Global Scaffold-free 3D Cell Culture Market By Type (Hanging Drop Method, Low-Attachment/Adhesion Plates, Micropatterned Surfaces/Microwells and Others (Magnetic Levitation, etc.)), By Application (Stem Cell Research & Tissue Engineering, Cancer Research, Drug Development & Toxicity Testing and Others), By End Use (Biotechnology & Pharmaceutical Companies, Academic & Research Institutes, Hospitals and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180963

- Number of Pages: 326

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

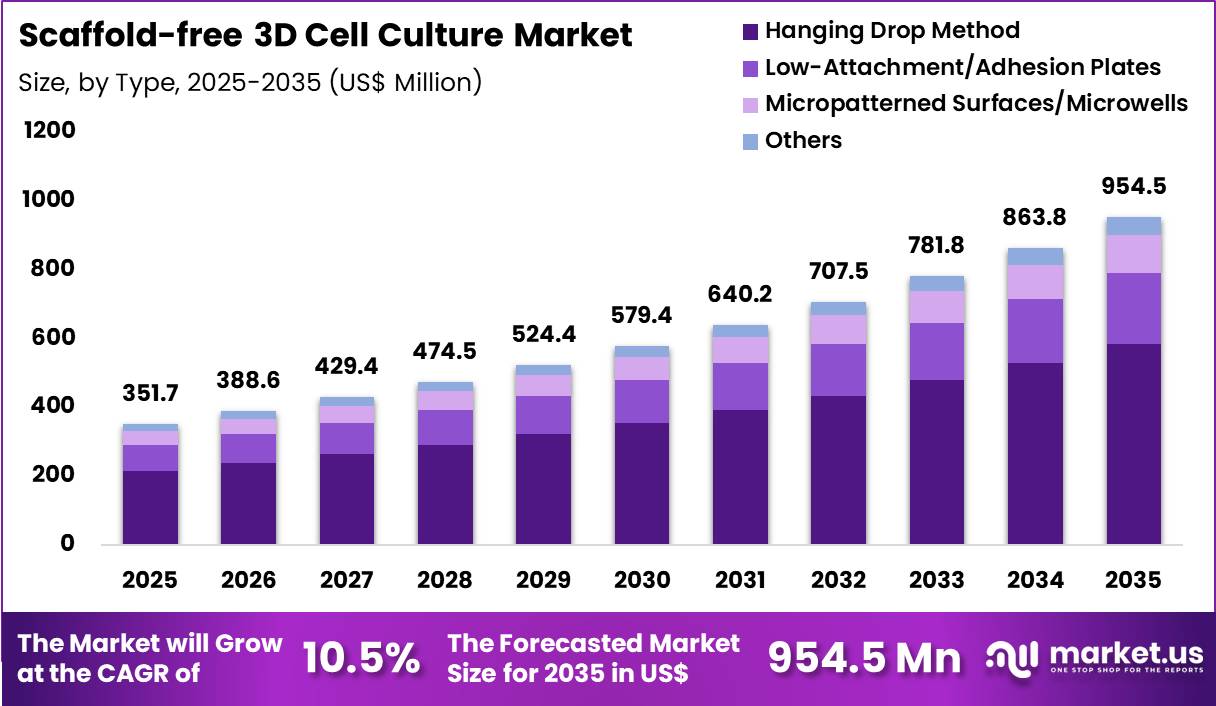

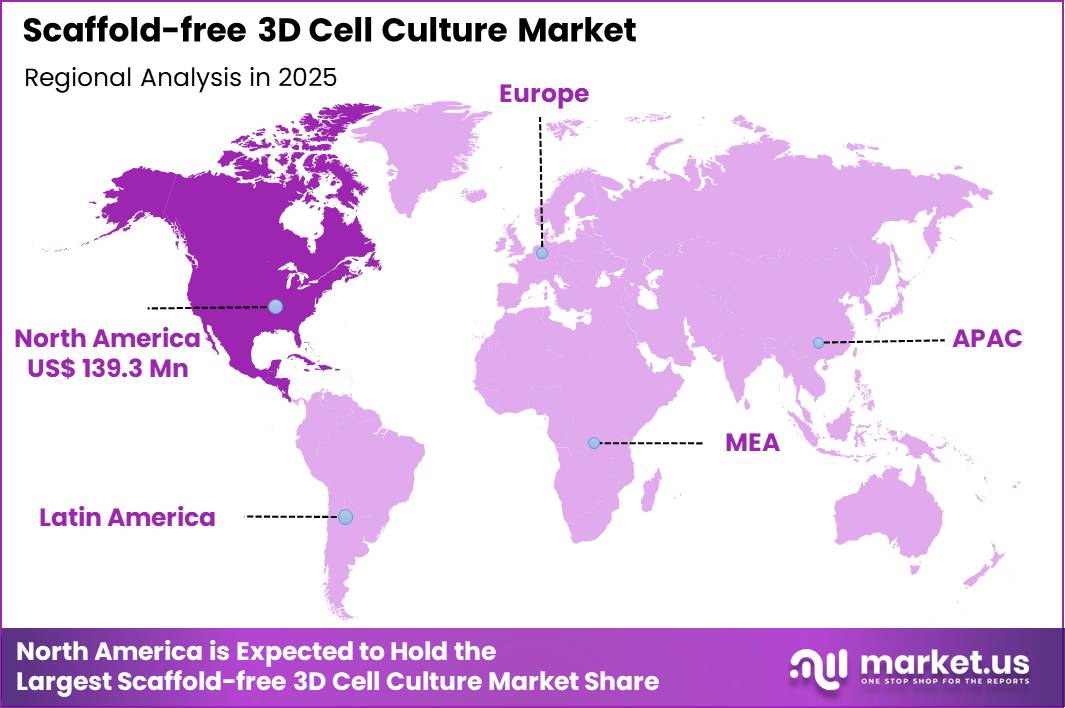

The Global Scaffold-free 3D Cell Culture Market size is expected to be worth around US$ 954.5 Million by 2035 from US$ 351.7 Million in 2025, growing at a CAGR of 10.5% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 39.6% share with a revenue of US$ 139.3 Million.

Increasing demand for physiologically relevant in vitro models accelerates the scaffold-free 3D cell culture market as researchers require platforms that recapitulate native tissue architecture without artificial scaffolds that can introduce artifacts or variability.

Biologists increasingly employ hanging drop and low-attachment plate methods to generate multicellular spheroids from cancer cell lines, enabling accurate assessment of tumor microenvironment interactions, drug penetration, and resistance mechanisms in preclinical oncology studies. These techniques support stem cell research by forming embryoid bodies that mimic early developmental processes, facilitating investigation of differentiation pathways and pluripotency maintenance in regenerative medicine applications.

Pharmaceutical developers utilize scaffold-free cultures to evaluate hepatotoxicity and drug metabolism in liver spheroids, providing more predictive data on compound safety compared to conventional 2D monolayers. Immunologists apply scaffold-free co-culture systems to study immune cell infiltration into tumor spheroids, advancing understanding of immunotherapy responses and checkpoint inhibitor efficacy.

In organoid research, scaffold-free approaches generate intestinal, brain, and kidney organoids that replicate organ-specific functions, supporting disease modeling for cystic fibrosis, neurodegenerative disorders, and renal pathologies.

Manufacturers pursue opportunities to scale scaffold-free platforms through high-throughput formats and automated handling systems, expanding applications in large-scale drug screening where patient-derived spheroids enable personalized therapy evaluation.

Developers advance magnetic levitation and acoustic aggregation techniques that form uniform spheroids rapidly, broadening utility in complex co-cultures involving multiple cell types for tumor-immune or organ-specific interactions.

These innovations facilitate integration with high-content imaging and flow cytometry for detailed phenotypic analysis. Opportunities emerge in bioreactor-compatible scaffold-free systems that support long-term culture and dynamic perfusion, improving relevance for chronic disease modeling. Companies invest in standardized protocols and quality-controlled consumables that reduce variability across studies.

In September 2025, Precision Cell Systems acquired BennuBio, a leader in high-throughput flow cytometry for large particles. According to recent reports, this strategic move aims to address current bottlenecks in the analysis of 3D multicellular spheroids, facilitating the rapid screening of patient-derived cell models in oncology research. Recent trends emphasize multi-cellular complexity, automation, and real-time monitoring, positioning scaffold-free 3D cell culture as a cornerstone of translational research and precision medicine.

Key Takeaways

- In 2025, the market generated a revenue of US$ 351.7 Million, with a CAGR of 10.5%, and is expected to reach US$ 954.5 Million by the year 2035.

- The type segment is divided into hanging drop method, low-attachment/adhesion plates, micropatterned surfaces/microwells and others, with hanging drop method taking the lead with a market share of 61.3%.

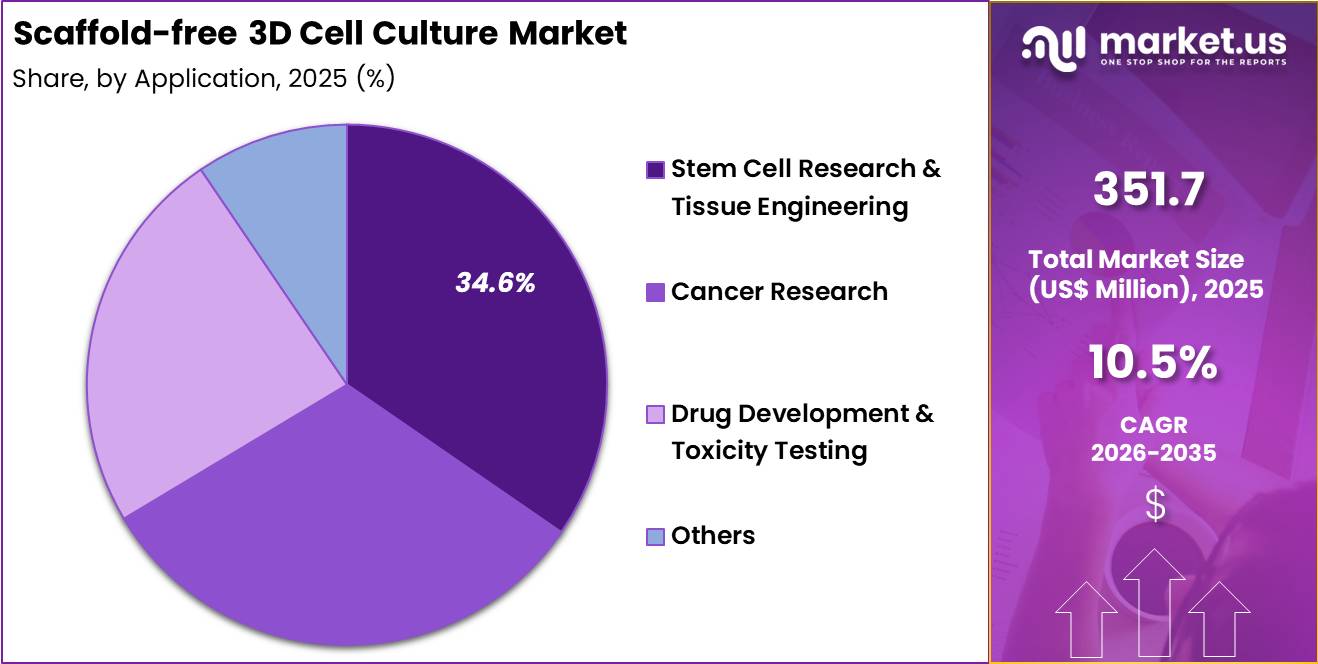

- Considering application, the market is divided into stem cell research & tissue engineering, cancer research, drug development & toxicity testing and others. Among these, stem cell research & tissue engineering held a significant share of 34.6%.

- Furthermore, concerning the end use segment, the market is segregated into biotechnology & pharmaceutical companies, academic & research institutes, hospitals and others. The biotechnology & pharmaceutical companies sector stands out as the dominant player, holding the largest revenue share of 49.6% in the market.

- North America led the market by securing a market share of 39.6%.

Type Analysis

Hanging drop method accounted for 61.3% of growth within type and dominate the scaffold-free 3D cell culture market due to its simplicity, reproducibility, and strong suitability for spheroid formation without requiring external scaffold materials.

Researchers increasingly prefer this method because it supports uniform cell aggregation, preserves cell-to-cell interaction, and creates microenvironments that better resemble in vivo biology than flat 2D cultures. Its lower setup complexity also makes it attractive for routine laboratory work, especially in stem cell studies and early-stage screening workflows.

Published scientific reviews note that scaffold-free 3D systems, including hanging drop techniques, improve cell communication and preserve native biological characteristics more effectively than conventional monolayer systems.

The segment is expected to strengthen further as laboratories seek standardized, low-cost, and biologically relevant culture platforms for regenerative studies and preclinical evaluation. Growing use of spheroid-based assays is likely to keep hanging drop formats at the center of scaffold-free 3D cell culture adoption.

Application Analysis

Stem cell research and tissue engineering accounted for 34.6% of growth within application and dominate the scaffold-free 3D cell culture market because these fields require biologically relevant models that support differentiation, self-organization, and tissue-like cellular behavior. Researchers increasingly use scaffold-free 3D culture platforms to study how stem cells communicate, organize, and mature in environments that more closely replicate living tissue.

Scientific literature shows that 3D stem cell culture better preserves stem cell characteristics and improves functions such as angiogenesis and immunomodulation when compared with many 2D systems. This segment is projected to expand as regenerative medicine programs pursue more realistic tissue models for transplantation research, wound repair, and organ regeneration studies.

Demand is also likely to increase as the need for advanced tissue engineering tools rises in both academic and translational medicine environments. Continued investment in cell-based therapies and engineered tissue constructs is expected to reinforce the leadership of this application segment.

End-Use Analysis

Biotechnology and pharmaceutical companies accounted for 49.6% of growth within end use and dominate the scaffold-free 3D cell culture market due to their strong focus on predictive preclinical testing, lead optimization, and biologically relevant disease models. These companies increasingly adopt scaffold-free systems because they help improve target validation and enable more realistic screening of efficacy and toxicity before clinical development.

FDA-linked research materials and alternative-method initiatives continue to emphasize the value of advanced cell-culture models and new approach methodologies for improving predictivity in nonclinical testing.

At the same time, PhRMA states that member companies have invested more than $1 trillion in R&D since 2000, which highlights the scale of biopharmaceutical investment behind advanced research tools and model systems. This segment is expected to maintain leadership as drug developers prioritize models that reduce translational risk, improve screening quality, and support faster evidence generation in therapeutic development.

Key Market Segments

By Type

- Hanging Drop Method

- Low-Attachment/Adhesion Plates

- Micropatterned Surfaces/Microwells

- Others (Magnetic Levitation, etc.)

By Application

- Stem Cell Research & Tissue Engineering

- Cancer Research

- Drug Development & Toxicity Testing

- Others

By End Use

- Biotechnology & Pharmaceutical Companies

- Academic & Research Institutes

- Hospitals

- Others

Drivers

Increasing adoption of scaffold-free systems in drug discovery is driving the market.

Scaffold-free 3D cell culture techniques enable cells to self-assemble into spheroids or organoids that better recapitulate in vivo physiology compared to traditional monolayer cultures. Pharmaceutical companies increasingly utilize these models to improve predictive accuracy in preclinical screening. The approach avoids artificial matrix interference, allowing native cell-cell interactions critical for compound efficacy evaluation.

Researchers observe enhanced sensitivity to drug responses in scaffold-free formats for oncology applications. The methodology supports high-throughput formats compatible with automated liquid handling systems. Academic institutions integrate scaffold-free platforms into translational research pipelines.

The driver aligns with regulatory emphasis on reducing animal testing through advanced in vitro alternatives. Providers achieve more reliable data on toxicity and pharmacokinetics. Sustained utilization reflects growing confidence in scaffold-free reproducibility across laboratories. This factor propels broader implementation in discovery workflows.

Restraints

High implementation costs of scaffold-free platforms is restraining the market.

Scaffold-free 3D cell culture requires specialized low-attachment plates, magnetic levitation tools, or bioreactor systems that command premium pricing compared to conventional 2D setups. Initial capital investment for compatible instrumentation poses barriers for smaller research entities.

Ongoing consumable expenses for optimized media and coatings add to operational burdens. The restraint limits widespread adoption in resource-constrained academic settings. Training requirements for handling fragile spheroids increase personnel costs. Variability in spheroid formation necessitates additional quality control measures.

The factor moderates penetration in emerging markets with constrained budgets. Facilities delay transitions from established 2D methods due to economic considerations. Such constraints slow overall market velocity during periods of fiscal caution. This element hinders accelerated scaling of scaffold-free applications.

Opportunities

Advancements in regulatory acceptance of non-animal models are creating growth opportunities.

The FDA Modernization Act 2.0, enacted in 2022, removed mandatory animal testing requirements for certain drug development pathways, opening avenues for scaffold-free 3D models as qualified alternatives. This legislative shift enables companies to submit data from scaffold-free organoids for IND applications.

Opportunities arise for validation studies demonstrating equivalence to traditional assays in toxicity prediction. Developers can pursue qualification programs for scaffold-free platforms in preclinical safety assessments. The framework supports partnerships between industry and regulators to standardize acceptance criteria.

Emerging markets gain momentum as global harmonization efforts progress. Such developments facilitate investment in scalable scaffold-free technologies. Stakeholders anticipate reduced timelines for model qualification through prioritized pathways. The opportunity fosters diversification into personalized medicine applications. This environment promotes long-term expansion of scaffold-free methodologies.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the scaffold-free 3D cell culture market through research funding levels, biotechnology investment, and pharmaceutical R&D priorities. Inflation increases costs for cell culture media, laboratory reagents, advanced imaging tools, and incubation systems, which raises operational expenses for research institutions.

Higher interest rates reduce venture capital flow to emerging biotech firms and slow adoption of advanced cell culture technologies. Geopolitical tensions affect global trade in specialty reagents, microplates, and laboratory automation equipment, creating procurement uncertainty for laboratories.

Current US tariffs on imported laboratory instruments, consumables, and precision components increase acquisition costs for research facilities and service providers. These pressures can delay equipment upgrades and limit experimentation budgets in smaller laboratories.

At the same time, organizations strengthen domestic supplier partnerships and invest in local biotechnology infrastructure to ensure supply continuity. Growing demand for accurate drug screening models and advanced disease research continues to support steady and confident market growth

Latest Trends

Launch of specialized scaffold-free platforms for neural cell culture is driving the market.

A major supplier introduced VitroGel Neuron in September 2025, a hydrogel system supporting both 3D and 2D neural cell growth while mimicking extracellular matrix properties. This platform enables tunable stiffness and biofunctional cues for enhanced neuron connectivity and viability.

The launch addresses demands for physiologically relevant models in neuroscience research. Researchers utilize the system for long-term culture of neural networks in drug screening. The development integrates seamlessly with existing imaging and analysis workflows. The 2025 introduction aligns with increased focus on neurodegenerative disease modeling.

Facilities report improved reproducibility in spheroid-based neural assays. The innovation stimulates adoption in high-content screening applications. Early implementations demonstrate superior neurite outgrowth compared to traditional matrices. Overall, this advancement elevates scaffold-free capabilities in specialized cellular research.

Regional Analysis

North America is leading the Scaffold-free 3D Cell Culture Market

North America accounted for 39.6% of the scaffold-free 3D cell culture market in 2025 as biotechnology companies and academic laboratories expanded adoption of advanced in-vitro models that better replicate human tissue biology. Research institutions across the United States and Canada increasingly rely on spheroids and organoid models to study complex cellular interactions in oncology, neurology, and regenerative medicine.

According to the National Institutes of Health, federal funding for stem cell research exceeded USD 2 billion in 2023, strengthening laboratory capacity for advanced cell culture technologies and supporting innovation in tissue engineering platforms.

Drug developers are also integrating three-dimensional cell models into early drug discovery workflows because these systems reproduce physiological responses more accurately than conventional two-dimensional cultures. Pharmaceutical companies across the region are therefore expanding partnerships with academic laboratories to improve predictive disease models and reduce experimental failures during clinical development.

Advances in microfluidic culture systems, automated imaging platforms, and cell analysis tools have further enhanced research productivity in biomedical laboratories. Universities and biotechnology startups are establishing specialized bioengineering laboratories dedicated to organoid development and personalized medicine research. These developments collectively accelerated the adoption of advanced cell culture platforms across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to record strong growth during the forecast period as governments increase investments in biotechnology research and advanced life science infrastructure. Countries such as China, Japan, South Korea, and Singapore are expanding national programs that support stem cell research, regenerative medicine, and advanced biomedical engineering.

Scientific publications and collaborative research projects in the region increasingly focus on organoid and spheroid technologies that enable realistic modeling of human diseases and drug responses. Research institutes across Asia are establishing dedicated stem cell laboratories and translational medicine centers that utilize three-dimensional cellular models for disease studies.

Growing pharmaceutical research activity is also encouraging adoption of advanced cell culture platforms to improve drug toxicity testing and reduce reliance on animal models. Governments are supporting biotechnology innovation through research grants, national laboratories, and biomedical innovation clusters.

Academic institutions are strengthening training programs in tissue engineering, cellular biology, and regenerative medicine to build skilled research talent. Regional biotechnology companies are developing new culture platforms and automated systems tailored for high-throughput drug screening applications. These developments are expected to accelerate the adoption of advanced cell culture technologies throughout Asia Pacific in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key companies in the Scaffold-free 3D Cell Culture Market strengthen growth by advancing spheroid formation technologies, improving ultra-low attachment culture plates, and developing microfluidic systems that support more realistic cell interactions for biomedical research. Firms collaborate with pharmaceutical companies and academic laboratories to accelerate drug discovery, toxicity testing, and disease modeling using three-dimensional cell environments.

They also expand reagent portfolios and automated culture platforms that simplify high-throughput screening in research laboratories. Corning Incorporated represents a significant participant in the Scaffold-free 3D Cell Culture Market and operates as a U.S.-based materials science company that supplies laboratory equipment, cell culture consumables, and advanced life science research solutions worldwide.

The company develops specialized culture plates and reagents designed to support spheroid formation and complex cellular studies. Industry competitors continue to introduce innovative culture systems, strengthen research partnerships, and expand laboratory product portfolios to support wider adoption of advanced three-dimensional cell research technologies.

Top Key Players

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Corning Incorporated

- InSphero AG

- Lonza Group AG

- Greiner Bio‑One International GmbH

- PromoCell GmbH

- Tecan Trading AG

Recent Developments

- In January 2025, Merck KGaA completed the acquisition of HUB Organoids Holding B.V. to significantly bolster its portfolio in the scaffold-free sector. According to the acquisition terms, this move integrates advanced organoid-based screening platforms into Merck’s drug discovery workflow, enabling more accurate mimicry of human organ functions without synthetic support structures.

- In June 2025, Mitsui Chemicals launched InnoCell™, a high-performance cell culture microplate designed for 3D models such as spheroids. As per the product specifications, the plate features superior oxygen permeability and low drug adsorption, which are critical for maintaining high cell viability in long-term drug toxicity assays.

Report Scope

Report Features Description Market Value (2025) US$ 351.7 Million Forecast Revenue (2035) US$ 954.5 Million CAGR (2026-2035) 10.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type (Hanging Drop Method, Low-Attachment/Adhesion Plates, Micropatterned Surfaces/Microwells and Others (Magnetic Levitation, etc.)), By Application (Stem Cell Research & Tissue Engineering, Cancer Research, Drug Development & Toxicity Testing and Others), By End Use (Biotechnology & Pharmaceutical Companies, Academic & Research Institutes, Hospitals and Others) Regional Analysis North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape Thermo Fisher Scientific, Merck KGaA, Corning, Lonza, Greiner Bio‑One, InSphero, PromoCell, Tecan. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Scaffold-free 3D Cell Culture MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Scaffold-free 3D Cell Culture MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Corning Incorporated

- InSphero AG

- Lonza Group AG

- Greiner Bio‑One International GmbH

- PromoCell GmbH

- Tecan Trading AG

Our Clients

- 180963

- March 2026