Global Protein Hydrolysate Market Size, Share, And Industry Analysis Report By Source (Dairy, Plant, Animal, Marine), By Form Type (Powder, Liquid), By Application (Food and Beverages, Infant Nutrition, Clinical and Medical Nutrition, Animal Feed and Pet Food, Pharmaceuticals and Nutraceuticals), By Production Method (Enzymatic, Chemical, Microbial), By Distribution Channel (Direct Sales, Distributors and Wholesalers), By End Use (B2B Food and Beverage Manufacturers, Nutraceutical and Supplement Companies, Pharmaceutical Companies, Animal Feed and Pet Food Manufacturers), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 182876

- Number of Pages: 345

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaways

- By Source Analysis

- By Form Type Analysis

- By Application Analysis

- By Production Method Analysis

- By Distribution Channel Analysis

- By End Use Analysis

- Key Market Segments

- Emerging Trends

- Drivers

- Restraints

- Growth Factors

- Regional Analysis

- Key Regions and Countries

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

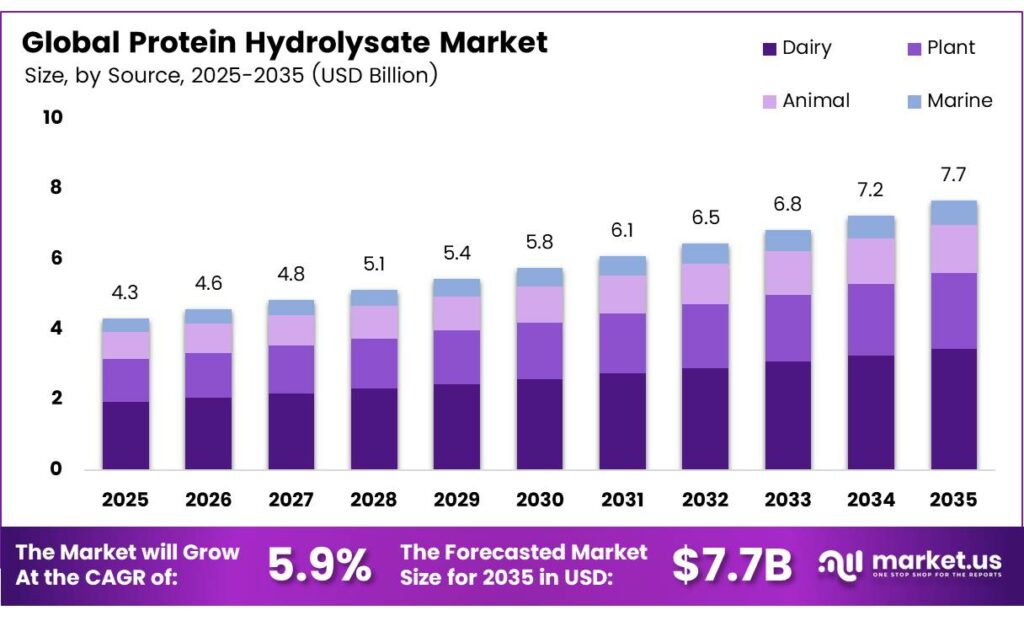

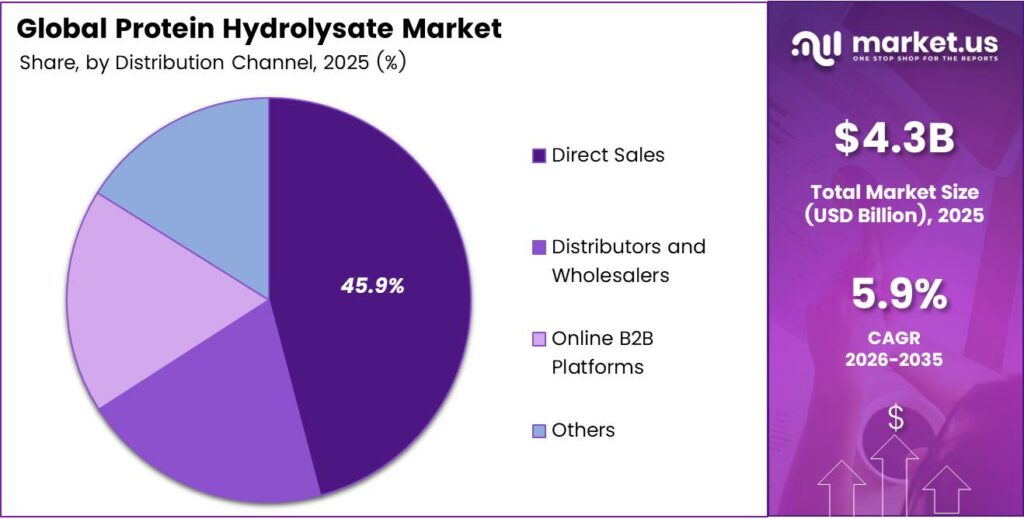

The Global Protein Hydrolysate Market size is expected to be worth around USD 7.7 billion by 2035 from USD 4.3 billion in 2025, growing at a CAGR of 5.9% during the forecast period 2026 to 2035.

Protein hydrolysates are proteins broken down into smaller peptides and amino acids through enzymatic, chemical, or microbial processes. Industries use these ingredients in sports nutrition, infant formula, clinical feeds, and functional foods. Their rapid absorption and high bioavailability make them valuable across both human and animal nutrition sectors.

