Quick Navigation

- Report Overview

- Key Takeaways

- North America White Box Server Market

- Type Analysis

- Operating System Analysis

- Processor Analysis

- Business Type Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Top Opportunities Awaiting for Players

- Recent Developments

- Report Scope

Report Overview

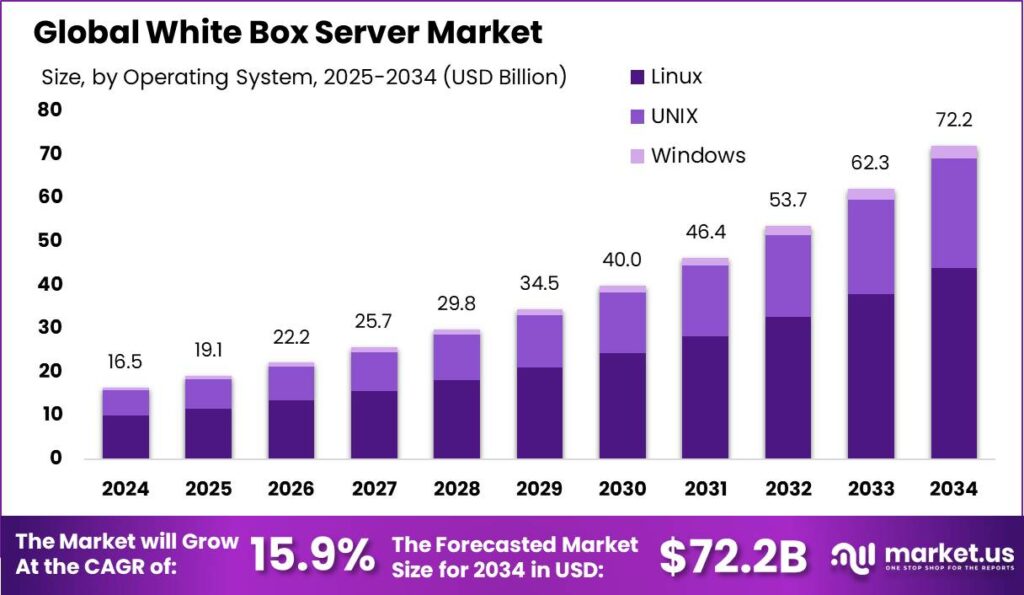

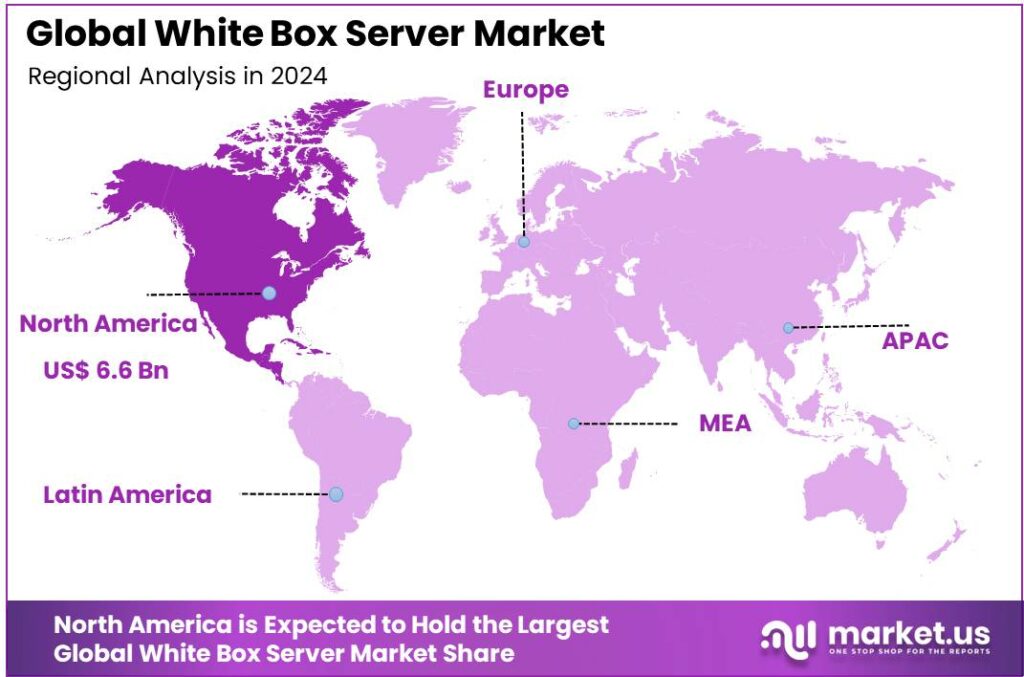

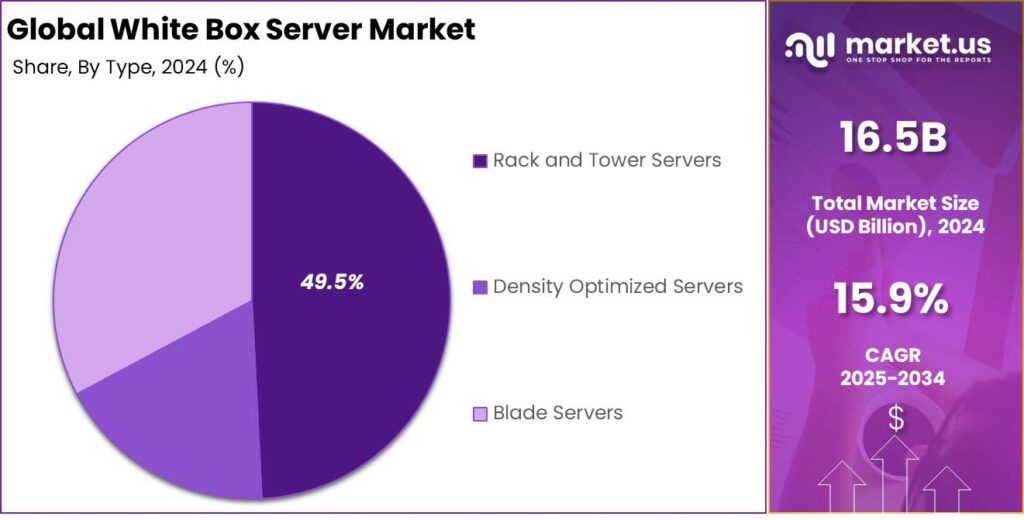

The Global White Box Server Market size is expected to be worth around USD 72.2 Billion By 2034, from USD 16.5 Billion in 2024, growing at a CAGR of 15.90% during the forecast period from 2025 to 2034. In 2024, North America captured the largest share of the white box server market, holding 40.1%, and generating USD 6.6 billion in revenues.

A white box server is a data center computer that is assembled from readily available hardware components, often without a well-known brand name associated with it. These servers are typically built by assembling generic parts that are widely available, allowing for a more cost-effective solution compared to servers from established brands like Dell or HP.

The white box server market has gained significant traction as it offers organizations the flexibility to customize hardware to meet specific performance needs while potentially reducing costs. This market caters to various industries, including cloud service providers, large enterprises, and small to mid-sized businesses, offering tailored solutions to meet diverse data processing needs.

The growth of the white box server market is driven by key factors, including the rising demand for cost-effective solutions in data centers, as white box servers are often cheaper than branded ones. Additionally, the rise of cloud computing and the expansion of data centers by cloud service providers fuel the need for these customizable servers, which can be tailored to specific tasks or operational needs.

Emerging trends in the white box server market include the integration of eco-friendly and energy-efficient technologies. Innovations such as advanced cooling systems, energy-saving processors, and greener materials are becoming prevalent. Additionally, the adoption of open-source hardware and software platforms is accelerating, enabling greater customization and flexibility.

Adoption rates for white box servers are increasing, particularly in data centers driven by the need for customizable, scalable, and cost-effective computing resources. These servers are particularly popular among tech giants like Google and Facebook, who utilize them to reduce costs while maintaining flexibility in their operations. The flexibility to customize and scale makes white box servers ideal for businesses looking to adapt quickly to changing technological needs.

The evolving nature of the white box server market presents numerous investment opportunities, particularly in innovations that reduce costs and enhance server performance and reliability. Investors can look into companies that are leading in product innovations and those expanding their reach in regions like Asia-Pacific, which is projected to be the fastest-growing region in this market segment.

Key Takeaways

- The Global White Box Server Market size is expected to reach USD 72.2 Billion by 2034, up from USD 16.5 Billion in 2024, growing at a CAGR of 15.90% during the forecast period from 2025 to 2034.

