Global Incinerator Market Size, Share, And Industry Analysis Report By Technology (Mass Burn Incineration, Modular Incineration, Fluidized Bed Incineration), By Waste Type (Municipal Solid Waste, Hazardous Waste, Industrial Waste), By Capacity (Small Scale, Medium Scale, Large Scale), By Application (Waste-to-Energy, Energy Recovery, Volume Reduction, Environmental Protection), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: December 2025

- Report ID: 168622

- Number of Pages: 384

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

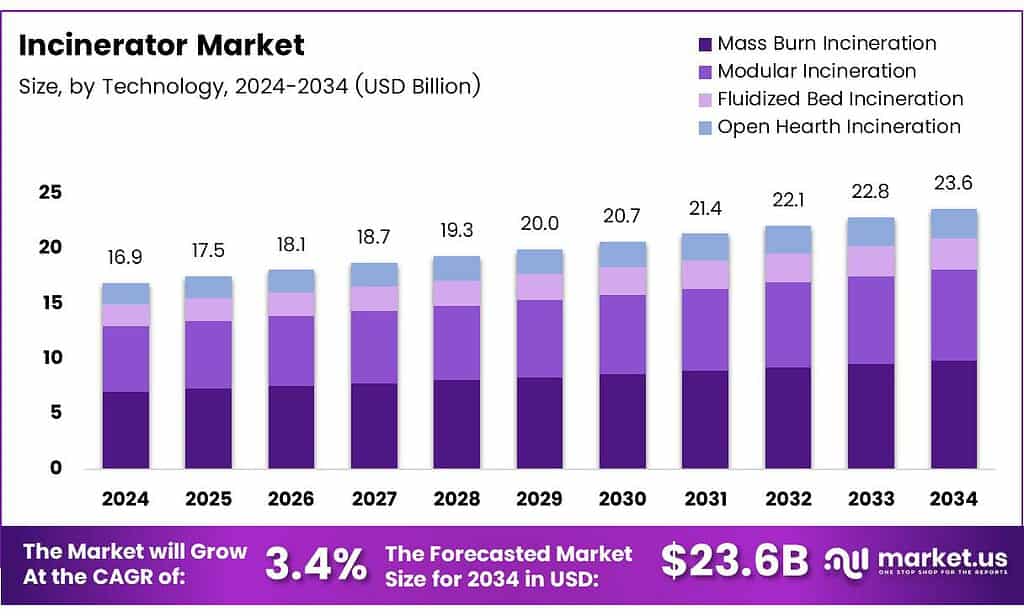

The Global Incinerator Market size is expected to be worth around USD 23.6 billion by 2034, from USD 16.9 billion in 2024, growing at a CAGR of 3.4% during the forecast period from 2025 to 2034.

The Incinerator Market covers engineered systems used for the controlled thermal treatment of municipal, industrial, biomedical, and agricultural waste. In simple business terms, incineration reduces waste volume while managing environmental risk. As landfill constraints increase, incinerators increasingly support regulatory compliance and long-term waste infrastructure planning.

Technical standards strongly shape system design and capital spending. Incinerators are required to sustain flue gas temperatures of at least 850°C to ensure full destruction of organic toxins. Where waste calorific value is insufficient, auxiliary burners stabilise thermal performance, increasing demand for advanced combustion control technologies.

- Energy recovery strengthens the commercial case for incineration. Heat from combustion commonly produces steam at around 400°C under pressures of 550–600 psi for electricity generation. After heat extraction, flue gas temperatures fall near 200°C before cleaning, supporting emission control and overall system efficiency.

Agricultural waste treatment presents additional opportunities. High-capacity animal incinerators now handle loading volumes up to 1300 kg, enabling biosecure on-site disposal. Consequently, large livestock farms adopt rotary kiln systems with primary and secondary chambers to improve burnout efficiency and disease risk management.

An incinerator is a closed combustion unit designed to safely destroy complex waste streams. Typically, it integrates combustion chambers, heat recovery units, and emission control systems. Incinerators remain essential for sectors requiring safe disposal, including healthcare, manufacturing, agriculture, and hazardous waste handling activities.

Key Takeaways

- The Global Incinerator Market is projected to grow from USD 16.9 billion in 2024 to USD 23.6 billion by 2034, registering a CAGR of 3.4%.

- Mass burn incineration leads the technology landscape, holding a dominant market share of 44.9% in 2024.

- Municipal solid waste is the largest waste type segment, accounting for 42.1% of the total market share in 2024.

- Large-scale incinerators represent the leading capacity segment with a market share of 49.8%, driven by centralized urban waste infrastructure.

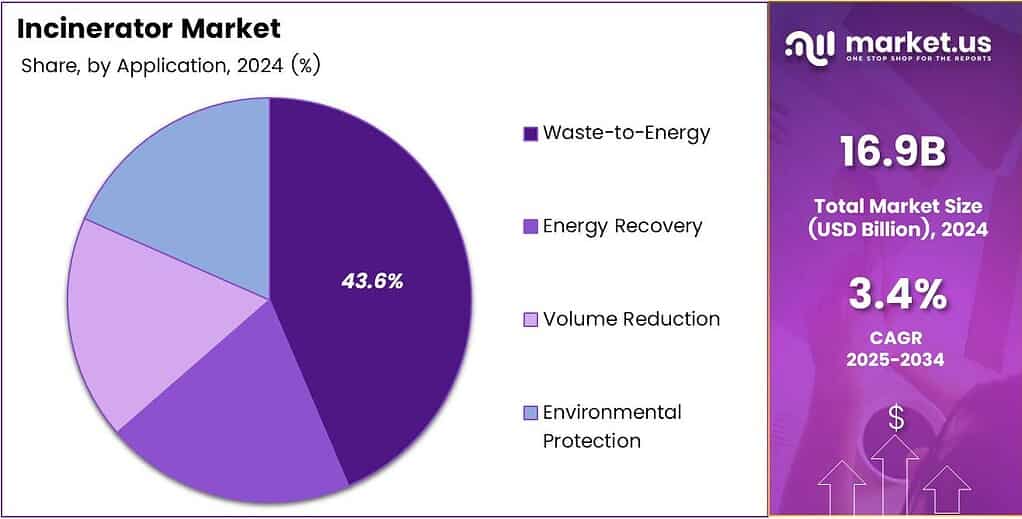

- Waste-to-energy applications dominate end-use demand, capturing 43.6% of the market by combining disposal with power generation.

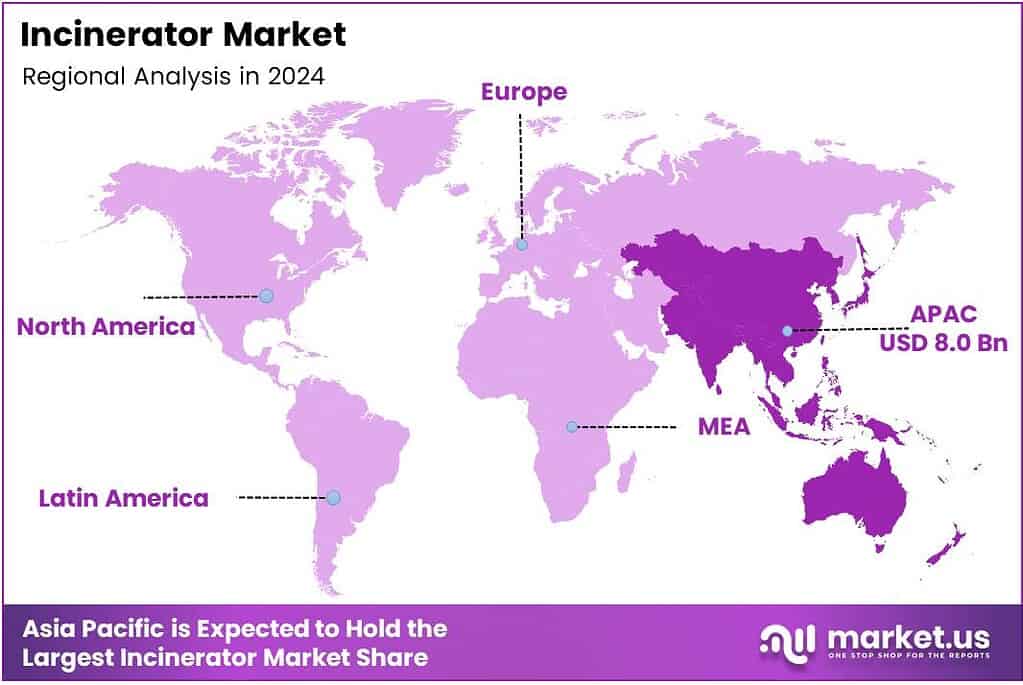

- Asia Pacific is the dominating region, holding 47.9% of the global market with a valuation of USD 8.0 billion in 2024.

By Technology Analysis

Mass Burn Incineration dominates with 44.9% due to its operational simplicity and ability to handle mixed waste streams.

In 2024, Mass Burn Incineration held a dominant market position in the By Technology Analysis segment of the Incinerator Market, with a 44.9% share. It is widely adopted because it processes unsegregated waste directly. Moreover, municipalities prefer it for stable throughput and predictable operating performance.

Modular Incineration supports decentralized waste disposal needs; therefore, it suits smaller towns and remote facilities. These systems are easier to install and relocate when required. However, capacity limitations and lower economies of scale restrict broader adoption when compared with mass burn solutions.

Fluidized Bed Incineration is gaining attention because it improves combustion efficiency for pre-treated waste. Consequently, it supports lower emissions and uniform heat distribution. Nonetheless, it requires consistent waste composition, which increases preprocessing costs and limits flexibility in handling mixed municipal waste streams.

By Waste Type Analysis

Municipal Solid Waste dominates with 42.1% as urban waste volumes continue rising globally.

In 2024, Municipal Solid Waste held a dominant market position in the By Waste Type Analysis segment of the Incinerator Market, with a 42.1% share. Rapid urbanization drives continuous waste generation. Therefore, cities rely on incineration to reduce landfill dependence and manage daily collection efficiently.

Hazardous Waste incineration is essential where chemical and toxic waste requires controlled destruction. As regulations strengthen, demand remains steady. However, high compliance costs and specialized system requirements limit large-scale expansion compared to municipal waste treatment installations.

Industrial Waste incineration supports manufacturing sectors by safely disposing of byproducts. Consequently, it reduces environmental liability for industries. Still, waste variability and the availability of alternative treatment methods influence adoption rates across different industrial regions.

By Capacity Analysis

Large-scale incinerators dominate with 49.8% due to centralized waste management infrastructure.

In 2024, large-scale incinerators held a dominant market position in the By Capacity Analysis segment of the Incinerator Market, with a 49.8% share. These facilities serve metropolitan regions efficiently. Moreover, they deliver economies of scale and consistent energy recovery advantages.

Small-scale incinerators up to fifty tons per day support localized waste needs. Therefore, they are suitable for islands and small communities. However, limited throughput and higher per-unit operating costs restrict widespread deployment.

Medium-scale incinerators bridge the gap between decentralization and efficiency. As a result, they are favored by mid-sized cities. Still, competition from both large centralized plants and emerging alternative technologies affects long-term investment decisions.

By Application Analysis

Waste-to-Energy dominates with 43.6% by combining disposal with power generation benefits.

In 2024, Waste-to-Energy held a dominant market position in the By Application Analysis segment of the Incinerator Market, with a 43.6% share. Governments promote these systems to reduce landfill pressure. Consequently, energy recovery strengthens project financial viability.

Energy Recovery applications focus on capturing heat and electricity from combustion. Therefore, they support grid stability in urban regions. However, efficiency levels depend heavily on waste consistency and technology sophistication. Volume Reduction remains a core application where landfill scarcity exists. Incineration significantly cuts waste volume.

Still, this approach generates limited additional revenue, which affects investment attractiveness. Environmental Protection applications prioritize safe disposal and emission control. As regulations tighten, this segment remains essential. Nevertheless, higher compliance costs influence budget-sensitive regions.

Key Market Segments

By Technology

- Mass Burn Incineration

- Modular Incineration

- Fluidized Bed Incineration

- Open Hearth Incineration

By Waste Type

- Municipal Solid Waste

- Hazardous Waste

- Industrial Waste

- Biomedical Waste

By Capacity

- Small Scale (Up to 50 tons/day)

- Medium Scale (51 to 200 tons/day)

- Large Scale (Over 200 tons/day)

By Application

- Waste-to-Energy

- Energy Recovery

- Volume Reduction

- Environmental Protection

Emerging Trends

Adoption of Advanced Emission Control Technologies Shapes Market Trends

One key trending factor in the incinerator market is the adoption of advanced emission control technologies. Manufacturers are focusing on systems that reduce harmful gases and particulate emissions. This helps operators comply with stricter environmental norms.

- Automation and digital monitoring are also becoming common. Smart control systems improve combustion efficiency and reduce operational errors. These technologies help lower operating costs and improve safety. According to the International Energy Agency (IEA), modern waste-to-energy plants supplied nearly 40 terawatt-hours (TWh) of electricity globally in 2022, enough to power more than 10 million households in urban regions.

Another emerging trend is the shift toward smaller, decentralized incinerators. Healthcare and industrial facilities prefer on-site waste treatment to avoid transportation risks. Overall, cleaner technology, automation, and decentralized models are shaping current market trends.

Drivers

Rising Urban Waste Generation Drives Incinerator Market Growth

Growing urban populations are creating more municipal solid waste every day, which directly supports the demand for incineration systems. As landfill space becomes limited, cities are looking for reliable waste disposal solutions. Incinerators help reduce waste volume significantly while ensuring safe handling of mixed waste streams.

- Additionally, rapid industrial growth increases hazardous and industrial waste generation. Many industries prefer incineration because it helps destroy toxic materials effectively. Incinerators offer a practical solution by reducing waste volume by up to 90%, helping cities manage waste within limited land footprints.

Energy recovery is another key driver. Modern incinerators can convert waste into usable heat and electricity. This helps countries balance waste management needs with energy demand. Overall, rising waste volumes and the need for safer disposal continue to drive the incinerator market forward.

Restraints

High Capital and Compliance Costs Restrain Market Expansion

One major restraint in the incinerator market is high initial investment. Setting up an incineration plant requires advanced equipment, emission control systems, and skilled operators. This makes projects costly, especially for developing regions with limited budgets.

- Strict environmental regulations also act as a challenge. Incinerators must meet tough air emission standards, which increases operating and maintenance costs. Delays in permits and public opposition can slow down project approvals. The European Commission reports that newer incinerators achieve energy recovery efficiencies above 70%, compared to less than 50% in older facilities.

In addition, alternative waste management methods such as recycling and composting are gaining attention. These options sometimes receive stronger public support, which can reduce new incinerator installations. Together, high costs and regulatory hurdles limit faster market growth.

Growth Factors

Expansion of Waste-to-Energy Projects Creates Growth Opportunities

Waste-to-energy projects offer strong growth opportunities for the incinerator market. Countries facing energy shortages are exploring incineration as a dual solution for waste disposal and power generation. This approach improves resource efficiency and reduces landfill dependence.

Developing economies are investing in modern waste management infrastructure. Urban development projects are creating demand for compact and efficient incinerators. Small and modular systems are especially attractive for hospitals, industries, and remote locations.

Public-private partnerships are also opening new doors for market players. Government support and long-term waste supply contracts help reduce commercial risks. These factors collectively create favorable opportunities for incinerator market expansion.

Regional Analysis

Asia Pacific Dominates the Incinerator Market with a Market Share of 47.9%, Valued at USD 8.0 billion

Asia Pacific leads the global incinerator market due to rapid urbanization, rising municipal solid waste volumes, and strong government focus on waste-to-energy projects. In 2024, the region accounted for a dominant 47.9% share, reaching a market value of USD 8.0 billion. Growing industrial activity and tightening environmental regulations continue to support long-term adoption.

North America shows steady growth driven by strict waste disposal regulations and increased focus on hazardous and biomedical waste treatment. Municipal authorities are upgrading aging waste infrastructure to meet emission standards. Waste-to-energy integration also supports market stability. Long-term investments in environmental protection initiatives sustain regional demand.

Europe remains a mature yet technology-driven market for incinerators, supported by strong circular economy policies. High landfill taxes encourage thermal waste treatment. The region emphasizes energy recovery and emission control technologies. Stable municipal waste generation ensures consistent equipment replacement and upgrades.

The U.S. incinerator market benefits from established waste management systems and consistent municipal waste output. Focus on emission compliance and energy recovery upgrades drives replacement demand. Public concerns over landfill capacity further support incineration usage. Regulatory oversight ensures steady technological modernization.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Alfatherm plays an important role in the global incinerator market by offering a wide range of systems for hazardous, biomedical, municipal, and industrial waste. In 2024, its strength lies in turnkey project execution and integrated pollution-control solutions, which help users meet stricter environmental rules while improving safe waste disposal efficiency across developing and urbanising regions.

Atlas Incinerators is strongly positioned in marine and offshore waste handling, supplying incinerators designed for ships, rigs, and ports. Its long operational history and focus on compact, reliable systems support consistent adoption as maritime regulations tighten. In 2024, the company will benefit from growing demand for onboard waste destruction and sludge management solutions.

Babcock and Wilcox stands out as a large-scale technology provider with deep expertise in waste-to-energy incineration systems. Its advanced combustion and heat-recovery technologies support municipalities seeking both waste reduction and power generation. In 2024, B&W remains well aligned with projects focused on efficiency, emissions control, and long-term infrastructure investments.

CHUWASTAR focuses primarily on medical and infectious waste incineration, serving hospitals, laboratories, and training institutions. Its emphasis on smokeless combustion and controlled temperature operation supports compliance with healthcare waste standards. In 2024, CHUWASTAR’s niche orientation provides steady growth as healthcare infrastructure expands and infection-control regulations become more rigorous globally.

Top Key Players in the Market

- Alfatherm

- Atlas Incinerators

- Babcock and Wilcox

- CHUWASTAR

- Dutch Incinerators

- ECO Concepts

- EEW Energy from Waste

- Haat Incinerator

- Incinco

- Inciner

Recent Developments

- In 2024, Alfatherm Ltd., an Indian manufacturer specializing in incinerators, shredders, and waste management solutions, has maintained a focus on sustainable waste processing technologies. The company continues to emphasize eco-friendly incineration systems compliant with global emission standards.

- In 2025, Atlas announced its leadership in providing containerized and SKID-mounted incinerators for major power plants and mining operators worldwide. These systems enable on-site waste reduction, reducing transport emissions and costs while complying with EU and U.S. EPA standards.

Report Scope

Report Features Description Market Value (2024) USD 16.9 billion Forecast Revenue (2034) USD 23.6 billion CAGR (2025-2034) 3.4% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Technology (Mass Burn Incineration, Modular Incineration, Fluidized Bed Incineration, Open Hearth Incineration), By Waste Type (Municipal Solid Waste, Hazardous Waste, Industrial Waste, Biomedical Waste), By Capacity (Small Scale – Up to 50 tons/day, Medium Scale – 51 to 200 tons/day, Large Scale – Over 200 tons/day), By Application (Waste-to-Energy, Energy Recovery, Volume Reduction, Environmental Protection) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Alfatherm, Atlas Incinerators, Babcock and Wilcox, CHUWASTAR, Dutch Incinerators, ECO Concepts, EEW Energy from Waste, Haat Incinerator, Incinco, Inciner Customization Scope Customisation for segments, region/country-level will be provided. Moreover, additional customisation can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Alfatherm

- Atlas Incinerators

- Babcock and Wilcox

- CHUWASTAR

- Dutch Incinerators

- ECO Concepts

- EEW Energy from Waste

- Haat Incinerator

- Incinco

- Inciner

Our Clients

- 168622

- December 2025