Quick Navigation

Report Overview

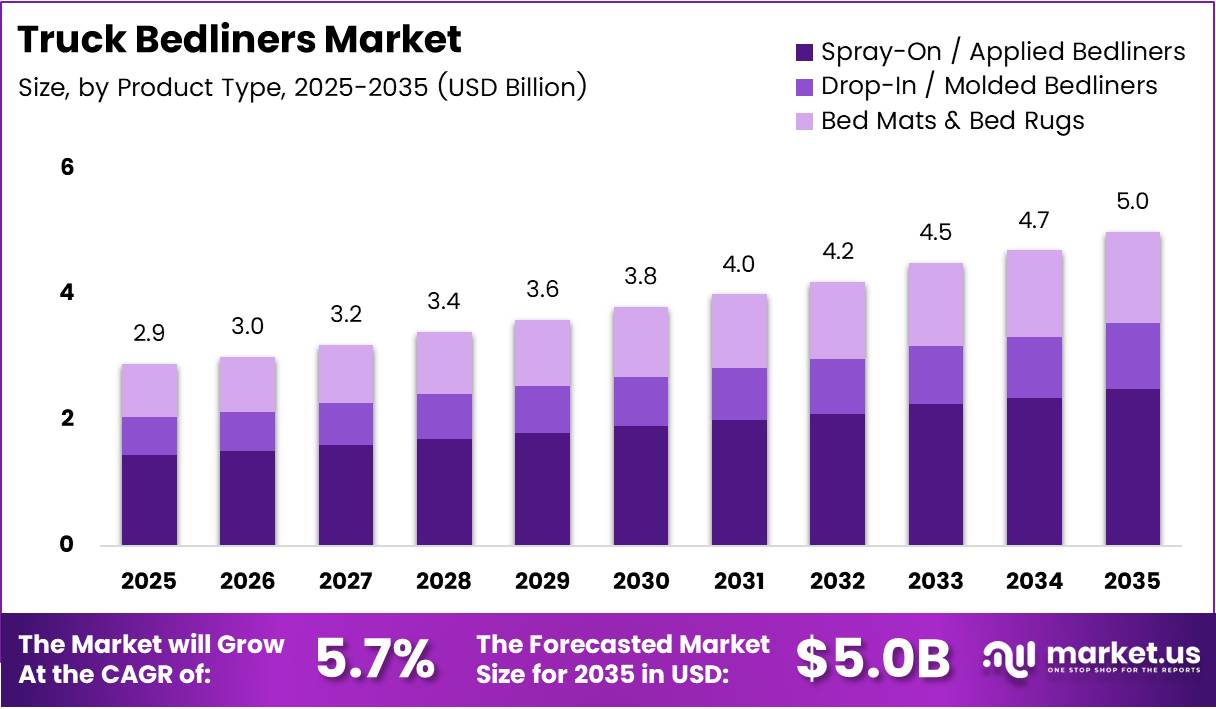

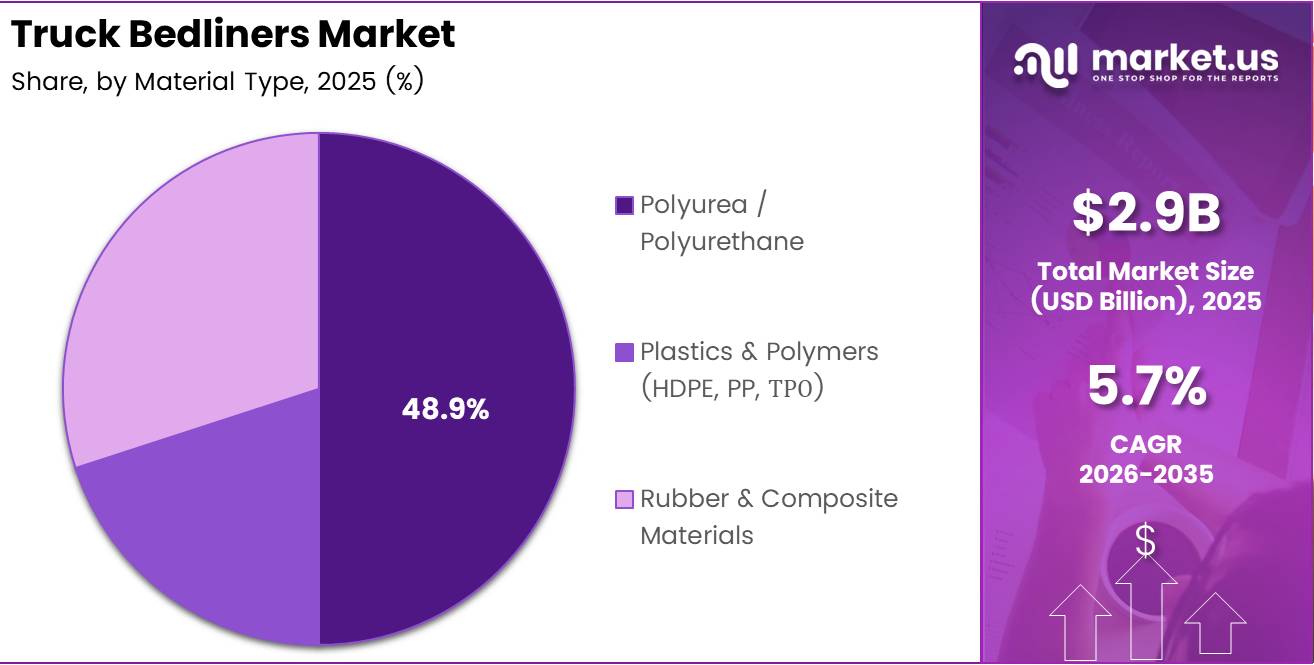

Global Truck Bedliners Market size is expected to be worth around USD 5.0 Billion by 2035 from USD 2.9 Billion in 2025, growing at a CAGR of 5.7% during the forecast period 2026 to 2035.

Truck bedliners protect cargo bed surfaces from impact, corrosion, abrasion, and chemical exposure. Pickup trucks carry heavy loads across construction sites, farms, and logistics operations. Without bed protection, metal surfaces corrode within years and resale values fall sharply. Bedliners solve this directly, making them a near-mandatory accessory for working truck operators.

The aftermarket segment drives the majority of revenue. Truck owners purchase bedliners independently, well after the original vehicle sale. This creates a recurring purchase cycle tied to vehicle ownership rates, not new truck production. Consequently, the market holds steady even when new truck sales slow temporarily.

Spray-on polyurea and polyurethane coatings hold the top position among product types. These materials bond chemically to the truck bed surface, creating a seamless protective layer that drop-in plastic alternatives cannot match. Professional installation through authorized service centers builds a recurring service revenue model for franchised applicator networks.

Government fleet procurement and defense vehicle maintenance programs add institutional demand. Fleet managers prioritize corrosion prevention because bed replacement costs far exceed protective coating costs. This cost-avoidance logic keeps commercial and government buyers returning to spray-on solutions across multi-vehicle contracts.

In July 2024, RealTruck acquired Protex, a web-based 3D product configuration and augmented reality platform, to strengthen visualization tools for truck accessory buyers. This signals a shift toward digital-first purchasing in the truck accessories segment, compressing the distance between consumer intent and purchase conversion.

According to Burtin technical data, the System 14 spray-on bedliner coating delivers theoretical coverage of 1,600 sq. ft. per drum set at 100 mil dry film thickness. This coverage efficiency directly reduces material waste per vehicle, improving installer margins and making professional spray services more cost-competitive against DIY alternatives.