- In 2024, the Rack and Tower Servers segment dominated the white box server market, capturing more than 49.5% of the market share.

- The Linux segment held a dominant position in the white box server market in 2024, accounting for more than 61.0% of the market share.

- The X86 Servers segment held a leading position in 2024, capturing more than 68.4% of the white box server market.

- In 2024, the Data Centers segment led the white box server market, holding more than 63.9% of the market share.

- In 2024, North America held the largest market share in the white box server market, with a 40.1% share, generating revenues of USD 6.6 billion.

North America White Box Server Market

In 2024, North America held a dominant market position in the white box server market, capturing more than a 40.1% share, with revenues amounting to USD 6.6 billion. This market share is driven by strong technological infrastructure and high adoption of advanced computing in sectors like IT, telecommunications, and finance.

The demand in North America is further driven by the increasing need for cost-effective and customizable server solutions among small and medium-sized enterprises (SMEs). White box servers offer these organizations the flexibility to tailor hardware to their specific requirements, often at a lower cost than branded servers.

Moreover, the growing trend towards cloud computing and virtualization in North America has played a crucial role in the expansion of the white box server market. As businesses migrate to cloud-based solutions, the demand for scalable and efficient data center technologies rises, thereby boosting the deployment of white box servers.

Europe’s growth in the white box server market is driven by data privacy regulations like GDPR. APAC is expanding rapidly due to IT services and data center growth, especially in China and India. Latin America and the Middle East are emerging markets, fueled by digital transformation and the need for improved data center efficiency.

Type Analysis

In 2024, the Rack and Tower Servers segment held a dominant market position within the white box server market, capturing more than a 49.5% share. This segment benefits significantly from its versatility and scalability, which are crucial for businesses expanding their data centers or updating their IT infrastructure.

The leadership of the Rack and Tower Servers segment can be attributed to their cost-effectiveness and ease of deployment. These servers are designed to be straightforward in both setup and maintenance, making them an attractive option for companies looking to minimize IT complexity and reduce overhead costs.

Furthermore, the Rack and Tower Servers segment leads due to its adaptability in integrating with existing technologies and infrastructures. This capability is particularly important in an era where companies are seeking to protect their IT investments by ensuring longevity and compatibility with future technologies.

Innovations in energy efficiency and cooling technologies in Rack and Tower Servers have bolstered their market leadership. As energy costs rise and environmental regulations tighten, these servers’ efficiency and sustainability appeal drive adoption, reinforcing their dominance.

Operating System Analysis

In 2024, the Linux segment held a dominant market position in the white box server market, capturing more than a 61.0% share. This leading position can be attributed to Linux’s open-source nature, which allows for extensive customization and flexibility, key attributes that are highly valued in the server environment.

Linux’s compatibility with diverse hardware and software makes it ideal for white box servers, which are built from varied components. This flexibility allows organizations to optimize their IT infrastructure with customized solutions, avoiding dependence on a single vendor’s ecosystem.

Linux servers are known for their stability and reliability, crucial for managing large complex data center operations. Their ability to handle multiple tasks with minimal downtime is a key advantage, especially for data-intensive sectors like technology and finance.

The adoption of cloud technologies and virtualized environments has driven growth in the Linux market. Linux-based white box servers are key to private and hybrid cloud solutions, offering efficiency and open standards, making them a preferred choice for companies seeking a competitive edge.

Processor Analysis

In 2024, the X86 Servers segment held a dominant position in the white box server market, capturing more than a 68.4% share. This leadership is primarily attributed to the compatibility of X86 servers with a wide range of operating systems and software applications, making them a preferred choice for many businesses.

The architecture is widely supported by major software developers, which simplifies integration and operation in diverse IT environments. This universal compatibility ensures that X86 servers continue to be the cornerstone of enterprise and cloud computing environments.

The dominance of X86 servers is also driven by their cost-effectiveness, offering a balance of performance and affordability. Their scalable options allow small and medium-sized businesses to invest in robust server solutions without significant financial strain.

Furthermore, the X86 Servers segment benefits from a vast ecosystem of developers and a strong community that continually drives innovation and improvements in this architecture. Regular updates and enhancements in X86 server technology boost their efficiency and functionality, making them highly attractive for companies looking to leverage the latest technologies.

Business Type Analysis

In 2024, the Data Centers segment held a dominant position in the White Box Server market, capturing more than 63.9% of the market share. This significant lead can be attributed primarily to the increasing demand for cost-effective and highly customizable server solutions within data centers.

As businesses seek more flexibility in their IT infrastructure, white box servers offer a strong alternative to branded ones. They provide customization to optimize operations, reduce costs, and enhance scalability, making them especially beneficial for data centers aiming to expand efficiently.

The adoption of white box servers in data centers is fueled by the rise of software-defined data centers (SDDCs), which prioritize scalability and agility. The modular nature of white box servers allows for flexible configuration and reconfiguration, making them ideal for the dynamic needs of SDDCs.

Advancements in networking and storage have boosted the Data Centers segment. With the rise of big data, IoT, and AI, data centers need servers that can efficiently handle vast data. White box servers, known for high performance and cost-effectiveness, are the preferred choice for these intensive tasks.

Key Market Segments

By Type

- Rack and Tower Servers

- Density Optimized Servers

- Blade Servers

By Operating System

- UNIX

- Windows

- Linux

By Processor

- X86 Servers

- Non-X86 Servers

By Business Type

- Enterprise Customers

- Data Centers

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Maximizing cost-effectiveness.

White box servers are gaining traction primarily due to their cost-effectiveness. Unlike branded servers, these are built using off-the-shelf components, eliminating brand premiums. This approach allows businesses to acquire high-performance servers at a fraction of the cost. For large-scale data centers and enterprises, this translates to significant savings in capital expenditures.

Moreover, the ability to customize hardware to specific needs ensures that companies pay only for the features they require, further optimizing their investments. This financial advantage is a key factor driving the widespread adoption of white box servers across various industries.

Restraint

Restricted support and ongoing maintenance.

A notable challenge with white box servers is the limited support and maintenance options. Unlike established brands that offer comprehensive service packages, white box servers often lack dedicated support teams. This absence can lead to difficulties in troubleshooting and prolonged downtimes during hardware failures.

Businesses may need to invest in in-house IT expertise or rely on third-party service providers, potentially increasing operational costs and complexity. This limitation makes some organizations hesitant to transition from traditional branded servers to white box solutions.

Opportunity

The emergence of hyperscale data centers.

The increasing establishment of hyperscale data centers presents a significant opportunity for the white box server market. These large-scale facilities, operated by tech giants and cloud service providers, demand scalable and cost-effective hardware solutions.

White box servers, with their customizable configurations and affordability, are well-suited to meet these requirements. As the demand for cloud services, big data analytics, and large-scale storage solutions grows, the adoption of white box servers in hyperscale data centers is expected to surge, offering substantial market growth potential.

Challenge

Concerns over perception and trust.

Despite their advantages, white box servers often face skepticism regarding their quality and reliability. The absence of a recognized brand name leads to concerns about performance consistency and product lifespan. Additionally, potential buyers may doubt the availability of timely support and warranty services.

Overcoming these perceptions requires educating the market about the rigorous standards many white box manufacturers adhere to and showcasing successful deployment case studies. Building trust is essential for broader acceptance and growth in markets traditionally dominated by established server brands.

Emerging Trends

White box servers are becoming popular for their flexibility and cost-effectiveness. Unlike branded servers, these unbranded systems offer customization, allowing businesses to choose components that optimize performance for specific workloads. This makes them a great choice for companies with unique requirements.

The growth of hyper-converged infrastructure (HCI), which integrates computing, storage, and networking, has increased demand for white box servers. Their flexibility makes them perfect for HCI setups, allowing businesses to create scalable infrastructures that can easily adapt to evolving technological needs.

The rise of open-source platforms like the Open Compute Project and the growth of edge computing have fueled the popularity of white box servers. These platforms promote customizable, cost-effective hardware, while edge computing demands versatile servers that can be deployed in various locations—traits that white box servers excel in.

Business Benefits

From a business perspective, white box servers offer several advantages. One of the most significant benefits is cost savings. By choosing only the components they need, businesses can avoid the markups often associated with pre-configured solutions, allowing for more strategic allocation of IT budgets.

Flexibility and customization are other key benefits. Businesses have the freedom to select components that precisely match their unique requirements, optimizing performance and efficiency. This level of customization ensures that the server infrastructure aligns perfectly with the company’s evolving needs.

Moreover, deploying white box servers can lead to faster implementation times. By utilizing readily available components and streamlined assembly processes, businesses can expedite the setup and integration of their servers, minimizing downtime and accelerating time-to-value.

Key Player Analysis

Key players in White Box Server Market are making significant strides to capitalize on these trends by offering flexible, scalable, and high-quality products.

Quanta Computer Inc. is a global leader in providing white box server solutions, recognized for its cutting-edge design and manufacturing capabilities. The company specializes in producing high-performance servers that meet the needs of large-scale data centers, cloud providers, and telecom companies.

Celestica Inc. is another key player in the white box server market, known for its advanced technological capabilities and deep expertise in supply chain management. The company focuses on providing tailored server solutions that cater to the diverse needs of businesses in sectors like telecommunications, cloud computing, and artificial intelligence.

Super Micro Computer, Inc. has established itself as a prominent force in the white box server market by offering a wide range of high-performance, energy-efficient servers. Known for its product flexibility and commitment to customer-specific requirements, Super Micro is highly regarded in industries such as cloud computing, enterprise IT, and scientific computing.

Top Key Players in the Market

- Quanta Computer Inc.

- Celestica Inc.

- Super Micro Computer, Inc.

- Inventec Corporation

- PEGATRON Corporation

- Penguin Solutions

- Hyve Solutions

- GIGA-BYTE Technology Co., Ltd.

- MiTAC Computing Technology Corporation

- Other Key Players

Top Opportunities Awaiting for Players

- Data Center Expansion: The increasing number of data centers worldwide is a major driver of growth in the White Box Server market. These facilities require robust server solutions that White Box Servers can provide, due to their cost-effectiveness and customization capabilities.

- Rising Cybersecurity Needs: As cyber threats continue to evolve, organizations are looking for more secure and customizable server solutions. White Box Servers allow for tailored security configurations, offering businesses the ability to enhance their defenses against cyberattacks.

- High Performance Requirements for AI and IoT: There is a growing demand for high-performance computing platforms due to the rise of AI and IoT applications. White Box Servers, known for their ability to be customized with high-performance components, are ideally suited to meet these demands, especially with recent innovations like liquid-cooled systems and advanced processing capabilities.

- Adoption of Open Architecture and Customization: There is a trend towards open architecture and customization in server solutions. White box servers, with their open designs, allow businesses to tailor hardware to their specific requirements, leading to better performance and cost efficiency. This trend is expected to continue, providing growth opportunities for companies offering customizable server solutions.

- Growth in Emerging Markets: Emerging markets, particularly in Asia-Pacific, are experiencing rapid digital transformation. The demand for affordable and customizable server solutions in these regions is increasing, presenting significant opportunities for white box server companies to expand their presence and cater to these growing markets.

Recent Developments

- In September 2024, a recent Dell’Oro Group report highlights a 46% growth in global data center capex for accelerated servers in Q2 2024. Additionally, the general-purpose server and storage system markets are recovering, with major OEMs seeing growth in both revenue and units year-to-date.

- In April 2024, Supermicro launched its X14 server portfolio, integrating support for Intel’s Xeon 6 processors. This product line focuses on rack plug-and-play capabilities and advanced liquid cooling solutions to meet diverse workload needs.

- In January 2024, Intel unveiled its 5th Gen Xeon processors (Emerald Rapids), offering improved performance per watt and reduced total cost of ownership for AI, HPC, and other applications. These processors maintain compatibility with previous generations, enabling seamless upgrades.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 16.5 Bn |

| Forecast Revenue (2034) | USD 72.2 Bn |

| CAGR (2025-2034) | 15.9% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Rack and Tower Servers, Density Optimized Servers, Blade Servers), By Operating System (UNIX, Windows, Linux), By Processor (X86 Servers, Non-X86 Servers), By Business Type (Enterprise Customers, Data Centers) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Quanta Computer Inc., Celestica Inc., Super Micro Computer, Inc., Inventec Corporation, PEGATRON Corporation, Penguin Solutions, Hyve Solutions, GIGA-BYTE Technology Co., Ltd., MiTAC Computing Technology Corporation, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |