Global Tara Gum Market Size, Share Analysis Report By Form (Powder, Liquid), By Application (Thickener, Stabilizer, Gelling Agent, Emulsifier), By End Use (Bakery, Dairy and Alternatives, Meat and Poultry, Beverages, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 181939

- Number of Pages: 199

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

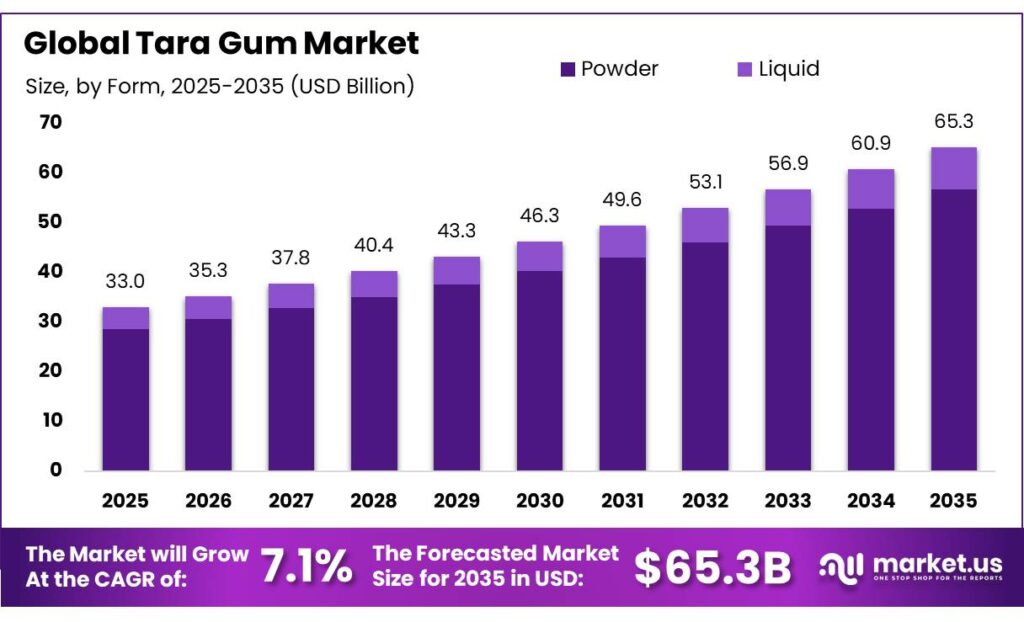

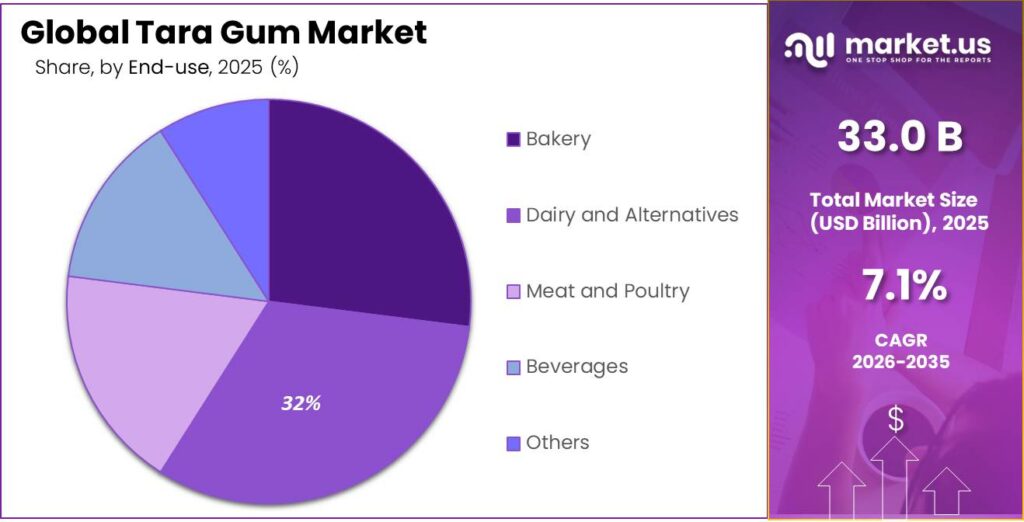

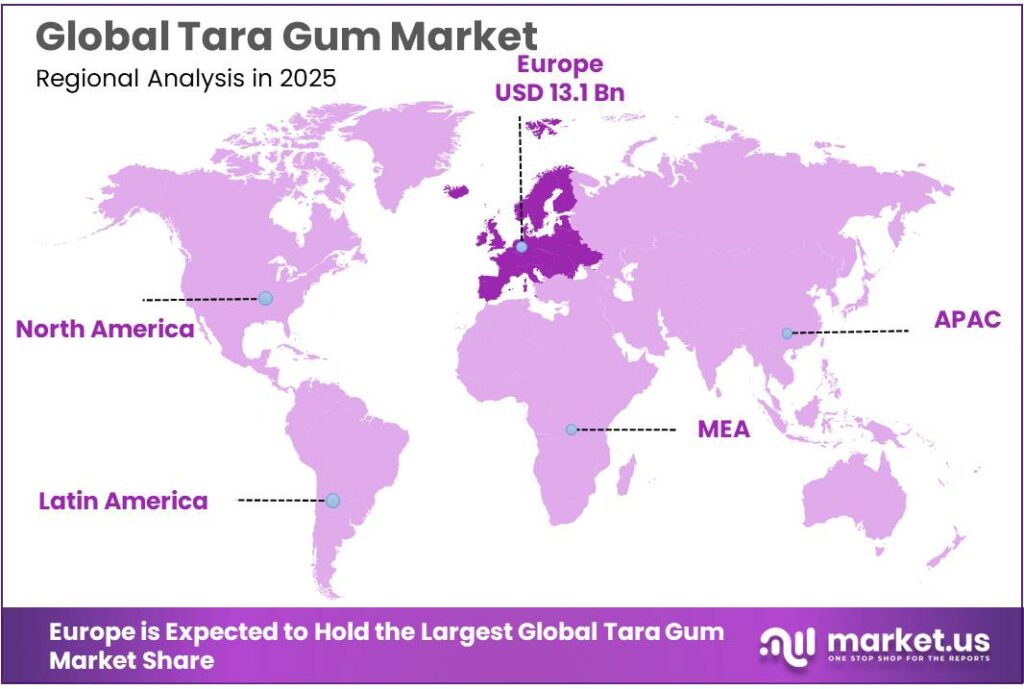

The Global Tara Gum Market size is expected to be worth around USD 65.3 Billion by 2035, from USD 33.0 Billion in 2025, growing at a CAGR of 7.1% during the forecast period from 2026 to 2035. In 2025, Europe held a dominant market position, capturing more than a 39.8% share, holding USD 13.1 Billion revenue.

Tara gum, commercially identified in the international food system as INS 417, is a plant-based hydrocolloid obtained from Caesalpinia spinosa and positioned as a natural thickener and stabilizer for food processing. From an industry standpoint, its relevance comes from its compatibility with clean-label formulation, viscosity management, and texture optimization across dairy, frozen desserts, bakery fillings, sauces, and selected plant-based products.

Its regulatory standing remains an important commercial support factor: the Joint FAO/WHO Expert Committee on Food Additives evaluated tara gum in 1986, while the Codex General Standard for Food Additives places it in Table 3, meaning it can be used in multiple food categories under good manufacturing practice conditions. This makes tara gum one of the recognized natural texturizing systems for formulators seeking functionality without moving toward synthetic texture aids.

The present industrial scenario is being shaped less by speculative market sizing and more by real food-production demand from end-use categories where hydrocolloids matter. In the United States, total cheese production reached 14.2 billion pounds in 2024, while regular ice cream output reached 886 million gallons and low-fat ice cream totaled 412 million gallons, indicating the scale of processed dairy and frozen applications where stabilizers and mouthfeel systems remain commercially relevant.