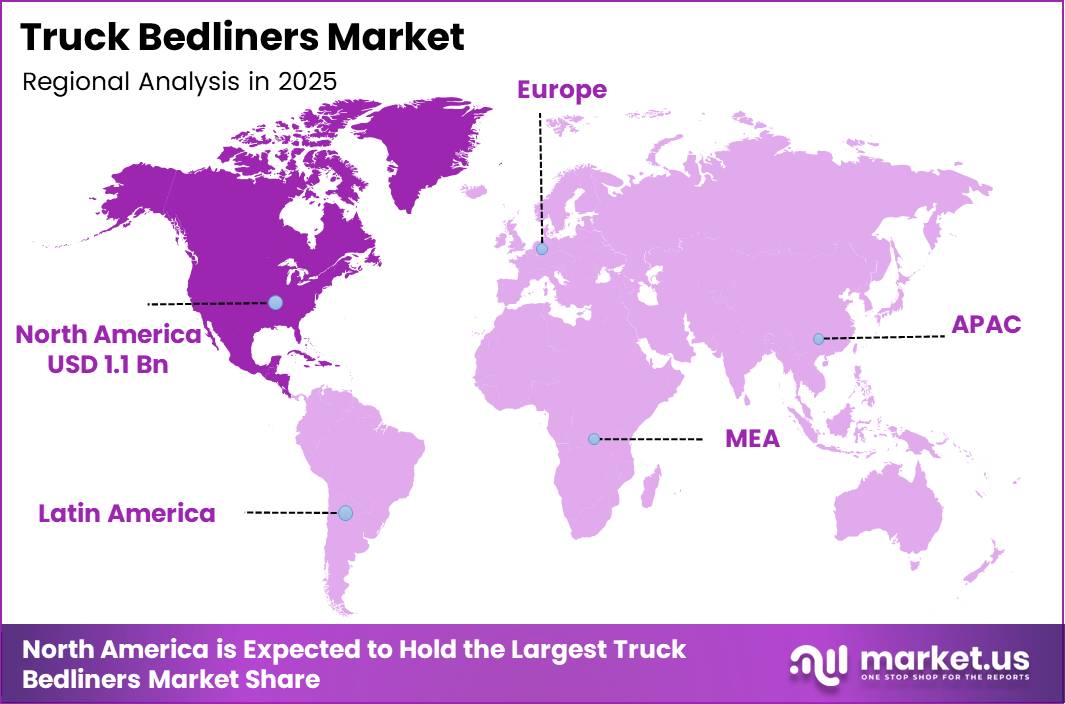

North America accounts for 38.80% of global truck bedliner revenue, valued at USD 1.1 Billion in 2025. This dominance reflects the region’s exceptionally high pickup truck ownership rates and a deeply established aftermarket accessories culture that consistently converts truck buyers into bedliner buyers.

Key Takeaways

- The global Truck Bedliners Market is valued at USD 2.9 Billion in 2025 and will reach USD 5.0 Billion by 2035.

- The market grows at a CAGR of 5.7% from 2026 to 2035.

- By Product Type, Spray-On / Applied Bedliners lead with a 48.9% share in 2025.

- By Truck Type, Light-Duty Pickup Trucks dominate with a 74.2% share in 2025.

- By Material Type, Polyurea / Polyurethane holds a 49.3% share in 2025.

- By Application, the Aftermarket segment leads with a 69.5% share in 2025.

- North America dominates regional revenue at 38.80%, valued at USD 1.1 Billion in 2025.

Product Type Analysis

Spray-On / Applied Bedliners dominate with 48.9% due to superior adhesion and corrosion resistance.

In 2025, Spray-On / Applied Bedliners held a dominant market position in the By Product Type segment of the Truck Bedliners Market, with a 48.9% share. Spray-on coatings bond chemically to the truck bed, eliminating gaps where moisture and debris collect. This performance advantage over plastic alternatives drives both consumer preference and professional installer revenue across commercial fleet contracts.

Drop-In / Molded Bedliners serve buyers who prioritize easy removal and reinstallation. These units suit users who carry diverse cargo types and need flexible access to the truck bed floor. However, moisture trapping beneath the liner remains a well-documented limitation, gradually shifting quality-conscious buyers toward permanent spray-on solutions.

Bed Mats & Bed Rugs address entry-level protection needs and seasonal use cases. Buyers in light-use segments choose these for affordability and simple installation. This sub-segment performs strongest in the residential and recreational vehicle owner category, where cargo loads are lighter and protection requirements are less demanding.

Truck Type Analysis

Light-Duty Pickup Trucks dominate with 74.2% due to high consumer ownership and aftermarket activity.

In 2025, Light-Duty Pickup Trucks held a dominant market position in the By Truck Type segment of the Truck Bedliners Market, with a 74.2% share. This segment benefits from the sheer volume of light-duty pickups registered across North America and global markets. High ownership rates translate directly into a large addressable aftermarket pool that bedliner manufacturers and installers actively serve.

Medium-Duty Pickup Trucks represent a smaller but commercially intensive buyer base. Fleet operators in construction, utilities, and logistics prioritize these vehicles for heavy haul tasks. Bedliner installations on medium-duty platforms typically involve higher-specification spray coatings, creating above-average revenue per unit for professional installers.

Material Type Analysis

Polyurea / Polyurethane dominates with 49.3% due to chemical bonding strength and rapid cure times.

In 2025, Polyurea / Polyurethane held a dominant market position in the By Material Type segment of the Truck Bedliners Market, with a 49.3% share. These materials cure within seconds of application and achieve tensile strength levels that rubber and plastic alternatives cannot match. Fleet operators and professional users specify polyurea coatings for applications where protection failure carries direct financial consequences.

Plastics & Polymers (HDPE, PP, TPO) serve the drop-in and molded bedliner segment. These materials offer cost-effective protection for moderate-use scenarios. Manufacturers continue improving polymer formulations to reduce weight and improve UV stability, narrowing the performance gap against premium spray-on materials in non-critical applications.

Rubber & Composite Materials occupy a niche position in heavy-duty and specialty use cases. Construction fleets and agricultural operators value rubber’s shock-absorption properties for protecting cargo and the truck bed simultaneously. However, rubber’s higher installation weight and cost limit broader adoption across the general pickup truck market.

Application Analysis

Aftermarket dominates with 69.5% due to post-purchase installation behavior and DIY demand.

In 2025, the Aftermarket segment held a dominant market position in the By Application segment of the Truck Bedliners Market, with a 69.5% share. Truck owners consistently opt to install bedliners after purchase rather than at the point of sale. This behavior sustains a large and predictable aftermarket revenue base that remains relatively insulated from new vehicle sales cycles.

OEM installations represent factory-fitted or dealer-installed bedliner solutions integrated at the point of vehicle production or delivery. Electric pickup truck platforms entering production from 2024 onward are creating new OEM bedliner integration contracts, as manufacturers seek to offer complete protection packages at the point of sale to justify premium pricing.

Key Market Segments

By Product Type

- Spray-On / Applied Bedliners

- Drop-In / Molded Bedliners

- Bed Mats & Bed Rugs

By Truck Type

- Light-Duty Pickup Trucks

- Medium-Duty Pickup Trucks

By Material Type

- Polyurea / Polyurethane

- Plastics & Polymers (HDPE, PP, TPO)

- Rubber & Composite Materials

By Application

- Aftermarket

- OEM

Drivers

Pickup Truck Sales Growth and DIY Customization Culture Expand Bedliner Demand Across Commercial and Consumer Segments

Pickup truck registrations continue rising across North America, Latin America, and Southeast Asia. Commercial operators in construction and logistics actively add utility vehicles to their fleets, and each new truck represents a near-immediate bedliner purchase opportunity. The aftermarket’s 69.5% application share confirms that buyers consistently act on this need after vehicle acquisition.

DIY vehicle customization has moved from niche hobbyist behavior into mainstream truck ownership culture. Consumers now treat bedliner selection as part of the truck ownership identity. This behavioral shift expands the addressable buyer base beyond commercial users, pulling residential and recreational truck owners into the market at a consistent rate.

In September 2024, LINE-X expanded its authorized installer network and introduced enhanced spray-on coating formulations. This move directly addresses installer capacity constraints, which have historically limited volume in high-demand metro markets. According to Burtin technical data, the System 14 spray coating achieves a minimum tensile strength of 2,600 psi and minimum elongation of 230%, demonstrating the material performance standard that professional installer networks now compete on when acquiring commercial fleet contracts.

Restraints

Raw Material Price Volatility and Counterfeit Products Compress Margins for Established Bedliner Manufacturers

Polyurethane and rubber feedstock prices fluctuate with petrochemical market cycles. When input costs rise sharply, manufacturers face a difficult choice between absorbing the cost or passing it to consumers. Neither option is clean. Price increases risk losing price-sensitive buyers to lower-grade alternatives, while margin compression limits investment in product development.

