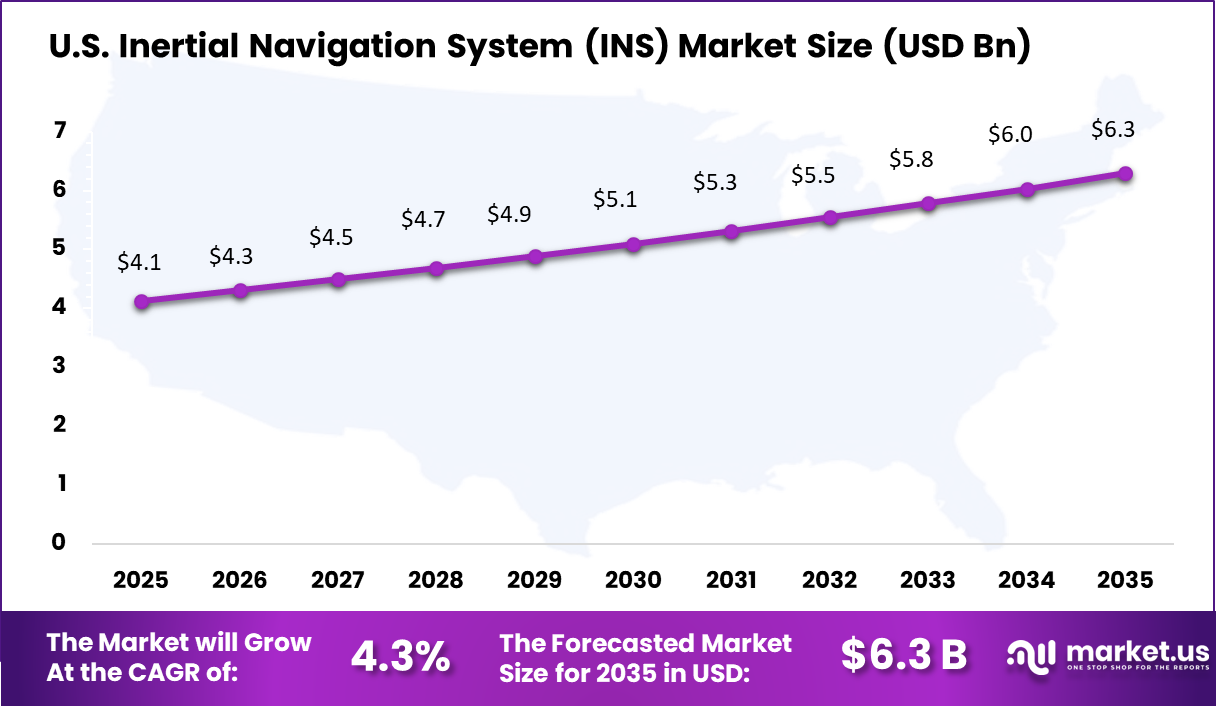

The U.S. market reached USD 4.13 Billion and is projected to grow at a CAGR of 4.3%, driven by steady procurement of defense systems and ongoing upgrades in commercial aviation and industrial applications. Organizations are adopting advanced INS solutions to improve accuracy, stability, and mission reliability in challenging environments.

Rising use of autonomous vehicles, drones, and marine navigation systems is also contributing to market expansion. In addition, continued focus on resilient navigation technologies and next-generation mobility platforms is expected to support stable growth of the INS market in the US over the coming years.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Analysis

The competitive landscape of the Inertial Navigation System (INS) Market is led by major aerospace, defense, and sensor technology companies. Companies such as Honeywell International Inc., Northrop Grumman Corp., Safran Electronics and Defense, Thales Group, Raytheon Technologies Corp., and Trimble Inc. focus on high-precision navigation systems for aircraft, defense platforms, marine systems, and industrial applications.

These players emphasize accuracy, reliability, and performance in challenging environments where continuous positioning is critical. Their strong engineering capabilities, government relationships, and global presence help them maintain a leading position in the market.

At the same time, companies such as Bosch Sensortec GmbH, STMicroelectronics NV, Analog Devices Inc., KVH Industries Inc., NovAtel Inc. (Hexagon), iXblue (Exail), VectorNav Technologies LLC, MEMSIC Inc., Parker Hannifin – LORD MicroStrain, Tersus GNSS Inc., Inertial Labs Inc., Oxford Technical Solutions Ltd., Inertial Sense LLC, and Aeron Systems Pvt. Ltd. compete by offering compact and cost-effective INS solutions based on MEMS and hybrid sensor technologies.

These players focus on drones, autonomous vehicles, robotics, and commercial navigation systems. Competition in this market is driven by sensor accuracy, miniaturization, cost efficiency, and integration with GNSS and autonomous platforms.

Top Key Players in the Market

- Honeywell International Inc.

- Northrop Grumman Corp.

- Safran Electronics and Defense

- Thales Group

- Bosch Sensortec GmbH

- KVH Industries Inc.

- Trimble Inc.

- NovAtel Inc. (Hexagon)

- iXblue (Exail)

- VectorNav Technologies LLC

- MEMSIC Inc.

- Parker Hannifin – LORD MicroStrain

- Tersus GNSS Inc.

- Inertial Labs Inc.

- Oxford Technical Solutions Ltd.

- Inertial Sense LLC

- Aeron Systems Pvt. Ltd.

- STMicroelectronics NV

- Analog Devices Inc.

- Raytheon Technologies Corp.

- Others

Future Outlook

The future outlook for the Inertial Navigation System (INS) Market looks strong as demand for accurate navigation and positioning continues to rise across defense, aerospace, marine, and autonomous vehicles. The market is expected to grow with increasing need for reliable systems that can operate without external signals such as GPS. Companies are anticipated to adopt advanced INS solutions for aircraft, drones, ships, and smart mobility platforms. In the coming years, improvements in sensor technology, miniaturization, and AI-based guidance systems are expected to enhance accuracy and reduce size and cost, supporting wider market adoption.

Recent Developments

- January, 2026 – Honeywell introduces a next‑gen HG1930 MEMS IMU for small drones and robots with lower noise and improved bias stability, targeting SWaP‑constrained platforms. These units feed into integrated INS/GNSS boxes for tactical UAVs and UGVs that must keep navigating when GPS is jammed.

- February, 2026 – Northrop Grumman enhances its LN‑200/300 family with updated fiber‑optic gyro electronics to support long‑duration missile and aircraft missions. The company also pushes higher‑grade RLG/FOG INS for submarines and strategic weapons needing very low drift over many hours without external updates.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 11.4 Billion |

| Forecast Revenue (2035) | USD 21.4 Billion |

| CAGR(2025-2035) | 6.50% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2024 |

| Forecast Period | 2025-2035 |

| Report Coverage | Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Platform (Aircraft (Fixed-Wing, Rotary-Wing), Missiles, Space Launch Vehicles, Marine Vessels), By Component (Accelerometers, Gyroscopes, Algorithms & Processors), By Technology (Mechanical Gyro, Ring Laser Gyro (RLG), Fiber Optic Gyro (FOG), Microelectromechanical Systems (MEMS), Others), By Grade (Marine, Navigation), By End-User (Commercial & Government, Defense) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Honeywell International Inc., Northrop Grumman Corp., Safran Electronics and Defense, Thales Group, Bosch Sensortec GmbH, KVH Industries Inc., Trimble Inc., NovAtel Inc. (Hexagon), iXblue (Exail), VectorNav Technologies LLC, MEMSIC Inc., Parker Hannifin – LORD MicroStrain, Tersus GNSS Inc., Inertial Labs Inc., Oxford Technical Solutions Ltd., Inertial Sense LLC, Aeron Systems Pvt. Ltd., STMicroelectronics NV, Analog Devices Inc., Raytheon Technologies Corp., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Market")