Global Hairbrush Market Size, Share, Growth Analysis By Product (Paddle Brush, Round Brush, Vent Brush, Cushion Brush, Detangling Brush, Others), By Material (Synthetic, Organic), By Application (Personal, Professional), By End-user (Women, Men, Children), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 182453

- Number of Pages: 393

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

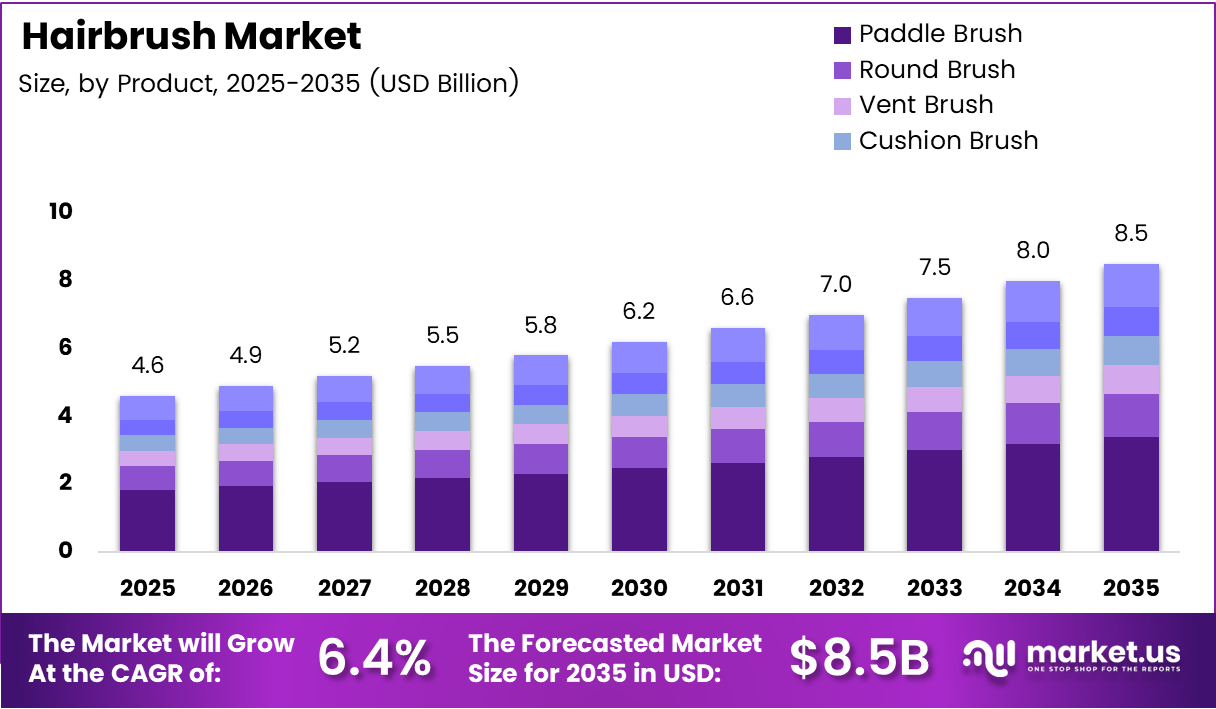

Global Hairbrush Market size is expected to be worth around USD 8.5 Billion by 2035 from USD 4.6 Billion in 2025, growing at a CAGR of 6.4% during the forecast period 2026 to 2035.

The hairbrush market covers a broad range of manual and technology-enhanced grooming tools designed for detangling, styling, and scalp care. Product categories include paddle brushes, round brushes, vent brushes, cushion brushes, and detangling brushes. Demand comes from both personal consumers and professional salon operators across global markets.

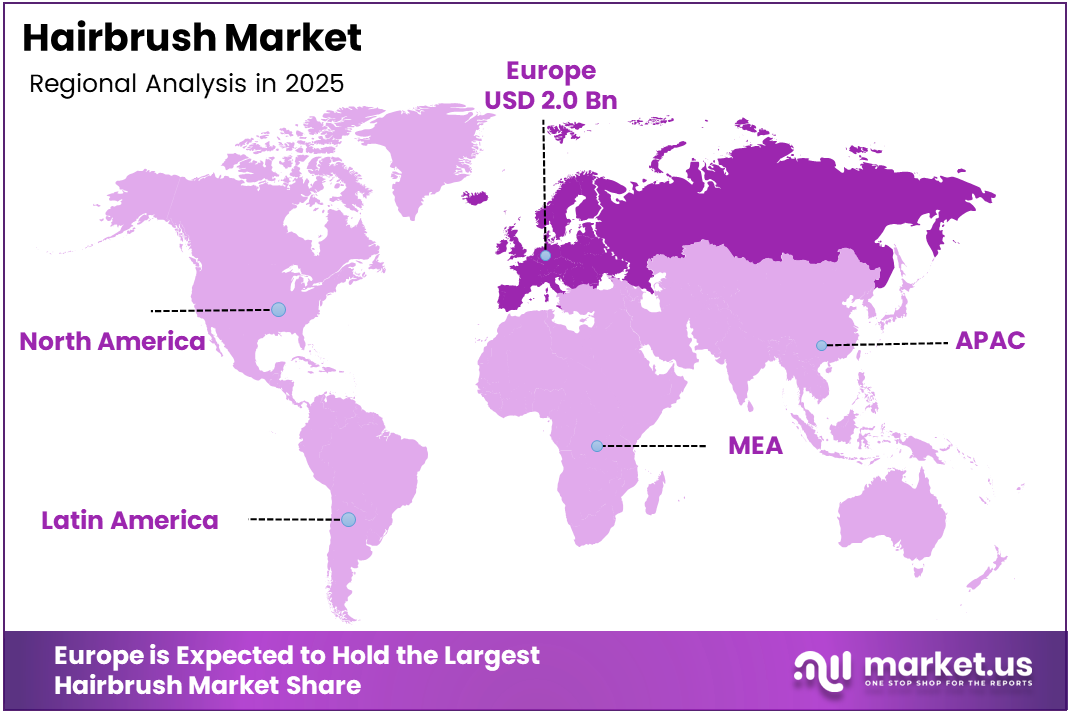

Europe leads this market with a 45.20% share valued at USD 2.0 Billion, reflecting mature grooming cultures and strong retail infrastructure. This regional concentration signals that premium brush formats — ergonomic, anti-breakage, and material-conscious designs — already command consumer willingness to pay in established markets. Brands targeting Europe must compete on quality and positioning, not price.

The 6.4% CAGR reflects a market where consumers are moving beyond commodity brush purchases toward purposeful grooming tools. This shift is most visible in the growth of detangling and anti-breakage brush categories, which directly address concerns around hair health. Buyers are making decisions based on performance claims, not aesthetics alone.

E-commerce expansion has materially changed how premium and specialized hairbrushes reach end consumers. Brands with strong digital presence now access consumer segments — particularly women with curly, long, or textured hair — that traditional retail channels underserved. This distribution shift creates structural advantages for direct-to-consumer and specialty brands.

Professional salon culture continues to anchor volume demand globally, while personal grooming habits among men and younger demographics expand the total addressable market. These two demand pools move at different speeds: salon channels prioritize performance, while personal consumers respond more to social proof, influencer endorsement, and ingredient claims.

According to a research study, a hairbrush designed with a new bristle pattern reduced hair breakage by up to 39% compared to a standard lab brush. This finding matters because it validates the premium pricing logic — consumers paying more for advanced brush designs can now point to measurable clinical outcomes, not just brand claims.

In the same research study, 77% of participants noticed less shedding and breakage after just 2 weeks of use. That level of consumer-observable improvement within a short trial window suggests that hair health benefits are not just a marketing angle — they are a retention and repurchase driver with real commercial value for brands that invest in bristle innovation.

Key Takeaways

- The Global Hairbrush Market was valued at USD 4.6 Billion in 2025 and is forecast to reach USD 8.5 Billion by 2035, at a CAGR of 6.4%.

- By Product, Paddle Brush holds the dominant share at 31.5% of the market.

- By Material, Synthetic brushes lead with a 68.9% share due to durability and cost advantages.

- By Application, Personal use accounts for 78.3% of total market demand.

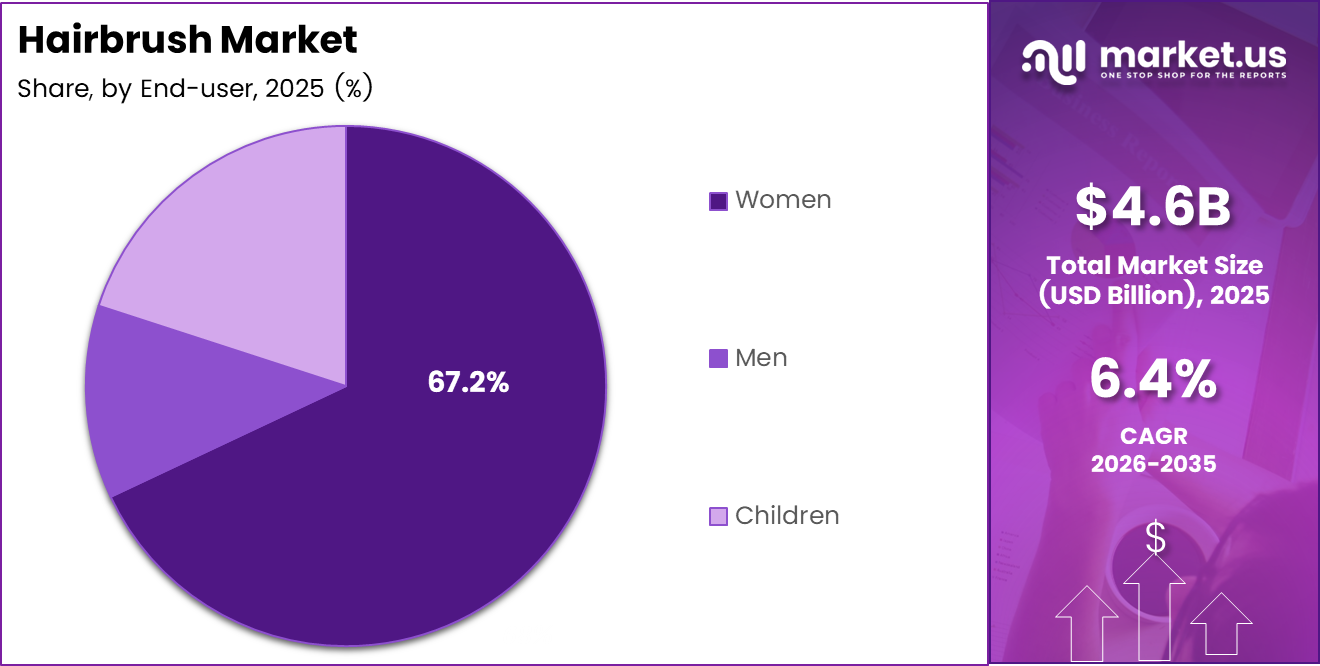

- By End-user, Women represent the largest segment with a 67.2% share.

- Europe dominates regionally with a 45.20% share, valued at USD 2.0 Billion.

- In December 2024, BIC acquired Tangle Teezer for approximately €200 million, signaling consolidation in the premium brush segment.

Product Analysis

Paddle Brush dominates with 31.5% due to broad suitability across hair types.

In 2025, Paddle Brush held a dominant market position in the By Product segment of the Hairbrush Market, with a 31.5% share. Its flat, wide base makes it effective for straightening, smoothing, and detangling, giving it functional utility that covers most consumer hair care routines. This cross-segment versatility is what sustains its share lead.

Round Brush serves as the primary professional styling tool for blowouts and volume creation. Salons and professional stylists drive consistent volume demand for this format, and as salon culture expands in emerging markets, round brush penetration follows. Its dependency on heat-styling technique limits mass consumer uptake but anchors it firmly in professional grooming channels.

Vent Brush differentiates through airflow-optimized design that reduces blowdry time. Consumers seeking faster styling routines favor vent brushes for their efficiency. This time-saving positioning makes them attractive to working professionals and daily grooming users who prioritize speed, creating a distinct buyer segment that premium brands can target.

Cushion Brush carries a strong value proposition in scalp comfort, thanks to its flexible pneumatic base that absorbs pressure during brushing. This design reduces mechanical stress on the scalp and is increasingly recommended for users with sensitivity concerns. Its positioning at the intersection of comfort and daily use supports steady demand.

Detangling Brush addresses one of the most common hair care complaints — knots and breakage during brushing. According to a research study, 79% of participants observed less hair buildup on a redesigned brush after regular use. This data signals that functional performance in detangling is measurable and consumer-verifiable, which strengthens the category’s case for premium pricing and repeat purchase.

Others in the product mix include boar bristle brushes, teasing brushes, and ionic-technology formats. These serve niche but high-value grooming needs. As consumers become more informed about hair damage and scalp health, specialty brushes gain relevance and command above-average margins for brands that position them correctly.

Material Analysis

Synthetic dominates with 68.9% due to cost efficiency and material durability.

In 2025, Synthetic materials held a dominant market position in the By Material segment of the Hairbrush Market, with a 68.9% share. Nylon and plastic bristles deliver consistent performance, resist moisture, and support high-volume manufacturing at lower cost. This combination of durability and affordability makes synthetic brushes the default choice across mass retail and e-commerce channels.

Organic material brushes — including boar bristle, bamboo handles, and plant-based components — represent the fastest-repositioning segment. Consumer interest in vegan and cruelty-free personal care products is shifting purchasing criteria away from purely functional metrics. Brands investing in certified organic and sustainably sourced materials are gaining shelf space in premium retail and attracting environmentally motivated buyers.

Application Analysis

Personal dominates with 78.3% due to daily household grooming volume.

In 2025, Personal use held a dominant market position in the By Application segment of the Hairbrush Market, with a 78.3% share. Household consumers brush their hair daily, generating the highest unit volume and repurchase frequency in the market. This makes personal-use formats the commercial anchor for both mass-market and premium brush brands.

Professional application covers salon operators, hairstylists, and grooming service providers. This segment buys at lower volumes but demands higher performance — durability, heat resistance, and ergonomic design for continuous use. Professional buyers also act as influencers on consumer purchasing, as styling professionals frequently recommend preferred brush brands to their clients.

End-user Analysis

Women dominate with 67.2% due to higher grooming frequency and product variety demands.

In 2025, Women held a dominant market position in the By End-user segment of the Hairbrush Market, with a 67.2% share. Women represent the core buyer base across all brush formats — from detangling and paddle brushes for daily use to round brushes for styling. Their purchasing behavior responds strongly to social media influence, product claims, and format innovation.

Men represent an underpenetrated but expanding end-user segment. Rising grooming awareness among male consumers, combined with the growth of beard care and textured hair styling categories, creates demand for specialized brush formats beyond traditional hairbrushes. Brands entering men’s grooming with targeted brush products face low direct competition and above-average margin potential.

Children as an end-user segment are primarily driven by parent purchasing decisions focused on gentleness and scalp safety. Brushes designed with soft, flexible bristles and ergonomic grips for pediatric use occupy a niche but defensible category. Safety certifications and dermatologist endorsements carry significant weight with this buyer group.

Key Market Segments

By Product

- Paddle Brush

- Round Brush

- Vent Brush

- Cushion Brush

- Detangling Brush

- Others

By Material

- Synthetic

- Organic

By Application

- Personal

- Professional

By End-user

- Women

- Men

- Children

Drivers

Scalp Health Awareness and Salon Culture Expansion Drive Demand for Advanced Hairbrush Formats

Consumer focus on hair health has moved from aesthetics to clinical outcomes. Buyers now evaluate brushes based on anti-breakage claims, scalp stimulation features, and bristle material quality. According to a research study, 87% of clinical participants reported that an advanced brush design felt gentle on the scalp and hair. This data shows that comfort-led brush innovation converts into measurable consumer preference.

Professional salon culture amplifies this demand across markets. As grooming services expand globally, salon professionals — who specify, purchase, and recommend brushes daily — pull premium and performance brush formats into wider consumer awareness. Brands with a credible professional-use positioning benefit from this halo effect in retail and direct-to-consumer channels.

In February 2025, Augustinus Bader and La Bonne Brosse launched the N.04 The Miracle Detangling Scalp Brush, combining luxury skincare credibility with functional brush design. This product signals that premium skincare brands now see hairbrushes as a viable adjacent category — raising consumer expectations for the segment and pressuring mid-tier brands to justify their formulations and materials more rigorously.

Restraints

Low-Cost Competition and Multifunctional Styling Tools Compress Hairbrush Market Growth

The proliferation of unbranded, low-cost hairbrushes across e-commerce platforms and discount retail creates sustained margin pressure on established brands. Price-sensitive consumers, particularly in emerging markets, default to commodity options that undercut branded products on unit economics. This dynamic limits premium brand penetration in high-volume, lower-income consumer segments.

Multifunctional hair styling tools — including heated styling brushes, electric detanglers, and combined brush-dryer formats — are absorbing demand that traditional brushes previously captured. According to a research study, 83% of clinical participants felt more confident about their hair health after using an advanced brush design. That confidence, however, increasingly attaches to technology-integrated products, not passive brush formats.

This shift toward powered tools does not eliminate traditional hairbrush demand, but it segments the market more sharply. Passive brushes retain relevance for daily maintenance and scalp care, while styling occasions migrate toward powered alternatives. Brands that fail to differentiate on materials, ergonomics, or clinical claims risk commoditization as buyers prioritize multifunctionality.

Growth Factors

Sustainable Materials, Smart Technology, and Men’s Grooming Expansion Create New Revenue Categories

Eco-conscious consumer behavior is reshaping brush material choices. Brands developing hairbrushes from bamboo handles, plant-based bristles, and recycled plastics are addressing a buyer group that actively filters purchases through environmental values. Peer-reviewed dermatology evidence also indicates that improperly used hairbrushes can contribute to traction alopecia and structural hair damage — a clinical finding that elevates the importance of material quality and brush design in purchase decisions.

Smart hairbrush technology — integrating sensors that monitor scalp condition, hair porosity, and brushing pressure — opens a premium tier that command significantly higher margins. According to a research study, 88% of participants would recommend an advanced brush to someone concerned about hair loss. This consumer readiness to endorse clinically positioned brush products confirms that a market for health-monitoring grooming tools exists and will reward early category builders.

Men’s grooming and beard care represent an underdeveloped demand pool with low direct competition. As grooming routines among male consumers become more structured, demand for specialized brushes — beard brushes, scalp stimulating brushes, and styling tools for short textured hair — creates product categories that current brush manufacturers are only beginning to serve systematically.

Emerging Trends

Ionic Technology, Social Media Influence, and Scalp-Massaging Bristles Redefine Consumer Brush Expectations

Ionic and anti-static hairbrush technology addresses frizz and static buildup — two persistent complaints among consumers with fine or chemically treated hair. This technology signals a move away from passive bristle designs toward brushes that actively modify hair surface chemistry during use. Brands integrating ionic features into everyday brush formats gain a tangible claim that separates them from commodity alternatives.

Social media platforms and beauty influencers have accelerated consumer education on hairbrush functionality. Tutorial content demonstrating brush technique, product comparisons, and before-and-after styling results builds purchase intent at scale. According to a research study, 82% of clinical participants said they would purchase an advanced brush after testing it — a conversion signal that aligns closely with the discovery-to-purchase journey that social media accelerates.

Scalp-massaging bristle technology is emerging as a standalone positioning pillar for brush brands. By targeting blood circulation improvement alongside traditional detangling and styling functions, these brushes extend into wellness positioning territory. Consumer interest in scalp health as a root cause of hair quality elevates the perceived value of brushes with massage functionality beyond standard grooming tools.

Regional Analysis

Europe Dominates the Hairbrush Market with a Market Share of 45.20%, Valued at USD 2.0 Billion

Europe leads the global hairbrush market with a 45.20% share valued at USD 2.0 Billion, supported by mature retail infrastructure, premium grooming culture, and strong consumer demand for quality personal care products. European buyers consistently favor branded, high-performance brushes across both personal and professional use segments, sustaining price premiums that drive high revenue concentration in this region.

North America Hairbrush Market Trends

North America represents a high-value market anchored by established personal care retail, broad e-commerce penetration, and strong salon industry demand. The region’s consumers respond well to clinically positioned and technology-enhanced brush products. Expanding men’s grooming product lines and the rising popularity of anti-breakage brush formats among women with textured hair sustain above-average unit pricing across the market.

Asia Pacific Hairbrush Market Trends

Asia Pacific presents volume-led growth potential driven by large consumer populations in China, India, and Southeast Asia, combined with rising disposable income and expanding beauty retail channels. Urban consumers in this region show strong responsiveness to social media-driven product discovery, making influencer marketing and digital commerce the primary route-to-market for brush brands entering or scaling in this geography.

Latin America Hairbrush Market Trends

Latin America offers a growing consumer base with high cultural investment in hair care and styling. Brazil and Mexico anchor demand, with professional salon density providing a pull channel for premium brush formats. Price sensitivity remains a structural constraint, however, and brands succeeding in this region typically offer tiered product lines that address both value and performance buyer segments simultaneously.

Middle East and Africa Hairbrush Market Trends

The Middle East and Africa region shows differentiated demand across its geography. Gulf Cooperation Council markets favor premium personal care products and have growing organized retail and e-commerce channels capable of distributing specialized brush formats. Sub-Saharan African markets are at an earlier stage of branded product penetration, but urbanization and rising income levels are expanding the addressable consumer base over the medium term.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Bristle Hair Brush positions itself around traditional bristle craftsmanship, a differentiation strategy that resonates with premium consumers who distrust synthetic mass-market alternatives. By anchoring its identity in material quality and hair-health outcomes, the brand insulates itself from commodity price competition. This positioning carries structural durability as clinical and wellness-oriented brush purchasing continues to displace commodity buying behavior.

Denman has built its market position through functional brush design optimized for curl definition and detangling — two of the highest-growth use cases in the current consumer environment. Its sustained relevance among consumers with textured and natural hair gives Denman a defensible niche that larger generalist brands find difficult to replicate. This user-community loyalty translates into organic social proof and reduced dependency on paid marketing.

Mason Pearson operates at the luxury tier of the hairbrush market, where the brand’s heritage and boar-bristle quality command prices that most competitors cannot justify. Its strategic value lies not in volume but in category anchoring — Mason Pearson defines what a premium hairbrush should cost and feel like, setting reference points that the entire market prices against. This anchor position is difficult to displace and generates consistent demand among high-income buyers.

Conair LLC dominates the mass-market segment through scale, distribution breadth, and product range depth. Its ability to serve every brush format across every price tier gives it unmatched retail coverage. For Conair, the strategic risk is commoditization from below — low-cost unbranded alternatives that compete on the same price tier — requiring continued investment in branding and format innovation to sustain its position.

Key Players

- Bristle Hair Brush

- Denman

- Mason Pearson

- Conair LLC

- G.B. Kent & Sons

- L’Oreal Paris

- Spornette

- Crave Naturals

- Dyson Limited

- Revlon Inc.

- Spectrum Brands, Inc.

Recent Developments

- December 2024 — BIC acquired Tangle Teezer for approximately €200 million, marking a significant consolidation move in the premium hairbrush segment. This acquisition signals BIC’s strategic intent to build a personal care portfolio beyond its core stationery and lighter businesses, placing Tangle Teezer’s specialist detangling brand equity under a global distribution network.

Report Scope

Report Features Description Market Value (2025) USD 4.6 Billion Forecast Revenue (2035) USD 8.5 Billion CAGR (2026-2035) 6.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Paddle Brush, Round Brush, Vent Brush, Cushion Brush, Detangling Brush, Others), By Material (Synthetic, Organic), By Application (Personal, Professional), By End-user (Women, Men, Children) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Bristle Hair Brush, Denman, Mason Pearson, Conair LLC, G.B. Kent & Sons, L’Oreal Paris, Spornette, Crave Naturals, Dyson Limited, Revlon Inc., Spectrum Brands, Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Bristle Hair Brush

- Denman

- Mason Pearson

- Conair LLC

- G.B. Kent & Sons

- L'Oreal Paris

- Spornette

- Crave Naturals

- Dyson Limited

- Revlon Inc.

- Spectrum Brands, Inc.

Our Clients

- 182453

- Mar 2026