Global Indoor Air Purification Market Size, Share, And Industry Analysis Report By Product (Dust Collectors and Vacuums, Fume and Smoke Collectors, Mist Eliminators, Fire and Emergency Exhaust), By Technology (High-Efficiency Particulate Arrestance (HEPA), Electrostatic Precipitators, Activated Carbon, Ionic Filters), By Application (Commercial, Industrial, Residential), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 180262

- Number of Pages: 326

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

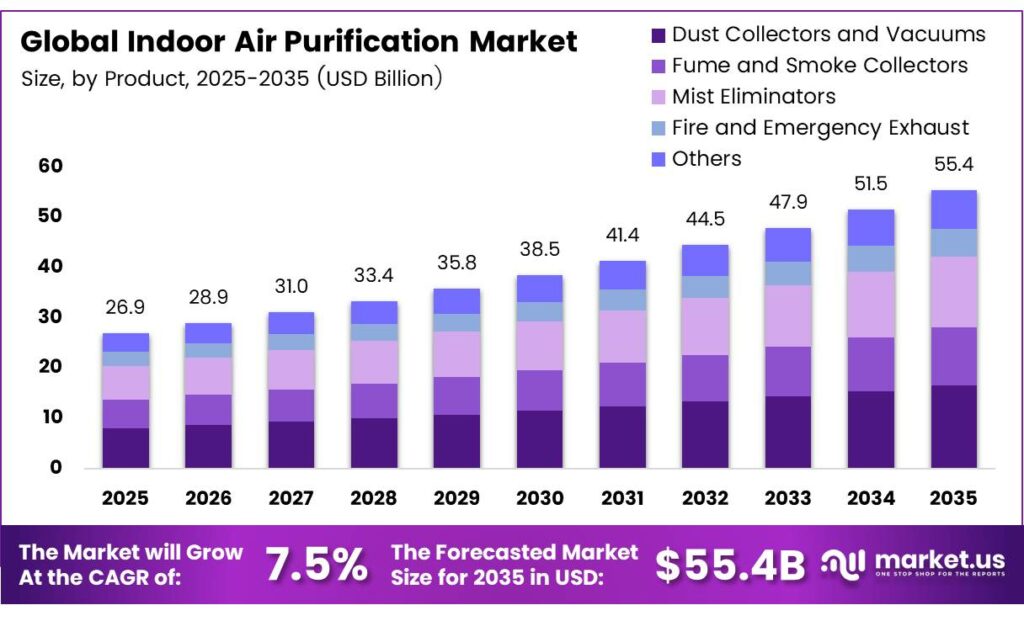

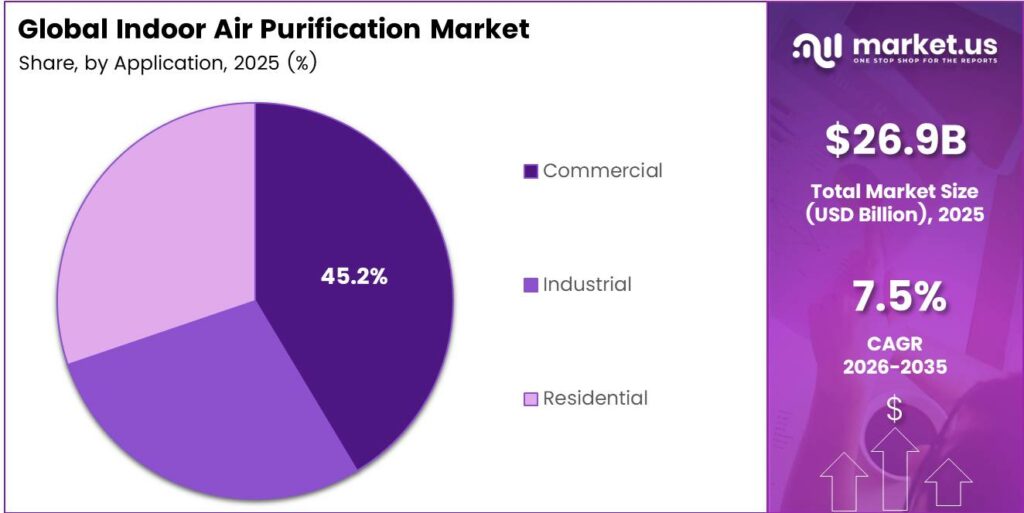

The Global Indoor Air Purification Market size is expected to be worth around USD 55.4 billion by 2035 from USD 26.9 billion in 2025, growing at a CAGR of 7.5% during the forecast period 2026 to 2035.

The indoor air purification market covers systems and devices that remove contaminants from enclosed spaces. These include dust, smoke, allergens, volatile organic compounds, and airborne pathogens. Residential units, commercial buildings, healthcare facilities, and industrial environments all drive consistent demand for reliable filtration solutions.

Modern air purification systems deploy multiple technologies to improve air quality. These include HEPA filtration, activated carbon, electrostatic precipitation, and UV-C light treatment. Manufacturers continuously improve these technologies to handle a broader range of pollutants. Consequently, product performance and consumer confidence continue to improve each year.

- According to the World Health Organization, household air pollution caused 2.9 million deaths globally, including more than 309,000 deaths among children under age 5. This large-scale health burden directly drives global indoor air purification demand, pushing both governments and private buyers toward better filtration investments.

Post-pandemic awareness significantly changed consumer behavior regarding indoor health protection. Households and businesses now invest proactively in air purification rather than reactively addressing air quality concerns. Moreover, smart home integration and app-controlled purifiers have broadened the appeal of indoor air solutions across all income segments.

- The combined effects of ambient and household air pollution cause approximately 6.7 million premature deaths worldwide each year. This alarming scale illustrates the depth of global demand for indoor filtration technologies, reinforcing the market’s long-term growth trajectory across both developed and emerging economies.

Government bodies across North America, Europe, and the Asia Pacific enforce stricter indoor air quality standards. Regulatory frameworks such as OSHA workplace safety rules and EU air quality directives mandate cleaner air in public and commercial spaces. Therefore, compliance requirements directly expand the addressable market for industrial and commercial purification systems.

Key Takeaways

- The Global Indoor Air Purification Market was valued at USD 26.9 billion in 2025 and is projected to reach USD 55.4 billion by 2035, growing at a CAGR of 7.5%.

- Dust Collectors and Vacuums held the dominant share at 35.8% in 2025.

- High-Efficiency Particulate Arrestance (HEPA) led the market with a 41.3% share.

- The Commercial applications dominated with a 45.2% market share.

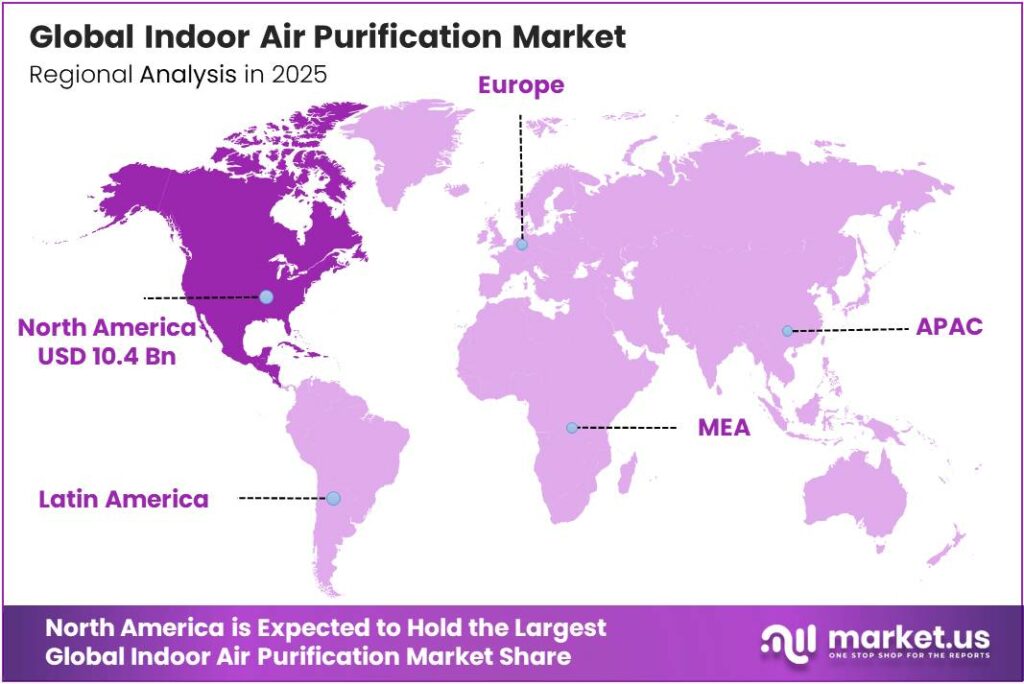

- North America led all regions with a 38.7% market share, valued at USD 10.4 billion.

By Product Analysis

Dust Collectors and Vacuums dominate with 35.8% due to widespread industrial and commercial adoption.

In 2025, Dust Collectors and Vacuums held a dominant market position in the By Product segment of the Indoor Air Purification Market, with a 35.8% share. Industrial facilities and commercial spaces widely deploy these systems to manage particulate emissions. Their proven effectiveness across manufacturing, woodworking, and food processing environments supports consistent demand.

Fume and Smoke Collectors serve critical safety functions in welding, chemical processing, and laboratory environments. Regulatory mandates around worker health drive adoption in these sectors. Moreover, growing automation in manufacturing increases fume generation, expanding the need for dedicated smoke and fume collection systems in industrial settings.

Mist Eliminators address airborne liquid particles in metalworking and machining operations. These systems prevent coolant mist from contaminating workspaces and compromising equipment. Additionally, stricter occupational health standards push facilities to install mist elimination technology as a baseline requirement rather than an optional upgrade.

Fire and Emergency Exhaust systems manage smoke and toxic gases during fire events in enclosed structures. Building codes and life safety regulations mandate their installation in commercial and high-rise residential buildings. Consequently, construction activity and building retrofit programs continue to sustain demand for emergency exhaust solutions globally.

By Technology Analysis

High-Efficiency Particulate Arrestance (HEPA) dominates with 41.3% due to superior particle capture performance.

In 2025, High-Efficiency Particulate Arrestance (HEPA) held a dominant market position in the By Technology segment of the Indoor Air Purification Market, with a 41.3% share. HEPA filters capture 99.97% of airborne particles at 0.3 microns or larger. This performance standard makes them the preferred choice in healthcare, cleanrooms, and residential settings globally.

Electrostatic Precipitators use charged plates to attract and collect airborne particles without replacing physical filters frequently. These systems appeal to industrial users seeking lower long-term operating costs. However, they require periodic cleaning and perform best in environments with consistent airflow conditions and stable particle loads.

Activated Carbon filters excel at removing odors, gases, and volatile organic compounds from indoor air. Residential and commercial users favor them as complementary layers in multi-stage purification systems. Furthermore, growing awareness of chemical pollutants from furniture and building materials increases demand for activated carbon filtration globally.

Ionic Filters emit charged ions that bind to airborne particles, causing them to settle on surfaces. These filters operate silently and without fan noise, appealing to bedroom and office users. Additionally, newer ionic designs reduce ozone byproduct levels, addressing earlier consumer safety concerns and improving market acceptance across residential segments.

By Application Analysis

Commercial applications dominate with 45.2% due to large-scale ventilation requirements and compliance obligations.

In 2025, Commercial applications held a dominant market position in the By Application segment of the Indoor Air Purification Market, with a 45.2% share. Office buildings, retail centers, hotels, and educational facilities invest in large-scale purification systems to meet air quality standards. Moreover, employee productivity and occupant health increasingly influence commercial real estate investment decisions.

Industrial applications address high-volume airborne contaminants generated by manufacturing processes, chemical handling, and heavy equipment operations. Compliance with occupational health regulations mandates reliable filtration in these environments. Consequently, industrial buyers prioritize durable, high-capacity systems that operate continuously under demanding conditions without frequent maintenance interruptions.

Residential applications cover standalone units and whole-home systems designed for households. Post-pandemic health awareness significantly expanded consumer interest in home air purification. Furthermore, rising urbanization and outdoor pollution levels in developing countries push residential buyers toward portable and fixed air purification solutions for daily indoor use.

Key Market Segments

By Product

- Dust Collectors and Vacuums

- Fume and Smoke Collectors

- Mist Eliminators

- Fire and Emergency Exhaust

- Others

By Technology

- High-Efficiency Particulate Arrestance (HEPA)

- Electrostatic Precipitators

- Activated Carbon

- Ionic Filters

- Others

By Application

- Commercial

- Industrial

- Residential

Emerging Trends

Multi-Layered Filtration and AI-Driven Intelligence Reshape Indoor Air Purification

Manufacturers now combine HEPA, activated carbon, and UV-C technologies into single units to address multiple pollutant types simultaneously. This multi-layered approach delivers broader protection against particulates, gases, and biological contaminants. China imported $1,666,636.52K worth of filtration and purification machinery in 2024, reflecting strong regional demand for advanced multi-technology systems.

Consumer preference increasingly favors compact, portable purifiers with smart app connectivity. Users want real-time air quality data and remote control via smartphones. Moreover, brands integrating Wi-Fi and voice assistant compatibility attract premium buyers who prioritize convenience alongside health performance in their purchasing decisions.

Artificial intelligence integration now enables purifiers to adjust filtration intensity based on real-time air quality readings. AI-powered systems detect pollution spikes and respond automatically without user input. Additionally, manufacturers increasingly design products with low-energy motors and quiet operation modes, targeting both sustainability-conscious buyers and noise-sensitive environments such as bedrooms and offices.

Drivers

Escalating Health Risks and Regulatory Mandates Drive Strong Indoor Air Purification Demand

Respiratory health issues, including asthma, allergies, and chronic obstructive pulmonary disease, drive households and businesses to invest in advanced filtration. The United States imported $6,122,443.30K worth of filtering and purifying machinery in 2024. This import volume reflects the depth of domestic demand for high-performance indoor air purification hardware.

Rapid urbanization intensifies indoor pollutant exposure from traffic emissions, construction dust, and dense building environments. Workers and residents in high-density urban areas face elevated risks from particulate matter and chemical vapors. Consequently, demand for commercial and residential purification systems accelerates in cities across Asia, the Middle East, and Latin America.

Strict workplace safety regulations across North America and Europe mandate superior indoor air quality in offices, factories, and healthcare settings. OSHA standards, EU directives, and national occupational health laws require employers to deploy certified filtration systems. Therefore, regulatory compliance becomes a primary procurement driver rather than a discretionary investment for businesses in regulated industries.

Restraints

High Maintenance Costs and Performance Variability Limit Broader Market Adoption

Substantial maintenance expenses represent a significant barrier to long-term adoption of air purification systems. Filter replacement costs accumulate over time, particularly for HEPA and multi-stage units requiring frequent servicing. Moreover, budget-constrained households and small businesses often defer maintenance, reducing system effectiveness and dampening repeat purchase cycles in price-sensitive segments.

Inconsistent performance across varying room sizes and airflow conditions reduces consumer confidence in certain product categories. Purifiers designed for smaller spaces often underperform when deployed in larger open-plan environments. Consequently, buyers who experience poor outcomes become reluctant to upgrade or recommend products, creating negative word-of-mouth that slows adoption in competitive retail and online channels.

The gap between laboratory-tested performance and real-world results frustrates both residential and commercial buyers. Products certified under controlled test conditions may not replicate those results in buildings with complex ventilation layouts. Additionally, a lack of standardized independent verification frameworks across markets makes it difficult for buyers to compare product claims with confidence.

Growth Factors

IoT Integration, Healthcare Demand, and Emerging Market Expansion Accelerate Market Growth

IoT-enabled air purifiers allow facility managers and homeowners to monitor air quality remotely and schedule maintenance automatically. These connected systems reduce operational costs and improve system uptime. The European Union imported $2,960,556.68K of filtration and purification machinery in 2024, signaling strong regional investment in advanced connected air management infrastructure.

Healthcare facilities and senior living communities represent fast-growing demand centers for high-performance air purification. Hospitals, clinics, and aged care homes require continuous pathogen and particulate control to protect vulnerable occupants. Moreover, aging global populations and expanding healthcare infrastructure in emerging economies create sustained procurement pipelines for medical-grade filtration systems.

Hybrid systems combining air purification with HVAC integration gain traction among commercial real estate developers and facility managers. These integrated solutions reduce installation footprints and improve energy efficiency compared to standalone units. Additionally, rapid urban infrastructure growth in Southeast Asia, Africa, and Latin America opens large untapped markets for both residential and commercial purification solutions.

Regional Analysis

North America Dominates the Indoor Air Purification Market with a Market Share of 38.7%, Valued at USD 10.4 Billion

North America leads the global indoor air purification market with a 38.7% share valued at USD 10.4 billion in 2025. The United States exported filtering and purifying machinery, confirming the region’s dual role as both a major consumer and manufacturer of air purification equipment. Robust healthcare, commercial real estate, and industrial sectors sustain this leadership position.

Europe represents a mature but steadily growing market for indoor air purification systems. EU energy efficiency directives and indoor air quality regulations push commercial and public building owners to upgrade filtration infrastructure. The United Kingdom imported filtration and purification machinery, reflecting sustained investment across the region’s industrial and commercial sectors.

Asia Pacific experiences rapid demand growth driven by severe urban air pollution and expanding industrial activity. China and India lead regional adoption as governments enforce stricter factory emission standards. Japan and China exported filtration machinery, illustrating both domestic consumption and large-scale manufacturing capacity across the region.

Latin America presents growing opportunities as urban populations expand and environmental awareness increases. Brazil and Mexico lead regional demand, driven by industrial growth and stricter occupational health enforcement. Moreover, rising middle-class spending on home health products gradually expands the residential purification segment across major cities in the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

FLSmidth operates as a global engineering company serving the cement and mining industries with specialized air pollution control and filtration systems. The company delivers large-scale baghouse filters, electrostatic precipitators, and gas cleaning systems for heavy industrial environments. FLSmidth’s engineering expertise and global service network position it as a trusted partner for industrial facilities managing high-volume emission control requirements.

Camfil specializes in high-performance air filtration solutions for commercial, industrial, and life science applications. The company designs HEPA and molecular filtration systems for cleanrooms, hospitals, and data centers. Camfil emphasizes energy efficiency and total cost of ownership in its product development strategy. Moreover, its global manufacturing footprint supports consistent supply and technical service across major markets worldwide.

Donaldson Company, Inc. delivers filtration systems across industrial, aerospace, and commercial transportation sectors. The company’s air filtration portfolio covers dust collection, fume extraction, and process filtration for demanding operational environments. Donaldson’s engineering depth and global distribution network enable it to serve diverse industrial customers. Additionally, its investment in connected filtration technology strengthens its position in the growing IoT-enabled purification segment.

Honeywell International Inc. provides a broad range of indoor air quality solutions spanning residential, commercial, and industrial applications. The company integrates air purification with building management systems to deliver smart, scalable solutions. Honeywell’s brand recognition and distribution reach give it competitive advantages in both consumer and enterprise markets. Furthermore, its focus on connected, energy-efficient products aligns with current trends in smart building management globally.

Top Key Players in the Market

- FLSmidth

- Hamon

- Camfil

- Thermax Limited

- Kelin Environmental Protection Technology Co., Ltd.

- KC Cottrell India

- Nederman Holding AB

- Sumitomo Heavy Industries, Ltd.

- Donaldson Company, Inc.

- Babcock and Wilcox Enterprises, Inc.

- SHARP CORPORATION

- Honeywell International Inc.

- DAIKIN INDUSTRIES, Ltd.

- Halton Group

- Trane

Recent Developments

- In 2025, FLSmidth introduced an upgraded fabric filter system with improved pulse-jet cleaning technology and digital monitoring to enhance particulate capture efficiency in industrial indoor settings. The system is positioned for retrofits in existing plants to meet stricter emission norms.

- In 2025, Hamon secured and progressed contracts for the retrofit of dry electrostatic precipitators and hybrid filtration systems at industrial sites in Europe and Asia, aimed at lowering fine particulate matter in operational indoor environments.

Report Scope

Report Features Description Market Value (2025) USD 26.9 Billion Forecast Revenue (2035) USD 55.4 Billion CAGR (2026-2035) 7.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Dust Collectors and Vacuums, Fume and Smoke Collectors, Mist Eliminators, Fire and Emergency Exhaust, Others), By Technology (High-Efficiency Particulate Arrestance (HEPA), Electrostatic Precipitators, Activated Carbon, Ionic Filters, Others), By Application (Commercial, Industrial, Residential) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape FLSmidth, Hamon, Camfil, Thermax Limited, Kelin Environmental Protection Technology Co., Ltd., KC Cottrell India, Nederman Holding AB, Sumitomo Heavy Industries, Ltd., Donaldson Company, Inc., Babcock and Wilcox Enterprises, Inc., SHARP CORPORATION, Honeywell International Inc., DAIKIN INDUSTRIES, Ltd., Halton Group, Trane Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Indoor Air Purification MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Indoor Air Purification MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- FLSmidth

- Hamon

- Camfil

- Thermax Limited

- Kelin Environmental Protection Technology Co., Ltd.

- KC Cottrell India

- Nederman Holding AB

- Sumitomo Heavy Industries, Ltd.

- Donaldson Company, Inc.

- Babcock and Wilcox Enterprises, Inc.

- SHARP CORPORATION

- Honeywell International Inc.

- DAIKIN INDUSTRIES, Ltd.

- Halton Group

- Trane

Our Clients

- 180262

- Mar 2026