The market continues to expand due to rising health awareness and growing demand for clean-label nutritional products. Consumers increasingly seek high-quality protein sources that support muscle recovery, immune function, and gut health. Manufacturers respond by investing in advanced hydrolysis technologies that improve peptide purity and taste profiles.

The United States imported protein substances and peptone products under HS 3504 worth approximately USD 1.42 billion in 2024, confirming its position as one of the largest hydrolysate import markets globally. This strong import volume reflects the country’s structural dependence on specialized dairy and plant protein ingredients.

European Union extra-EU exports under CN/HS 3504 exceeded EUR 1.1 billion in 2024, led by Germany, the Netherlands, Ireland, and France. Germany exported approximately EUR 430 million of CN 3504 protein derivatives in 2024, reflecting strong enzymatic hydrolysis and clinical nutrition ingredient manufacturing capacity in the region.

Plant-based and allergen-free hydrolysates gain momentum as consumer preferences shift toward sustainable protein sources. Food and beverage manufacturers reformulate products using soy, pea, and rice hydrolysates to meet vegan and allergen-sensitive demand. This trend strengthens market diversification and expands the addressable customer base globally.

Key Takeaways

- The Global Protein Hydrolysate Market is valued at USD 4.3 billion in 2025 and is projected to reach USD 7.7 billion by 2035 at a CAGR of 5.9% during the forecast period 2026 to 2035.

- Dairy dominates with a 44.8% market share in 2025.

- Powder leads the market with an 81.1% share in 2025.

- Food and Beverages holds the largest share at 34.7% in 2025.

- Enzymatic processing dominates with a 43.6% share in 2025.

- Direct Sales leads with a 45.9% share in 2025.

- B2B Food and Beverage Manufacturers hold the largest share at 31.4% in 2025.

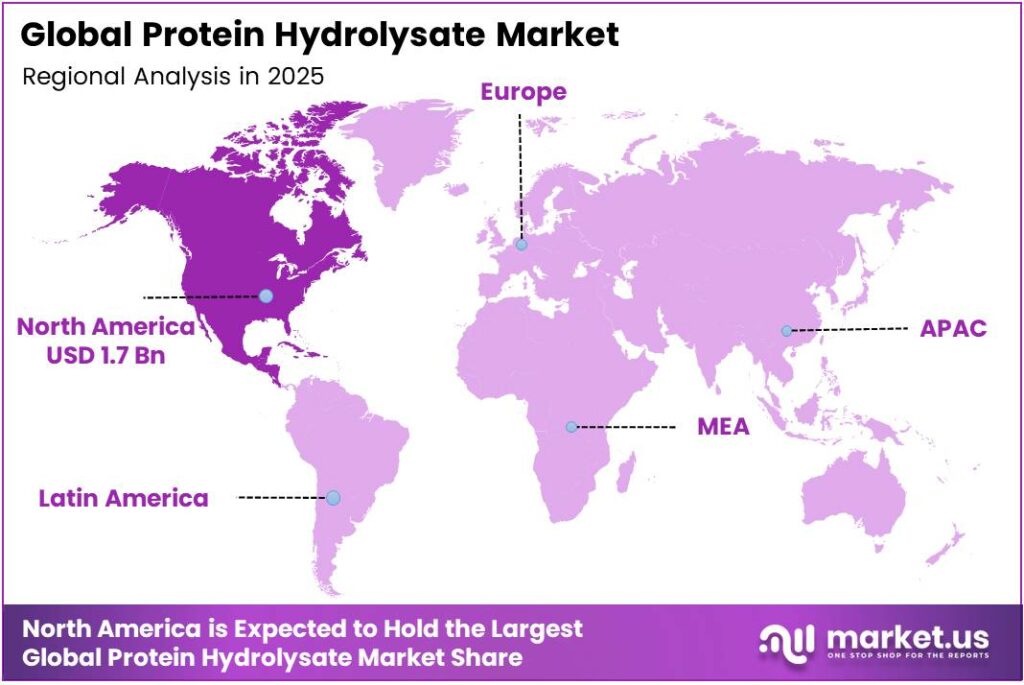

- North America dominates the regional market with a 38.5% share, valued at USD 1.7 billion in 2025.

By Source Analysis

Dairy dominates with 44.8% due to high bioavailability and established supply chains in infant and clinical nutrition.

In 2025, Dairy held a dominant market position in the By Source segment of the Protein Hydrolysate Market, with a 44.8% share. Dairy-derived hydrolysates, including Whey, Casein, and Milk proteins, deliver superior amino acid profiles. Moreover, their well-documented clinical safety record supports widespread use in infant formula and medical nutrition globally.

The Plant segment gains momentum as health-conscious consumers shift toward allergen-free and vegan nutrition. Sub-categories such as Soy, Pea, Rice, Wheat, and Others serve functional food and supplement manufacturers. Consequently, plant hydrolysates attract investment from companies developing sustainable and clean-label ingredient portfolios across multiple product categories.

By Form Type Analysis

Powder dominates with 81.1% due to superior shelf life, ease of handling, and broad formulation compatibility.

In 2025, Powder held a dominant market position in the By Form Type segment of the Protein Hydrolysate Market, with an 81.1% share. Manufacturers prefer powder hydrolysates for their extended shelf stability, precise dosing, and ease of integration into dry blends and encapsulated supplements. Moreover, powder forms reduce cold chain logistics costs for global ingredient distribution.

The Liquid form serves specific processing applications where direct incorporation into beverages and liquid nutritional products is required. Food and beverage manufacturers use liquid hydrolysates to simplify production workflows in ready-to-drink formats. However, their shorter shelf life and refrigeration requirements limit adoption compared to the dominant powder segment.

By Application Analysis

Food and Beverages dominate with 34.7% due to widespread protein enrichment demand across functional and mainstream product categories.

In 2025, Food and Beverages held a dominant market position in the By Application segment of the Protein Hydrolysate Market, with a 34.7% share. This segment spans Functional Foods, Beverages, Bakery and Confectionery, Dairy Products and Alternatives, and Meat and Meat Alternatives. Consequently, it drives the largest volume demand for hydrolysate ingredients among all application categories.

The Sports Nutrition segment records strong growth as athletes and fitness-oriented consumers demand faster-absorbing proteins. Sub-segments include Powders and Supplements, Pre- and Post-Workout Products, Recovery and Endurance Products, and Weight Management Products. Additionally, the rise of gym culture and performance-focused diets across global markets accelerates hydrolysate adoption in this category.

Infant Nutrition represents a premium application segment driven by hypoallergenic formula requirements for infants with protein sensitivity. Regulatory authorities mandate strict safety and efficacy standards for hydrolysates used in infant products. Therefore, this segment sustains consistent demand and supports high-margin ingredient positioning across dairy and clinical hydrolysate categories.

By Production Method Analysis

Enzymatic processing dominates with 43.6% due to precise peptide control, mild conditions, and superior product quality.

In 2025, Enzymatic production held a dominant market position in the By Production Method segment of the Protein Hydrolysate Market, with a 43.6% share. Enzymatic hydrolysis uses specific protease enzymes to cleave proteins under controlled conditions, preserving amino acid integrity. Moreover, this method produces consistent peptide profiles preferred by infant nutrition, clinical, and sports supplement manufacturers.

The Chemical hydrolysis method uses acid or alkali treatment to break down proteins rapidly and at a lower cost. However, chemical processes can degrade sensitive amino acids and generate undesired byproducts, limiting their use in premium nutrition applications. The Microbial and Novel and Emerging Methods sub-segments attract growing investment as manufacturers seek scalable, cost-efficient, and sustainable production alternatives for next-generation hydrolysate ingredients.

By Distribution Channel Analysis

Direct Sales dominates with 45.9% due to strong B2B relationships and customized ingredient supply arrangements.

In 2025, Direct Sales held a dominant market position in the By Distribution Channel segment of the Protein Hydrolysate Market, with a 45.9% share. Large ingredient manufacturers supply hydrolysates directly to food, beverage, and nutritional companies under long-term contracts. Direct sales allow suppliers to offer tailored specifications, technical support, and supply chain integration to key industrial customers.

Distributors and Wholesalers serve mid-tier buyers and regional markets where direct manufacturer relationships are impractical. Online B2B Platforms gain traction as digital procurement tools reduce transaction friction and expand supplier discovery for smaller manufacturers. Additionally, the Others sub-segment covers trade shows, brokers, and agent-based sales that support niche ingredient sourcing across specialty markets.

By End Use Analysis

B2B Food and Beverage Manufacturers dominate with 31.4% due to high-volume ingredient procurement and broad application needs.

In 2025, B2B Food and Beverage Manufacturers held a dominant market position in the By End Use segment of the Protein Hydrolysate Market, with a 31.4% share. These large-scale buyers integrate hydrolysates into thousands of product SKUs across mainstream and functional food categories. Consequently, they generate the highest consistent purchase volumes across the entire protein hydrolysate supply chain.

Nutraceutical and Supplement Companies represent a fast-growing end-use category driven by consumer demand for bioavailable protein ingredients. Pharmaceutical Companies use hydrolysates in parenteral nutrition and specialized medical formulations requiring precise amino acid delivery. Animal Feed and Pet Food Manufacturers, Cosmetics and Personal Care Companies, Research and Academic Institutions.

Key Market Segments

By Source

- Dairy

- Whey

- Casein

- Milk

- Plant

- Soy

- Pea

- Rice

- Wheat

- Others

- Animal

- Meat

- Collagen

- Egg

- Marine

- Fish

- Seafood

- Marine

By Form Type

- Powder

- Liquid

By Application

- Food and Beverages

- Functional Foods

- Beverages

- Bakery and Confectionery

- Dairy Products and Alternatives

- Meat and Meat Alternatives

- Sports Nutrition

- Powders and Supplements

- Pre and Post Workout Products

- Recovery and Endurance Products

- Weight Management Products

- Infant Nutrition

- Clinical and Medical Nutrition

- Animal Feed and Pet Food

- Cosmetics and Personal Care

- Pharmaceuticals and Nutraceuticals

By Production Method

- Enzymatic

- Chemical

- Microbial

- Novel and Emerging Methods

By Distribution Channel

- Direct Sales

- Distributors and Wholesalers

- Online B2B Platforms

- Others

By End Use

- B2B Food and Beverage Manufacturers

- Nutraceutical and Supplement Companies

- Pharmaceutical Companies

- Animal Feed and Pet Food Manufacturers

- Cosmetics and Personal Care Companies

- Research and Academic Institutions

- Direct-To-Consumer Brands

Emerging Trends

Sustainable and Clean-Label Plant Protein Hydrolysates Gain Market Traction

Manufacturers accelerate development of plant-based hydrolysates using pea, soy, and rice proteins to meet clean-label consumer expectations. Brands reformulate products to eliminate allergens and artificial additives, attracting health-conscious buyers globally. Japan imported approximately USD 412 million of HS 3504 products in 2024, signaling a strong regional appetite for functional protein ingredients. This import volume reflects Asia’s growing premium nutrition market.

Precision Fermentation and Taste Masking Technologies Reshape Product Development

Bioengineering firms invest in precision fermentation techniques to produce next-generation hydrolysates with targeted peptide functionality. Simultaneously, innovation in low-bitter taste masking technologies expands the range of hydrolysate-compatible food and beverage applications. Regulatory bodies in the EU and the US expedite approvals for specialized clinical nutrition hydrolysates, further accelerating product commercialization timelines across global markets.

Drivers

Rising Sports Nutrition Demand and Hypoallergenic Infant Nutrition Requirements Fuel Market Growth

Athletes and fitness consumers drive strong demand for high-bioavailability protein hydrolysates that support rapid muscle recovery. Pediatric nutritionists recommend hypoallergenic whey and casein hydrolysates for infants with milk protein intolerance. According to UN Comtrade, China’s HS 3504 imports reached approximately USD 760 million in 2024, with infant formula and medical nutrition proteins remaining the primary demand drivers. This volume confirms Asia’s critical role in hydrolysate market expansion.

Consumer Health Awareness and Enzymatic Innovation Accelerate Adoption

Health-aware consumers increasingly prefer allergen-free and plant-based dietary supplements, expanding the protein hydrolysate customer base globally. Breakthroughs in enzymatic processing technologies improve peptide functionality, absorption rates, and taste profiles. The United States exported HS 3504 protein substances valued at approximately USD 886 million in 2024, reflecting strong domestic processing capability and growing global supply reach.

Restraints

High Production Costs and Raw Material Price Volatility Limit Market Scalability

Protein hydrolysate production requires expensive enzymatic reagents, controlled processing equipment, and high-quality raw protein sources. Raw material price swings, particularly in dairy and marine proteins, directly compress manufacturer margins. Therefore, smaller producers struggle to achieve cost parity with large-scale ingredient companies, limiting competitive entry and slowing overall market supply expansion.

Stringent International Regulatory Requirements Create Compliance Barriers

Regulatory frameworks governing protein hydrolysates differ significantly across the EU, the US, and Asian markets, creating complex compliance obligations. Manufacturers must meet distinct labeling, safety, and clinical efficacy standards in each jurisdiction. Consequently, the cost and time required for multi-market regulatory approval slow product launches and reduce speed-to-market for innovative hydrolysate formulations.

Growth Factors

Functional Food Innovation and Emerging Market Expansion Drive Revenue Opportunities

Food and beverage companies invest in clean-label, protein-enriched product lines that leverage hydrolysate ingredients for functionality and consumer appeal. Emerging markets in Southeast Asia, Latin America, and Africa show rising disposable income levels and growing nutritional awareness. Kerry Group reported EUR 6.9 billion in continuing revenue in FY2024 with +3.3% volume growth, demonstrating sustained commercial demand for protein hydrolysate solutions in clinical and sports nutrition globally.

Personalized Nutrition and Animal Feed Applications Expand the Market Frontier

Personalized nutrition platforms create demand for customized hydrolysate formulations targeting individual metabolic and health profiles. Animal feed and aquaculture sectors adopt protein hydrolysates to enhance livestock and fish performance and feed conversion ratios. New Zealand exported approximately USD 640 million of HS 3504 protein derivatives in 2024, supported by whey hydrolysate and dairy peptide shipments, confirming the global scale of hydrolysate ingredient trade flows.

Regional Analysis

North America Dominates the Protein Hydrolysate Market with a Market Share of 38.5%, Valued at USD 1.7 Billion

North America leads the global protein hydrolysate market, holding a 38.5% share valued at USD 1.7 billion in 2025. The United States drives this dominance through high sports nutrition consumption, advanced infant formula standards, and robust clinical nutrition infrastructure. Moreover, strong domestic manufacturing capacity and a well-developed B2B ingredient supply ecosystem sustain regional leadership throughout the forecast period.

Europe represents a mature and innovation-driven protein hydrolysate market, led by Germany, the Netherlands, France, and Ireland. The EU’s strict food safety regulations and high clinical nutrition standards push manufacturers to develop premium-grade hydrolysate ingredients. Additionally, European trade infrastructure supports significant export activity, reinforcing the region’s role as a global hydrolysate ingredient supplier.

Asia Pacific records the fastest growth rate among all regions, driven by China, Japan, South Korea, and India. Rising middle-class incomes, increasing health supplement consumption, and high infant nutrition demand fuel regional market expansion. Furthermore, government nutritional programs and expanding modern retail distribution channels accelerate protein hydrolysate product penetration across diverse Asian consumer markets.

The Middle East and Africa market remains at an early development stage, but shows increasing momentum from GCC countries and South Africa. Government health initiatives and rising sports nutrition consumption among young urban populations drive nascent demand. Consequently, international ingredient suppliers target this region with affordable hydrolysate product formats to capture long-term growth opportunities as disposable incomes rise.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Arla Foods operates as one of the world’s largest dairy cooperative ingredient suppliers, producing whey and casein hydrolysates used extensively in infant and medical nutrition. The company maintains strong global distribution networks across Europe, Asia, and North America. Moreover, its continued investment in dairy processing infrastructure supports consistent hydrolysate ingredient quality and supply reliability for major food and nutrition customers.

Glanbia PLC positions itself as a leading performance nutrition and ingredient company with deep expertise in whey protein hydrolysate manufacturing. The company serves sports nutrition brands and clinical nutrition manufacturers across multiple global markets. Additionally, Glanbia’s integrated supply chain from dairy farming to finished ingredient production gives it a competitive advantage in delivering customized hydrolysate solutions to B2B customers.

Koninklijke DSM N.V. (now part of DSM-Firmenich) operates a diversified nutrition ingredient platform that includes specialized peptide and protein hydrolysate products. The company serves pharmaceutical, infant nutrition, and functional food markets globally with science-backed ingredient formulations. Furthermore, its integrated research and development capabilities allow it to deliver innovative hydrolysate solutions that meet evolving regulatory and consumer safety requirements.

Abbott is a global healthcare and nutrition company that develops and commercializes hydrolysate-based medical and infant nutrition formulas worldwide. The company’s clinical nutrition brands incorporate extensively hydrolyzed proteins for patients with specific medical conditions and dietary intolerances. Consequently, Abbott drives significant downstream demand for premium-grade protein hydrolysate ingredients through its established hospital, pharmacy, and retail distribution channels globally.

Top Key Players in the Market

- Arla Foods

- Glanbia PLC

- Koninklijke DSM N.V.

- Abbott

- Kerry Group PLC

- Tate and Lyle PLC

- Archer Daniels Midland Company

- Danone Nutricia

- Nestlé S.A.

- Agrilife

- BRISK BIO

Recent Developments

- In 2025, Arla Foods launched Lacprodan DI-3092, a new highly hydrolyzed whey protein for peptide-based medical nutrition. It is UHT-stable, low-lactose, and offers a superior taste profile (minimal bitterness) compared to similar ingredients, while enabling 10 g of high-quality protein per 100 ml.

- In 2025, Koninklijke DSM N.V. (now DSM-Firmenich) launches or develops specifically in the protein hydrolysate sector. The company references hydrolyzed proteins in broader contexts. Compatibility with their human milk oligosaccharides/HMOs in extensively hydrolyzed infant formulas or unrelated applications like seafood extracts/flavors.

Report Scope

Report Features Description Market Value (2025) USD 4.3 Billion Forecast Revenue (2035) USD 7.7 Billion CAGR (2026-2035) 5.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Source (Dairy, Plant, Animal, Marine), By Form Type (Powder, Liquid), By Application (Food and Beverages, Sports Nutrition, Infant Nutrition, Clinical and Medical Nutrition, Animal Feed and Pet Food, Cosmetics and Personal Care, Pharmaceuticals and Nutraceuticals), By Production Method (Enzymatic, Chemical, Microbial, Novel and Emerging Methods), By Distribution Channel (Direct Sales, Distributors and Wholesalers, Online B2B Platforms, Others), By End Use (B2B Food and Beverage Manufacturers, Nutraceutical and Supplement Companies, Pharmaceutical Companies, Animal Feed and Pet Food Manufacturers, Cosmetics and Personal Care Companies, Research and Academic Institutions, Direct-To-Consumer Brands) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Arla Foods, Glanbia PLC, Koninklijke DSM N.V., Abbott, Kerry Group PLC, Tate and Lyle PLC, Archer Daniels Midland Company, Danone Nutricia, Nestlé S.A., Agrilife, BRISK BIO Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Protein Hydrolysate MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Protein Hydrolysate MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Arla Foods

- Glanbia PLC

- Koninklijke DSM N.V.

- Abbott

- Kerry Group PLC

- Tate and Lyle PLC

- Archer Daniels Midland Company

- Danone Nutricia

- Nestlé S.A.

- Agrilife

- BRISK BIO

Our Clients

- 182876

- March 2026