According to Oak Ridge technical data, the OR93BL polyurethane-urea hybrid bedliner records a Taber abrasion loss of 95 mg per 1,000 cycles at Shore D hardness of 50. This performance benchmark matters because counterfeit products consistently fail to reach it, yet buyers without technical knowledge cannot differentiate at the point of sale. Established manufacturers lose revenue to inferior substitutes without visible quality differentiation in the retail environment.

Low-cost counterfeit bedliner products undercut pricing from established brands without meeting material performance standards. Distributors in unregulated secondary markets carry these products alongside legitimate alternatives. The resulting margin erosion forces premium manufacturers to invest in brand authentication and installer certification programs, adding cost without generating direct revenue.

Growth Factors

Fleet Management Adoption, EV Truck Production, and Lightweight Material Development Create New Revenue Streams

Fleet management companies are standardizing spray-on bedliner specifications across entire vehicle pools. A single corporate fleet contract covering hundreds of trucks delivers installation volume that individual retail sales cannot match. This commercial adoption pattern creates predictable, high-value revenue for authorized applicator networks and coating manufacturers with fleet-grade product certifications.

Electric pickup trucks entering production from manufacturers including Ford and Rivian require OEM bedliner solutions designed for their specific platform dimensions and load characteristics. In October 2024, Rhino Linings showcased its advanced spray-on formula at the SEMA Show through off-road racing vehicle applications, demonstrating the durability performance needed to win OEM specification contracts. According to Oak Ridge technical data, the OR93BL formulation delivers tensile strength of 5,630 psi and elongation of 140%, setting a material benchmark directly relevant to electric truck platform requirements.

Development of lightweight composite bedliner materials targets the fuel efficiency sensitivity of both conventional and electric pickup trucks. Reducing bedliner weight improves vehicle range and payload ratings simultaneously. Manufacturers that resolve this weight-performance trade-off first will hold a durable specification advantage in OEM contracts where vehicle weight budgets are tightly managed.

Emerging Trends

Custom Finishes, Antimicrobial Coatings, and Mobile Application Services Redefine the Bedliner Customer Experience

Custom-colored and textured bedliner finishes are shifting truck protection from a utility purchase into a vehicle personalization decision. Buyers now select coating colors to match or contrast vehicle paint, treating the truck bed as a visible design element. This premiumization trend allows installers to charge above-standard pricing for custom finish work, improving per-vehicle revenue.

Antimicrobial and easy-clean coating technologies address the food transport, agricultural, and healthcare fleet segments where hygiene compliance carries regulatory weight. According to RAPTOR technical data, the 2K bedliner coating achieves a dry film thickness of approximately 230μ (9.0 mils) in a single coat, providing a smooth, cleanable surface that industrial users require. This specification makes spray-on bedliners directly relevant to commercial hygiene applications previously underserved by the market.

Mobile on-site spray bedliner application services remove the requirement for fleet operators to transport vehicles to a fixed installation facility. Service providers bring professional spray equipment directly to fleet yards, cutting downtime per vehicle. This delivery model unlocks large-volume commercial contracts that fixed-location installers could not previously serve efficiently.

Regional Analysis

North America Dominates the Truck Bedliners Market with a Market Share of 38.80%, Valued at USD 1.1 Billion

North America holds 38.80% of global truck bedliner revenue at USD 1.1 Billion in 2025. The United States leads this position through the highest per-capita pickup truck ownership rate of any major economy. Deep aftermarket culture, a dense authorized installer network, and commercial fleet upgrade cycles sustain consistent annual demand across both consumer and industrial buyer segments.

Europe Truck Bedliners Market Trends

Europe’s truck bedliner market develops through commercial vehicle fleet procurement and tightening corrosion standards in logistics operations. Regulatory requirements around cargo containment and vehicle maintenance push fleet operators toward premium protective coatings. Spray-on polyurethane solutions align with European preferences for durable, low-maintenance surface treatments across industrial and agricultural vehicle applications.

Asia Pacific Truck Bedliners Market Trends

Asia Pacific posts the fastest volume growth among all regions, driven by rising pickup truck sales in Thailand, Australia, and India. Construction and infrastructure activity across Southeast Asia increases utility vehicle utilization rates, accelerating demand for cargo bed protection. Australian agricultural operators represent a particularly active buyer segment given the harsh operating environments and high vehicle investment values.

Latin America Truck Bedliners Market Trends

Latin America’s truck bedliner adoption is closely tied to agricultural and mining sector activity in Brazil and Mexico. These industries operate large pickup truck fleets under severe abrasion and chemical exposure conditions. Spray-on coating installations on commercial fleets represent the primary revenue source, with the aftermarket channel handling the majority of vehicle throughput.

Middle East & Africa Truck Bedliners Market Trends

The Middle East and Africa region presents demand driven by extreme heat, UV exposure, and sandy operating environments that accelerate unprotected truck bed deterioration. Oil and gas sector fleet operators in GCC countries specify corrosion-resistant and chemical-resistant bedliner coatings as standard maintenance items. South Africa’s mining industry adds further commercial fleet volume to the regional base.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

In January 2025, RealTruck entered a strategic agreement to acquire Vehicle Accessories Group (VAI), adding protective automotive accessories to its expanding portfolio. RealTruck’s acquisition strategy signals a deliberate move to consolidate the fragmented truck accessories aftermarket under one distribution platform. For competitors, this consolidation pressure is real. RealTruck’s scale advantages in distribution and brand ownership will make independent accessory positioning increasingly difficult without differentiated product performance.

LINE-X operates through a franchised installer network that creates geographic coverage advantages over product-only manufacturers. The company’s September 2024 network expansion and enhanced coating formulation launch reinforce two simultaneous competitive levers: installer capacity and product quality. For fleet buyers evaluating spray-on bedliner vendors, LINE-X’s network density reduces installation lead times, which is a direct procurement advantage over smaller regional operators.

Penda Corporation (Pendaliner) focuses on the drop-in and molded bedliner segment, serving buyers who prioritize removable protection over permanent coatings. This positioning captures a distinct buyer profile from spray-on specialists and avoids direct head-to-head competition on coating performance. However, the long-term structural shift toward spray-on solutions creates a strategic ceiling for molded liner specialists unless they expand their product range.

Rhino Linings Corporation uses high-visibility motorsport applications to validate its spray-on coating technology for commercial and consumer buyers. The October 2024 SEMA Show demonstration through off-road racing vehicles directly targeted the performance-conscious buyer segment that pays premiums for proven durability. This brand-building approach is particularly effective in the North American aftermarket where consumer trust in installer brand reputation directly influences purchasing decisions.

Key Players

- DualLiner

- LINE-X

- Penda Corporation (Pendaliner)

- Rhino Linings

- Rugged Liner

- Scorpion Protective Coatings

- SPEEDLINER

- Truck Hero (BedRug)

- Ultimate Linings

- Weather Tech

Recent Developments

- July 2025 – RealTruck announced the acquisition of Husky Liners, adding a leading floor and cargo liner manufacturer to its vehicle protection portfolio. This move broadens RealTruck’s product coverage across multiple truck accessory categories.

- January 2026 – LINE-X announced stronger partnership expansion and continued brand momentum following growth initiatives across 2025 in the truck bedliner market. The company reinforced its position as a leading authorized installer network in North America.

- 2026 – Ford Motor Company continued expanding its OEM truck protection accessory lineup with modular and molded bedliner solutions for 2024 to 2026 Ford F-150 and Ranger models. Ford emphasized compatibility with cargo management accessories and improved durability features.

- March 2025 – RealTruck completed the acquisition of Vehicle Accessories Group (VAI), broadening distribution for truck protection products and bedliner-related accessories through its global aftermarket network. This completion followed the January 2025 strategic agreement announcement.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.9 Billion |

| Forecast Revenue (2035) | USD 5.0 Billion |

| CAGR (2026-2035) | 5.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Spray-On / Applied Bedliners, Drop-In / Molded Bedliners, Bed Mats & Bed Rugs), By Truck Type (Light-Duty Pickup Trucks, Medium-Duty Pickup Trucks), By Material Type (Polyurea / Polyurethane, Plastics & Polymers (HDPE, PP, TPO), Rubber & Composite Materials), By Application (Aftermarket, OEM) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | DualLiner, LINE-X, Penda Corporation (Pendaliner), Rhino Linings, Rugged Liner, Scorpion Protective Coatings, SPEEDLINER, Truck Hero (BedRug), Ultimate Linings, Weather Tech |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |