Quick Navigation

Report Overview

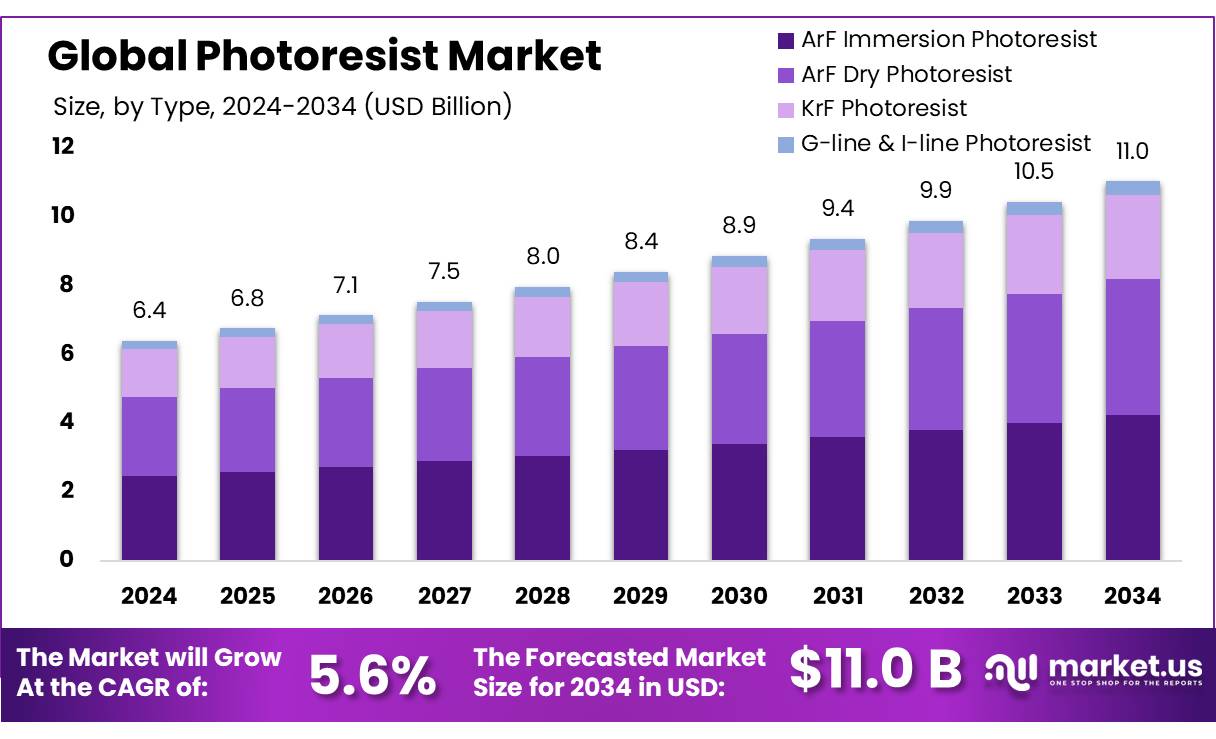

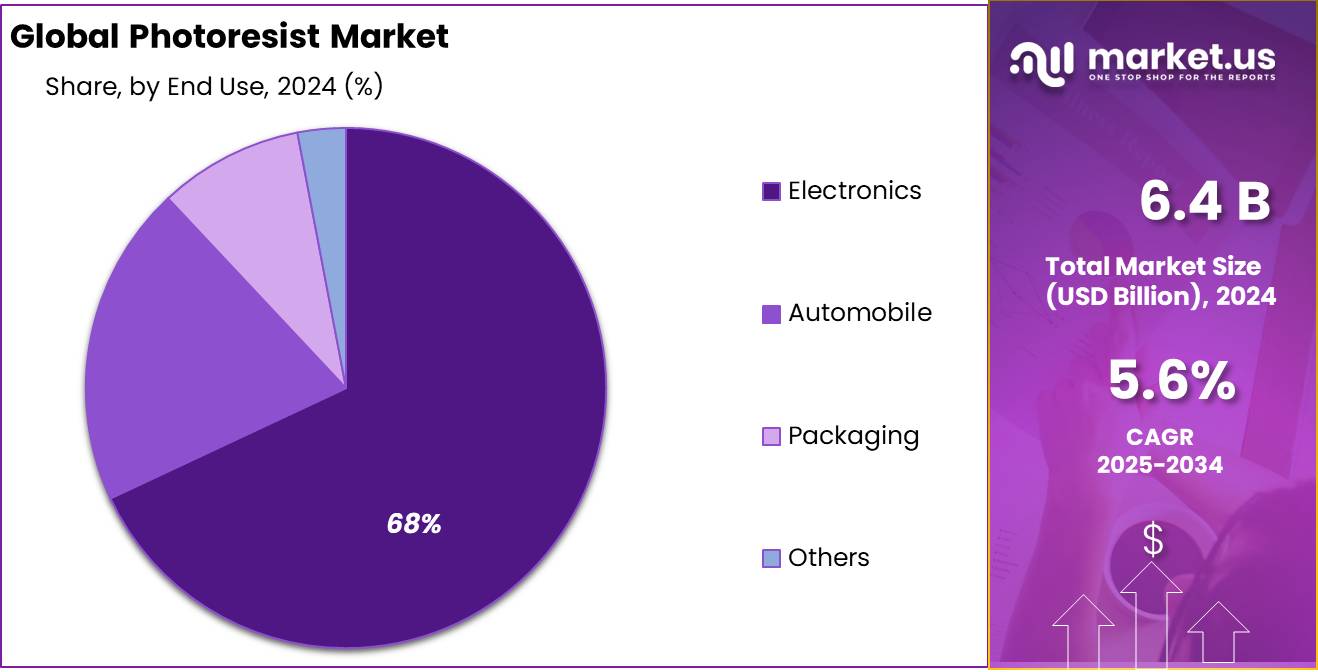

The Global Photoresist Market size is expected to be worth around USD 11.0 Billion by 2034, from USD 6.4 Billion in 2024, growing at a CAGR of 5.6% during the forecast period from 2025 to 2034.

Photoresist cellulose concentrates represent an innovative intersection between photolithographic materials and cellulose-based biopolymers. While photoresists are predominantly utilized in semiconductor manufacturing, the integration of cellulose derivatives into these materials is an emerging area of research, particularly in the context of sustainable and biodegradable alternatives. However, specific data on the market size, growth projections, or industrial applications of photoresist cellulose concentrates remain limited.

Technological advancements, particularly in lithography processes, are propelling the demand for advanced photoresists. The adoption of extreme ultraviolet (EUV) lithography has increased by 25%, enhancing the precision of semiconductor fabrication. Additionally, the rise in consumer electronics, including smartphones, OLED and LCD displays, and wearable devices, has led to a 40% increase in the use of high-resolution photolithography materials.

Government initiatives are playing a crucial role in market expansion. In the United States, the CHIPS and Science Act provides substantial funding to boost domestic semiconductor manufacturing, thereby increasing the demand for photoresist materials. Similarly, the European Union’s efforts to strengthen its semiconductor industry are expected to create new opportunities for photoresist suppliers.

Key Takeaways

- Photoresist Market size is expected to be worth around USD 11.0 Billion by 2034, from USD 6.4 Billion in 2024, growing at a CAGR of 5.6%.

- ArF Immersion Photoresist held a dominant market position, capturing more than a 38.4% share.

- Anti-reflective Coatings held a dominant market position, capturing more than a 43.5% share.

- Semiconductor & IC held a dominant market position, capturing more than a 63.6% share.

- Electronics held a dominant market position, capturing more than a 68.1% share.

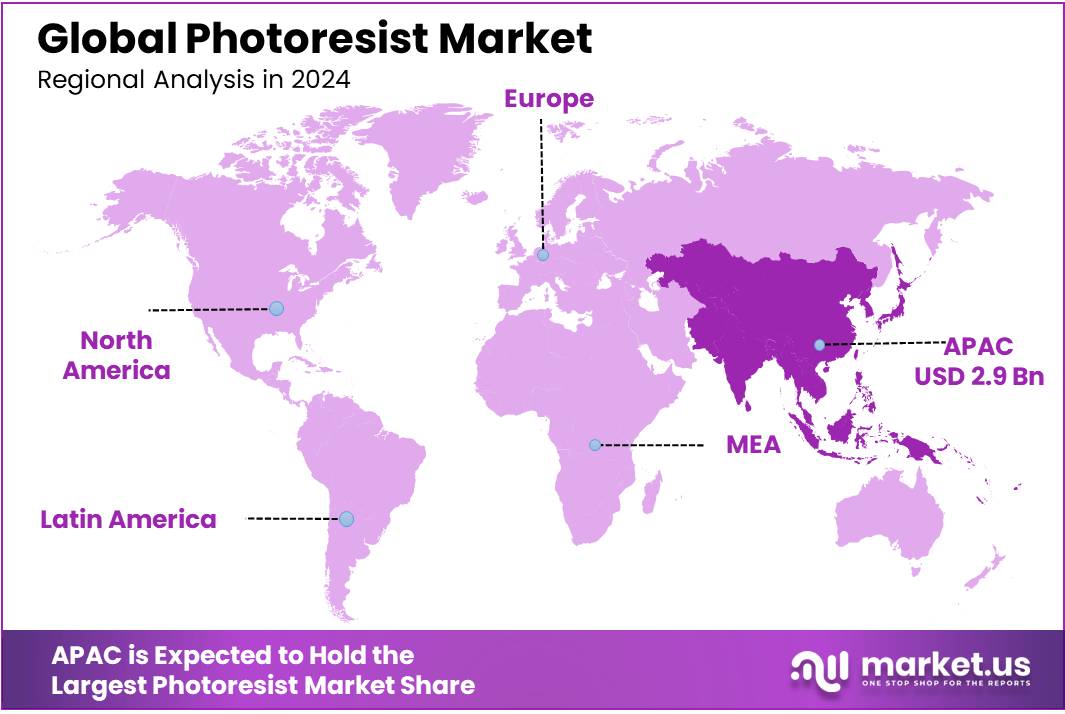

- Asia-Pacific (APAC) region emerged as the dominant player in the global photoresist market, capturing a substantial 46.2% market share valued at approximately USD 2.9 billion.

By Type

ArF Immersion Photoresist leads with 38.4% share in 2024, driven by demand for advanced semiconductor lithography.

In 2024, ArF Immersion Photoresist held a dominant market position, capturing more than a 38.4% share. This segment has gained strong traction mainly due to its superior resolution capabilities, which are critical in advanced semiconductor manufacturing. The immersion lithography technique, which uses liquid between the lens and the wafer surface, allows for more precise patterning at smaller nodes, a key requirement in producing cutting-edge chips used in smartphones, processors, and memory devices.

The continued adoption of 5nm and 3nm process nodes by major foundries like TSMC and Samsung has fueled consistent demand for ArF immersion materials throughout 2024. Additionally, the push for technological independence by economies such as the U.S., Japan, and South Korea has further encouraged local sourcing and usage of advanced photolithography materials, adding momentum to this segment. Looking ahead into 2025, the demand is expected to remain steady, with the share projected to sustain its lead as chip manufacturers prepare for high-volume EUV integration and hybrid lithography strategies.

By Product Type

Anti-reflective Coatings dominate with 43.5% in 2024, driven by precision needs in photolithography processes.

In 2024, Anti-reflective Coatings held a dominant market position, capturing more than a 43.5% share. These coatings are essential in minimizing light reflections during the photolithography stage, which helps improve image fidelity and pattern accuracy on silicon wafers. With the rise in demand for higher-density semiconductor devices, especially in logic and memory chips, the role of anti-reflective materials has become more critical.

The growth in this segment during 2024 can be closely linked to increasing production of advanced chips using sub-10nm process nodes, where even slight distortions in light reflection can lead to defects. This technology ensures more consistent results across high-volume production, which has been a priority for leading foundries throughout the year. Moving into 2025, this product type is expected to maintain its strong presence, particularly as fabs expand capacity for next-generation nodes and continue investing in optical enhancement solutions.

By Application

Semiconductor & IC segment leads with 63.6% share in 2024, fueled by chip demand across electronics and automotive sectors.

In 2024, Semiconductor & IC held a dominant market position, capturing more than a 63.6% share. This strong lead came as global semiconductor manufacturing continued expanding to meet the surge in demand from sectors like consumer electronics, electric vehicles, and industrial automation. The application of photoresists in the fabrication of integrated circuits and microprocessors remained at the core of this growth, especially as companies advanced to smaller technology nodes such as 5nm and 3nm. Foundries and IDM players increased production runs to meet supply gaps created in previous years, further boosting the consumption of photolithographic materials.

Moreover, initiatives from governments—such as the U.S. CHIPS Act and semiconductor self-reliance programs in India and Europe—accelerated investments in domestic chip production in 2024, pushing demand for photoresists used in wafer patterning. This upward trend is expected to continue into 2025, with new fabs coming online and existing ones shifting to high-performance computing and AI-related chip architectures.

By End Use

Electronics end-use dominates with 68.1% share in 2024, backed by booming demand for smartphones, displays, and IoT devices.

In 2024, Electronics held a dominant market position, capturing more than a 68.1% share. This significant share reflects the widespread use of photoresist materials in the production of electronic components like printed circuit boards (PCBs), displays, sensors, and microchips. The sharp rise in consumer electronics production, particularly smartphones, OLED and LCD screens, laptops, and smartwatches, played a major role in pushing demand across the year.

Additionally, the rapid growth of IoT-enabled devices and the rollout of 5G infrastructure in several countries further increased the requirement for miniaturized and high-performance electronic parts. Major electronics hubs such as China, South Korea, and Taiwan continued to expand their fabrication capacities in 2024, intensifying the need for high-quality photoresist materials. As we look ahead into 2025, the segment is expected to sustain its leading position, supported by strong investments in consumer electronics, wearable tech, and next-gen display technologies.

Key Market Segments

By Type

- ArF Immersion Photoresist

- ArF Dry Photoresist

- KrF Photoresist

- G-line & I-line Photoresist

By Product Type

- Anti-reflective Coatings

- Remover

- Developer

- Others

By Application

- Semiconductor & IC

- LCD

- Printed Circuit Boards

- Others

By End Use

- Electronics

- Automobile

- Packaging

- Others

Drivers

Government Initiatives Fueling Growth in the Photoresist Market

One of the primary drivers of the photoresist market is the robust support from governments worldwide to bolster domestic semiconductor manufacturing. This backing has significantly increased the demand for photoresist materials, essential in the photolithography processes of semiconductor fabrication.

In the United States, the CHIPS and Science Act, enacted in August 2022, allocated approximately $52.7 billion to enhance domestic semiconductor research and manufacturing. Of this, $39 billion is designated for manufacturing subsidies, and $13 billion is earmarked for research and workforce development. By March 2024, this initiative had spurred between 25 and 50 projects, with total projected investments ranging from $160 to $200 billion, and the creation of 25,000 to 45,000 new jobs.

Similarly, China’s “Made in China 2025” initiative, launched in 2015, aims to reduce reliance on foreign technology by promoting domestic innovation in high-tech industries, including semiconductors. The Chinese government committed to investing approximately $300 billion into this industrial plan.

In India, the government has introduced several schemes to attract investments in the electronics and semiconductor sectors. Notably, the “Make in India” initiative and the allowance of 100% Foreign Direct Investment (FDI) in the Electronics System Design and Manufacturing (ESDM) sector have been pivotal. These measures aim to establish a robust semiconductor ecosystem, thereby increasing the demand for photoresist materials.

Restraints

Environmental Regulations Pose Challenges for the Photoresist Market

In 2024, the photoresist industry faced significant challenges due to stringent environmental regulations. These regulations, aimed at ensuring chemical safety and reducing environmental impact, led to an 18% increase in compliance costs for manufacturers. The heightened scrutiny and the need for cleaner production processes have compelled companies to invest more in research and development to meet these standards.

The complexity of advanced lithography processes, such as extreme ultraviolet (EUV) lithography, has further exacerbated these challenges. The adoption of next-generation photoresists has been delayed by 15%, primarily due to the intricate requirements of these technologies and the associated environmental considerations.

Additionally, the necessity for cleanroom manufacturing environments has led to a 10% increase in production expenses. Maintaining such environments is crucial to prevent contamination and ensure the quality of photoresist materials.

These factors collectively contribute to a challenging landscape for the photoresist market. While the demand for high-performance photoresists continues to grow, especially with the advancement of semiconductor technologies, the industry must navigate the complexities of environmental compliance and the associated financial implications.

Opportunity

Advancements in EUV Lithography Present Significant Growth Opportunities for the Photoresist Market

The photoresist market is poised for substantial growth, largely driven by the advancements in Extreme Ultraviolet (EUV) lithography. EUV lithography, operating at a wavelength of 13.5 nanometers, enables the production of smaller and more efficient semiconductor devices, catering to the escalating demand for high-performance computing, artificial intelligence, and 5G technologies.

This growth trajectory underscores the increasing adoption of EUV technology in semiconductor manufacturing, which, in turn, amplifies the demand for advanced photoresist materials compatible with EUV processes.

The United States has been at the forefront of this technological advancement, with significant investments aimed at bolstering domestic semiconductor manufacturing capabilities. The CHIPS and Science Act, enacted in 2022, allocated substantial funding to support semiconductor research and development, including EUV lithography initiatives. This legislative support is instrumental in fostering innovation and ensuring the United States remains competitive in the global semiconductor landscape.

Moreover, leading companies in the semiconductor equipment industry, such as ASML, have made remarkable strides in EUV lithography. ASML’s EUV scanners have achieved a throughput of up to 200 wafers per hour as of 2022, a significant improvement from earlier prototypes. This enhancement in production efficiency is pivotal in meeting the growing demand for advanced semiconductor devices.

Trends

Rising Demand for Advanced Lithography in Semiconductor Manufacturing

The semiconductor industry’s shift towards smaller and more complex integrated circuits necessitates the use of sophisticated lithography processes, such as extreme ultraviolet (EUV) lithography. EUV lithography enables the production of chips with features as small as 7 nanometers, enhancing performance and energy efficiency. This technological advancement has led to a 25% increase in the adoption of EUV photoresists, which are crucial for achieving the desired resolution and pattern fidelity in chip fabrication.

Government initiatives have played a pivotal role in supporting this trend. For instance, the United States’ CHIPS and Science Act, enacted in 2022, allocated substantial funding to bolster domestic semiconductor manufacturing, including investments in advanced lithography technologies. Similarly, China’s “Made in China 2025” initiative emphasizes self-reliance in semiconductor production, encouraging the development and adoption of cutting-edge lithography processes.

The Asia-Pacific region, particularly countries like China, Japan, and South Korea, dominates the global photoresist market, accounting for over 60% of the market share. This dominance is attributed to the presence of major semiconductor foundries and the continuous expansion of fabrication facilities in the region.

Regional Analysis

Asia-Pacific Leads Global Photoresist Market with 46.2% Share Valued at USD 2.9 Billion

In 2024, the Asia-Pacific (APAC) region emerged as the dominant player in the global photoresist market, capturing a substantial 46.2% market share valued at approximately USD 2.9 billion. This strong regional performance is primarily attributed to the presence of key semiconductor manufacturing hubs such as China, Japan, South Korea, and Taiwan. These countries collectively account for a significant portion of global chip production, driving high-volume consumption of photoresist materials used in advanced lithography processes.

South Korea continues to lead in memory chip fabrication, with major players like Samsung and SK Hynix expanding their facilities to support production of next-generation DRAM and NAND chips. In parallel, Taiwan’s TSMC has sustained its leadership in logic chip foundry services, investing over USD 30 billion in capital expenditures in 2024 alone, which includes upgrades for EUV-compatible lithography lines. Japan, known for its strength in materials innovation, continues to supply high-purity photoresist chemicals and raw materials that meet the stringent requirements of modern semiconductor fabs.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

ALLRESIST, based in Germany, specializes in the development and production of high-resolution photoresists and complementary materials for micro- and nanolithography. The company offers a wide portfolio, including positive and negative resists used in MEMS, microsystems technology, and sensor applications. In recent years, ALLRESIST has focused on environmentally friendly resists, aligning with European regulatory norms. Its commitment to R&D has enabled collaborations with universities and cleanroom facilities across Europe, strengthening its niche presence in specialized photoresist applications.

DJ MicroLaminates, headquartered in Massachusetts, USA, is known for its dry film photoresist technology, particularly suited for high-aspect ratio microfabrication. Its dry film resists are used in applications such as microfluidics, microelectromechanical systems (MEMS), and micro-optics. The company offers solutions compatible with standard lithography tools, enabling ease of integration for foundries and research labs. Its growth has been supported by increasing demand for simpler, cleanroom-compatible processes and by the rise of bioMEMS and lab-on-a-chip manufacturing sectors.

DuPont is a major global supplier in the photoresist market, offering advanced materials for both conventional and EUV lithography. With deep roots in the electronics segment, DuPont provides photoresists and ancillary materials such as antireflective coatings and developers. The company has expanded its capabilities through the acquisition of Laird Performance Materials and collaborations with chipmakers in the U.S. and Asia. Its robust supply chain and strong R&D allow it to address next-gen semiconductor demands with scalable and precise solutions.

Top Key Players in the Market

- ALLRESIST

- DJ MicroLaminates

- DuPont

- Everlight Chemical Industrial Co.

- Fujifilm Corporation

- JSR Corporation

- LG Chem

- Merck Group

- Micro Resist Technology

- Mitsui Chemicals Inc

- Shin-Etsu Chemical Co., Ltd

- Tokyo Ohka Kogyo Co., Ltd

Recent Developments

March 2025, Fujifilm’s Electronics segment, which includes its photoresist business, reported revenue of ¥432.8 billion (approximately USD 2.9 billion), marking a 20.7% increase from the previous year.

March 31, 2024, JSR reported consolidated revenue of ¥404.6 billion (approximately USD 2.9 billion), with 60.4% of this revenue generated from overseas markets.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 6.4 Bn |

| Forecast Revenue (2034) | USD 11.0 Bn |

| CAGR (2025-2034) | 5.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (ArF Immersion Photoresist, ArF Dry Photoresist, KrF Photoresist, G-line and I-line Photoresist), By Product Type (Anti-reflective Coatings, Remover, Developer, Others), By Application (Semiconductor and IC, LCD, Printed Circuit Boards, Others), By End Use (Electronics, Automobile, Packaging, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | ALLRESIST, DJ MicroLaminates, DuPont, Everlight Chemical Industrial Co., Fujifilm Corporation, JSR Corporation, LG Chem, Merck Group, Micro Resist Technology, Mitsui Chemicals Inc, Shin-Etsu Chemical Co., Ltd, Tokyo Ohka Kogyo Co., Ltd |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |