Quick Navigation

Report Overview

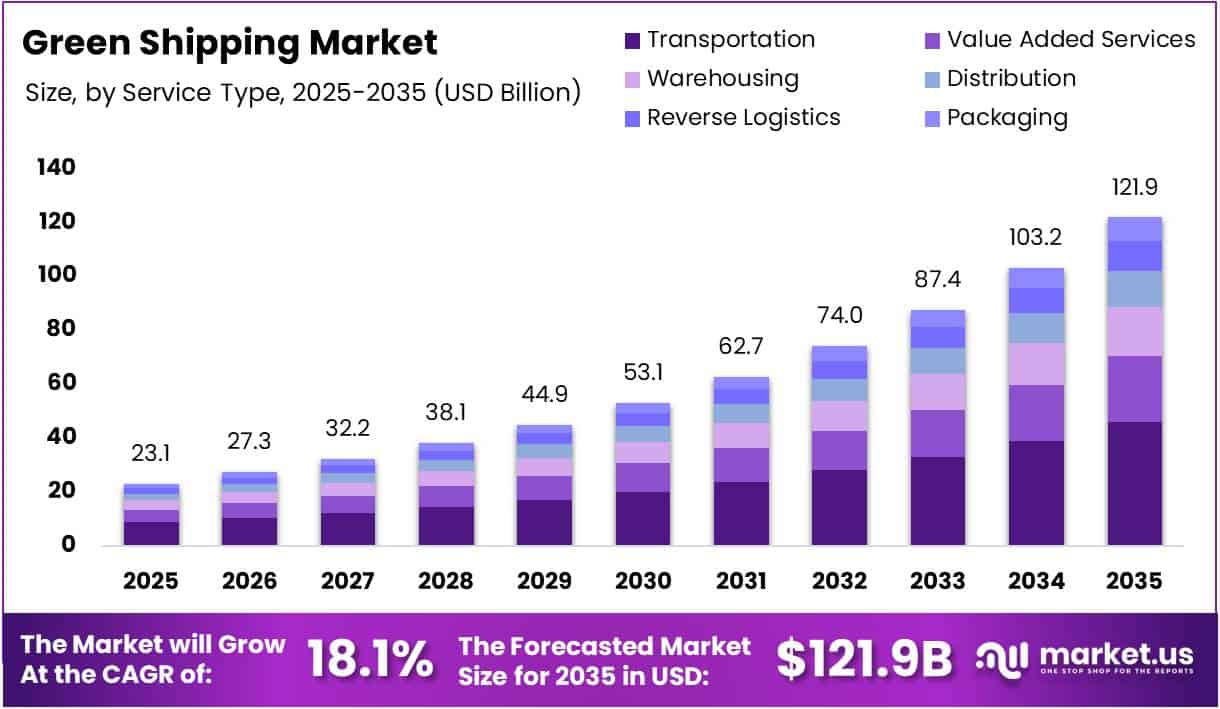

The Global Green Shipping Market size is expected to be worth around USD 121.9 Billion by 2035 from USD 23.1 Billion in 2025, growing at a CAGR of 18.1% during the forecast period 2026 to 2035.

Green shipping refers to the adoption of environmentally sustainable practices across maritime logistics and freight transport. It encompasses the use of alternative fuels, energy-efficient vessel technologies, and low-emission operational strategies. The market is gaining momentum as global trade increasingly aligns with climate-focused regulations and net-zero commitments.

The market covers a wide range of services including transportation, warehousing, distribution, and reverse logistics. Moreover, it spans multiple modes of operation such as seaways, roadways, airways, and railways. End-use industries including manufacturing, healthcare, automotive, retail, and banking are actively integrating green shipping into their supply chains.

Regulatory pressure is a significant growth catalyst. The International Maritime Organization’s Net-Zero 2050 framework mandates strict decarbonization across global fleets. Additionally, the European Union Emissions Trading System now includes maritime activities, compelling shipping operators to invest in cleaner technologies and fuel alternatives.

Government-backed infrastructure investments are accelerating green shipping adoption worldwide. Onshore power supply installations, green port initiatives, and alternative fuel bunkering facilities are receiving substantial public and private funding. Consequently, operators are developing commercially viable zero-emission shipping corridors, particularly for short-sea and coastal routes.

Statistical evidence further supports robust market expansion. According to Shipping Telegraph, nearly 60% of shipping firms surveyed are now developing formal decarbonization roadmaps. Furthermore, according to Seatrade Maritime, adoption of bio-blended fuels rose from 22% to 46% among carriers, demonstrating a clear industry-wide shift toward sustainable fuel solutions.

According to the World Economic Forum, fuel combustion in maritime operations accounts for over 80% of total shipping life cycle emissions, primarily due to reliance on fossil fuels. Additionally, according to Shipping Telegraph, wind-assisted propulsion systems deliver 5–20% fuel consumption reductions depending on vessel type and route, making them a commercially attractive green investment.

Key Takeaways

- The Global Green Shipping Market was valued at USD 23.1 Billion in 2025 and is projected to reach USD 121.9 Billion by 2035.

- The market is growing at a CAGR of 18.1% during the forecast period 2026 to 2035.

- By Service Type, the Transportation segment holds a dominant share of 37.8%.

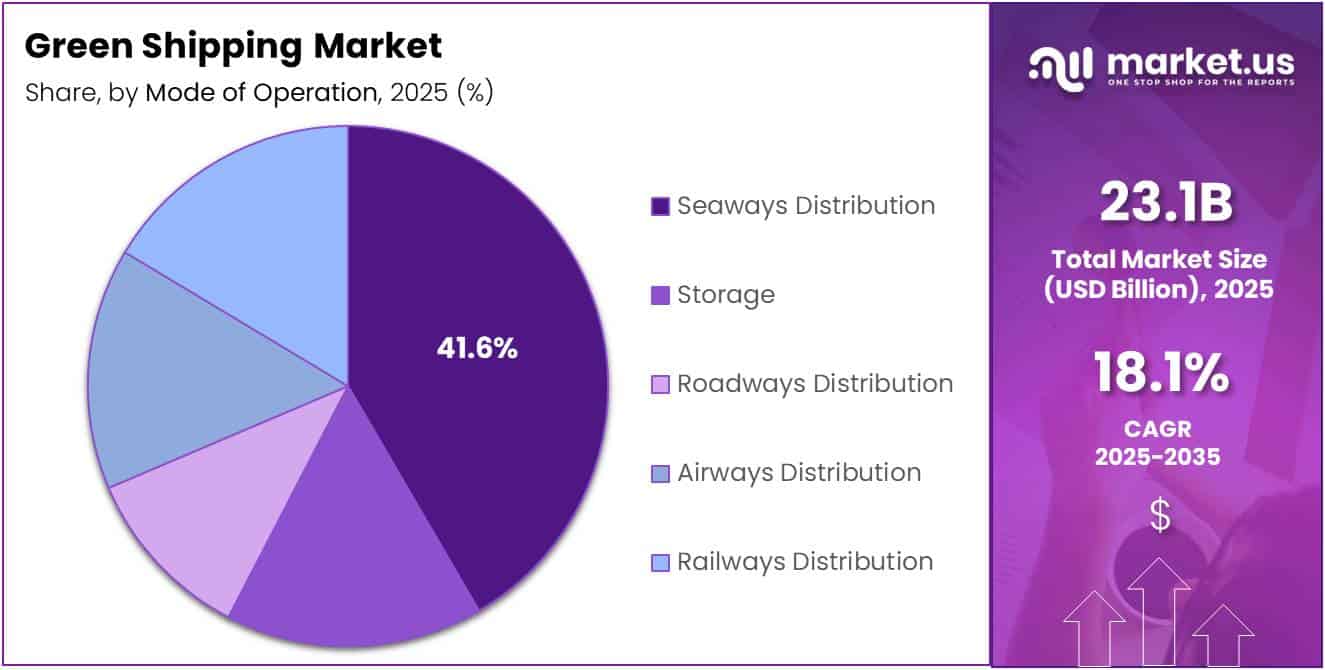

- By Mode of Operation, the Seaways Distribution segment leads with a 41.6% market share.

- By End Use, the Manufacturing segment captures the largest share at 31.5%.