Key driving factors for the tara gum market include the accelerating demand for clean-label and plant-based food products, particularly in dairy alternatives, bakery, and processed foods. The Food and Agriculture Organization (FAO) and global trade data indicate rising imports of botanical hydrocolloids, with the European Union alone importing 32,034,600 kg of such derivatives in 2024

Tate & Lyle reported pro forma revenue of £2.1 billion and adjusted EBITDA of £446 million for fiscal 2025, and highlighted that the addition of CP Kelco expanded its portfolio in pectin, specialty gums, and other nature-based ingredients, signaling stronger competition and broader customer education around mouthfeel systems.

Key Takeaways

- Tara Gum Market size is expected to be worth around USD 65.3 Billion by 2035, from USD 33.0 Billion in 2025, growing at a CAGR of 7.1%.

- Powder held a dominant market position, capturing more than a 87.4% share.

- Thickener held a dominant market position, capturing more than a 41.7% share.

- Dairy and Alternatives held a dominant market position, capturing more than a 32.5% share.

- Europe held a dominant position in the tara gum market, accounting for 39.8% of the global share with a market value of USD 13.1 Bn.

By Form Analysis

Powder form leads strongly with 87.4% share due to ease of use and wide industrial adoption

In 2025, Powder held a dominant market position, capturing more than a 87.4% share. This strong presence is mainly because powdered tara gum is easier to handle, store, and incorporate into different formulations compared to other forms.

Food manufacturers prefer the powder form as it blends quickly in both hot and cold systems, making it highly suitable for products like dairy alternatives, sauces, bakery fillings, and processed foods. Its fine particle size ensures better dispersion and consistent texture, which is important for maintaining product quality at scale.

By Application Analysis

Thickener application leads with 41.7% share driven by strong demand in food processing

In 2025, Thickener held a dominant market position, capturing more than a 41.7% share. This leading position is mainly because tara gum is widely used to improve texture and consistency in a range of food products. It is commonly added to sauces, dressings, dairy alternatives, and bakery fillings where maintaining the right thickness is important for product quality.

Food manufacturers rely on tara gum as a thickening agent because it works efficiently even in small quantities and provides a smooth, stable texture without affecting taste. Its natural origin also supports its use in clean-label products, which is becoming increasingly important for consumers.

By End Use Analysis

Dairy and alternatives lead with 32.5% share supported by rising plant-based consumption

In 2025, Dairy and Alternatives held a dominant market position, capturing more than a 32.5% share. This leading share is mainly driven by the growing use of tara gum in dairy-based and plant-based products where texture and stability are critical. It is commonly used in ice creams, flavored milk, yogurt, and especially in plant-based drinks like almond, soy, and oat beverages.

Tara gum helps improve mouthfeel, prevents separation, and maintains consistency during storage, which makes it highly valuable for manufacturers. As consumers continue to look for better texture in dairy alternatives, the demand for effective natural stabilizers like tara gum has increased.

Key Market Segments

By Form

- Powder

- Liquid

By Application

- Thickener

- Stabilizer

- Gelling Agent

- Emulsifier

By End Use

- Bakery

- Dairy and Alternatives

- Meat and Poultry

- Beverages

- Others

Emerging Trends

Blending of Hydrocolloids Becoming a Key Trend in Food Formulation

A clear and growing trend in the tara gum market is the increasing use of blended hydrocolloid systems instead of relying on a single ingredient. Food manufacturers are no longer using tara gum alone; instead, they are combining it with other gums like guar gum or locust bean gum to achieve better texture, stability, and cost efficiency. This approach is becoming more common as companies try to fine-tune product performance, especially in dairy alternatives, sauces, and processed foods.

This trend is also linked to the growing complexity of food products. Today’s consumers expect plant-based foods to match the texture of traditional dairy or meat products. Achieving that level of quality is difficult with one ingredient alone. By combining tara gum with other hydrocolloids, companies can create smoother textures and more stable formulations. This is especially important in products like vegan ice cream or plant-based yogurt, where consistency and mouthfeel are critical for consumer acceptance.

Clean-Label Innovation and Regulatory Acceptance Supporting the Shift

Another important part of this trend is the strong push toward clean-label innovation. Food producers are trying to reduce synthetic additives and replace them with natural ingredients, but they still need to maintain product quality. Tara gum fits well into this shift because it is plant-based and already approved for use under good manufacturing practices by global food authorities

Regulatory backing further strengthens its use. The Joint FAO/WHO Expert Committee on Food Additives has assigned tara gum an “ADI not specified,” meaning it is considered safe for regular consumption without strict intake limits. This gives manufacturers confidence to use it more freely in combination with other natural ingredients.

Drivers

Rising Demand for Plant-Based Foods Driving Tara Gum Usage

One of the most important factors pushing the growth of tara gum is the fast shift toward plant-based food consumption. Around the world, more people are moving toward vegetarian, vegan, or flexitarian diets, and this is directly increasing the need for natural food ingredients that can replace animal-based functionality. According to the Food and Agriculture Organization, there is a clear “uptick in adoption of plant-based diets” globally, showing how consumer preferences are changing toward more sustainable and plant-derived food systems

This shift is not small. Studies indicate that nearly 42% of global consumers identify as flexitarians, meaning they are actively reducing meat and dairy intake while looking for plant-based alternatives. As a result, the plant-based food sector has expanded rapidly, reaching an estimated USD 29 billion to USD 44.2 billion market value in 2020. These numbers clearly show that plant-based food is no longer a niche category—it has become a major part of the global food industry.

Functional Ingredient Demand and Government Support Strengthening Growth

Another key aspect of this driving factor is the increasing reliance on functional ingredients in modern food systems. The food industry today depends heavily on hydrocolloids to improve product quality, and reports suggest that nearly 80% of hydrocolloids are used in food applications. This highlights how essential ingredients like tara gum have become in everyday food manufacturing, especially in processed and convenience foods.

At the same time, governments and global organizations are promoting more sustainable and efficient food production systems. The FAO has highlighted that nearly 1.3 billion tonnes of food is wasted every year globally, which has pushed industries to develop more stable and longer-lasting food products. Ingredients like tara gum help improve shelf life and reduce product spoilage by maintaining structure and preventing separation, making them valuable in addressing food waste challenges.

Restraints

Limited and Concentrated Supply Chain Creating Market Constraints

One of the biggest challenges for tara gum is its highly concentrated and limited supply base. Unlike other hydrocolloids that are produced across multiple regions, tara gum depends heavily on a single country for raw material availability. Peru alone accounts for nearly 80% of global tara production, making the entire supply chain highly dependent on one geography.

The situation becomes more concerning when looking deeper into production patterns. Research shows that Peru contributes around 85% of global tara-derived tannins and gum production, with exports reaching 31,442 tonnes in 2018. Despite this, global demand for tara derivatives is estimated at 42,326 tonnes annually, which indicates that supply is not always able to meet demand.

Regulatory Dependence and Processing Limitations Adding Pressure

In addition to supply constraints, regulatory and processing factors also limit the wider adoption of tara gum. Although it is recognized as a safe food additive by global bodies such as the Joint FAO/WHO Expert Committee on Food Additives, its usage is still controlled under good manufacturing practices and specific food standards. This means manufacturers must carefully manage inclusion levels and comply with regulatory frameworks, which can slow down adoption in certain regions.

Another important factor is the limited processing infrastructure. A significant portion of tara production is exported in raw or semi-processed forms. For example, around 60% of Peru’s tara production is exported as powder, while only a small portion is processed domestically. This dependence on export-oriented processing creates bottlenecks, as any disruption in logistics or trade policies can affect global supply.

Opportunity

Expanding Use in Clean-Label and Natural Food Formulations

One of the strongest growth opportunities for tara gum lies in the increasing demand for clean-label and natural food ingredients. Consumers today are paying more attention to ingredient lists and prefer products that contain fewer synthetic additives. This shift is creating a favorable space for plant-based hydrocolloids like tara gum. Global food safety authorities such as the Joint FAO/WHO Expert Committee on Food Additives (JECFA) have confirmed that tara gum does not require a specified daily intake limit, indicating a high level of safety for regular consumption

From a formulation perspective, tara gum offers flexibility as it can be used across multiple food categories at low inclusion levels, typically ranging between 0.05% to 1% in food products. This makes it cost-effective while still delivering the required thickness and stability. As companies aim to reduce artificial stabilizers, tara gum becomes a practical alternative that meets both functional and labeling requirements.

Growing Need for Shelf-Life Improvement and Food Waste Reduction

Another major opportunity comes from the increasing global focus on reducing food waste and improving product shelf life. According to global estimates highlighted by food organizations, a significant portion of food loss happens due to poor stability and spoilage during storage and transportation. Ingredients like tara gum help address this issue by improving texture consistency and preventing separation in products such as dairy alternatives, sauces, and beverages.

Dietary studies also show that tara gum is already widely consumed through everyday food products. For example, average intake levels have been estimated at around 5.3 grams per day in general populations, with even higher exposure levels in certain consumer groups depending on diet patterns. This indicates that the ingredient is already well integrated into food systems, providing a strong base for future expansion.

Regional Insights

Europe dominates with 39.8% share valued at USD 13.1 Bn driven by strong food processing base

Europe held a dominant position in the tara gum market, accounting for 39.8% of the global share with a market value of USD 13.1 Bn. This strong regional presence is largely supported by the well-established food processing industry across countries such as Germany, France, and the United Kingdom, where demand for stabilizers and natural texturizing agents remains consistently high.

The region has a mature food manufacturing ecosystem that relies heavily on hydrocolloids for applications in dairy, bakery, and convenience foods. This creates a steady demand environment for tara gum, especially as companies focus on improving product texture and shelf stability.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Tate & Lyle remains a key global player in specialty food ingredients, with strong capabilities in texture and stabilizer solutions relevant to tara gum applications. In 2025, the company reported revenue of £2.1 billion and adjusted EBITDA of £446 million, reflecting its strong presence in food formulation systems. The company is actively expanding its mouthfeel and hydrocolloid portfolio through acquisitions such as the US$1.8 billion CP Kelco deal, strengthening its position in natural gums and texturizers used across dairy and plant-based segments.

Prodhyg is a specialized player in the hydrocolloid segment, focusing on natural gums and stabilizers including tara gum. The company operates with a strong emphasis on sourcing and processing plant-based raw materials, supporting food manufacturers with customized ingredient solutions. Its business model is centered on supplying high-quality hydrocolloids for applications such as thickening and stabilization.

Top Key Players Outlook

- Tate & Lyle

- Nexira

- Clariant

- Prodhyg

- Exandal

- Silvateam

- Gelymar

- Ingredion

Recent Industry Developments

In 2025, Tate & Lyle has strengthened its position in the tara gum and broader hydrocolloid sector by focusing on natural texture and stabilizing solutions used in food applications. The company reported around £2.1 billion in revenue and £446 million in adjusted EBITDA in 2025, showing stable performance in its ingredients business.

In 2025, Nexira is steadily strengthening its role in the tara gum and broader hydrocolloid sector by focusing on natural, plant-based ingredient solutions used in food and beverage applications. The company operates with an estimated turnover of around US$150 million, supported by strong growth in its health and nutrition segment, which alone generated about US$40.9 million in revenue.

In 2025, Exandal continues to hold a strong position in the tara gum sector as one of the leading global producers and exporters of tara-based ingredients. The company operates with a production capacity of around 100,000 kilos (100 metric tons) of tara gum per month, along with about 1,000 metric tons of tara powder per month, highlighting its large-scale manufacturing strength.

Report Scope

Report Features Description Market Value (2025) USD 33.0 Bn Forecast Revenue (2035) USD 65.3 Bn CAGR (2026-2035) 7.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Form (Powder, Liquid), By Application (Thickener, Stabilizer, Gelling Agent, Emulsifier), By End Use (Bakery, Dairy and Alternatives, Meat and Poultry, Beverages, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Tate & Lyle, Nexira, Clariant, Prodhyg, Exandal, Silvateam, Gelymar, Ingredion Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Tate & Lyle

- Nexira

- Clariant

- Prodhyg

- Exandal

- Silvateam

- Gelymar

- Ingredion

Our Clients

- 181939

- Mar 2026