Quick Navigation

Report Overview

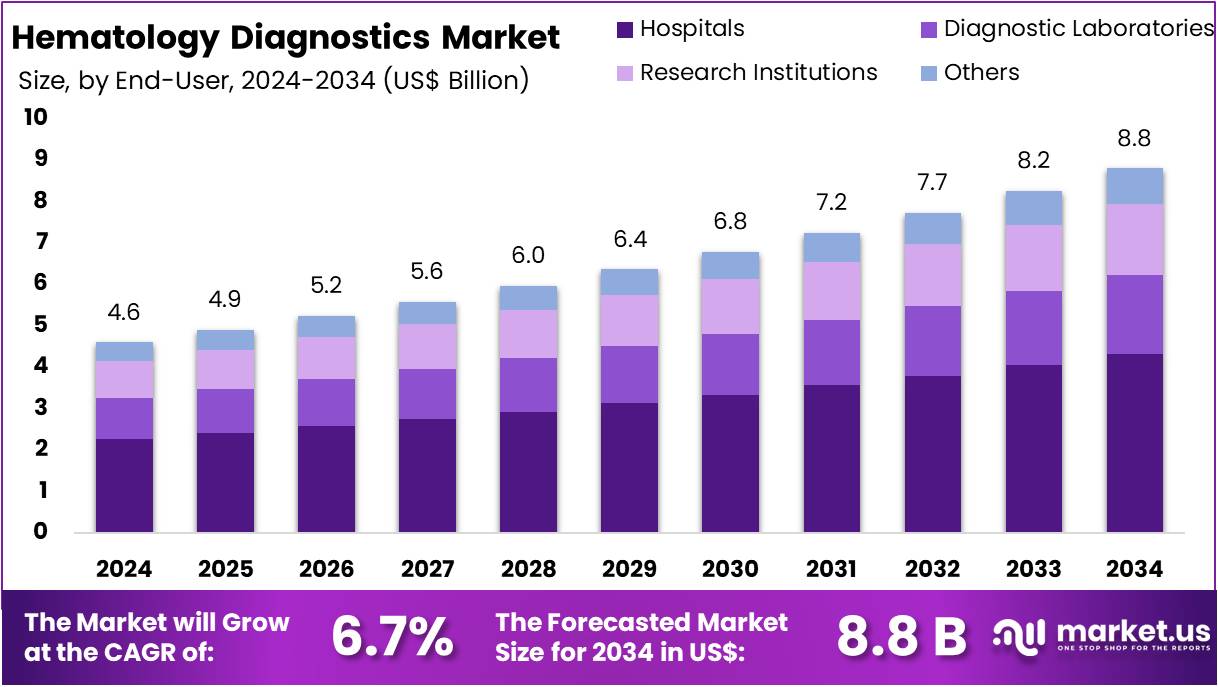

The Hematology Diagnostics Market is expected to reach a value of US$ 8.8 billion by 2034, up from US$ 4.6 billion in 2024, growing at a compound annual growth rate (CAGR) of 6.7% during the forecast period from 2025 to 2034.

This growth is primarily driven by the increasing demand for accurate and comprehensive diagnostic solutions, as well as the rising prevalence of chronic diseases, blood disorders, and lifestyle-induced health conditions. Blood tests, such as the complete blood count (CBC), play a critical role in diagnosing both hematological and non-hematological conditions.

The CBC test evaluates a range of hematological parameters, including white and red blood cell counts, platelet count, hematocrit, hemoglobin levels, differential white blood cell count, and several red blood cell indices. These tests are essential for detecting conditions like infections, anemia, blood cancers, and inflammatory diseases. The market has been further bolstered by the introduction of innovative technologies, with key players expanding their reach globally and integrating automation and artificial intelligence into hematology diagnostics. This integration not only enhances diagnostic accuracy but also streamlines workflows.

Additionally, the growing awareness around the importance of regular health screenings and preventive healthcare is contributing to the widespread adoption of hematology diagnostics. Technological advancements, including the rise of point-of-care testing devices, are opening up new opportunities to provide rapid and reliable diagnostics in underserved and remote areas. The increasing focus on personalized and precision diagnostics is further driving growth, particularly for conditions such as leukemia, anemia, and clotting disorders.

The role of digital health platforms and telemedicine is improving accessibility by enabling remote consultations and monitoring, which is crucial in expanding the reach of hematology diagnostics. Furthermore, the ongoing investments in healthcare infrastructure and diagnostic laboratories are accelerating the adoption of advanced hematology solutions.

Governments worldwide, such as India’s National Health Mission, are contributing to the market by implementing initiatives like the Free Drugs and Diagnostics Service to reduce the financial burden of essential tests. Furthermore, ongoing investments in healthcare infrastructure and research are fueling innovation and ensuring the global availability of cutting-edge diagnostic solutions.

- For example, Sysmex Corporation’s introduction of the Clinical Flow Cytometry System in Japan in May 2023 highlights the continued development of advanced diagnostic tools. As the emphasis on early detection and personalized healthcare increases, the hematology diagnostics market is poised for continued growth in the coming years.

Key Takeaways

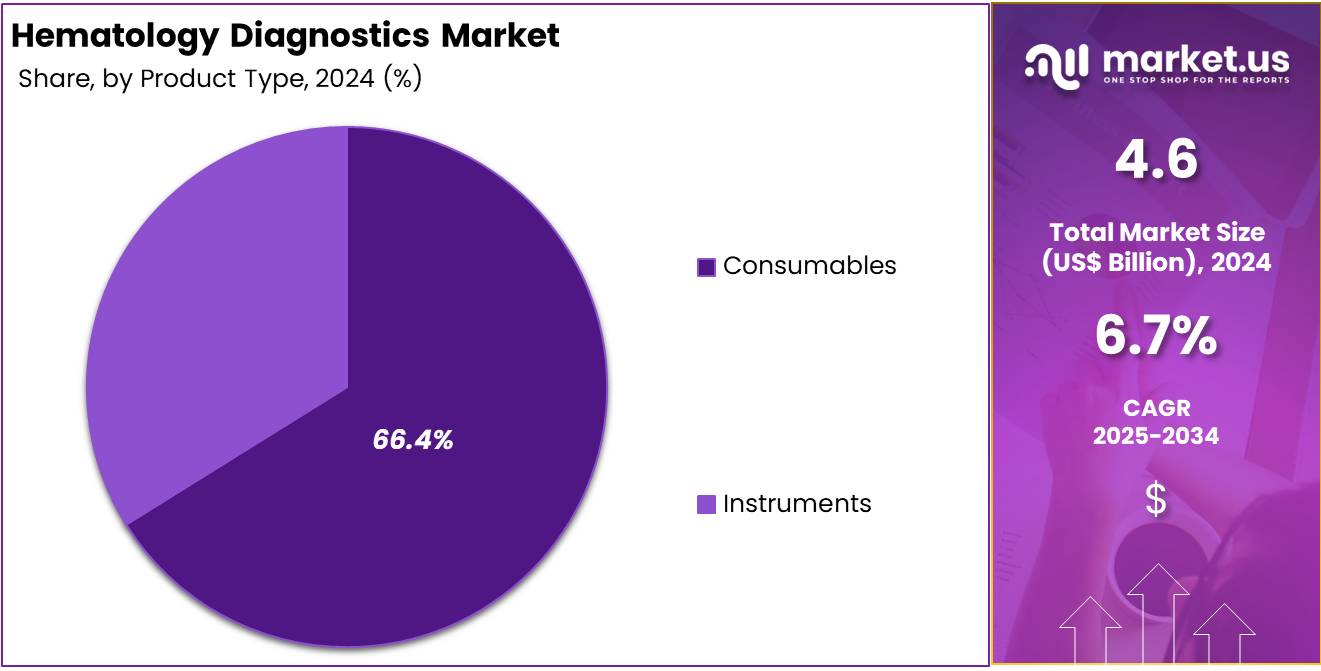

- In 2024, the market for Hematology Diagnostic generated a revenue of US$ 4.6 billion, with a CAGR of 6.7%, and is expected to reach US$ 8.8 billion by the year 2033.

- By product type segment is divided into instrument and consumables in which consumables taking the lead in 2024 with a market share of 66.4%.

- By test type is divided into complete blood count, hemoglobin testing, hematocrit testing, platelet function testing, coagulation testing. Among these, complete blood count held a significant share of 45.3%.

- By application the market is segregated into drug testing, auto immune disease, blood cancer, anemia, infectious disease, other applications, in which Blood cancer held the major share of 33.4% the market in 2024.

- By End User the market is segregated into hospital, diagnostic laboratory, research institution, others in which hospital held the major share of 41.4% the market in 2024.

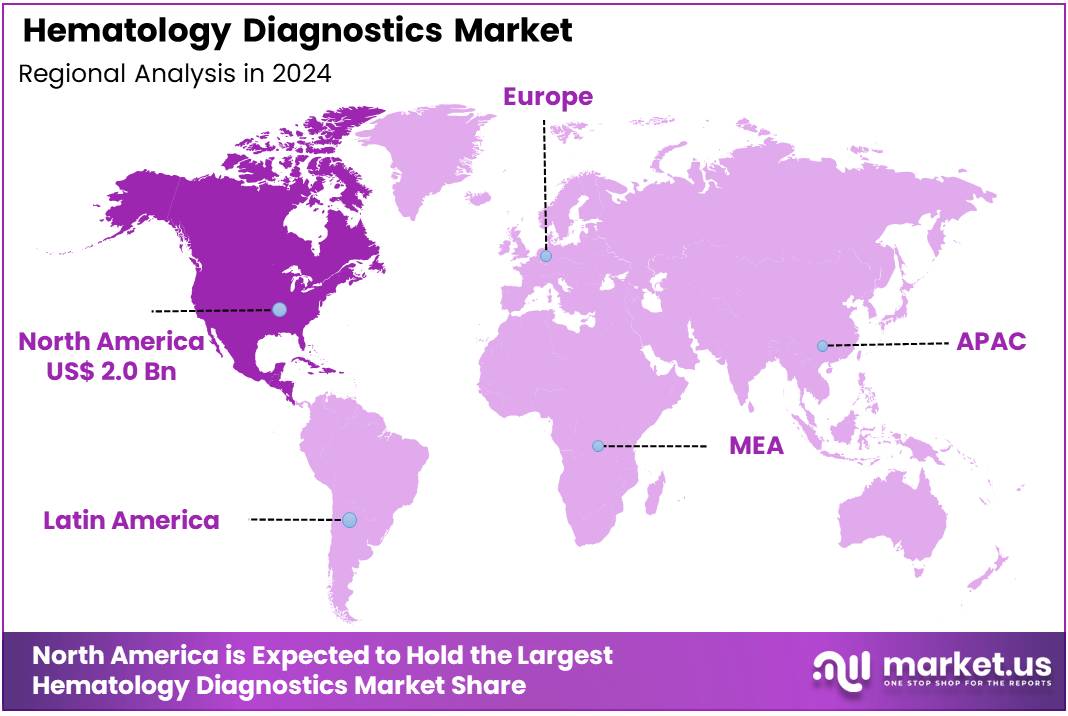

- North America led the market by securing a market share of 45.2% in 2024.

Product Type Analysis

In 2024, the Consumables Segment held a dominant market position in the Product Type Segment of Hematology Diagnostics Market, and captured more than a 58.8% share. The hematology diagnostics market is experiencing significant growth, driven by increasing demand for consumables and advancements in diagnostic technologies. The market is segmented into instruments and consumables, with consumables being the dominant and fastest-growing segment.

Consumables, including reagents, stains, controls, and test kits, are essential for routine testing and maintaining sample integrity in hematology diagnostics. They play a crucial role in ensuring accurate and precise results, particularly in tests like Complete Blood Count (CBC), coagulation studies, and molecular diagnostics. The rising prevalence of blood disorders, such as anemia, infections, and leukemia, is contributing to the growing need for diagnostic testing and the subsequent demand for consumables.

Consumables are integral to the proper functioning of automated analyzers and point-of-care (PoC) devices, providing specialized materials tailored for rapid, high-precision results. These consumables are also cost-effective, easy to use, and compatible with modern diagnostic workflows, which makes them indispensable in both clinical laboratories and point-of-care settings.

In addition to reagents and test kits, consumables include pipettes, vacutainer tubes, and quality control materials such as lancets and gloves, which prevent contamination and support the reliability of diagnostic processes. The increased focus on developing specialized consumables for high-throughput and precise testing, particularly in the context of automated systems, is further boosting market growth.

- For example, Sysmex Corporation launched its blood testing reagents for detecting Amyloid Beta (Aβ) accumulation, linked to Alzheimer’s disease in Europe in January 2024. The HISCL™ β-Amyloid 1-42 and 1-40 assay kits, which received CE-IVD marking on May 17, 2022, were previously introduced in Japan and the U.S. Sysmex aims to expand its immunochemistry testing business in Europe, including further developing the assay kits.. As diagnostic technology continues to advance, consumables will remain a vital and rapidly expanding segment in the hematology diagnostics market.

Test Type Analysis

In 2024, the Complete Blood Count Segment held a dominant market position in the Test Type Segment of Hematology Diagnostics Market, and captured more than a 45.3% share. CBC remains a crucial diagnostic tool in hematology, widely recognized for its ability to provide a comprehensive overview of blood health. This test evaluates key parameters such as red and white blood cell counts, hemoglobin concentration, hematocrit levels, and platelet counts, making it essential for diagnosing a wide range of health conditions.

By analyzing red blood cell indices, CBC is particularly valuable in determining the underlying cause of anemia, where an increase in red blood cells leads to elevated hemoglobin and hematocrit levels. Its versatility allows for the detection of both common issues like anemia and infections, as well as more serious diseases such as blood cancers and autoimmune disorders. One of the primary reasons for the CBC’s continued prominence is its role as a routine screening tool in general health assessments, enabling the early detection of irregularities, often before symptoms appear.

Furthermore, CBC is crucial for monitoring disease progression and assessing the effectiveness of treatments, including those for hematological conditions and cancer therapies. The test is widely used across various healthcare settings, from primary care centers to specialized oncology and hematology facilities. Its simplicity, cost-effectiveness, and accessibility, even in resource-limited environments, have contributed to its broad adoption.

Technological advancements, particularly in automated hematology analyzers, have enhanced the accuracy, speed, and consistency of CBC results, allowing for the detection of subtle changes in blood cell morphology and increasing the test’s diagnostic value.

- The rising prevalence of chronic illnesses and the aging global population have further driven the demand for routine blood testing. This is evident as over 1.5 billion CBC tests were performed globally in 2022, underscoring its vital role in medical diagnostics and its widespread use across healthcare systems worldwide.

Application Analysis

In 2024, the Blood cancer Segment held a dominant market position in the Application Segment of Hematology Diagnostics Market, and captured more than a 33.4% share.

The blood cancer segment is projected to witness the fastest growth within the hematology diagnostic market. This is mainly due to the complex nature and high prevalence of diseases like leukemia, lymphoma, and multiple myeloma. These conditions make up a significant share of hematological disorders. They demand frequent and specialized diagnostic testing to ensure accurate disease detection and monitoring. The need for early identification of abnormalities and timely treatment planning has further elevated the importance of this segment.

Advanced diagnostic tools play a critical role in blood cancer management. Techniques such as flow cytometry, polymerase chain reaction (PCR), next-generation sequencing, and cytogenetic analysis are commonly used. These methods help identify cellular and genetic abnormalities that are vital for diagnosis. Bone marrow analysis is also frequently required to provide detailed insights into disease progression. The regular use of such tools is essential for tracking treatment responses and detecting possible relapses.

In 2024, blood cancers are expected to contribute significantly to the overall cancer burden in the United States. New cases of leukemia, lymphoma, and myeloma are projected to make up 9.4% of the estimated 2,001,140 cancer diagnoses. This trend highlights the urgent need for reliable hematology diagnostics. Growing disease incidence and continuous advancements in diagnostic technologies will further drive market demand.

End User Analysis

In 2024, the hospital held a dominant market position in the End User Segment of Hematology Diagnostics Market, and captured more than a 41% share. Hospitals held a dominant position in hematology diagnostics, primarily because they serve as centralized centers equipped with advanced infrastructure and specialized expertise necessary for comprehensive diagnostic testing.

They offer access to cutting-edge technologies such as flow cytometry, molecular diagnostics, cytogenetics, and automated hematology analyzers, all essential for accurately diagnosing and monitoring complex hematological conditions like blood cancers, anemia, and bleeding disorders. Hospitals are home to multidisciplinary teams that include hematologists, oncologists, pathologists, and laboratory technicians who work together to provide precise diagnoses and tailored treatment plans.

This integrated approach ensures that patients receive comprehensive care, covering both diagnosis and treatment under one roof. Hospitals are also well-suited for high-volume testing, with the capacity to handle large numbers of patients and samples efficiently. Their ability to perform advanced diagnostic procedures, such as bone marrow biopsies and genetic testing, further reinforces their central role in hematology diagnostics.

Additionally, hospitals are equipped to handle emergencies, offering immediate care for patients with critical blood disorders, such as severe anemia or acute leukemia. Furthermore, hospitals often serve as research and training centers, contributing to innovations in hematology diagnostics and fostering ongoing advancements in the field. These factors collectively make hospitals the cornerstone of hematology diagnostic testing.

Key Market Segments

Product Type

- Instruments

- Hematology Analyzer

- Flow Cytometers

- Coagulation Analyzers

- Others

- Consumables

- Reagents

- Stains

- Controls

- Others

By Test Type

- Complete Blood Count (CBC)

- Hemoglobin Testing

- Hematocrit Testing

- Platelet Function Testing

- Coagulation Testing

By Application

- Drug Testing

- Auto-Immune Disease

- Blood Cancer

- Anemia

- Infectious Disease

- Other Applications

By End-User

- Hospitals

- Diagnostic Laboratories

- Research Institutions

- Others

Drivers

Increasing Prevalence of Blood Disorders

The increasing prevalence of blood disorders is a key driver for advancements in hematology diagnostics. Conditions such as anemia, blood cancers, clotting disorders, and inherited blood diseases are becoming more prevalent due to factors such as aging populations, lifestyle changes, environmental influences, and genetic predispositions. This growing burden has led to heightened demand for accurate, efficient, and innovative diagnostic tools.

Hematology diagnostics have evolved to address these challenges, incorporating advanced technologies like molecular testing, flow cytometry, and next-generation sequencing, which have significantly improved diagnostic accuracy, optimized workflows, and enhanced patient experiences. These advancements enable early detection, precise classification, and effective monitoring of blood disorders, ultimately improving patient outcomes.

The increasing need for personalized medicine and targeted therapies has further accelerated the development of sophisticated diagnostic techniques. The global impact of blood disorders underscores the importance of continued research, improved accessibility to diagnostic tools, and the integration of cutting-edge technologies in hematology diagnostics.

- For instance, approximately 1.7 million people in the US are living with or in remission from blood cancers such as leukemia, lymphoma, myeloma, myelodysplastic syndromes, or myeloproliferative neoplasms. Additionally, the National Library of Medicine reports that around 24.8% of individuals worldwide are affected by anemia, amounting to an estimated 1.62 billion people.

- The rising prevalence of chronic conditions, including cardiovascular diseases and diabetes, also plays a significant role in driving market growth. The World Health Organization highlights that hemoglobin disorders impact 75% of births worldwide, while anemia affects 12.7% of men globally. In 2024, blood cancers are projected to contribute to 9.4% of cancer-related deaths, with an estimated 611,720 fatalities, further emphasizing the growing need for effective diagnostic solutions.

Restraints

Rising Cost of Equipment

The rising cost of advanced equipment is a significant restraint in the field of hematology diagnostics, particularly for healthcare facilities in low-resource settings. Advanced analyzers, flow cytometers, and molecular diagnostic tools require substantial financial investment, and the ongoing costs of maintenance, calibration, and software upgrades further add to the financial burden. These technologies, while essential for accurate diagnostics, are often less accessible in developing regions due to their high acquisition costs and the financial strain on healthcare systems.

Additionally, a shortage of skilled professionals to operate and interpret results from such sophisticated equipment can lead to operational inefficiencies and underutilization of these tools. The cost of supplies, such as reagents, equipment, and consumables, also significantly influences the overall expense of diagnostic tests. Some tests require costly reagents or specialized equipment, further raising the price of diagnostics.

- For example, high-end hematology analyzers typically range in price from US$ 10,000 to USD 150,000, which presents a considerable financial challenge and limits the widespread adoption of these advanced tools, especially in regions with constrained healthcare budgets.

These financial and resource-related barriers underscore the need for cost-effective alternatives and innovative funding strategies to ensure broader access to hematology diagnostics and improve healthcare outcomes.

Opportunities

Increased Automation

Increased automation in hematology diagnostics presents significant opportunities for enhancing efficiency, precision, and workflow optimization. The integration of advanced robotics, artificial intelligence, and next-generation sequencing can drive greater accuracy and consistency in results, transforming the field of hematology diagnostics. Automated hematology analyzers offer substantial advantages, such as improved speed, precision, and operational efficiency, but they also present opportunities for further advancement, including reducing reliance on manual oversight and lowering operational costs.

Innovations in automation, combined with AI-driven algorithms, can analyze vast amounts of data, enabling faster and more precise predictions and diagnoses. This technological evolution also opens the door to expanding access to these diagnostic tools in resource-limited settings, making global diagnostic reach more achievable. The automation of processes like sample preparation, data acquisition, and analysis not only minimizes human error but also boosts throughput, allowing laboratories to process larger volumes of samples with consistent accuracy.

Intelligent algorithms facilitate rapid interpretation of data, aiding in the detection of cellular markers essential for diagnosing and monitoring blood disorders. This automation reduces turnaround times and ensures reproducibility, solidifying hematology diagnostics as a cornerstone of personalized medicine. As more diagnostic laboratories embrace automated systems to improve test accuracy, expedite results, and minimize administrative errors, the demand for automated hematology diagnostic solutions is expected to grow substantially.

- For instance, in January 2024, HORIBA Medical launched its HELO 2.0 high-throughput automated hematology platform in France, which is CE-IVDR certified and awaiting US FDA approval, further emphasizing the growing trend of automation in the field.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly influence the hematology diagnostics market, affecting both supply chains and demand dynamics. The recent imposition of a 145% tariff on Chinese goods by the United States has disrupted global trade, particularly impacting medical device manufacturers that rely on Chinese imports. These tariff-related disruptions have broader implications for the healthcare sector, potentially leading to increased costs and shortages of medical supplies.

The U.S. healthcare system, which heavily relies on imported medical devices, faces challenges as tariffs may increase costs and worsen shortages of pharmaceuticals and medical supplies. Furthermore, the European Union has announced countermeasures to protect European businesses and consumers from the impact of U.S. tariffs, including the reimposition of suspended 2018 and 2020 retaliatory tariffs and the imposition of a new, additional package of retaliatory measures.

These macroeconomic and geopolitical factors contribute to a volatile market environment, influencing the pricing, availability, and innovation within the hematology diagnostics sector. Companies operating in this space must navigate these challenges to maintain supply chain stability and meet the growing demand for diagnostic services.

Trends

Growing Popularity of Point-of-Care (PoC) Testing

The growing popularity of PoC testing in the hematology diagnostics market reflects a significant shift towards more accessible and efficient healthcare delivery. PoC testing enables healthcare professionals to conduct essential hematological tests directly at the patient’s location, whether in hospitals, clinics, or even at home. This shift is largely driven by the demand for rapid diagnosis, particularly in emergency situations or in areas with limited access to centralized laboratory services.

For example, devices that perform complete blood counts (CBC), a common hematology test, are now portable and compact, providing results within minutes. This rapid turnaround time is especially crucial in acute care settings where quick decision-making is vital for patient outcomes. An example of PoC testing’s impact is its role in managing chronic conditions such as anemia or blood clotting disorders. With the introduction of PoC devices capable of measuring hemoglobin levels or assessing coagulation profiles, patients can be monitored more frequently without the need for frequent visits to a diagnostic lab.

Additionally, these devices often require smaller blood samples, which makes the testing process more convenient and less invasive for patients. The increasing adoption of PoC testing is also seen in the adoption of portable and easy-to-use devices for rural or remote areas where access to sophisticated lab facilities is limited. In many developing regions, the ability to perform critical blood tests on-site reduces the need for patients to travel long distances, improving diagnostic access and treatment outcomes.

Furthermore, advances in connectivity and telemedicine are enhancing the role of PoC testing. Many PoC devices now integrate with cloud-based systems, allowing results to be instantly shared with healthcare professionals, even in remote locations. This integration facilitates quicker follow-ups, better disease management, and the ability to provide continuous care for conditions requiring ongoing monitoring, such as blood-related disorders.

The study titled “The Evaluation of a Point-of-Care Hematology Analyzer”, published in 2023 assessed the performance of the HemoScreen PoC hematology analyzer, comparing its results with those from standard laboratory analyzers. The findings indicated that HemoScreen provided reliable and accurate results, even for abnormal blood samples, suggesting its potential for effective PoC hematology diagnostics.

Regional Analysis

North America is leading the Market

North America leads the hematology diagnostics market, driven by a combination of factors that include a highly developed healthcare infrastructure, significant prevalence of blood-related disorders, and strong research and development investments. The region’s healthcare systems are well-equipped to support advanced diagnostic technologies, which is particularly important given the high incidence of conditions such as anemia, leukemia, and lymphoma.

This demand has spurred the adoption of sophisticated diagnostic tools, including automated hematology analyzers, flow cytometry, and next-generation sequencing. The U.S. is expected to maintain a dominant market share, with projections indicating it will lead the hematology diagnostics market by 2034.

- For example, acute myeloid leukemia (AML) is the most common form of acute leukemia in the U.S., accounting for 33% of all leukemia cases. According to data from the National Center for Health Statistics (NCHS), from August 2021 to August 2023, the prevalence of anemia among individuals aged 2 years and older was 9.3%. Given its aggressive progression, early and accurate diagnosis is critical.

Furthermore, government organizations like the Centers for Disease Control and Prevention (CDC) are actively supporting research, further enhancing North America’s leadership in hematology diagnostics. The region’s availability of skilled professionals, advanced healthcare systems, and continuous innovation in diagnostic technologies solidify its position as a leader in this market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The hematology diagnostics market is characterized by intense competition among several key players, including Abbott Laboratories, Siemens Healthineers, Sysmex Corporation, Beckman Coulter (a subsidiary of Danaher Corporation), F. Hoffmann-La Roche Ltd, Bio-Rad Laboratories, EKF Diagnostics, HORIBA Ltd., Mindray, and Boule Diagnostics.

These companies dominate the market by offering a wide range of hematology analyzers, reagents, and diagnostic solutions. They focus on technological advancements such as automation, artificial intelligence integration, and point-of-care testing to enhance diagnostic accuracy and efficiency.

The market is witnessing increased demand driven by the rising prevalence of blood disorders and the aging population. Additionally, regional players like Boule Diagnostics cater to smaller clinical laboratories with cost-effective solutions, while global giants like Siemens Healthineers and Roche lead in high-throughput diagnostics. Strategic initiatives such as mergers, acquisitions, and partnerships are common as companies strive to expand their product portfolios and market presence.

Top Key Players in the Hematology Diagnostic Market

- Abbott Laboratories

- Sysmex Co.

- Beckman Coulter

- Horiba, Ltd.

- Boule Diagnostics AB

- EKF Diagnostics

- Bio-Rad Laboratories

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- Siemens Healthineers AG

- Hoffmann-La Roche Ltd

- NIHON KOHDEN CORPORATION

- Ortho Clinical Diagnostics

- Diatron

Recent Developments

- In March 2025, Sysmex America, Inc., a prominent provider of diagnostic solutions specializing in hematology, hemostasis, urinalysis, flow cytometry, and informatics, announced the expansion of its 3-part differential automated hematology analyzer line with the introduction of the XQ-320™. This new model offers reliable and precise CBC testing.

- In September 2024, Beckman Coulter and Scopio Labs, a medtech company known for its digital cell morphology workflow solutions, announced the expansion of their long-term partnership to include a global distribution agreement for Scopio’s Full-Field Bone Marrow Aspirate™ (FF-BMA) Application. The Scopio X100 / X100HT with the FF-BMA Application is CE-Marked. Bone marrow aspirate analysis is a crucial procedure that delivers key insights for evaluating a range of hematologic disorders.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 4.6 Bn |

| Forecast Revenue (2034) | US$ 8.8 Bn |

| CAGR (2025-2034) | 6.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Instrument- Hematology Analyzer, Flow Cytometer, Coagulation Analyzer, Others; Consumables- Reagent, Stains, Control, Others), By Test Type (Complete Blood Count, Hemoglobin Testing, Hematocrit Testing, Platelate Function Testing, Coagulation Testing), By Application (Blood Cancer, Drug Testing, Auto-Immune Disease, Anemia, Infectious Disease, Others), By End-User (Hospitals, Diagnostic Laboratory, Research Institutions, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Abbott Laboratories, Sysmex Co., Beckman Coulter, Horiba, Ltd., Boule Diagnostics AB, EKF Diagnostics, Bio-Rad Laboratories, Shenzhen Mindray Bio-Medical Electronics Co., Ltd., Siemens Healthineers AG, F. Hoffmann-La Roche Ltd, NIHON KOHDEN CORPORATION, Ortho Clinical Diagnostics, Diatron |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |