Quick Navigation

Report Overview

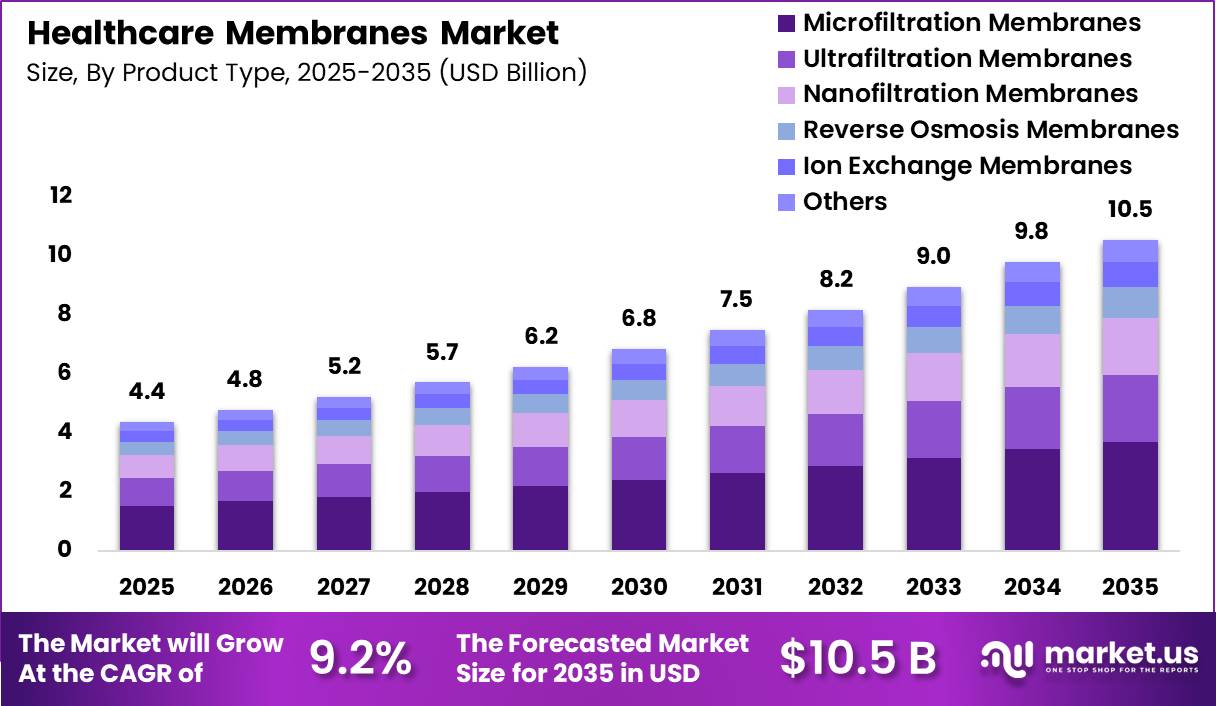

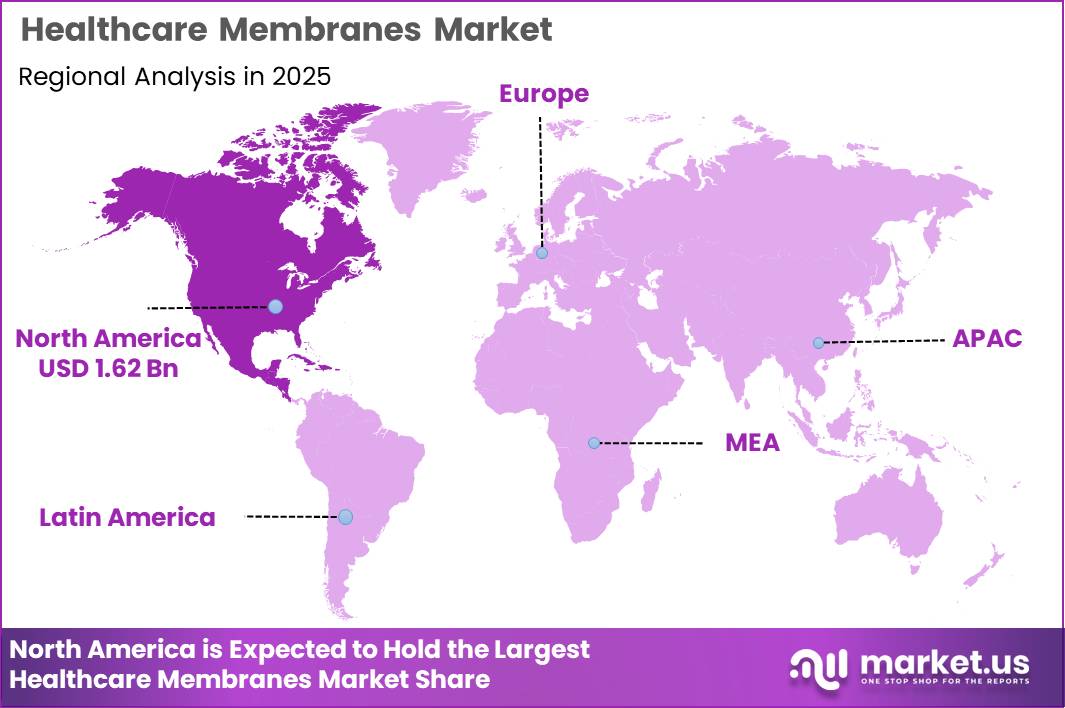

Global Healthcare Membranes Market size is expected to be worth around US$ 10.5 Billion by 2035 from US$ 4.4 Billion in 2025, growing at a CAGR of 9.2% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 39.51% share with a revenue of US$ 1.62 Billion.

The healthcare membrane market refers to the use of semi-permeable materials designed for selective separation, filtration, and purification in medical and pharmaceutical applications.

These membranes act as critical barriers that allow the passage of specific molecules while blocking contaminants such as bacteria, viruses, and toxins. They are widely used in processes such as hemodialysis, drug delivery, sterile filtration, and biopharmaceutical production.

From a technical perspective, healthcare membranes are engineered using materials such as polysulfone, polyethersulfone, polytetrafluoroethylene, and polyvinylidene fluoride. These materials are selected for their biocompatibility, chemical resistance, and precise pore structure, which ensures high selectivity and efficiency in medical applications. Filtration technologies commonly applied include microfiltration, ultrafiltration, nanofiltration, and reverse osmosis, each designed to target specific particle sizes and contaminants.

The demand for healthcare membranes is closely associated with the increasing burden of chronic diseases and the expansion of advanced medical treatments. For instance, dialysis procedures one of the primary applications are growing due to the rising prevalence of kidney disorders globally.

According to global health estimates, millions of patients rely on renal replacement therapies, which directly increases the utilization of membrane-based filtration systems. Additionally, membranes are essential in ensuring sterility in injectable drugs and vaccines, supporting stringent regulatory requirements in pharmaceutical manufacturing.

Overall, the healthcare membrane market is characterized by its essential role in ensuring patient safety, product purity, and regulatory compliance. Growth is primarily driven by increasing healthcare expenditure, technological advancements in filtration systems, and expanding applications in biologics and precision medicine.

Key Takeaways

- Market Size: Globalo Healthcare Membranes Market size is expected to be worth around US$ 10.5 Billion by 2035 from US$ 4.4 Billion in 2025.

- Market Share: The market growing at a CAGR of 9.2% during the forecast period from 2026 to 2035.

- Product Type Analysis: Microfiltration membranes are projected to dominate the segment, accounting for approximately 35.2% of the total market share in 2025.

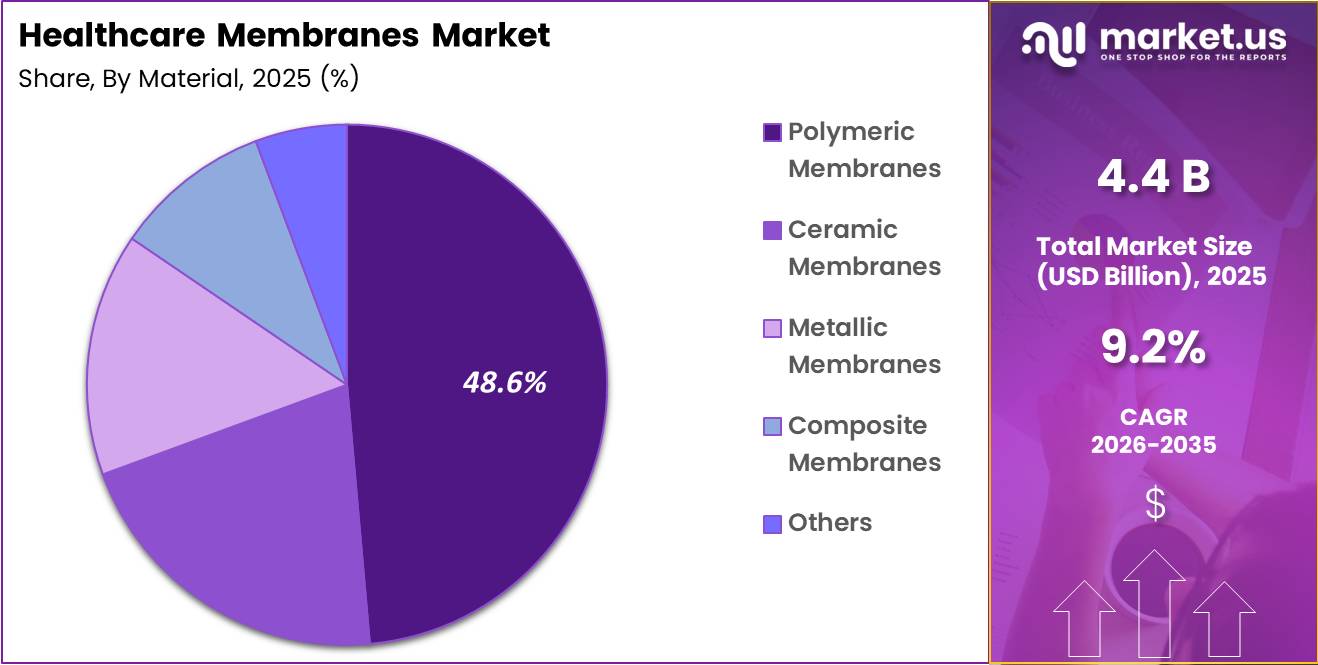

- Material Analysis: The healthcare membranes market is largely dominated by polymeric membranes, which are expected to hold a 48.6%

- Application Analysis: pharmaceutical manufacturing is anticipated to lead the healthcare membranes market, capturing approximately 34.7% of the total share in 2025.

- End User Analysis: consumables accounting for the largest share at 42.3% in 2025.

- Regional Analysis: In 2025, North America led the market, achieving over 39.51% share with a revenue of US$ 1.62 Billion.

Product Type Analysis

The healthcare membranes market, when segmented by product type, demonstrates a diversified portfolio driven by varying filtration requirements and precision levels. Microfiltration membranes are projected to dominate the segment, accounting for approximately 35.2% of the total market share in 2025.

This dominance is attributed to their widespread application in sterilization, bacteria removal, and clarification processes, particularly within pharmaceutical and clinical environments. Ultrafiltration membranes represent the second-largest segment, supported by their efficiency in separating macromolecules and proteins, making them essential in bioprocessing and vaccine production.

Nanofiltration membranes are gaining traction due to their capability to remove divalent ions and organic compounds, thus supporting advanced purification processes. Reverse osmosis membranes continue to play a critical role in achieving high-purity water standards required in healthcare facilities and drug manufacturing.

Ion exchange membranes are increasingly utilized in electrochemical applications, including drug formulation processes. Other membrane types, including specialty and hybrid membranes, contribute to niche applications, ensuring technological diversity. Overall, the segment is characterized by innovation-driven demand and increasing adoption across critical healthcare operations.

Material Analysis

Based on material type, the healthcare membranes market is largely dominated by polymeric membranes, which are expected to hold a 48.6% market share in 2025. Their dominance can be attributed to cost-effectiveness, flexibility, and ease of manufacturing, which make them suitable for a wide range of medical and pharmaceutical applications.

Polymeric membranes are extensively used in filtration, separation, and purification processes due to their tunable properties and scalability. Ceramic membranes represent a significant segment, particularly valued for their thermal stability, chemical resistance, and longer operational lifespan, making them suitable for harsh processing conditions.

Metallic membranes, though relatively niche, are gaining importance in specialized applications requiring high mechanical strength and durability. Composite membranes are witnessing increased adoption due to their ability to combine the advantages of multiple materials, thereby enhancing performance characteristics such as selectivity and permeability.

Other materials, including emerging bio-based and nanomaterial-integrated membranes, are gradually entering the market, driven by innovation and sustainability trends. The material landscape is thus evolving with a focus on performance optimization and cost efficiency.

Application Analysis

In terms of application, pharmaceutical manufacturing is anticipated to lead the healthcare membranes market, capturing approximately 34.7% of the total share in 2025. This leadership is driven by the critical need for high-purity filtration, sterile processing, and stringent regulatory compliance in drug production. Membranes play an essential role in ensuring product safety and consistency across various stages of pharmaceutical manufacturing.

Bioprocessing is another key segment, supported by the rising demand for biologics, vaccines, and cell-based therapies, where membranes are used for separation, concentration, and purification of biomolecules. Drug delivery applications are expanding steadily, particularly with the development of controlled-release and transdermal systems that leverage membrane technologies.

Hemodialysis remains a vital application area, driven by the increasing prevalence of chronic kidney diseases and the growing patient pool requiring dialysis treatment. Diagnostic applications also contribute significantly, utilizing membranes in rapid testing kits and analytical devices. Other applications include medical device filtration and tissue engineering, reflecting the broadening scope of membrane usage across healthcare.

End User Analysis

From an end-user perspective, pharmaceutical and biotechnology companies represent a major segment within the healthcare membranes market, with consumables accounting for the largest share at 42.3% in 2025. The high share of consumables is driven by their recurring usage in filtration, separation, and sterilization processes, which ensures continuous demand.

Hospitals and clinics form another key segment, where membranes are extensively used in dialysis, sterilization, and infection control procedures. Diagnostic laboratories are witnessing steady growth due to increased testing volumes and the adoption of advanced diagnostic technologies that rely on membrane filtration.

Research and academic institutes also contribute significantly, supported by ongoing research activities in life sciences, drug discovery, and biomedical engineering. Other end users, including contract research organizations and specialty clinics, add to the overall market demand.

The segmentation reflects a strong dependence on routine consumption and technological integration, particularly within pharmaceutical and biotechnology environments, which continue to drive sustained market expansion.

Key Market Segments

By Product Type

- Microfiltration Membranes

- Ultrafiltration Membranes

- Nanofiltration Membranes

- Reverse Osmosis Membranes

- Ion Exchange Membranes

- Others

By Material

- Polymeric Membranes

- Ceramic Membranes

- Metallic Membranes

- Composite Membranes

- Others

By Application

- Pharmaceutical Manufacturing

- Bioprocessing

- Drug Delivery

- Hemodialysis

- Water Purification

- Diagnostic Applications

- Others

By End User

- Pharmaceutical and Biotechnology Companies

- Hospitals and Clinics

- Diagnostic Laboratories

- Research and Academic Institutes

- Others

Driving Factors

Rising Burden of Kidney Diseases and Dialysis Demand

The growth of the healthcare membranes market is strongly driven by the increasing prevalence of chronic kidney diseases (CKD) and the subsequent demand for dialysis procedures. According to the Centers for Disease Control and Prevention, millions of patients require regular hemodialysis, with each patient typically undergoing treatment multiple times per week.

This results in high recurring consumption of dialysis membranes as essential consumables. It has been observed that bloodstream infection ratios in dialysis settings declined by nearly 40% between 2014 and 2019, reflecting improved adoption of advanced membrane-based systems and infection control technologies.

Additionally, patients undergoing dialysis face elevated infection risks due to repeated vascular access, increasing the need for high-performance, biocompatible membranes that enhance safety and filtration efficiency.

The rising incidence of diabetes and hypertension key contributors to end-stage renal disease—has further expanded the patient pool globally. As dialysis remains a life-sustaining therapy, the demand for high-flux and synthetic membranes continues to increase steadily, reinforcing long-term market growth.

Trending Factors

Shift Toward Advanced and Biocompatible Membrane Technologies

A key trend shaping the healthcare membranes market is the transition from conventional cellulose-based membranes to advanced synthetic and biocompatible materials.

Clinical research published on National Center for Biotechnology Information indicates that modern membranes such as AN69 and other synthetic variants provide improved toxin removal, better biocompatibility, and enhanced patient outcomes compared to earlier technologies.

These advanced membranes are designed to efficiently remove middle molecules and inflammatory mediators, which are critical for improving long-term dialysis outcomes. Furthermore, improvements in membrane permeability and selectivity have enabled better clearance of uremic toxins while minimizing protein loss.

Another emerging trend is the integration of membranes in biopharmaceutical processing, including sterile filtration and virus removal. The adoption of single-use membrane systems is increasing due to reduced contamination risk and operational efficiency.

This trend aligns with global healthcare priorities focusing on infection control, precision treatment, and improved patient safety, thereby supporting sustained technological advancement in membrane design and application.

Restraining Factors

Stringent Regulatory Requirements and Clinical Risks

The healthcare membranes market faces significant restraints due to strict regulatory frameworks and clinical safety concerns. Regulatory authorities such as the Centers for Disease Control and Prevention emphasize stringent infection prevention guidelines in dialysis settings, requiring continuous compliance and validation of membrane performance.

Membranes used in medical applications must meet rigorous standards for biocompatibility, sterility, and durability. Any failure in membrane performance can lead to severe complications, including bloodstream infections, which remain a critical concern in dialysis patients. Although infection rates have declined, the risk persists, particularly among patients using central venous catheters.

Additionally, high production costs associated with advanced materials and the need for continuous innovation increase the financial burden on manufacturers. Limited lifespan and fouling of membranes also necessitate frequent replacement, adding to operational costs for healthcare providers. These factors collectively restrain widespread adoption, particularly in cost-sensitive healthcare systems and emerging economies.

Opportunity

Expansion of Biopharmaceutical Manufacturing and Water Purification Applications

Significant opportunities are emerging in the healthcare membranes market through the expansion of biopharmaceutical manufacturing and advanced water purification systems. Membrane technologies are increasingly utilized in biologics production for applications such as protein separation, virus filtration, and sterile processing, supporting the growing pipeline of vaccines and monoclonal antibodies.

In parallel, the demand for high-quality dialysis water systems is rising. Dialysis water filtration markets are projected to grow from USD 671 million in 2025 to USD 1,083 million by 2035, reflecting a 4.9% CAGR, driven by the need for ultrapure water in clinical settings.

Government and healthcare agencies are emphasizing patient safety and quality standards, which is accelerating investments in membrane-based purification systems. Additionally, the expansion of home dialysis and decentralized healthcare infrastructure presents new growth avenues for compact and efficient membrane technologies.

Emerging markets such as India and China are witnessing increased healthcare infrastructure development, further supporting adoption. These factors collectively create a favorable environment for innovation and long-term growth in healthcare membrane applications.

Regional Analysis

The global medical membrane market is regionally segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Among these, North America has been identified as the leading regional market, supported by well-established healthcare infrastructure and a rising demand for advanced membrane-based medical technologies.

Continuous technological advancements in medical membrane equipment have further strengthened regional growth. In 2025, North America accounted for over 39.51% of the global market, generating approximately US$ 1.62 billion in revenue. Within this region, the United States is expected to maintain its dominant position, followed by Canada.

Europe represents another significant market, with countries such as France, Germany, and the United Kingdom contributing substantial shares. Growth in this region is supported by strong healthcare systems and increasing adoption of innovative medical technologies.

The Asia Pacific region is projected to experience notable growth over the forecast period. This expansion is driven by increasing healthcare demand, favorable manufacturing conditions, and the presence of cost-effective labor.

Additionally, regulatory flexibility has encouraged global manufacturers to establish production facilities in this region. Emerging economies such as China and India, along with developed markets like Japan, are expected to be key contributors to regional growth, supported by evolving demographics and expanding healthcare access.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The Healthcare Membranes Market is characterized by the presence of several established multinational corporations and specialized membrane technology providers, resulting in a moderately consolidated competitive landscape.

Key players such as Merck KGaA, Danaher Corporation (through its subsidiary Pall Corporation), 3M Company, and Sartorius AG dominate the market due to their extensive product portfolios and global distribution networks.

It has been observed that these companies focus heavily on research and development to enhance membrane efficiency, biocompatibility, and filtration performance. Strategic initiatives such as mergers, acquisitions, and partnerships are frequently adopted to strengthen technological capabilities and expand regional presence.

For instance, advancements in ultrafiltration and nanofiltration membranes are being prioritized to address the growing demand for sterile filtration in biopharmaceutical production.

Emerging players and regional manufacturers are also entering the market, intensifying competition through cost-effective solutions and niche applications. However, high capital investment and stringent regulatory requirements create entry barriers, favoring established firms.

Overall, the competitive dynamics are expected to remain innovation-driven, with leading companies leveraging advanced materials science and process optimization to maintain market share and address evolving healthcare needs.

Market Key Players

- Merck KGaA

- Danaher Corporation

- Sartorius AG

- Thermo Fisher Scientific Inc.

- 3M Company

- Asahi Kasei Corporation

- Parker Hannifin Corporation

- GE Healthcare

- Pentair plc

- Koch Membrane Systems Inc.

- Repligen Corporation

- GEA Group AG

- Meissner Filtration Products Inc.

- Porvair Filtration Group

- Graver Technologies LLC

- Others

Recent Developments

- Thermo Fisher Scientific Inc.: February, 2025, The company announced the acquisition of Solventum’s purification and filtration business valued at approximately $4.1 billion, strengthening its position in bioprocessing filtration and enabling deeper entry into membrane-based purification solutions used in drug manufacturing.

- Danaher Corporation: In Q2 2025, Danaher completed the acquisition of a specialty medical membrane manufacturer for about 150 million USD, strengthening its high‑value filtration and bioprocessing portfolio and deepening its position in single‑use and advanced medical membrane solutions for pharma and biotech customers.

- GE Healthcare: In March 2025, GE Healthcare introduced a new nanostructured dialysis membrane platform aimed at improving uremic toxin clearance while preserving essential proteins, positioning the company more strongly in high‑performance renal care membranes.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 4.4 Billion |

| Forecast Revenue (2035) | US$ 10.5 Billion |

| CAGR (2026-2035) | 9.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Microfiltration Membranes, Ultrafiltration Membranes, Nanofiltration Membranes, Reverse Osmosis Membranes, Ion Exchange Membranes, Others) By Material (Polymeric Membranes, Ceramic Membranes, Metallic Membranes, Composite Membranes, Others) By Application (Pharmaceutical Manufacturing, Bioprocessing, Drug Delivery, Hemodialysis, Water Purification, Diagnostic Applications, Others) By End User (Pharmaceutical and Biotechnology Companies, Hospitals and Clinics, Diagnostic Laboratories, Research and Academic Institutes, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Merck KGaA, Danaher Corporation, Sartorius AG, Thermo Fisher Scientific Inc., 3M Company, Asahi Kasei Corporation, Parker Hannifin Corporation, GE Healthcare, Pentair plc, Koch Membrane Systems Inc., Repligen Corporation, GEA Group AG, Meissner Filtration Products Inc., Porvair Filtration Group, Graver Technologies LLC, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |