Quick Navigation

Report Overview

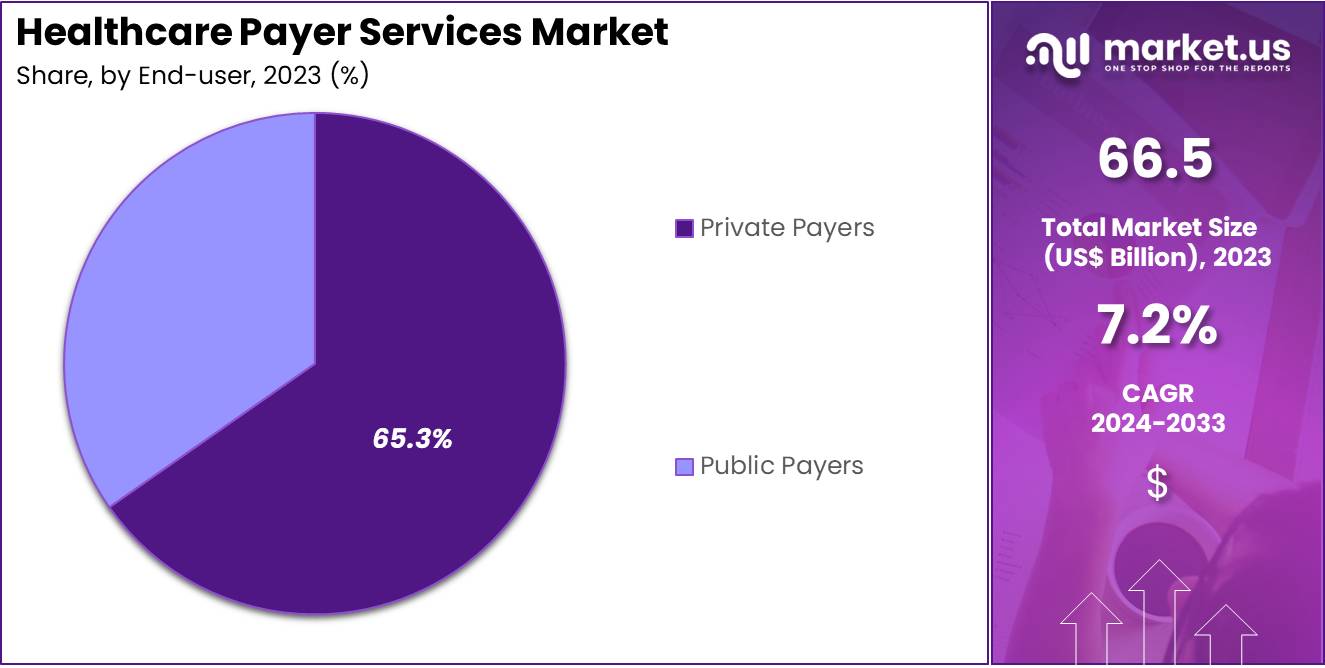

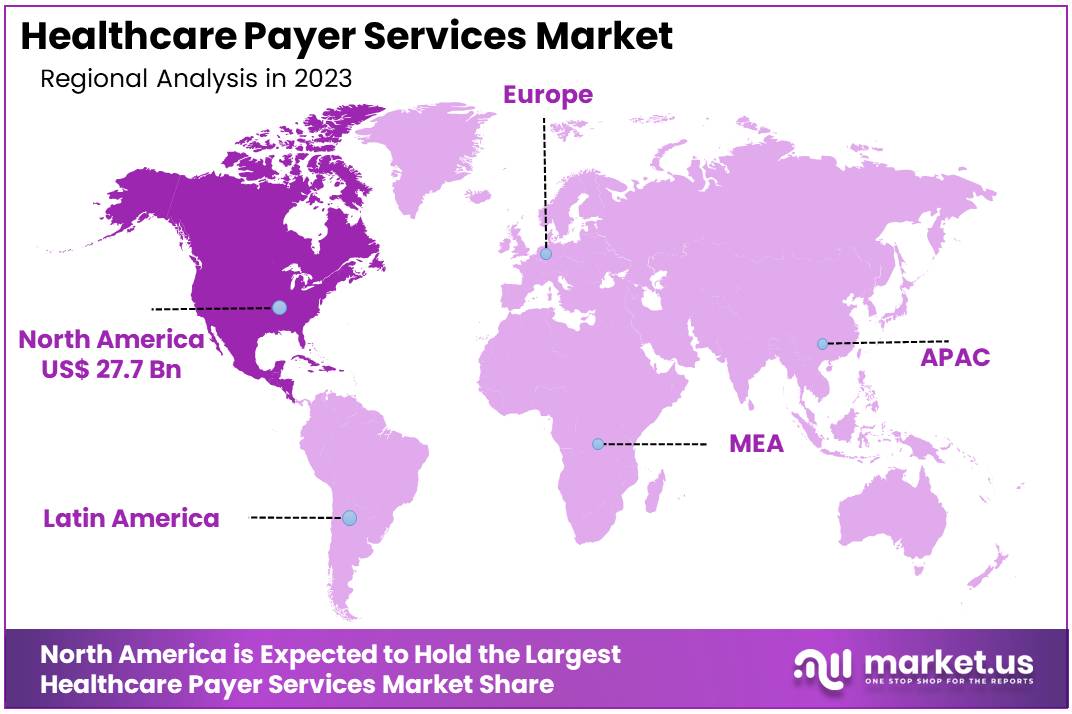

The Global Healthcare Payer Services Market size is expected to be worth around US$ 133.3 Billion by 2033, from US$ 66.5 Billion in 2023, growing at a CAGR of 7.2% during the forecast period from 2024 to 2033. North America held a dominant market position, capturing more than a 41.7% share and holds US$ 27.7 Billion market value for the year.

Increasing pressure on healthcare systems to improve efficiency, reduce costs, and enhance customer satisfaction is driving the growth of the healthcare payer services market. Healthcare payer services encompass a wide range of functions, including claims management, billing, fraud detection, customer service, and network management, which are essential for the effective operation of health insurance plans.

The rising complexity of healthcare delivery models, including value-based care and telemedicine, has created a demand for more advanced payer solutions that can address these evolving needs. In December 2022, Ernst & Young LLP (EY US) and EXL, a leading provider of data analytics and digital operations solutions, entered into a strategic partnership to accelerate digital transformation within the healthcare sector. This collaboration highlights the growing role of digital technologies and data analytics in streamlining payer operations and improving decision-making.

Additionally, the increasing reliance on digital systems for managing medical records, as noted in a 2022 survey by the Organization for Economic Co-operation and Development (OECD), has raised concerns about data security, further emphasizing the need for secure and compliant payer solutions. Opportunities for growth in the healthcare payer services market also stem from the rising demand for personalized health plans, real-time claims processing, and predictive analytics to reduce fraud and administrative costs.

Moreover, advancements in artificial intelligence (AI) and machine learning (ML) are transforming claims automation, enhancing fraud detection, and improving customer support through chatbots and virtual assistants. As healthcare payers face increasing regulatory pressures and the need to adopt more flexible, technology-driven systems, the market for payer services continues to evolve, offering significant opportunities for innovation and efficiency gains.

Key Takeaways

- In 2023, the market for healthcare payer services generated a revenue of US$ 66.5 billion, with a CAGR of 7.2%, and is expected to reach US$ 133.3 Billion by the year 2033.

- The service segment is divided into information technology outsourcing, business process outsourcing, and knowledge process outsourcing, with information technology outsourcing taking the lead in 2023 with a market share of 48.7%.

- Considering application, the market is divided into integrated front office service & back office operations, claims management services, member management services, billing & accounts management services, provider management services, analytics & fraud management services, payment management services, hr services, and audit & analysis systems. Among these, claims management services held a significant share of 29.4%.

- Furthermore, concerning the end-user segment, the market is segregated into private payers and public payers. The private payers sector stands out as the dominant player, holding the largest revenue share of 65.3% in the healthcare payer services market.

- North America led the market by securing a market share of 41.7% in 2023.

Service Analysis

The information technology outsourcing segment led in 2023, claiming a market share of 48.7% as healthcare organizations increasingly turn to external service providers for their IT needs. The rising demand for digital transformation, including electronic health records (EHR), telemedicine, and cloud-based solutions, is anticipated to drive this growth.

Outsourcing IT functions allows healthcare payers to focus on core business activities while accessing cutting-edge technologies and expertise at lower costs. Furthermore, the complexity of healthcare regulations and the need for compliance with HIPAA and other standards are likely to make ITO services even more essential. The ongoing shift toward automation, data analytics, and artificial intelligence (AI) in healthcare further fuels the demand for IT outsourcing in payer services.

Application Analysis

The claims management services held a significant share of 29.4% due to the increasing complexity of claims processing and the need for efficiency. Healthcare payers are expected to adopt advanced claims management services to streamline claims adjudication, reduce errors, and accelerate reimbursement cycles.

With rising healthcare costs and an increasing volume of claims, payers require integrated solutions that improve operational efficiency and reduce administrative costs. Additionally, the growing adoption of digital tools, AI-driven analytics, and automation technologies is likely to enhance the accuracy and speed of claims management, driving further adoption across the sector. As the need for cost-effective and scalable solutions grows, the claims management services segment is expected to continue its expansion.

End-user Analysis

The private payers segment had a tremendous growth rate, with a revenue share of 65.3% as private health insurance providers seek innovative ways to enhance service offerings and optimize operational efficiency. The increasing number of privately insured individuals, combined with the rising demand for tailored healthcare plans, is expected to contribute to the growth of this segment. Private payers are also likely to invest in digital transformation and automation technologies to streamline operations and improve customer service.

Additionally, the growing prevalence of value-based care models, in which insurers focus on improving patient outcomes while managing costs, is expected to further drive investment in healthcare payer services. As healthcare costs rise and consumer expectations increase, private payers are projected to continue leveraging outsourcing solutions to meet these demands and improve their competitive position in the market.

Key Market Segments

By Service

- Information Technology Outsourcing

- Business Process Outsourcing

- Knowledge Process Outsourcing

By Application

- Integrated Front Office Service & Back Office Operations

- Claims Management Services

- Member Management Services

- Billing & Accounts Management Services

- Provider Management Services

- Analytics & Fraud Management Services

- Payment Management Services

- HR Services

- Audit & Analysis Systems

By End-user

- Private Payers

- Public Payers

Drivers

Increasing Innovations In Healthcare Payer Services

The increasing innovation in healthcare technology significantly drives the growth of the healthcare payer services market. New advancements in data management and reporting systems have enabled payers to streamline operations, enhance service offerings, and improve customer experiences. In March 2022, IMAT Solutions launched an innovative solution aimed at enhancing real-time healthcare data management and reporting.

This solution, which targets healthcare payers, state agencies, and Health Information Exchanges, offers advanced features in data collection, aggregation, and distribution. It also earned the Data Aggregator Validation recognition from the NCQA, underscoring the company’s commitment to high standards of compliance and quality in healthcare data management.

As payers increasingly adopt advanced technology to handle large volumes of healthcare data, the demand for efficient, secure, and scalable solutions is expected to rise. The continuous evolution of data analytics, machine learning, and artificial intelligence will likely further enhance healthcare payer services by enabling more personalized care, improving cost efficiency, and optimizing decision-making processes.

Restraints

Data Privacy and Security Concerns

Increasing concerns over data privacy and security significantly restrain the growth of the healthcare payer services market. Healthcare payers handle vast amounts of sensitive personal and medical information, which makes them prime targets for cyberattacks and data breaches. High-profile data breaches in the healthcare sector have raised alarms over the potential for unauthorized access to personal health data.

Strict regulations, such as the Health Insurance Portability and Accountability Act (HIPAA) in the U.S., impose significant compliance requirements on healthcare payers, creating a complex regulatory environment. These privacy and security concerns hinder the ability of healthcare payer service providers to innovate freely, as they must prioritize cybersecurity measures and compliance.

The need to implement robust data protection protocols increases operational costs, which may further slow market growth. As data privacy regulations continue to tighten and cyber threats evolve, healthcare payers are expected to face heightened pressure to invest in secure infrastructure, which could impact their overall service delivery and profitability.

Opportunities

Rising Need for Personal Health Data Collection

The rising need for personal health data collection presents a significant opportunity for the healthcare payer services market. Increasingly, both patients and healthcare providers recognize the value of comprehensive health data in improving patient outcomes and optimizing healthcare delivery. In 2021, a survey conducted by the U.S. Department of Health and Human Services found that over 70% of respondents felt they had lost control over the collection and use of their personal health data.

This growing concern about personal data ownership has prompted calls for better data collection practices and greater transparency in the healthcare system. As a result, healthcare payers are expected to focus more on empowering individuals to track and control their health data while ensuring privacy and security.

The rise in wearable health devices, health apps, and electronic health records (EHRs is expected to further drive the demand for more sophisticated data management solutions. By leveraging these innovations, healthcare payers will be able to offer more personalized insurance plans, preventative care programs, and tailored health interventions, thus enhancing customer satisfaction and improving health outcomes.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly impact the healthcare payer services market by influencing both demand and regulatory environments. Economic downturns can lead to increased pressure on healthcare budgets, prompting cost-cutting measures that affect payer service models.

Conversely, periods of economic growth tend to support increased health insurance coverage and expansion of payer services, as individuals and businesses are more willing to invest in comprehensive health plans. Geopolitical instability, such as trade tensions or changes in healthcare regulations, can also create challenges for payer organizations, particularly in international markets.

However, governments’ ongoing efforts to reform healthcare systems and improve access to services create opportunities for payer organizations to innovate and expand. As global economies stabilize and healthcare reforms continue, the payer services market is poised for steady growth, particularly as new solutions emerge to manage costs and improve efficiency.

Trends

Growing Digital Transformation Driving the Healthcare Payer Services Market

The growing digital transformation is driving significant growth in the healthcare payer services market as organizations adopt new technologies to streamline operations and enhance service delivery. Increasing reliance on digital platforms allows payers to improve claims management, enhance customer service, and reduce administrative costs.

High adoption of automation, artificial intelligence, and data analytics in payer services will likely improve decision-making processes and enable more personalized offerings. In March 2022, the introduction of a Contract Lifecycle Management tool aimed at aiding healthcare providers with their digital transformation efforts signaled a shift toward more efficient management of complex contracts, including payer agreements.

These innovations are expected to optimize payer operations, reduce friction, and increase customer satisfaction, further propelling the growth of digital healthcare solutions. As these technologies continue to evolve, they are projected to play a pivotal role in shaping the future of payer services.

Regional Analysis

North America is leading the Healthcare Payer Services Market

North America dominated the market with the highest revenue share of 41.7% owing to several key factors including increased demand for healthcare coverage, evolving regulatory requirements, and the ongoing expansion of both private and government insurance programs. According to a report by the Congressional Research Service, most Americans are covered by private health insurance or government programs such as Medicare and Medicaid, which has significantly influenced the payer services market.

With the aging population and rising healthcare costs, the demand for efficient payer services has surged, prompting insurance providers to invest in advanced technologies and digital solutions to streamline claims processing, enhance customer service, and improve operational efficiency. The expansion of government health programs, particularly Medicaid and Medicare, has also contributed to market growth, as more individuals gain access to insurance, creating a larger pool of beneficiaries.

Additionally, the continued shift towards value-based care models has driven payer organizations to adopt new technologies that support data-driven decision-making and personalized healthcare. This trend is expected to persist, further fueling the demand for innovative payer services that can meet the needs of both consumers and healthcare providers.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

The Asia Pacific region is poised for the fastest growth in the healthcare payer services market, primarily due to increased healthcare spending, a burgeoning middle class, and heightened demand for quality healthcare. Nations like India, China, and Japan are expected to boost investments in health insurance, both publicly and privately. This surge is spurred by a growing awareness of the necessity for comprehensive health coverage among their populations.

Rapid urbanization and an aging demographic are intensifying the need for effective healthcare payer services. These services are crucial for managing insurance plans, processing claims, and providing customer support efficiently. The dynamics of urban growth and demographic shifts are prompting a greater reliance on sophisticated healthcare management solutions in the region.

In a significant development, Tata Consultancy Services (TCS) was named a Leader in the Market in Horizons for Healthcare Payer Service Providers in April 2023. TCS leverages cutting-edge technology and deep sector knowledge to help streamline operations for healthcare payers. With an increasing focus on digital solutions, automation, and advanced analytics, the healthcare payer services market in Asia Pacific is set to expand considerably, driven by both governmental and private sector initiatives.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The major players in the healthcare payer services market are actively engaged in the development and introduction of innovative products, as well as implementing strategic initiatives aimed at enhancing their competitive positioning. Key players in the healthcare payer services market focus on strategies such as digital transformation, cost optimization, and enhancing customer experience to foster growth.

Companies invest in advanced data analytics and artificial intelligence to streamline claims processing, improve fraud detection, and personalize healthcare plans for clients. They also form strategic partnerships with healthcare providers, technology firms, and insurance companies to expand service offerings and increase market penetration. By improving operational efficiency through automation and integrating telehealth services, players aim to reduce costs and improve care delivery. Additionally, many players are increasing focus on regulatory compliance to meet the evolving needs of the healthcare landscape.

One of the key players in the market is Anthem, Inc., a leading health insurance provider. Anthem’s growth strategy centers on expanding its payer services portfolio, which includes offering a wide range of health plans, as well as administrative and claims management services to employers, government programs, and individual consumers. The company invests heavily in technology to improve its service delivery and customer experience, integrating digital tools such as mobile apps and AI-based chatbots. Anthem also emphasizes strategic acquisitions and partnerships to diversify its offerings and strengthen its position in the healthcare market.

Top Key Players in the Healthcare Payer Services Market

- Accenture

- Cognizant

- Concentric Corporation

- EXL

- Genpact

- HCL Technologies

- WIPRO Ltd.

- Xerox Corporation

Industrial Advantages and Opportunities For Market Players

The Healthcare Payer Services market research report provides key industry players with invaluable data for strategic planning. It includes comprehensive information on market trends, forecasts, and areas of growth. This allows companies to align their resources effectively and capitalize on emerging opportunities. Such detailed insights facilitate better strategic decision-making and resource allocation.

Insights into competitor strategies and customer preferences are also pivotal. These details help companies tailor their marketing strategies and service offerings to meet specific demands. Furthermore, understanding the strengths and weaknesses of competitors allows businesses to position themselves more effectively within the market.

Risk management and regulatory compliance are critical aspects covered in the report. It highlights potential market risks and regulatory changes, enabling companies to develop robust contingency plans. Additionally, staying updated on compliance requirements helps maintain credibility and avoid penalties, enhancing operational resilience and market standing.

Lastly, the report supports financial planning and identifies potential partnerships. It provides a clear analysis of market dynamics and their financial implications, aiding in precise budgeting and investment decisions. Identifying potential partners and collaboration opportunities also helps expand market reach and enhance service offerings, driving business growth and innovation.

Recent Developments

- In September 2023: Genpact expanded its partnership with Amazon Web Services (AWS) to enhance financial crime risk management using generative AI and large language models. This expansion is expected to provide a significant competitive advantage, enabling Genpact to stay ahead of rivals in the market.

- In April 2023, Cognizant, a leading IT services provider, announced the extension of its long-standing partnership with Microsoft in the healthcare sector. This extended collaboration will enable healthcare payers and providers to gain quick access to cutting-edge technological solutions, streamline claims processing, and improve interoperability, all aimed at optimizing business operations and enhancing patient and member experiences.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 66.5 billion |

| Forecast Revenue (2033) | US$ 133.3illion |

| CAGR (2024-2033) | 7.2% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Service (Information Technology Outsourcing, Business Process Outsourcing, and Knowledge Process Outsourcing), By Application (Integrated Front Office Service & Back Office Operations, Claims Management Services, Member Management Services, Billing & Accounts Management Services, Provider Management Services, Analytics & Fraud Management Services, Payment Management Services, HR Services, and Audit & Analysis Systems), By End-user (Private Payers and Public Payers) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Accenture, Cognizant, Concentric Corporation, EXL, Genpact, HCL Technologies, WIPRO Ltd., and Xerox Corporation. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |