Global Manual Resuscitator Market By Product Type (Self-Inflating, Flow Inflating, and T-piece) By Modality (Disposable and Reusable) By Technology (Pop-off Valve, PEEP Valve, and Others) By Application (Chronic Obstructive Pulmonary Disease, Cardiopulmonary Arrest, and Others) By Material (Silicon, PVC, and Rubber) By End-User (Hospitals, ASCs, and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Aug 2025

- Report ID: 156647

- Number of Pages: 205

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaways

- Product Type Analysis

- Modality Analysis

- Technology Analysis

- Application Analysis

- Material Analysis

- End-User Analysis

- Key Market Segments

- Drivers

- Restraints

- Opportunities

- Impact of Macroeconomic / Geopolitical Factors

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

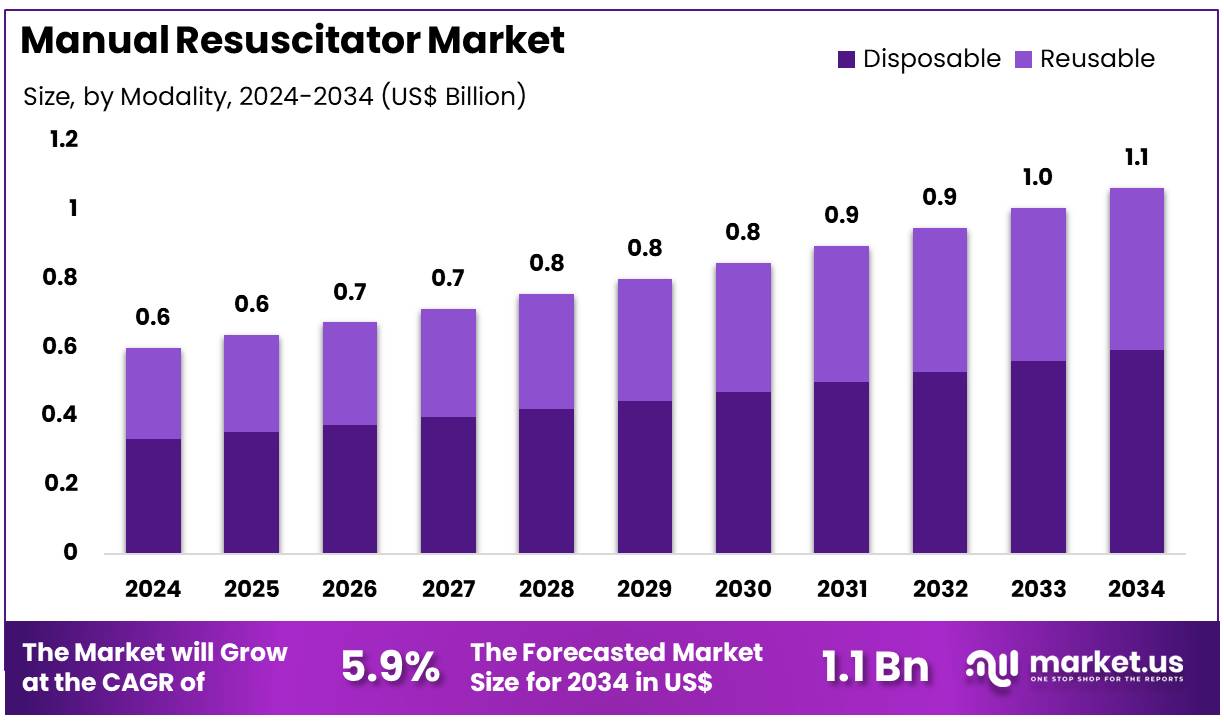

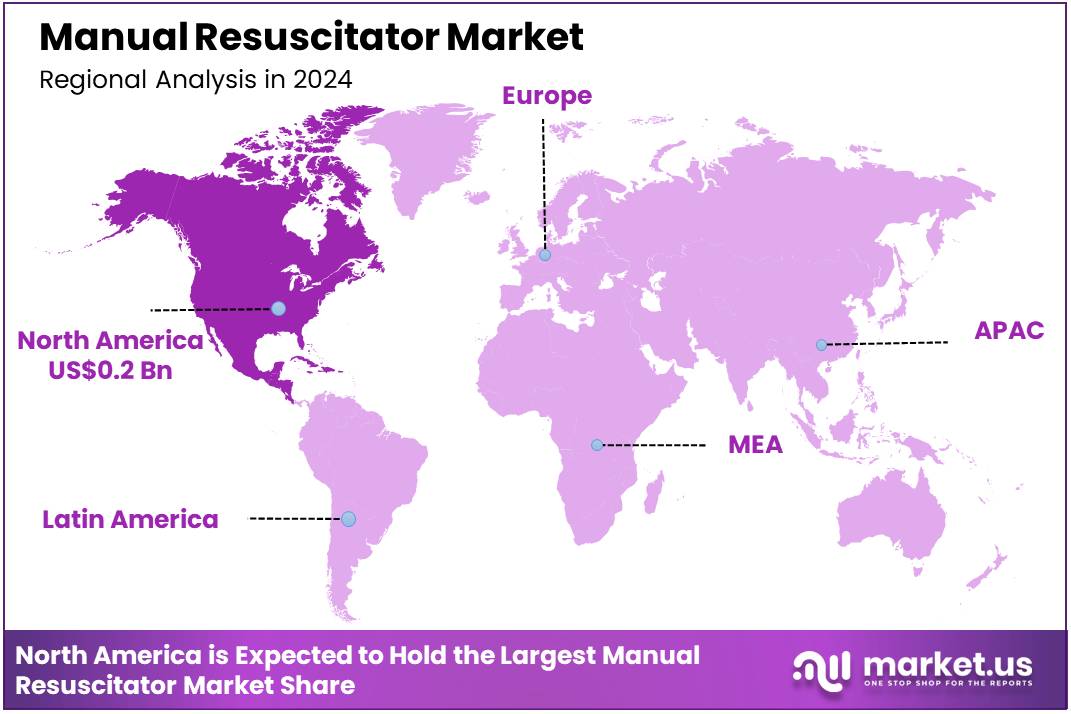

The Global Manual Resuscitator Market size is expected to be worth around US$ 1.1 Billion by 2034 from US$ 0.6 Billion in 2024, growing at a CAGR of 5.9% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 39.5% share with a revenue of US$ 0.2 Billion.

Increasing incidence of cardiovascular and respiratory diseases is a primary driver of the manual resuscitator market. These devices, also known as bag valve masks (BVMs), are crucial for providing ventilation during medical emergencies like cardiac arrest and respiratory failure. With an estimated 19.8 million people dying from cardiovascular diseases in 2022, representing approximately 32% of all global deaths, the demand for immediate and effective resuscitation tools is paramount.

The World Health Organization (WHO) also reports that chronic obstructive pulmonary disease (COPD) affects over 380 million people globally, and asthma impacts over 350 million. This high global prevalence of chronic respiratory conditions ensures a sustained and growing need for manual resuscitators across both hospital and pre-hospital settings. Growing technological advancements and a strong focus on patient safety are shaping key market trends. Manufacturers are now designing manual resuscitators with improved features to minimize complications and enhance efficacy.

For example, in May 2024, the Global LEADR clinical trial showcased the reliable performance of Medtronic’s OmniaSecure defibrillation lead, which, while not a manual resuscitator, highlights the industry’s broader trend toward smaller, more reliable devices to reduce complications. This particular lead achieved a 97.5% success rate in defibrillation testing and a 97.1% freedom from significant complications, reflecting the industry’s dedication to developing technologies that enhance patient outcomes while minimizing common risks.

Rising public health awareness and the expansion of emergency medical services (EMS) are creating significant opportunities for market expansion. The Centers for Disease Control and Prevention (CDC) provides data that underscores the critical role of manual resuscitators in out-of-hospital emergencies, reporting that more than 356,000 Americans experience out-of-hospital cardiac arrests each year.

This statistic, along with the increasing emphasis on training first responders and the general public in life-saving techniques, drives the demand for readily available and easy-to-use manual resuscitators. Furthermore, the push for enhanced infection control, especially in the wake of the COVID-19 pandemic, has led to a major shift toward single-use, disposable manual resuscitators, which offer a high level of safety and eliminate the risks associated with reprocessing.

Key Takeaways

- In 2024, the market for manual resuscitator generated a revenue of US$ 0.6 billion, with a CAGR of 5.9%, and is expected to reach US$ 1.1 billion by the year 2034.

- The product type segment is divided into self-inflating, flow inflating, and T-piece, with self-inflating taking the lead in 2023 with a market share of 40.2%.

- Considering modality, the market is divided into disposable and reusable. Among these, disposable held a significant share of 55.7%.

- Furthermore, concerning the technology segment, the market is segregated into pop-off valve, PEEP valve, and others. The pop-off valve sector stands out as the dominant player, holding the largest revenue share of 49.8% in the manual resuscitator market.

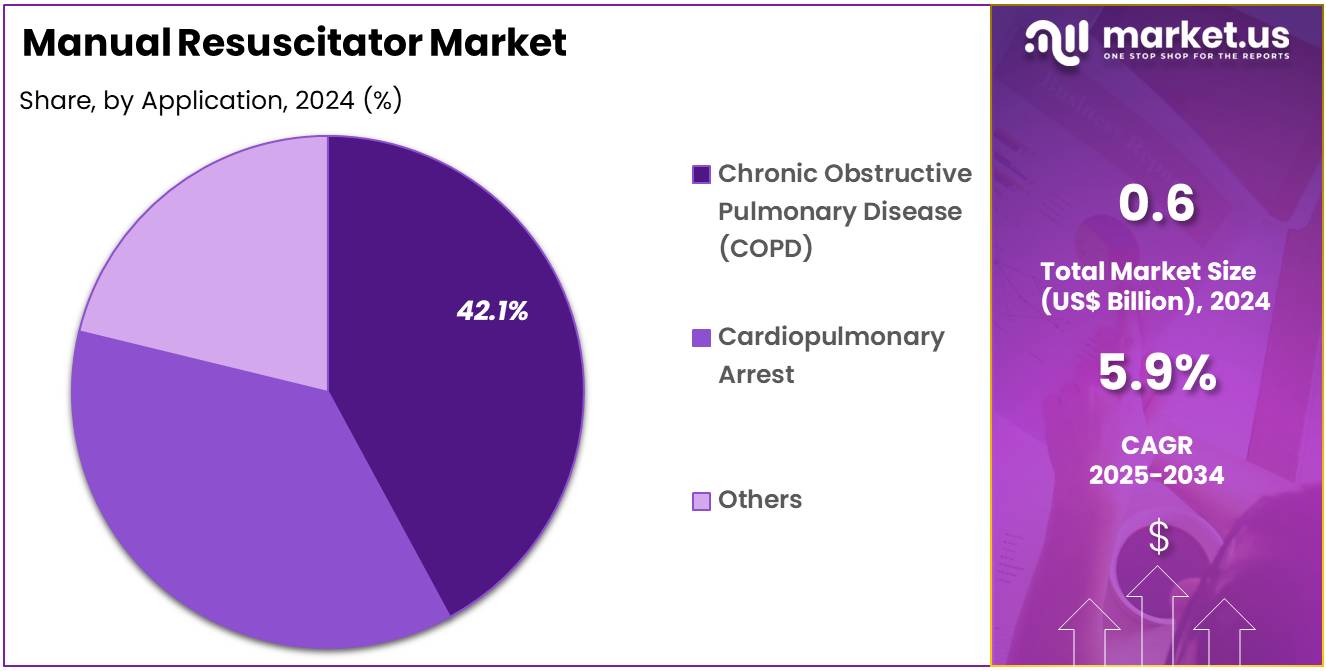

- The application segment is segregated into chronic obstructive pulmonary disease, cardiopulmonary arrest, and others, with the chronic obstructive pulmonary disease segment leading the market, holding a revenue share of 42.1%.

- Considering material, the market is divided into silicon, PVC, and rubber. Among these, PVC held a significant share of 48.9%.

- The end-user segment is segregated into hospitals, ASCs, and others, with the hospitals segment leading the market, holding a revenue share of 55.1%.

- North America led the market by securing a market share of 39.5% in 2023.

Product Type Analysis

Self-inflating resuscitators hold the largest share of 40.2% in the market. This growth is expected to continue due to the simplicity, reliability, and ease of use of self-inflating manual resuscitators. They are commonly used in emergency situations and are preferred in both hospital and pre-hospital settings. The demand for self-inflating resuscitators is projected to increase with the rising prevalence of respiratory diseases, such as COPD and asthma. The compact design and ability to function without an external power source make them particularly suitable for emergency medical services (EMS).

Additionally, advancements in materials that enhance durability and safety are expected to drive further adoption. The growing emphasis on efficient and quick resuscitation methods, especially in critical care settings, is likely to boost the demand for self-inflating resuscitators. Furthermore, the increase in awareness about patient safety and emergency preparedness is anticipated to contribute to the growth of this segment.

Modality Analysis

The disposable modality holds a significant share of 55.7% in the manual resuscitator market. This growth is expected to continue due to the increasing demand for hygiene and safety in medical environments. Disposable resuscitators eliminate the risk of cross-contamination, making them highly preferred in hospitals and emergency care settings, particularly during pandemics or infectious disease outbreaks. The increasing adoption of disposable medical devices in hospitals is projected to drive growth, as they reduce the need for sterilization and maintenance, ensuring higher efficiency.

The growing emphasis on infection control and patient safety is likely to contribute to the rising demand for disposable manual resuscitators. Additionally, as healthcare facilities strive to minimize operational costs, the cost-effectiveness of disposable resuscitators is expected to support the segment’s growth. The trend towards disposable equipment in both high-volume and low-resource settings, particularly in emergency medical services (EMS), is likely to boost this segment.

Technology Analysis

Pop-off valves account for 49.8% of the technology segment in the manual resuscitator market. This growth is expected to continue as pop-off valves are essential for controlling the pressure during resuscitation, preventing barotrauma and ensuring safe ventilation. Hospitals, emergency services, and critical care units increasingly prefer manual resuscitators with pop-off valves for their safety features. The rising incidence of respiratory diseases, including COPD, is projected to drive demand for devices that provide controlled and safe ventilation.

Technological advancements in pop-off valves, such as improved pressure settings and automatic adjustments, are likely to increase their adoption in both hospital and homecare settings. The focus on reducing mechanical ventilation complications and improving patient outcomes is expected to support further growth. The integration of pop-off valve technology in both disposable and reusable resuscitators is likely to contribute to market expansion.

Application Analysis

Chronic obstructive pulmonary disease (COPD) accounts for 42.1% of the application segment in the manual resuscitator market. This segment’s growth is projected to continue as the global burden of COPD rises due to smoking, pollution, and an aging population. COPD patients often require emergency respiratory support, driving demand for manual resuscitators, especially in hospitals and emergency medical services.

With increasing awareness and early detection of COPD, more patients are expected to receive timely care, which could lead to a higher usage of resuscitation devices. Technological advancements in resuscitation techniques and devices are anticipated to improve patient outcomes, making manual resuscitators with specialized features, such as pop-off and PEEP valves, more desirable. The growing focus on managing chronic respiratory conditions is expected to contribute to the sustained demand for manual resuscitators.

Material Analysis

PVC accounts for 48.9% of the material segment in the manual resuscitator market. This material is preferred due to its durability, flexibility, and low cost, making it ideal for both disposable and reusable resuscitators. PVC’s chemical resistance and ability to be easily molded into different shapes and sizes contribute to its widespread use in resuscitation devices. The increasing demand for disposable resuscitators, which use PVC for cost-effective production, is likely to drive growth.

Additionally, the material’s biocompatibility and ease of sterilization contribute to its popularity in medical devices. Hospitals and emergency care settings are expected to continue using PVC resuscitators due to their practicality and availability. The increasing adoption of eco-friendly alternatives and innovation in PVC formulations will likely impact growth but will not diminish PVC’s position as the dominant material in the segment.

End-User Analysis

Hospitals represent 55.1% of the end-user segment in the manual resuscitator market. This growth is expected to continue as hospitals remain the primary settings for emergency care, especially for patients suffering from respiratory distress and cardiac arrest. The demand for manual resuscitators is projected to increase as hospitals continue to prioritize rapid and effective patient resuscitation methods. Technological advancements in resuscitator features, such as integrated pop-off valves and pressure control, are likely to enhance adoption rates.

Rising hospital admissions, especially in emergency departments, will likely boost the demand for resuscitation equipment. Hospitals’ investment in patient safety and high-quality care is expected to drive the continued demand for manual resuscitators. The increasing focus on training healthcare professionals and equipping hospitals with reliable emergency care tools will further fuel growth in this segment.

Key Market Segments

By Product Type

- Self-Inflating

- Flow Inflating

- T-piece

By Modality

- Disposable

- Reusable

By Technology

- Pop-off valve

- PEEP Valve

- Others

By Application

- Chronic Obstructive Pulmonary Disease

- Cardiopulmonary Arrest

- Others

By Material

- Silicon

- PVC

- Rubber

By End-user

- Hospitals

- ASCs

- Others

Drivers

The rising prevalence of chronic respiratory diseases and emergency situations is driving the market.

The market for manual resuscitators is experiencing significant growth driven by the rising global incidence of chronic respiratory diseases and the constant demand for emergency medical equipment. Conditions like asthma, chronic obstructive pulmonary disease (COPD), and other respiratory ailments create a sustained need for devices that can provide immediate and effective respiratory support in a variety of settings.

According to a 2025 World Health Organization (WHO) and European Respiratory Society report, more than 81.7 million people in the WHO European Region alone are living with a chronic respiratory disease, with 6.8 million new diagnoses each year. These patient demographics require continuous care and, often, emergency intervention. Furthermore, emergency medical services (EMS) departments are crucial customers.

A 2024 California Emergency Medical Services Authority report revealed that in fiscal year 2023, there were over 4.3 million EMS calls in California alone, with respiratory-related complaints representing a significant portion of this call volume. This high frequency of respiratory emergencies across the globe ensures a consistent and growing demand for reliable, portable life-saving equipment.

Restraints

The increasing availability of advanced mechanical ventilators is restraining the market.

A significant restraint on the market is the growing adoption of sophisticated, automated mechanical ventilators in healthcare settings, which can sometimes be preferred over manual resuscitators for long-term patient support. While resuscitators are invaluable for immediate and temporary ventilation, the continuous advancement and increased availability of automated systems offer greater precision, consistency, and monitoring capabilities.

A 2024 analysis of the mechanical ventilator market found that it was valued at over $3.15 billion, reflecting the strong and increasing investment in these advanced devices. These ventilators can deliver a precise volume and flow of air for extended periods, reducing the risk of human error and fatigue, which is a major concern with manual operation.

Furthermore, despite their simple appearance, effective use of these manual devices requires proper training. A typical Basic Life Support (BLS) training course, which includes the use of manual resuscitators, can have fees ranging from hundreds of dollars for an individual, adding to the total operational costs for healthcare providers, a factor that encourages the adoption of more automated solutions.

Opportunities

The growing focus on emergency preparedness and disaster management is creating growth opportunities.

The market is presented with significant opportunities due to the increasing focus on emergency preparedness and disaster management by governments and healthcare organizations worldwide. In an era of heightened awareness of public health crises and natural disasters, there is a strong emphasis on building robust medical stockpiles to ensure a rapid and effective response. The US government’s Strategic National Stockpile (SNS), a national repository of medical supplies, received a budget of $980 million in fiscal year 2024 to enhance its capacity for emergency response.

This consistent investment demonstrates the ongoing demand for essential medical devices, including resuscitators, which are critical for mass casualty events. Furthermore, a 2024 report on state-level medical stockpiling in New York noted that the state’s Department of Health had incurred costs of over $452.8 million to procure medical equipment. This trend of national and regional authorities building up their emergency supplies to prepare for a wide range of scenarios, from pandemics to natural disasters, creates a major avenue for sustained sales and market expansion.

Impact of Macroeconomic / Geopolitical Factors

The manual resuscitator market is impacted by macroeconomic and geopolitical factors that challenge manufacturing and distribution. In the U.S., national health expenditures increased by 7.5% in 2023 to reach US$4.9 trillion, signaling robust but inflationary demand for medical goods. Geopolitical tensions and trade policies add significant cost pressures.

The USTR’s Section 301 tariffs on medical products from China have been a key factor, with new duties raising the tariff rate on certain syringes and needles to 100% and on surgical gloves to 50% as of early 2025. These components are essential to the broader emergency medical supply chain, and the duties directly increase procurement costs for hospitals.

Despite these pressures, the market remains strong, driven by a growing need for emergency medical equipment worldwide. Companies are adapting by diversifying their supply chains and investing in domestic production, which helps ensure a more stable supply of critical life-saving devices.

Latest Trends

The trend toward single-use, disposable resuscitators to prevent infection is a recent development.

A significant trend in 2024 is the shift toward the development and adoption of single-use, disposable resuscitators to mitigate the risk of cross-contamination and hospital-acquired infections (HAIs). Unlike their reusable counterparts, which require a labor-intensive and costly sterilization process, disposable models can be used on one patient and then safely discarded, providing a simple and effective infection control solution. This trend is driven by a strong emphasis on patient safety in clinical settings.

According to a 2024 report by the Pennsylvania Patient Safety Authority, the state’s long-term care facilities submitted 23,970 infection reports in 2023, representing an 18.6% increase over the prior year. This concerning data highlights the critical need for enhanced infection control measures in healthcare. A major medical device manufacturer, Ambu, has positioned its Ambu SPUR II resuscitator as a leader in this area, marketing its single-patient-use design as a solution to this problem. This strategic shift towards single-use products is becoming a standard practice for many healthcare facilities and is a key innovation shaping the market.

Regional Analysis

North America is leading the Manual Resuscitator Market

The North American market for manual resuscitators held a significant 39.5% share of the global market in 2024. This dominant position is a direct result of the region’s well-developed healthcare infrastructure, a high incidence of respiratory emergencies, and substantial investment in emergency medical services. The US in particular faces a considerable burden from respiratory illnesses, including chronic obstructive pulmonary disease (COPD), which according to the CDC affects over 15.3 million Americans. This high disease prevalence creates a continuous and critical need for effective resuscitation devices. Furthermore, public and private funding for innovative medical devices is a key growth driver.

For example, in February 2022, the US National Science Foundation (NSF) awarded a US$1 million grant to Dr. Prathamesh Prabhudesai to develop a novel, user-friendly manual resuscitator. This project aims to create a device that requires minimal training, enhancing its accessibility for a wider range of users in emergency scenarios and underscoring the market’s focus on user-centric innovation and public health preparedness.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

The Asia Pacific market for manual resuscitators is anticipated to experience the fastest growth during the forecast period. This is largely a result of rapidly improving healthcare infrastructure, a burgeoning population, and rising awareness of emergency medical care. The region is home to a significant portion of the global population, and with it, a substantial burden of chronic respiratory diseases. For example, a 2023 study published on ResearchGate highlighted that the prevalence of chronic obstructive pulmonary disease in Vietnam was estimated to be between 7% and 10%.

Additionally, the World Health Organization (WHO) has noted significant progress in the development of emergency medical teams in the Western Pacific Region, with a number of countries, including Singapore and the Philippines, establishing WHO-classified teams by the end of 2024. This growth in emergency medical services is projected to increase the demand for reliable and portable resuscitation devices. Community initiatives also play a crucial role in increasing demand.

In September 2023, a mini cardiac medical and CPR awareness camp was held in Madurai, India, aimed at raising community awareness on resuscitation techniques in emergencies. The initiative sought to improve public preparedness, equipping individuals with the knowledge and skills that could help save lives in critical situations, and this trend is expected to continue across the region, further boosting market growth.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

As an essential tool in emergency care and clinical settings, key players in the manual resuscitation bag market strategically drive growth through product innovation and targeted business development. These companies prioritize developing advanced devices with integrated features like pressure monitoring and PEEP valves to enhance patient safety and clinical efficacy. They also actively pursue mergers and acquisitions to expand their product portfolios and strengthen their global market presence. Additionally, a strong focus on manufacturing single-use, disposable products addresses growing concerns around infection control in a post-pandemic healthcare environment.

Ambu is a Danish medical technology company specializing in single-use and life-supporting equipment. The company pioneered the self-inflating resuscitator, known as the “Ambu Bag,” in 1956, a breakthrough that revolutionized emergency medicine. Today, Ambu maintains a leadership position by consistently introducing innovative solutions across its core business areas of anesthesia and patient monitoring. The firm operates globally and continually develops products that improve patient safety, streamline workflows, and support healthcare professionals in critical care scenarios.

Top Key Players

- VYAIRE

- Teleflex Inc

- ResMed

- Medtronic Plc

- Medline Industries, LP

- Laerdal Medical

- HUM GmbH

- Hopkins Medical Products

- CareFusion

- Ambu A/S

Recent Developments

- In July 2025, Teleflex Incorporated announced the acquisition of BIOTRONIK’s Vascular Intervention business to strengthen its portfolio in interventional cardiology and peripheral vascular treatments. While this move is not directly linked to manual resuscitators, it highlights the ongoing trend of industry consolidation and underscores Teleflex’s dedication to providing comprehensive emergency care solutions.

- In September 2024, Medtronic introduced the VitalFlow Extracorporeal Membrane Oxygenation (ECMO) system, designed to improve usability and performance in critical care environments. The system is engineered to seamlessly connect bedside treatment and intra-hospital transport, offering an intuitive interface and adaptable configuration to support manual resuscitation efforts in patients experiencing complex cardiac and respiratory failure.

Report Scope

Report Features Description Market Value (2024) US$ 0.6 Billion Forecast Revenue (2034) US$ 1.1 Billion CAGR (2025-2034) 5.9% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Self-Inflating, Flow Inflating, and T-piece) By Modality (Disposable and Reusable) By Technology (Pop-off Valve, PEEP Valve, and Others) By Application (Chronic Obstructive Pulmonary Disease, Cardiopulmonary Arrest, and Others) By Material (Silicon, PVC, and Rubber) By End-User (Hospitals, ASCs, and Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape VYAIRE, Teleflex Inc, ResMed, Medtronic Plc, Medline Industries, LP, Laerdal Medical, HUM GmbH, Hopkins Medical Products, CareFusion, Ambu A/S. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- VYAIRE

- Teleflex Inc

- ResMed

- Medtronic Plc

- Medline Industries, LP

- Laerdal Medical

- HUM GmbH

- Hopkins Medical Products

- CareFusion

- Ambu A/S

Our Clients

- 156647

- Aug 2025