Quick Navigation

Report Overview

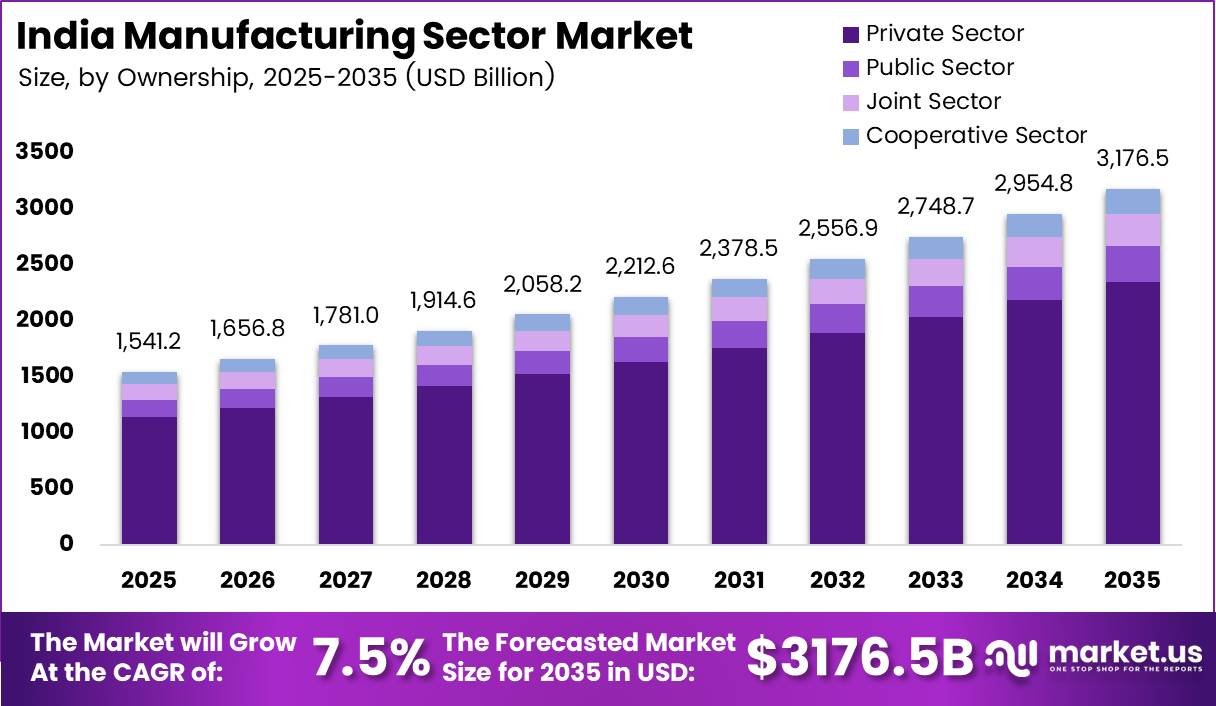

The India Manufacturing Sector Market size is expected to be worth around USD 3,176.5 Billion by 2035 from USD 1,541.2 Billion in 2025, growing at a CAGR of 7.5% during the forecast period 2026 to 2035.

India’s manufacturing sector has entered a structurally different phase of expansion. Government policy, rising capital investment, and a broadening industrial base are pushing output well beyond the commodity-driven growth of the previous decade. The sector now spans automotive, electronics, pharmaceuticals, defense, and green energy, giving it a diversified revenue base that earlier cycles lacked.

The Production-Linked Incentive (PLI) scheme has been the single most consequential policy lever. It has channeled targeted subsidies into electronics assembly, pharmaceutical APIs, specialty chemicals, and advanced automotive components. This approach has shifted India’s manufacturing profile from assembly-only to higher-value production, attracting global OEMs and component suppliers seeking alternatives to single-country supply chains.

Foreign direct investment inflows have accelerated in parallel. Private corporate investment announcements reached INR 14.6 lakh crore in the first half of FY 2025–26, versus INR 7.9 lakh crore in the same period of FY 2024–25, according to PIB. This near-doubling of announced investment signals that global capital is making long-duration bets on India’s industrial trajectory, not simply testing the market.

In May 2026, Reliance Industries operationalized the first phase of its Dhirubhai Ambani Green Energy Giga Complex in Jamnagar and delivered its first 200 MW of heterojunction solar modules. This marks the start of commercial-scale domestic solar manufacturing, a segment that previously depended almost entirely on imports. Such investments indicate that India is building industrial depth, not just capacity.

According to India Briefing and PIB, India’s manufacturing Purchasing Managers’ Index held above 50 for every month measured, with readings of 55.0 in December 2025 and 55.4 in January 2026. PMI readings above 50 signal expansion in new orders, output, and employment. Sustained readings in the mid-50s suggest that demand pressure on factories remains real and broad-based, not concentrated in a single sub-sector.

According to PIB, medium- and high-technology industries accounted for 46.3% of India’s manufacturing value added in FY 2025–26. This figure matters because it shows that nearly half of manufacturing output now comes from technically complex activities. Vendors competing in commodity segments face rising pressure, while suppliers of precision components, advanced materials, and specialized equipment hold defensible pricing power.

The Union Budget 2026–27 reduced the minimum alternate tax rate from 15% to 14% for corporations, directly improving post-tax cash flow for manufacturers. Combined with gross fixed capital formation estimated at 30% of GDP in FY 2025–26, the fiscal environment reinforces long-term industrial asset creation. For investors, this combination of policy support and rising CAPEX commitments reduces the risk profile of new manufacturing capacity decisions.

Key Takeaways

- The India Manufacturing Sector Market was valued at USD 1,541.2 Billion in 2025 and is forecast to reach USD 3,176.5 Billion by 2035.

- The market is forecast to grow at a CAGR of 7.5% from 2026 to 2035.

- By Ownership, the Private Sector dominates with a 73.2% market share in 2025.

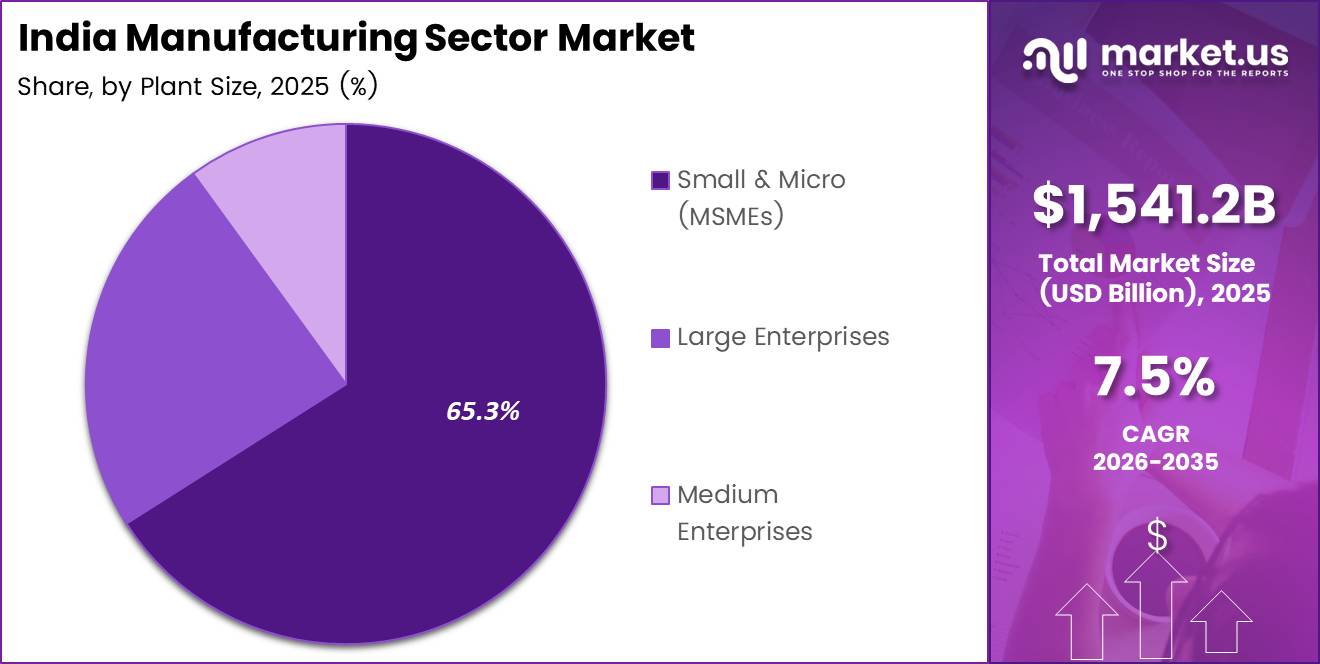

- By Plant Size, Small & Micro (MSMEs) hold the leading position with a 65.3% share in 2025.

- By End-user, the Automotive & Auto Components segment leads with a 17.8% share in 2025.

- Manufacturing PMI readings remained above 50 every month in 2026, with 56.9 recorded in February 2026.

- Manufacturing CAPEX reached INR 2.98 trillion (~USD 31.45 billion) in FY 2025–26, up from INR 2.45 trillion the prior year.

- Medium- and high-technology industries contributed 46.3% of manufacturing value added in FY 2025–26.

- MSMEs employ over 32.82 crore people across 7.47 crore enterprises and contribute 35.4% of manufacturing output.

- India’s CIP index ranking improved from 40th in 2022 to 37th in 2023.

Ownership Analysis

Private Sector dominates with 73.2% due to capital flexibility and output scale.

In 2025, the Private Sector held a dominant market position in the By Ownership segment of the India Manufacturing Sector Market, with a 73.2% share. Private enterprises drive investment decisions faster than state-owned counterparts, enabling quicker capacity additions. This share reflects decades of deregulation that shifted production responsibility from government entities to commercially driven firms across automotive, consumer goods, and chemicals.

Public Sector manufacturing operates in strategic industries where commercial return is secondary to national security or supply continuity. State-owned enterprises concentrate in defense, heavy engineering, steel, and petroleum refining. Their role is not shrinking but is becoming more focused. Private-public hybrid models are replacing direct state ownership in several legacy sectors.

Joint Sector entities combine government equity with private management discipline. This structure is common in ports, airports, and large infrastructure-linked manufacturing zones. Joint ventures between state governments and global OEMs are expanding, particularly in semiconductor fabrication and defense component manufacturing, where technology transfer requirements make full private ownership impractical.

Cooperative Sector manufacturing is concentrated in agro-processing, dairy, sugar, and handloom textiles. Cooperatives serve rural industrial employment more than export-grade output. However, value-addition programs under the Ministry of Food Processing are gradually improving cooperative plant productivity and product standardization, creating new distribution channels for processed goods.

Plant Size Analysis

Small & Micro (MSMEs) dominate with 65.3% due to enterprise volume and labor deployment scale.

In 2025, Small & Micro (MSMEs) held a dominant market position in the By Plant Size segment of the India Manufacturing Sector Market, with a 65.3% share. According to PIB, MSMEs contribute 35.4% of manufacturing output and employ over 32.82 crore people across 7.47 crore enterprises. Their collective output weight makes MSME policy the most consequential lever for overall manufacturing performance.

Large Enterprises generate disproportionate output relative to their unit count. They anchor industrial corridors, operate capital-intensive facilities, and set quality benchmarks that cascade through supplier networks. Large manufacturers in automotive, steel, and pharmaceuticals are now investing in automation and digital production systems, which will reshape their labor-to-output ratios over the next decade.

Medium Enterprises occupy the structural middle ground between MSME informality and large-enterprise process discipline. They are the segment most responsive to PLI scheme incentives and export promotion programs. Medium manufacturers in electronics, auto components, and specialty chemicals are expanding plant capacity through debt and equity financing at a pace not seen in the prior cycle.

End-user Analysis

Automotive & Auto Components dominates with 17.8% due to integrated supply chain depth and output volume.

In 2025, the Automotive & Auto Components segment held a dominant market position in the By End-user segment of the India Manufacturing Sector Market, with a 17.8% share. India is the third-largest automobile market globally, and domestic OEM demand sustains a deep tier-1 and tier-2 supplier ecosystem. In May 2025, Hyundai Motor India announced the commencement timeline for production at the Talegaon facility acquired from General Motors, bringing a dormant automotive asset back into active manufacturing use.

Textile & Apparel manufacturing serves both domestic consumption and export markets, with government schemes supporting technical textiles and man-made fiber production. The segment benefits from India’s large cotton-growing base but faces competitive pressure from Bangladesh and Vietnam on price-sensitive export categories. Investment in textile parks and plug-and-play infrastructure is improving production efficiency.

Electronics & Electricals manufacturing has received the largest concentration of PLI funding among end-user segments. Mobile handset assembly has already scaled significantly, and the pipeline now includes display modules, printed circuit boards, and semiconductor substrates. This segment carries the highest growth trajectory of any end-user category over the forecast period.

Food & Beverages manufacturing draws on India’s agricultural surplus and serves a domestic consumer base of over 1.4 billion people. Cold chain expansion and organized retail penetration are raising the share of processed food in total food expenditure. This creates direct volume lift for packaged food manufacturers and ingredient suppliers.

Pharmaceuticals & Healthcare manufacturing holds a globally recognized position, with India supplying 20% of global generic medicines by volume. API localization programs have reduced dependence on Chinese imports for key drug ingredients. The segment is moving up the value chain toward biologics, biosimilars, and complex injectables.

Construction Materials manufacturing is directly linked to India’s infrastructure build-out. Cement production reached about 453 million tonnes in FY 2024–25, up from 270 million tonnes in FY 2014–15, according to PIB. This sustained volume growth reflects real demand from roads, railways, housing, and industrial parks, not inventory accumulation.

Chemicals manufacturing covers specialty chemicals, agrochemicals, dyes, and petrochemical derivatives. India’s chemical manufacturers are benefiting from global supply chain diversification away from China. New chemical clusters in Gujarat and Andhra Pradesh are attracting both domestic and foreign investment in capacity creation.

Aerospace & Defence manufacturing is undergoing a structural shift from import dependence to domestic production. The government’s defence indigenization policy mandates local content requirements across procurement categories. Private sector participation is expanding, with licensed production of engines, airframes, and radar systems entering the manufacturing pipeline.

Metals manufacturing, including steel, aluminum, and copper, underpins most other industrial segments. During April–October FY 2025–26, crude steel production increased by 11.7% and finished steel production grew by 10.8% compared with the prior year, according to PIB. This output expansion directly supports automotive, machinery, and construction equipment manufacturers downstream.

Machinery and Capital Goods manufacturing determines India’s self-sufficiency in industrial tooling and production equipment. The sector is a leading indicator of broader manufacturing investment cycles. Rising CAPEX commitments across sectors are driving orders for domestic machine tool manufacturers, presses, and industrial automation equipment.

Others encompasses furniture, rubber, plastics, glass, and miscellaneous industrial products. These segments collectively serve as fillers across manufacturing value chains and serve end consumers through branded and unbranded channels.

Key Market Segments

By Ownership

- Private Sector

- Public Sector

- Joint Sector

- Cooperative Sector

By Plant Size

- Small & Micro (MSMEs)

- Large Enterprises

- Medium Enterprises

By End-user

- Automotive & Auto Components

- Textile & Apparel

- Electronics & Electricals

- Food & Beverages

- Pharmaceuticals & Healthcare

- Construction Materials

- Chemicals

- Aerospace & Defence

- Metals

- Machinery and Capital Goods

- Others

Drivers

Rising Capital Investment and Government-Backed Industrial Policy Are Accelerating Manufacturing Capacity Expansion

India’s central government capital expenditure rose from INR 3.07 lakh crore in FY 2018–19 to INR 11.21 lakh crore in FY 2025–26, according to PIB. This near-fourfold increase in public investment has funded road, rail, port, and industrial corridor infrastructure. Without this foundation, private manufacturers cannot operate efficiently at scale.

According to India Briefing, manufacturing CAPEX reached INR 2.98 trillion (~USD 31.45 billion) in FY 2025–26, up from INR 2.45 trillion (~USD 24.8 billion) in FY 2024–25. This 21.6% year-on-year increase in manufacturing-specific investment signals that firms are committing capital ahead of demand, not in response to it. Early movers are securing industrial land, talent, and supply agreements before capacity tightens.

In April 2025, ebm-papst began construction of its third India manufacturing plant in Chennai with an investment of about EUR 36 million, expanding local production of fans, motors, and ventilation technologies. This decision by a specialized European industrial manufacturer illustrates the broader pattern: global suppliers are building permanent production bases in India rather than serving the market through exports. This deepens India’s industrial ecosystem over time.

Restraints

Infrastructure Bottlenecks and Cost Volatility Compress Manufacturing Margins and Deter Sustained Capacity Commitment

Logistics inefficiencies add direct cost to every unit of manufactured output in India. Road freight dominates industrial supply chains, but highway capacity, last-mile connectivity, and warehousing infrastructure remain uneven across states. Manufacturers in inland locations bear disproportionately higher logistics costs compared to those in coastal industrial clusters, creating geographic concentration risks.

Volatility in raw material costs and energy prices compounds the margin pressure that logistics costs create. India’s coal production reached 1,047.52 million tonnes in FY 2024–25, a 4.98% increase, according to PIB. However, domestic production growth has not fully insulated energy-intensive manufacturers from global price movements. Steel, cement, and chemical producers remain exposed to input cost cycles that compress operating margins during commodity upswings.

According to India Briefing, manufacturing absorbed 50.17% of total private corporate CAPEX in FY 2025–26, with its share expected to rebalance to 44.35% in FY 2026–27 as energy-sector investments rise. This rebalancing reflects investor sensitivity to cost environments. When input costs rise, capital rotates away from manufacturing toward sectors with more predictable returns, slowing the pace of capacity expansion.

Growth Factors

Semiconductor and Advanced Electronics Manufacturing Are Creating High-Value New Revenue Streams for India’s Industrial Base

In May 2026, Intel Corporation and 3D Glass Solutions signed an agreement with the Odisha government to invest approximately USD 3.3 billion in an advanced semiconductor substrate manufacturing facility. This represents one of India’s largest semiconductor manufacturing investments to date. The deal confirms that India’s push into chip-related manufacturing has moved from aspiration to signed capital commitment.

The localization of global supply chains is creating durable demand for India’s manufacturing base beyond traditional cost arbitrage. Global buyers across electronics, automotive, and industrial equipment are actively qualifying Indian suppliers to reduce single-source risk. According to PIB, industrial production grew 7.8% in December 2025, the strongest expansion in over two years, with electronics and motor vehicles leading sectoral output gains.

Green manufacturing represents a new category of industrial revenue that did not exist at scale a decade ago. Reliance Industries’ first 200 MW of heterojunction solar modules from the Jamnagar Giga Complex, operationalized in May 2026, demonstrates that domestic demand for clean energy components can now be met by Indian manufacturers. This removes import dependency in a segment where demand will only increase over the forecast period.

Emerging Trends

Industry 4.0 Adoption and Industrial Corridor Development Are Redefining India’s Manufacturing Competitiveness Architecture

According to PIB, India’s ranking in UNIDO’s Competitive Industrial Performance index improved from 40th in 2022 to 37th in 2023. This three-position gain in a single year reflects measurable improvements in manufacturing value density, export sophistication, and technology intensity. Countries that climb this index consistently attract higher-value foreign investment in subsequent years.

Integrated industrial corridors are concentrating manufacturing activity into zones with shared utilities, logistics access, and regulatory clearance. This clustering reduces per-unit infrastructure cost for manufacturers and creates labor market density that supports skills development. The Delhi-Mumbai Industrial Corridor and Chennai-Bengaluru Industrial Corridor are the most advanced examples of this structural shift in how Indian manufacturing geography is organized.

Export-oriented manufacturing across high-value categories is a deliberate policy objective, not a market outcome. India’s rankings in defense export approvals, pharmaceutical export certifications, and electronics component export schemes have all improved since 2020. Combined with a rising share of medium- and high-technology industries in total output, this trend indicates that India’s manufacturing export basket is becoming less price-sensitive and more quality-driven over time.

Key Company Insights

Reliance Industries Ltd has positioned itself as the anchor of India’s green manufacturing transition. Its Jamnagar Giga Complex is the largest single clean-energy manufacturing investment by an Indian corporation. By delivering the first 200 MW of solar modules in May 2026, Reliance has established a first-mover advantage in a segment where domestic demand will compound for decades. Few Indian manufacturers have the balance sheet scale to replicate this vertical integration.

Tata Motors Ltd holds a strategically differentiated position across commercial vehicles, passenger cars, and electric mobility in one of the world’s fastest-growing automotive markets. Its ownership of Jaguar Land Rover gives it global manufacturing and engineering exposure. However, the transition to electric vehicles requires simultaneous investment in battery supply chains and charging infrastructure, creating capital allocation complexity that smaller competitors do not face.

Mahindra & Mahindra Ltd has built a dominant position in utility vehicles and farm equipment, two segments with structurally different demand cycles that provide natural revenue hedging. Its farm machinery business benefits directly from government agricultural support programs, while the SUV segment benefits from India’s rising middle-class consumption. This dual exposure reduces the firm’s sensitivity to single-sector downturns.

Maruti Suzuki India Ltd commands the largest share of India’s passenger vehicle market through a combination of price competitiveness, wide dealership reach, and high brand trust in tier-2 and tier-3 cities. Its manufacturing operations in Gurugram and Manesar run at high utilization rates. However, its concentration in small and mid-size vehicles creates exposure to competitive pressure from both domestic SUV manufacturers and incoming global electric vehicle brands.

Key Players

- Reliance Industries Ltd

- Tata Motors Ltd

- Mahindra & Mahindra Ltd

- Maruti Suzuki India Ltd

- Tata Steel Ltd

- Larsen & Toubro Ltd

- JSW Steel Ltd

- Hindustan Unilever Ltd

- Godrej Group

- Ashok Leyland Ltd

- Hero MotoCorp Ltd

- TVS Motor Company Ltd

- Bharat Forge Ltd

Recent Developments

- May 2026 – Intel Corporation and 3D Glass Solutions signed an agreement with the Odisha government to invest approximately USD 3.3 billion in an advanced semiconductor substrate manufacturing facility, representing one of India’s largest semiconductor manufacturing investments to date.

- March 2025 – Bel Fuse Inc. inaugurated a new manufacturing facility in Manesar, Gurugram, following its November 2024 acquisition of Enercon Technologies. The new plant is expected to double the company’s manufacturing capacity in India for power solutions and protection products.

- May 2025 – Hyundai Motor India announced the commencement timeline for production at the Talegaon manufacturing facility acquired from General Motors, bringing a dormant automotive manufacturing asset back into active operation.

- March 2025 – Haier India announced an INR 800 crore investment to expand domestic air-conditioner manufacturing and establish PCB manufacturing capabilities in India, deepening local electronics production infrastructure.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1,541.2 Billion |

| Forecast Revenue (2035) | USD 3,176.5 Billion |

| CAGR (2026-2035) | 7.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Ownership (Private Sector, Public Sector, Joint Sector, Cooperative Sector), By Plant Size (Small & Micro (MSMEs), Large Enterprises, Medium Enterprises), By End-user (Automotive & Auto Components, Textile & Apparel, Electronics & Electricals, Food & Beverages, Pharmaceuticals & Healthcare, Construction Materials, Chemicals, Aerospace & Defence, Metals, Machinery and Capital Goods, Others) |

| Competitive Landscape | Reliance Industries Ltd, Tata Motors Ltd, Mahindra & Mahindra Ltd, Maruti Suzuki India Ltd, Tata Steel Ltd, Larsen & Toubro Ltd, JSW Steel Ltd, Hindustan Unilever Ltd, Godrej Group, Ashok Leyland Ltd, Hero MotoCorp Ltd, TVS Motor Company Ltd, Bharat Forge Ltd |

| Customization Scope | Customization for segments will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |