Global Hypersonic Flight Market Size, Share, Growth Analysis By Type (Hypersonic Aircraft [Military Jet, Commercial Plane], Hypersonic Spacecraft [Spaceplane, Airbreathing Hypersonic Vehicle, Hypersonic Testbed & Demonstrator]), By Component (Propulsion [Scramjet Engine, Ramjet Engine, Rocket Engine, Hybrid Engine], Aerostructure [Airframe Structure, Wing and Control Surface, Nose Cone and Leading Edge], Avionics [Flight Control System, Navigation System, Communication System], Others), By End Use (Military & Defense, Space Agencies, Commercial), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 183448

- Number of Pages: 270

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

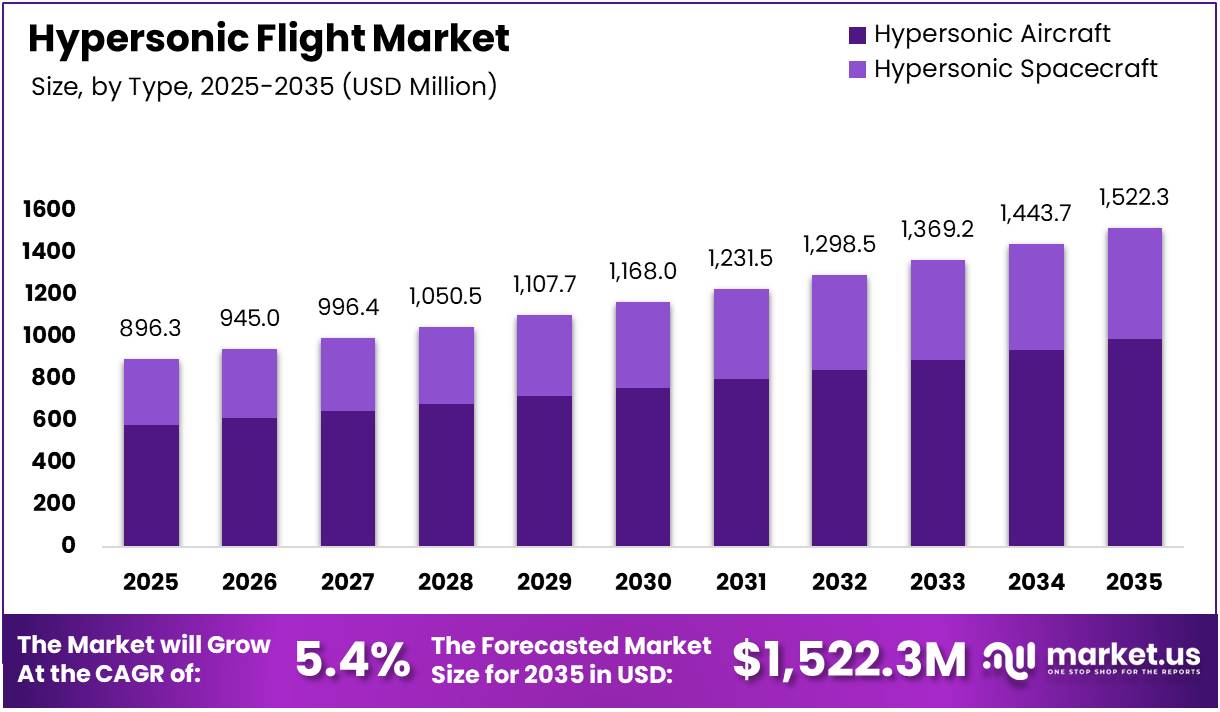

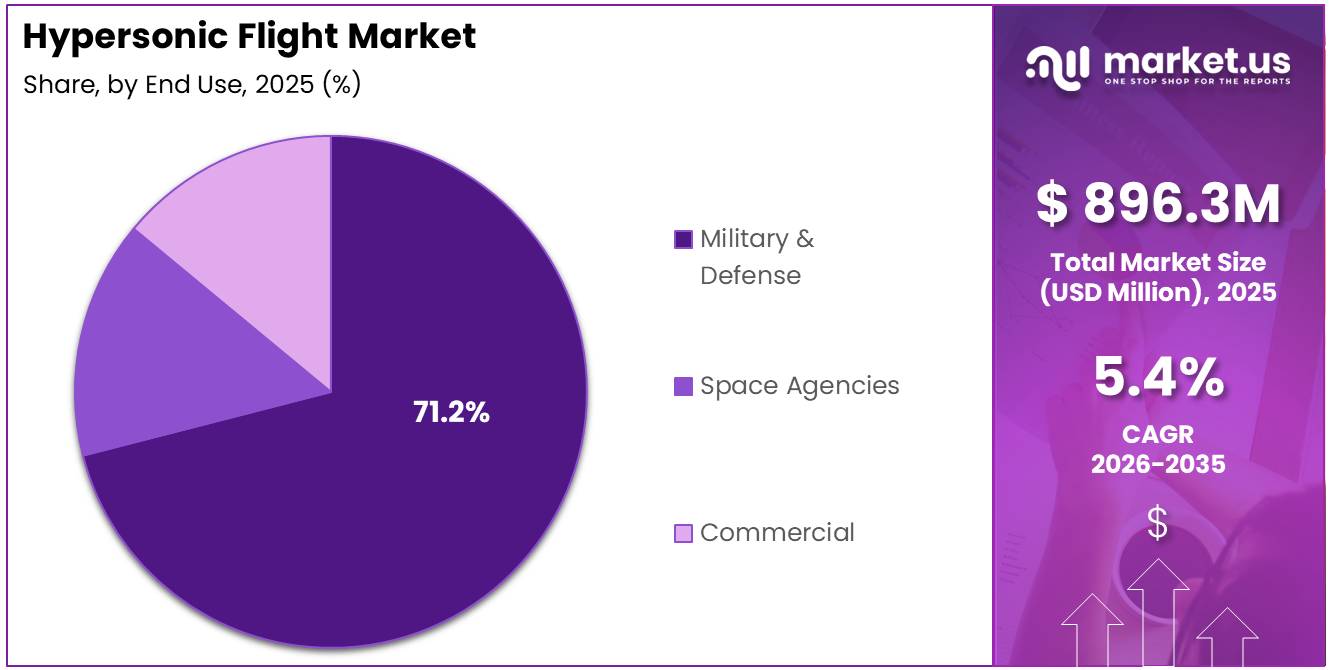

The Global Hypersonic Flight Market size is expected to be worth around USD 1,522.3 Million by 2035 from USD 896.3 Million in 2025, growing at a CAGR of 5.4% during the forecast period 2026 to 2035.

The hypersonic flight market encompasses vehicles and systems capable of traveling at speeds exceeding Mach 5, or roughly 6,174 km/h. These platforms include hypersonic aircraft, missiles, spaceplanes, and demonstrators. Moreover, they are designed for applications ranging from national defense to space access and, increasingly, commercial travel.

Hypersonic systems differ fundamentally from conventional aircraft in terms of propulsion, materials, and aerodynamics. They operate in extreme heat and pressure environments. Consequently, specialized components such as scramjet engines, advanced airframes, and high-temperature nose cones are essential to sustain stable flight at such velocities.

Defense programs have been the primary driver of hypersonic research globally. Nations are investing heavily to develop rapid-strike and precision-delivery systems. Additionally, space agencies are exploring reusable hypersonic platforms as cost-effective alternatives to traditional launch vehicles, creating a dual-use demand across the market.

Government funding continues to shape market direction significantly. Programs in the United States, China, Russia, and Europe are channeling billions into hypersonic test infrastructure and prototyping. Therefore, public investment acts as the foundation for both military procurement and civilian technology development in this segment.

Regulatory frameworks for hypersonic flight remain under development across most jurisdictions. Safety certification standards for hypersonic systems are not yet standardized. However, international bodies and national aviation authorities are beginning to address certification pathways, which will be critical for eventual commercial applications.

According to ResearchGate, advanced scramjet combustors achieved up to 93% combustion efficiency using hydrogen fuel optimization techniques, demonstrating significant progress in propulsion performance. Additionally, according to The Sun, reusable hypersonic vehicle tests conducted in 2025 achieved approximately 3,800 mph (6,115 km/h), confirming real-world Mach 5+ performance and validating the commercial and defense potential of modern hypersonic platforms.

Key Takeaways

- The global Hypersonic Flight Market was valued at USD 896.3 Million in 2025 and is projected to reach USD 1,522.3 Million by 2035.

- The market is growing at a CAGR of 5.4% during the forecast period 2026 to 2035.

- By Type, Hypersonic Aircraft leads with a dominant share of 63.7% in 2025.

- By Component, Propulsion holds the largest share at 43.1% in the market.

- By End Use, Military and Defense accounts for the highest share at 71.2%.

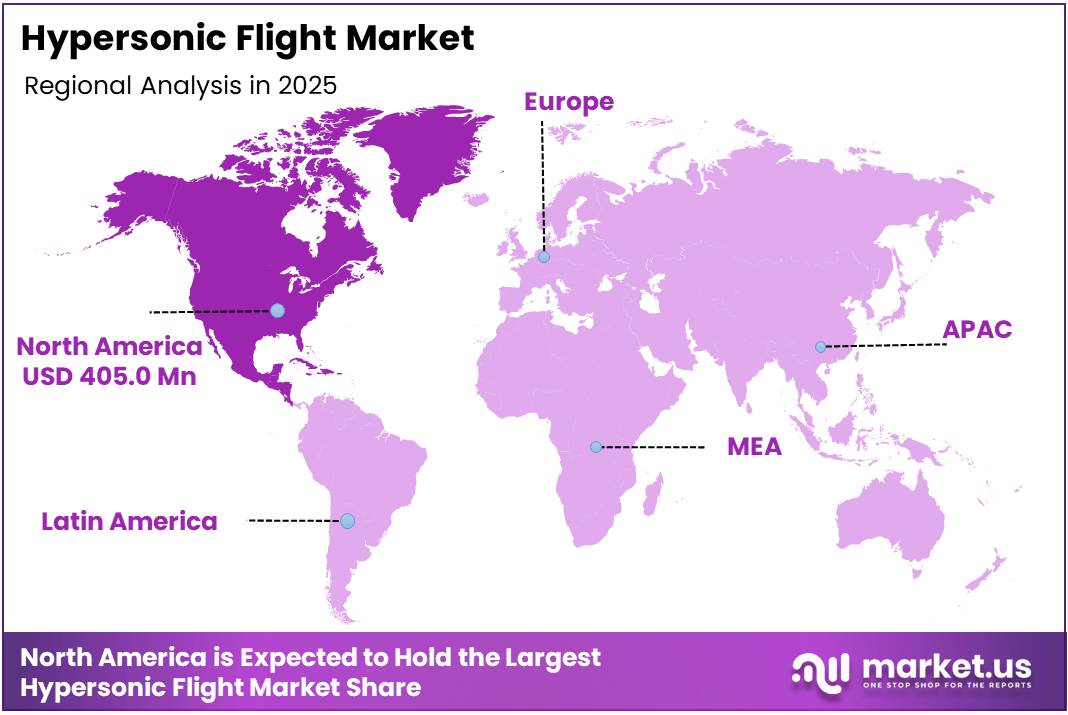

- North America dominates the regional landscape with a market share of 45.20%, valued at USD 405.0 Million in 2025.

By Type Analysis

Hypersonic Aircraft dominates with 63.7% due to strong military procurement and advanced defense program investments.

In 2025, Hypersonic Aircraft held a dominant market position in the By Type segment of the Hypersonic Flight Market, with a 63.7% share. This segment includes military jets and commercial planes. Moreover, sustained defense budgets and rapid prototype development programs have accelerated demand for high-speed aircraft across multiple nations globally.

Hypersonic Spacecraft represents a growing segment that includes spaceplanes and airbreathing hypersonic vehicles. Additionally, hypersonic testbed and demonstrator platforms are becoming critical tools for validating new flight concepts. Consequently, space agency investments and private launch companies are expanding this sub-segment significantly over the forecast period.

By Component Analysis

Propulsion dominates with 43.1% due to the critical role of scramjet and advanced engine systems in hypersonic flight.

In 2025, Propulsion held a dominant market position in the By Component segment of the Hypersonic Flight Market, with a 43.1% share. This sub-segment covers scramjet engines, ramjet engines, rocket engines, and hybrid engines. Moreover, propulsion innovation remains the single most important technical challenge and investment priority across all hypersonic programs worldwide.

Aerostructure is another essential component category covering airframe structure, wings and control surfaces, and nose cone and leading edge components. These elements must withstand extreme thermal and mechanical stress. Therefore, development of high-temperature composite materials is driving significant research and procurement activity within this sub-segment globally.

Avionics encompasses flight control systems, navigation systems, and communication systems critical for mission success. Additionally, the Others category includes supplementary systems that support hypersonic platform operations. Consequently, the integration of advanced sensors and AI-enabled autonomous guidance is becoming a key differentiator across hypersonic avionics development programs.

By End Use Analysis

Military and Defense dominates with 71.2% due to national security priorities and large-scale hypersonic weapons procurement programs.

In 2025, Military and Defense held a dominant market position in the By End Use segment of the Hypersonic Flight Market, with a 71.2% share. Defense agencies across major powers are funding hypersonic glide vehicles, cruise missiles, and boost-glide systems. Moreover, rapid strike and precision delivery requirements continue to be the primary demand drivers in this end-use category.

Space Agencies represent a significant and expanding end-use segment. Hypersonic platforms offer cost-effective pathways to low Earth orbit and beyond. Additionally, reusable hypersonic vehicles align with agency goals of reducing launch costs, making this sub-segment a key growth area over the forecast period through government and international collaboration programs.

Commercial end use remains in early development stages, driven by concepts for ultra-fast passenger travel and point-to-point cargo delivery. However, regulatory, safety, and cost barriers must be addressed before commercial routes become viable. Consequently, this segment is expected to grow gradually as demonstration programs mature and certification frameworks are established globally.

Key Market Segments

By Type

- Hypersonic Aircraft

- Military Jet

- Commercial Plane

- Hypersonic Spacecraft

- Spaceplane

- Airbreathing Hypersonic Vehicle

- Hypersonic Testbed & Demonstrator

By Component

- Propulsion

- Scramjet Engine

- Ramjet Engine

- Rocket Engine

- Hybrid Engine

- Aerostructure

- Airframe Structure

- Wing and Control Surface

- Nose Cone and Leading Edge

- Avionics

- Flight Control System

- Navigation System

- Communication System

- Others

By End Use

- Military & Defense

- Space Agencies

- Commercial

Drivers

Rising Strategic Defense Investments and Technological Advances Drive Hypersonic Flight Market Growth

Nations worldwide are increasing defense budgets to develop hypersonic weapons and rapid-strike capabilities. Military procurement programs in the US, China, and Europe are funding hypersonic glide vehicles and cruise missiles. Moreover, strategic competition among global powers is accelerating procurement timelines and increasing overall investment in this segment significantly.

Advancements in high-temperature materials and thermal protection systems are solving one of hypersonic flight’s biggest engineering challenges. New ceramic composites and ablative coatings now allow sustained flight at Mach 5 and above. Additionally, improved manufacturing techniques are reducing production costs, making these advanced materials more accessible across both defense and commercial development programs.

Government-supported research programs are expanding hypersonic test infrastructure globally. Agencies are building new wind tunnels, flight test ranges, and ground simulation facilities. Consequently, increased access to advanced testing infrastructure allows faster iteration of hypersonic designs, shortening development cycles and reducing the technical risk associated with bringing new hypersonic platforms to operational readiness.

Restraints

Extreme Technical Complexity and Regulatory Certification Challenges Limit Hypersonic Market Adoption

Sustaining stable flight at hypersonic speeds requires solving complex aerodynamic, thermal, and control challenges simultaneously. Minor instabilities at Mach 5 and above can result in catastrophic system failures. Moreover, the precision engineering required for hypersonic platforms significantly increases development costs, making it difficult for smaller manufacturers and emerging economies to participate effectively.

Developing reliable flight control systems for hypersonic vehicles remains a critical technical barrier. Real-time response requirements at these speeds exceed the capabilities of many existing avionics platforms. Additionally, communication blackouts caused by plasma formation around hypersonic vehicles during flight create significant operational challenges that engineers have yet to fully resolve across all program types.

Stringent regulatory and safety certification pathways for hypersonic systems are largely undefined in most countries. Aviation authorities lack established frameworks for certifying vehicles operating at these extreme speeds. Consequently, the absence of clear certification standards delays commercial development and adds substantial cost and uncertainty to programs seeking operational approval from civil aviation regulators worldwide.

Growth Factors

Hypersonic Passenger Travel, Space Access Integration, and Advanced Propulsion Development Accelerate Market Expansion

The concept of hypersonic passenger travel for long-haul routes is gaining commercial attention. Point-to-point travel times could be reduced from hours to minutes on major intercontinental routes. Moreover, early feasibility studies and prototype programs are attracting private investment, signaling growing confidence in the eventual commercial viability of high-speed passenger transport globally.

Hypersonic platforms are increasingly being evaluated for space access and reusable launch system applications. Their ability to reach near-orbital velocities makes them attractive as first-stage launch vehicles. Additionally, reusability significantly reduces per-mission costs, driving interest from both government space agencies and commercial launch operators seeking affordable and reliable orbital access solutions.

Development of advanced propulsion systems including scramjets and combined-cycle engines is a central growth enabler. These engines can operate efficiently across a wide speed range from subsonic to hypersonic. Consequently, combined-cycle propulsion reduces dependence on rocket engines for initial acceleration, improving fuel efficiency and expanding the operational flexibility of next-generation hypersonic platforms worldwide.

Emerging Trends

Rapid Prototyping, AI-Enabled Flight Control, and Miniaturization Reshape the Hypersonic Flight Market

Rapid prototyping and testing of hypersonic glide vehicles and cruise missiles is becoming a defining trend. Defense programs are moving from long development cycles to agile test-and-iterate models. Moreover, additive manufacturing and digital twin technologies are enabling faster design validation, reducing the time and cost required to bring hypersonic weapon systems to operational readiness globally.

Increasing focus on autonomous guidance and AI-enabled flight control systems is transforming hypersonic platform capabilities. AI allows real-time adaptation to aerodynamic changes at extreme speeds. Additionally, machine learning algorithms are being integrated into mission planning and target acquisition systems, enhancing the precision and autonomy of hypersonic platforms in both defense and research applications.

Miniaturization of hypersonic technologies is opening new doors for tactical and scalable applications. Smaller hypersonic vehicles can be launched from aircraft, ships, or ground platforms with reduced logistics requirements. Consequently, this trend is expanding the addressable market beyond major defense programs to include a wider range of tactical military applications and commercial technology demonstration missions globally.

Regional Analysis

North America Dominates the Hypersonic Flight Market with a Market Share of 45.20%, Valued at USD 405.0 Million

North America leads the global hypersonic flight market with a dominant share of 45.20%, valued at USD 405.0 Million in 2025. The United States drives this dominance through massive defense investments, major research programs, and collaboration between government agencies and leading aerospace contractors. Moreover, extensive test infrastructure and established manufacturing capabilities reinforce the region’s strategic position across all hypersonic platform categories.

Europe Hypersonic Flight Market Trends

Europe is steadily advancing its hypersonic capabilities through coordinated national and EU-level programs. Countries including the UK, France, and Germany are investing in high-speed propulsion and vehicle demonstration projects. Additionally, European defense agencies are partnering with private aerospace firms to develop next-generation hypersonic systems, driven by growing security concerns and the need to maintain technological parity globally.

Asia Pacific Hypersonic Flight Market Trends

Asia Pacific is the fastest-growing regional market for hypersonic flight. China is at the forefront with extensive military hypersonic glide vehicle programs, while India, Japan, and South Korea are expanding their own research and development efforts. Consequently, regional defense modernization priorities and space agency ambitions are together driving significant investment in hypersonic propulsion and airframe technologies across the region.

Middle East and Africa Hypersonic Flight Market Trends

The Middle East and Africa region represents an emerging and evolving market for hypersonic technologies. Gulf nations are increasing defense procurement budgets and exploring advanced military systems. Additionally, partnerships with North American and European defense contractors are introducing hypersonic system awareness to this region, laying a foundation for gradual market development over the forecast period.

Latin America Hypersonic Flight Market Trends

Latin America currently holds a limited but developing presence in the global hypersonic flight market. Brazil leads regional activity with its own aerospace research institutions and defense modernization programs. However, limited defense budgets and infrastructure constraints slow broader market participation. Consequently, technology transfer partnerships and bilateral defense agreements are expected to gradually shape this region’s future hypersonic capabilities.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Lockheed Martin Corporation is one of the most prominent players in the global hypersonic flight market. The company has long-standing expertise in advanced aerospace systems and continues to lead development of hypersonic strike vehicles under US defense contracts. Moreover, its Skunk Works division remains at the forefront of classified and semi-classified hypersonic research programs driving next-generation military capability.

L3Harris Technologies Inc. plays a significant role in the hypersonic market through its advanced electronics, sensor integration, and communication systems tailored for high-speed platforms. The company supports both government and defense prime contractors with critical avionics and mission system components. Additionally, its expertise in electronic warfare and signal processing adds strategic value to hypersonic flight programs requiring robust situational awareness capabilities.

Rolls-Royce brings deep propulsion engineering expertise to the hypersonic flight market, with growing investments in high-speed air-breathing engine technologies. The company is exploring advanced thermodynamic cycles suited for hypersonic cruise and access-to-space applications. Consequently, Rolls-Royce’s collaboration with defense and space agencies positions it as a key propulsion partner for next-generation European and international hypersonic platform development programs.

DLR (German Aerospace Center) serves as a leading research institution shaping hypersonic technology development across Europe. DLR conducts extensive wind tunnel testing, scramjet combustion research, and re-entry vehicle studies. Moreover, its partnerships with European space agencies and academic institutions provide an essential knowledge base that informs both military and civilian hypersonic system design and validation globally.

Key Players

- Lockheed Martin Corporation

- L3Harris Technologies Inc.

- Rolls-Royce

- DLR

- Rocket Lab USA

- Raytheon Technologies Corporation

- SpaceX

- The Boeing Company

- Leidos

- Blue Origin

- Northrop Grumman Corporation

- GE Group

- BAE Systems Plc

- Dassault Aviation

- Hermeus Corporation

Recent Developments

- March 2026 – Starfighters Space and Blackstar Orbital announced a strategic partnership to conduct hypersonic flight tests, aiming to validate next-generation high-speed vehicle technologies. This collaboration is expected to accelerate the development of reusable hypersonic test platforms and expand the private sector’s role in hypersonic research programs.

- March 2026 – Booz Allen was selected to support the US Air Force’s Arnold Engineering Development Complex (AEDC) Hypersonic Test Improvement Project under a contract valued at USD 82 Million. The project aims to upgrade hypersonic ground test facilities, enhancing the capacity to evaluate next-generation hypersonic vehicles and propulsion systems for defense applications.

Report Scope

Report Features Description Market Value (2025) USD 896.3 Million Forecast Revenue (2035) USD 1,522.3 Million CAGR (2026-2035) 5.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Hypersonic Aircraft (Military Jet, Commercial Plane), Hypersonic Spacecraft (Spaceplane, Airbreathing Hypersonic Vehicle, Hypersonic Testbed & Demonstrator)), By Component (Propulsion (Scramjet Engine, Ramjet Engine, Rocket Engine, Hybrid Engine), Aerostructure (Airframe Structure, Wing and Control Surface, Nose Cone and Leading Edge), Avionics (Flight Control System, Navigation System, Communication System), Others), By End Use (Military & Defense, Space Agencies, Commercial) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Lockheed Martin Corporation, L3Harris Technologies Inc., Rolls-Royce, DLR, Rocket Lab USA, Raytheon Technologies Corporation, SpaceX, The Boeing Company, Leidos, Blue Origin, Northrop Grumman Corporation, GE Group, BAE Systems Plc, Dassault Aviation, Hermeus Corporation Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Lockheed Martin Corporation

- L3Harris Technologies Inc.

- Rolls-Royce

- DLR

- Rocket Lab USA

- Raytheon Technologies Corporation

- SpaceX

- The Boeing Company

- Leidos

- Blue Origin

- Northrop Grumman Corporation

- GE Group

- BAE Systems Plc

- Dassault Aviation

- Hermeus Corporation

Our Clients

- 183448

- March 2026