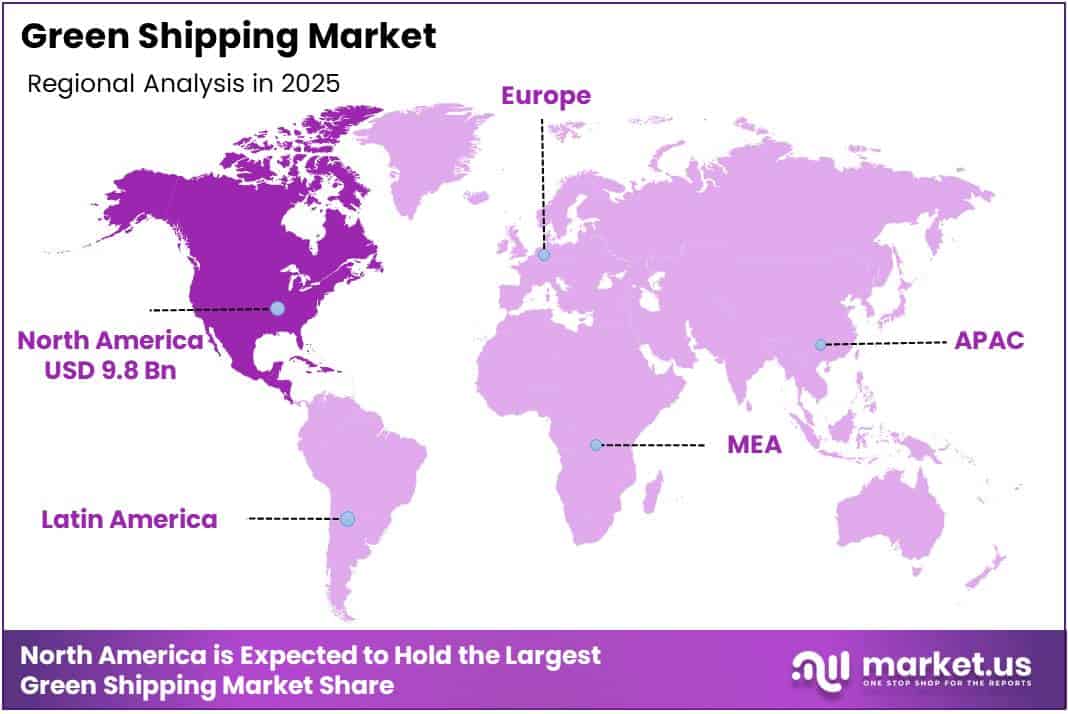

- North America dominates the regional landscape with a 42.7% market share, valued at USD 9.8 Billion.

By Service Type Analysis

Transportation dominates with 37.8% due to high freight volume demands and green fuel adoption in core logistics operations.

In 2025, Transportation held a dominant market position in the By Service Type segment of the Green Shipping Market, with a 37.8% share. This segment leads because primary freight movement accounts for the largest portion of logistics activity. Moreover, rising demand for low-emission freight carriers has accelerated green technology adoption within transportation operations globally.

Value Added Services are growing steadily as clients demand sustainability-integrated logistics beyond standard freight. Companies are offering green consulting, carbon tracking, and eco-certified handling as part of broader service packages. Consequently, value added services are becoming a key differentiator for logistics providers seeking to attract environmentally committed corporate customers.

Warehousing is undergoing a significant sustainability transformation as operators invest in energy-efficient storage facilities. Solar-powered warehouses and smart energy management systems are becoming standard expectations. Furthermore, green-certified warehousing is increasingly required by large retailers and manufacturers who embed environmental standards into their entire supply chain partner requirements.

Distribution networks are being redesigned to reduce last-mile and mid-mile emissions across urban and regional freight corridors. Electric vehicles and route optimization technologies are central to this shift. Additionally, green distribution strategies help companies lower operating costs while meeting both regulatory requirements and corporate sustainability targets simultaneously.

Reverse Logistics supports circular economy goals by enabling efficient product return and recycling processes with minimal environmental impact. Companies are building dedicated low-emission return supply chains to handle growing e-commerce return volumes. Moreover, sustainable reverse logistics is helping businesses recover value from returned goods while reducing landfill waste across global supply chains.

Packaging is gaining traction as brands replace single-use plastics with recyclable, biodegradable, and lightweight materials throughout the shipping cycle. Reducing packaging weight directly lowers freight emissions by improving load efficiency. Therefore, eco-friendly packaging is increasingly viewed as both a sustainability commitment and a practical cost-reduction strategy for green shipping operations.

By Mode of Operation Analysis

Seaways Distribution dominates with 41.6% due to its critical role in global trade and the sector’s urgent shift toward low-emission maritime solutions.

In 2025, Seaways Distribution held a dominant market position in the By Mode of Operation segment of the Green Shipping Market, with a 41.6% share. Maritime transport handles the majority of global trade by volume. Consequently, decarbonization efforts in seaways have attracted the largest share of green investment and regulatory focus worldwide.

Storage operations within the green shipping ecosystem are evolving to meet sustainability standards at ports and inland logistics hubs. Energy-efficient storage facilities with low-emission handling equipment are in growing demand. Furthermore, operators are integrating renewable energy sources into port storage infrastructure to reduce the overall carbon footprint of cargo handling activities.

Roadways Distribution is experiencing rapid green transformation through the deployment of electric and hydrogen-powered trucks across regional and urban freight networks. Fleet electrification is being supported by government incentives and corporate sustainability mandates. Moreover, advances in battery technology and charging infrastructure are making zero-emission road freight increasingly viable at commercial scale.

Airways Distribution is addressing its significant carbon intensity through the adoption of sustainable aviation fuels and operational efficiency improvements. Airlines and air freight operators are blending sustainable fuels to reduce lifecycle emissions on key cargo routes. Additionally, investment in next-generation aircraft and weight-reduction strategies is contributing to measurable emissions reductions across air logistics operations.

Railways Distribution continues to gain preference as a lower-carbon alternative to road freight for medium and long-distance cargo movement. Rail freight emits significantly less carbon per tonne-kilometre compared to road transport. Therefore, shippers with strong sustainability commitments are increasingly incorporating rail into their multimodal logistics strategies to reduce overall supply chain emissions.

By End Use Analysis

Manufacturing dominates with 31.5% due to large freight volumes and mounting corporate sustainability mandates within global production supply chains.

In 2025, Manufacturing held a dominant market position in the By End Use segment of the Green Shipping Market, with a 31.5% share. Manufacturers generate large and consistent freight volumes across global supply chains. Therefore, they are among the earliest and largest adopters of green shipping commitments, driven by both regulatory compliance and supplier sustainability requirements.

Healthcare logistics is increasingly demanding low-emission, temperature-controlled transport solutions to move pharmaceuticals, medical devices, and supplies globally. Sustainability is becoming a procurement criterion for healthcare organizations worldwide. Moreover, cold chain operators are investing in energy-efficient refrigeration technologies and cleaner transport modes to meet healthcare sector environmental and compliance standards.

Automotive logistics is aligning its inbound and outbound freight operations with broader electric vehicle production sustainability goals. Automakers are embedding green shipping criteria into supplier contracts and inbound parts logistics. Consequently, logistics providers serving the automotive sector are accelerating fleet electrification and carbon reporting capabilities to retain and grow key industry partnerships.

Banking and Financial Services firms are integrating green logistics into their operational sustainability frameworks, particularly for document handling, equipment distribution, and branch supply chains. ESG commitments are influencing procurement decisions across the sector. Furthermore, financial institutions are increasingly requiring sustainability certifications from logistics partners as part of their own corporate reporting and disclosure obligations.

Retail and E-Commerce is one of the fastest-growing end-use segments, driven by consumer expectations for sustainable delivery and packaging. Major e-commerce platforms are committing to net-zero last-mile delivery programs. Additionally, retailers are partnering with green logistics providers to meet Scope 3 emissions reduction targets and satisfy growing regulatory and investor scrutiny on supply chain sustainability.

Others encompass industries such as agriculture, chemicals, and energy, where green logistics compliance is becoming increasingly mandatory. These sectors generate significant freight volumes with complex cross-border supply chains. Therefore, they represent a substantial and growing demand base for certified low-emission shipping services as global sustainability standards tighten across all major trade corridors.

Key Market Segments

By Service Type

- Transportation

- Value Added Services

- Warehousing

- Distribution

- Reverse Logistics

- Packaging

By Mode of Operation

- Seaways Distribution

- Storage

- Roadways Distribution

- Airways Distribution

- Railways Distribution

By End Use

- Manufacturing

- Healthcare

- Automotive

- Banking and Financial Services

- Retail and E-Commerce

- Others

Drivers

Stringent Decarbonization Mandates and Carbon Pricing Pressure Drive Green Shipping Market Growth

The International Maritime Organization’s Net-Zero 2050 framework is one of the most powerful forces shaping this market. Shipping companies must develop and implement credible decarbonization roadmaps to remain compliant. Consequently, this mandate is accelerating investment in alternative fuels, cleaner vessels, and sustainable logistics infrastructure across global trade routes.

The European Union’s Emissions Trading System now includes maritime shipping, creating direct carbon cost exposure for operators. This carbon pricing mechanism incentivizes early adoption of green technologies. Moreover, companies facing rising carbon costs are fast-tracking fuel switching and fleet upgrades to protect margins and maintain access to key European trade lanes.

Rising green freight procurement commitments from global retail and manufacturing conglomerates are creating sustained commercial demand. Large corporations are embedding sustainability criteria into supplier selection and logistics contracts. Therefore, shipping and logistics providers that offer certified low-emission freight solutions are securing long-term partnerships and positioning themselves for stronger revenue growth.

Restraints

Infrastructure Gaps and High Capital Costs Restrain Green Shipping Market Adoption

A major restraint in the green shipping market is the limited global availability of scalable bunkering infrastructure for green marine fuels. Ports capable of supplying green methanol, ammonia, or hydrogen at commercial scale remain scarce. Consequently, shipping operators face range limitations and operational uncertainty that slow their transition away from conventional fossil fuel systems.

High capital intensity creates significant barriers for vessel operators considering alternative-fuel retrofits or newbuilds. Financing constraints are especially challenging for small and mid-sized shipping companies. Moreover, lenders and investors require clearer long-term return profiles before committing to large green vessel projects, creating a funding gap that delays the pace of fleet transformation.

Technology uncertainty remains a persistent challenge, particularly around the long-term viability of ammonia and hydrogen propulsion systems. Both fuels face safety, storage, and energy density challenges that are not yet fully resolved. Therefore, many operators are adopting a wait-and-see approach, preferring dual-fuel or transitional solutions rather than committing fully to next-generation propulsion technologies.

Growth Factors

Green Fuel Supply Chains, Zero-Emission Corridors, and Port Infrastructure Investment Accelerate Market Expansion

The expansion of green methanol and ammonia supply chains through strategic energy partnerships is a key growth enabler. Energy companies and port authorities are investing in production and distribution networks for these fuels. Moreover, international collaborations between governments and private sector firms are shortening timelines for commercial green fuel availability at scale.

The development of zero-emission coastal and short-sea shipping corridors is creating replicable models for decarbonized freight. These corridors allow shipping firms to test green technologies on shorter, lower-risk routes. Consequently, successful corridor projects are building investor and operator confidence, leading to faster deployment across longer deep-sea trade routes globally.

Investment in Onshore Power Supply, commonly known as cold ironing, at major container ports is growing rapidly. This technology allows vessels to switch off engines and connect to shore-based electricity while berthed. Therefore, it reduces port emissions significantly and supports broader green shipping compliance goals, making it a highly attractive infrastructure investment priority.

Emerging Trends

Dual-Fuel Vessels, Wind-Assisted Propulsion, and Blockchain Carbon Accounting Reshape Green Shipping

The commercial deployment of dual-fuel LNG and methanol-ready container vessels is emerging as a dominant industry trend. Shipbuilders and owners are ordering vessels capable of operating on multiple fuel types to hedge against fuel market uncertainty. Moreover, methanol-ready designs are gaining favor as green methanol supply chains develop and long-term cost structures become clearer.

Wind-assisted propulsion technologies, including rotor sails and rigid wings, are gaining significant traction among shipping operators. These systems reduce fuel consumption without requiring full fuel switching. Furthermore, according to Shipping Telegraph, wind-assisted propulsion can deliver 5–20% fuel savings depending on route and vessel type, making it one of the most cost-effective near-term decarbonization tools available.

The integration of blockchain-based carbon accounting systems is transforming maritime logistics transparency. These systems allow shippers and cargo owners to track verified emissions data across the supply chain. Consequently, blockchain-enabled carbon reporting is becoming a competitive differentiator, helping logistics providers meet corporate sustainability disclosure requirements and satisfy growing demand for verifiable green freight credentials.

Regional Analysis

North America Dominates the Green Shipping Market with a Market Share of 42.7%, Valued at USD 9.8 Billion

North America leads the global Green Shipping Market, holding a dominant 42.7% share valued at USD 9.8 Billion in 2025. The region benefits from strong regulatory frameworks, significant port infrastructure investment, and large-scale green procurement commitments from major retail and manufacturing corporations. Moreover, government-backed clean energy programs continue to accelerate the adoption of alternative fuels and zero-emission logistics solutions.

Europe Green Shipping Market Trends

Europe is a key growth region, driven by the European Union’s Emissions Trading System and aggressive maritime decarbonization policies. Major shipping nations including Germany, the UK, and the Netherlands are investing heavily in green port infrastructure and alternative fuel bunkering. Furthermore, the region’s strong regulatory environment is pushing logistics providers to fast-track fleet upgrades and low-emission freight commitments.

Asia Pacific Green Shipping Market Trends

Asia Pacific represents a high-growth opportunity given its massive trade volumes and large shipbuilding industry. China, Japan, and South Korea are leading investments in green vessel construction and alternative fuel development. Additionally, government-backed industrial policies across the region are supporting the integration of cleaner shipping technologies to address both environmental and energy security goals.

Middle East and Africa Green Shipping Market Trends

The Middle East and Africa region is emerging as a strategic hub for green shipping fuel production, particularly green hydrogen and ammonia. Gulf nations are investing in large-scale clean energy export infrastructure aligned with global shipping decarbonization goals. Consequently, the region is attracting international partnerships aimed at supplying alternative marine fuels to key global trade corridors.

Latin America Green Shipping Market Trends

Latin America is gradually building green shipping momentum, supported by renewable energy resources and growing port modernization programs. Brazil and Mexico are expanding their logistics infrastructure with increasing sustainability considerations. Moreover, rising corporate sustainability standards among export-oriented industries such as agriculture and mining are beginning to drive demand for low-emission freight solutions across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

FedEx Corporation is a global logistics leader actively advancing its sustainability agenda within the green shipping market. The company has committed to achieving carbon-neutral operations by 2040 and is investing in electric delivery vehicles and sustainable aviation fuel programs. Moreover, FedEx is integrating renewable energy across its facilities and expanding low-emission freight solutions for corporate customers.

DSV is one of the world’s largest transport and logistics providers, with a growing commitment to green freight services. The company is expanding its sustainable logistics offerings through investments in low-emission road transport and carbon-neutral air freight options. Furthermore, DSV actively partners with customers to develop science-based emissions reduction targets across complex, multi-modal global supply chains.

GEODIS is positioning itself as a sustainability-focused logistics partner through its commitment to reducing the environmental impact of freight operations. The company has set ambitious targets to cut its carbon emissions intensity significantly by 2030. Additionally, GEODIS is deploying electric and hydrogen-powered vehicles, investing in eco-efficient warehouses, and developing green supply chain solutions for global clients.

Deutsche Post DHL Group is one of the most active participants in the global green shipping transition. The group has pledged to achieve net-zero logistics emissions by 2050 and is investing billions in sustainable aviation fuels, electric vehicles, and green facilities. Consequently, DHL’s GoGreen Plus service allows customers to directly support decarbonization through investment in sustainable fuel and technology programs.

Key Players

- FedEx Corporation

- DSV

- GEODIS

- Deutsche Post DHL Group

- YUSEN LOGISTICS CO., LTD.

- Bolloré SE

- CEVA Logistics

- XPO Logistics, Inc.

- United Parcel Service of America, Inc.

- ARK India

Recent Developments

- February 2026 – Hapag-Lloyd agreed to acquire ZIM Integrated Shipping for approximately $4.2 billion, marking one of the largest consolidation moves in the maritime industry. This acquisition is expected to strengthen Hapag-Lloyd’s fleet capacity and accelerate its positioning within the evolving green shipping landscape.

- January 2026 – V.Group acquired maritime fuel efficiency and decarbonisation partner Njord, expanding its technical management and green advisory capabilities. This move reflects growing industry demand for specialized decarbonization expertise and fuel optimization services across commercial shipping fleets.

- August 2025 – HD KSOE acquired Doosan Vina for $207.5 million as part of a strategic push into green shipbuilding. The acquisition strengthens HD KSOE’s production capacity for eco-friendly vessels powered by alternative fuels including LNG and ammonia-ready technologies.

- January 2025 – Pherousa fully acquired and integrated the previously independent company Pherousa Green Shipping AS, consolidating its green maritime operations under a unified corporate structure. This integration supports Pherousa’s broader strategy to scale its sustainable shipping solutions and expand service offerings to global clients.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 23.1 Billion |

| Forecast Revenue (2035) | USD 121.9 Billion |

| CAGR (2026-2035) | 18.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Service Type (Transportation, Value Added Services, Warehousing, Distribution, Reverse Logistics, Packaging), By Mode of Operation (Seaways Distribution, Storage, Roadways Distribution, Airways Distribution, Railways Distribution), By End Use (Manufacturing, Healthcare, Automotive, Banking and Financial Services, Retail and E-Commerce, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | FedEx Corporation, DSV, GEODIS, Deutsche Post DHL Group, YUSEN LOGISTICS CO., LTD., Bolloré SE, CEVA Logistics, XPO Logistics, Inc., United Parcel Service of America, Inc., ARK India |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |