Global Industrial Sugar Market Size, Share, And Enhanced Productivity By Type (White sugar, Brown sugar, Liquid sugar), By Source (Sugarcane, Sugar beet), By Form (Granulated, Powdered, Syrup), By Application (Dairy Products, Bakery Products, Confectioneries, Beverages, Canned and Frozen Foods, Pharmaceutical, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2026-2035

- Published date: March 2026

- Report ID: 182882

- Number of Pages: 285

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

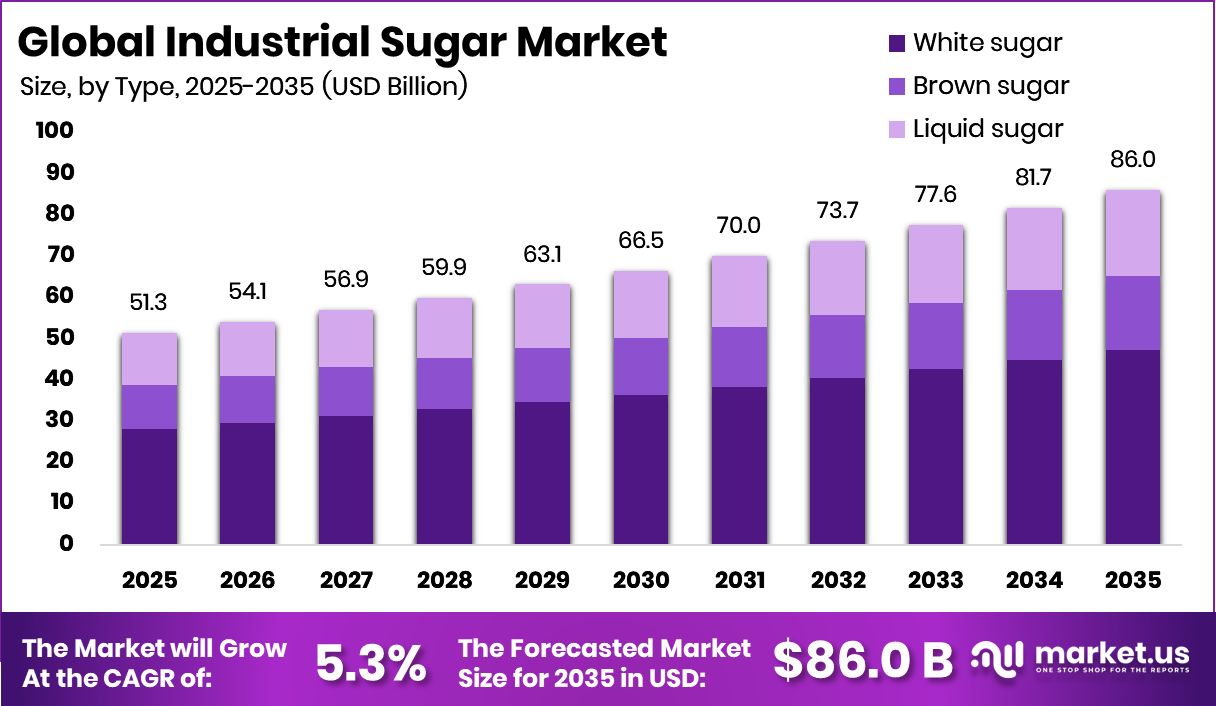

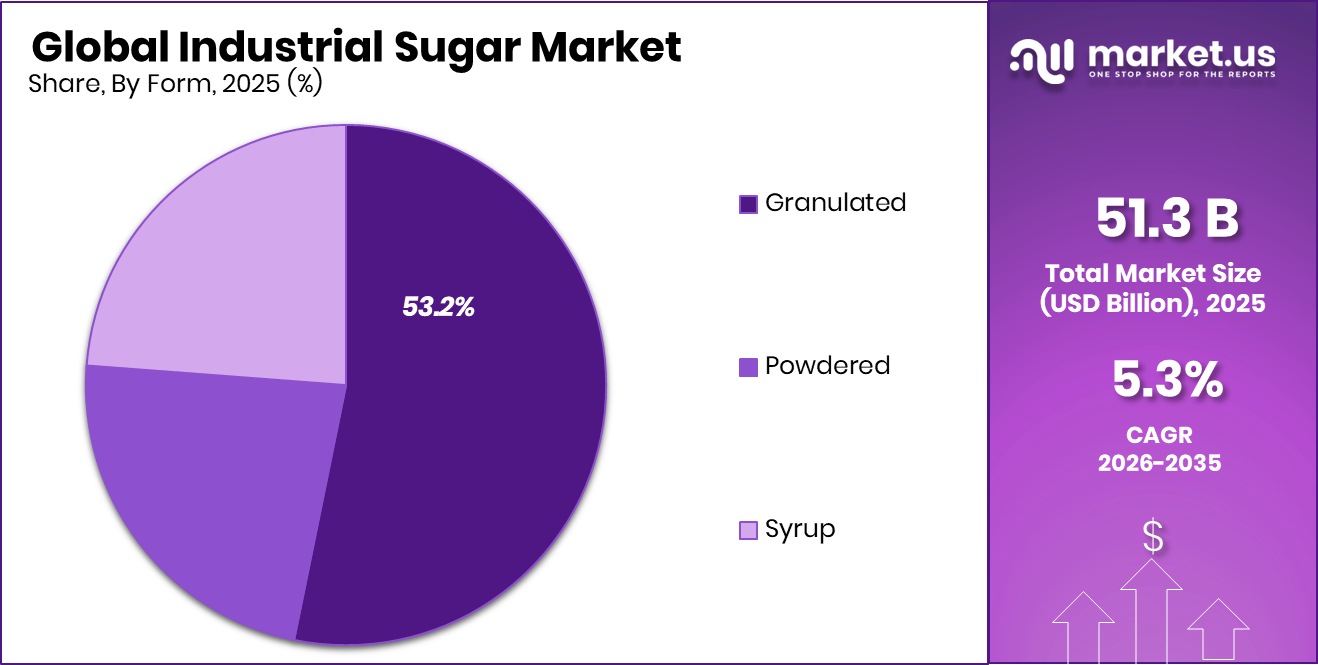

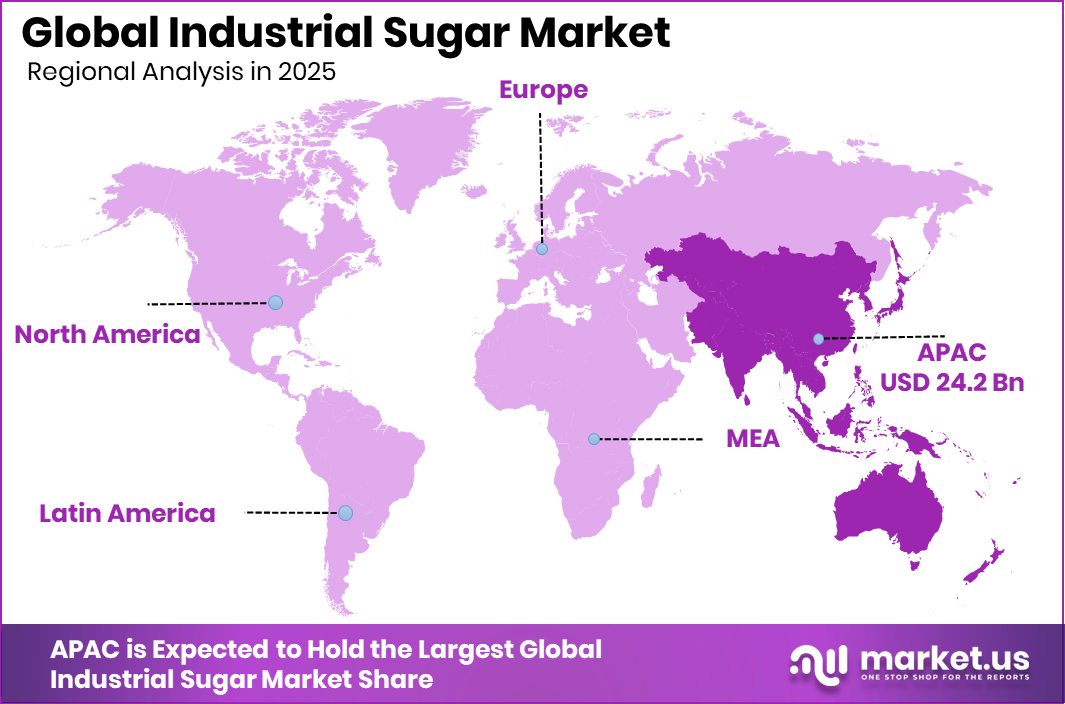

The Global Industrial Sugar Market is expected to be worth around USD 86.0 billion by 2035, up from USD 51.3 billion in 2025. It is projected to grow at a CAGR of 5.3% from 2026 to 2035. With 47.2% share, the Asia Pacific reached USD 24.2 billion in industrial sugar market revenues.

Industrial sugar refers to sugar that is produced and supplied in bulk quantities for commercial manufacturing use rather than direct household consumption. It is widely used as a functional ingredient across dairy products, bakery goods, confectionery products, beverages, canned and frozen foods, pharmaceutical formulations, and other processed applications. Based on your taxonomy, the market is structured by type, including white sugar, brown sugar, and liquid sugar; by source through sugarcane and sugar beet; by form, such as granulated, powdered, and syrup; and by application across multiple food and industrial sectors. Its role goes beyond sweetness, as it also supports texture, preservation, fermentation, color development, and shelf-life stability in large-scale manufacturing.

The Industrial Sugar Market represents the global trade and consumption of sugar used by manufacturers in food, beverage, dairy, pharmaceutical, and processed product industries. Market growth is mainly supported by rising demand for packaged foods, convenience products, flavored dairy items, ready-to-drink beverages, and bakery innovation. Supportive industry funding is also strengthening downstream demand, including a new dairy plant worth nearly $10 million in Kyrgyzstan backed by the Russian Dairy Industry Fund, alongside USDA’s $11M in dairy grants, which expand ingredient requirements for sugar-based formulations.

Demand continues to rise from dairy and beverage processing, where sugar is essential for flavor balance, texture, and preservation. Additional support comes from the EU’s €1.5bn promotion scheme for sustainable meat and dairy, $750,000 for dairy farms to improve long-term success, and $3.45 million awarded to the Northeast Dairy Business Innovation Center, all of which encourage processed dairy expansion and indirectly increase industrial sugar usage.

The key growth factor for the market lies in the steady expansion of food processing infrastructure and value-added product manufacturing. As dairy, bakery, confectionery, and frozen food categories continue to diversify, manufacturers require flexible sugar formats such as granulated, powdered, and syrup for precise formulation needs. This broad usability across multiple applications keeps demand stable and scalable.

A major market opportunity is the increasing development of premium dairy, fortified beverages, functional foods, and pharmaceutical syrups, where sugar remains critical for taste masking, viscosity control, and product consistency. With continued investment flowing into dairy and processed food ecosystems, industrial sugar is well-positioned to benefit from long-term manufacturing expansion.

- In August 2025, Associated British Foods plc, which works in industrial sugar, sugar beet, and cane processing, announced a £75 million acquisition of Hovis. This merger strengthens manufacturing scale, distribution efficiency, and supports long-term growth across its food and sugar-linked business operations.

Key Takeaways

- The Global Industrial Sugar Market is expected to be worth around USD 86.0 billion by 2035, up from USD 51.3 billion in 2025. It is projected to grow at a CAGR of 5.3% from 2026 to 2035.

- In the industrial sugar market, white sugar leads demand at 54.8%, favored for broad food processing globally.

- In the industrial sugar market, sugarcane sources dominate 69.4%, ensuring a reliable supply for large-scale refining operations worldwide.

- The industrial sugar market’s granulated form captures 53.2%, with a preference for storage stability and handling efficiency overall.

- The industrial sugar market’s beverage application holds 26.9%, fueled by soft drinks, juices, and energy products.

- Asia Pacific generated USD 24.2 Bn, contributing 47.2% to the industrial sugar market regionally.

By Type Analysis

In the industrial sugar market, white sugar leads the type share at 54.8% worldwide today.

In 2025, the Industrial Sugar Market continued to be strongly led by white sugar, which accounted for 54.8% of the total market share. This dominance comes from its wide usability across food processing, pharmaceuticals, bakery, confectionery, and beverage manufacturing, where consistency in color, purity, and sweetness is essential. White sugar remains the preferred choice because it blends easily into formulations and supports standardized large-scale production.

Manufacturers also favor it for its longer shelf stability and compatibility with automated industrial systems. Rising demand for packaged foods, ready-to-eat snacks, and processed beverages further strengthened this segment’s position. Its refined texture and neutral taste profile make it highly suitable for premium and mass-market products alike, ensuring continued leadership across industrial applications worldwide.

By Source Analysis

In the industrial sugar market, sugarcane dominates sources with a 69.4% share across production globally.

In 2025, sugarcane remained the leading source in the Industrial Sugar Market, contributing 69.4% of the overall share. Its strong position is supported by abundant cultivation in major producing countries, established milling infrastructure, and efficient extraction processes that make it economically attractive for large-scale industrial use.

Sugarcane-based sugar is widely preferred by manufacturers because of its reliable supply chain and suitability for bulk production across food, beverage, ethanol, and pharmaceutical industries. The growing use of sugar derivatives in fermentation, sweetener blends, and processed food ingredients also reinforced the importance of this source segment. In tropical and subtropical regions, especially, favorable climatic conditions continue to support higher cane yields, helping processors maintain cost efficiency while meeting the rising global demand for industrial-grade sugar products.

By Form Analysis

The industrial sugar market’s granulated form captures a 53.2% share due to the versatility demands.

In 2025, granulated sugar held 53.2% of the Industrial Sugar Market by form, making it the most widely used format across industries. Its popularity is driven by ease of storage, accurate portion control, fast dissolution, and compatibility with high-volume manufacturing lines. Granulated sugar is extensively used in bakery products, confectionery, dairy items, beverages, and dry mix formulations where uniform particle size is critical for product consistency. Industrial buyers prefer this form because it simplifies transportation, reduces handling complications, and performs efficiently in both automated and manual processing systems.

The form is also highly versatile, supporting caramelization, texture enhancement, and sweetness balancing in numerous recipes. Continued expansion of packaged food and beverage production globally has further strengthened demand for granulated sugar in industrial operations.

By Application Analysis

The industrial sugar market beverage application holds a 26.9% share, driven by rising consumption.

In 2025, beverages emerged as the leading application segment in the Industrial Sugar Market, representing 26.9% of total demand. This share reflects the extensive use of industrial sugar in carbonated drinks, juices, flavored milk, energy beverages, syrups, and alcoholic products. Sugar plays a central role not only in sweetness but also in mouthfeel, preservation, fermentation support, and flavor balancing, making it indispensable in beverage manufacturing. Rapid growth in ready-to-drink products and functional beverages has significantly increased sugar consumption across processing facilities.

Emerging markets, where urban lifestyles and convenience-driven consumption continue to rise, contributed strongly to this demand. Seasonal beverages, premium flavored drinks, and expanding quick-service restaurant chains also supported market growth, ensuring beverages remain a key revenue-generating application for industrial sugar producers.

Key Market Segments

By Type

- White sugar

- Brown sugar

- Liquid sugar

By Source

- Sugarcane

- Sugar beet

By Form

- Granulated

- Powdered

- Syrup

By Application

- Dairy Products

- Bakery Products

- Confectioneries

- Beverages

- Canned and Frozen Foods

- Pharmaceutical

- Others

Driving Factors

Rising packaged food and beverage demand

In the Industrial Sugar Market, rising packaged food and beverage demand continues to act as a major growth driver as manufacturers require consistent sugar supply for sweetness, preservation, texture, and shelf stability. The expansion of ready-to-drink beverages, processed snacks, flavored dairy, and convenience foods keeps industrial sugar consumption strong across white sugar, liquid sugar, and syrup formats.

A strong, supportive development comes from NSDC and NEXIM’s high-impact financing alliance to accelerate Nigeria’s $2bn sugar industry transformation, which strengthens supply infrastructure, processing capacity, and long-term industrial availability. This type of financing-backed expansion supports larger food and beverage production ecosystems, creating stable downstream demand for industrial sugar in large-volume applications across domestic and export-focused packaged food manufacturing.

Expanding dairy and bakery processing

The expansion of dairy and bakery processing remains a strong demand catalyst for the Industrial Sugar Market, as sugar plays a key role in sweetness, browning, moisture retention, fermentation, and texture enhancement. Growth in premium desserts, flavored yogurts, pastries, confectionery fillings, and baked snacks directly supports industrial sugar demand in granulated, powdered, and syrup forms.

A notable supportive funding example is Vegan Sweets TREASURE IN STOMACH, accelerating global expansion with ¥50 million funding, which reflects growing investment in modern sweet product manufacturing. Such developments strengthen the broader bakery and dessert ecosystem, indirectly increasing industrial sugar usage in scalable production lines. As dairy innovation and baked product diversification continue, industrial processors are expected to maintain strong procurement volumes.

Restraining Factors

Volatile raw sugar material prices

Volatile raw sugar material prices remain a key restraint in the Industrial Sugar Market, affecting procurement planning, contract pricing, and production margins for industrial buyers. Price fluctuations in sugarcane and sugar beet can directly influence costs across beverage, dairy, bakery, and pharmaceutical manufacturing. While broader funding news, such as the White House releasing $5.5bn in education funds it had withheld, is not directly linked to sugar production, it still reflects macro-level fiscal movement that can influence logistics, labor, and institutional food supply programs over time.

For industrial users, unstable raw material costs often lead to margin pressure, reduced purchasing flexibility, and short-term formulation adjustments. This pricing uncertainty remains a core challenge for manufacturers dependent on long-term bulk sugar contracts.

Health concerns over sugar intake

Health concerns over sugar intake continue to restrain the Industrial Sugar Market, especially as food and beverage producers face increasing pressure to reduce sugar content in mainstream formulations. Consumer preference for low-sugar, reduced-calorie, and functional products has encouraged manufacturers to rethink product recipes, especially in beverages and dairy.

A relevant external signal is Australia’s planned AU$1.1 billion investment in low-carbon liquid fuels, which, while energy-focused, also highlights broader industrial transitions toward healthier and sustainability-driven systems. In food processing, similar shifts are pushing producers toward balanced sweetness systems and portion-controlled products. These health-led formulation changes can limit growth in traditional high-volume sugar usage categories, particularly in soft drinks, confectionery, and sweet dairy products.

Growth Opportunity

Growth in pharmaceutical syrup applications

A major opportunity in the Industrial Sugar Market is the growth in pharmaceutical syrup applications, where sugar is widely used for viscosity control, taste masking, preservation, and stability. The rising production of cough syrups, pediatric formulations, nutritional tonics, and liquid supplements continues to support demand for syrup-grade industrial sugar.

A strong supportive innovation signal comes from Elo Life Systems, raising $20.5m in Series A2 and targeting a natural sweetener launch in 2026, reflecting how the healthcare and wellness sectors are actively exploring advanced sweetening systems. This broader movement opens opportunities for industrial sugar suppliers to serve both traditional syrup manufacturing and hybrid sweetener formulations, especially in regulated pharmaceutical and nutraceutical production environments.

Premium dairy product manufacturing expansion

Premium dairy product manufacturing expansion offers a strong long-term opportunity for the Industrial Sugar Market, particularly in flavored milk, yogurts, dessert creams, ice cream, and indulgent dairy snacks. Sugar remains essential for taste balance, texture improvement, and shelf-life support in premium formulations.

A strong business-supportive signal is Canada’s Awake Chocolate securing significant $8 million funding, showing continued investment in value-added sweet food categories that share formulation overlap with dairy innovation. As premium dairy brands continue launching fortified, flavored, and dessert-oriented products, industrial sugar demand is expected to rise across granulated and syrup forms. This trend creates stable growth opportunities in both mainstream and specialty dairy manufacturing.

Latest Trends

Increasing demand for liquid sugar

A major trend in the Industrial Sugar Market is the increasing demand for liquid sugar, especially in beverage, dairy, bakery fillings, frozen desserts, and pharmaceutical syrup applications. Liquid sugar supports faster blending, accurate dosing, and improved process efficiency in automated manufacturing environments. Financial developments such as Barry Callebaut raising €1.7 billion in bonds amid its refinancing drive reflect broader confidence in ingredient and processed food supply chains, indirectly supporting advanced sweetener and liquid ingredient systems.

As manufacturers continue shifting toward efficiency-focused processing, liquid sugar is becoming a preferred format due to easier storage integration, reduced dust loss, and faster solubility in high-speed industrial production lines.

Functional beverage production is driving usage

Functional beverage production is emerging as a key trend shaping the Industrial Sugar Market, with growing demand from energy drinks, flavored hydration products, dairy beverages, fortified juices, and wellness tonics. Industrial sugar supports flavor balance, mouthfeel, and preservative functionality in these products.

A broader ecosystem support indicator comes from PBGC allocating $3.4 billion for a bakery union pension plan, which reflects financial stabilization in adjacent food manufacturing sectors. As beverage innovation expands into nutrition, immunity, and performance-focused categories, industrial sugar continues to hold value in formulation systems that require taste masking and texture support, particularly in syrup and liquid formats.

Regional Analysis

In 2025, the Asia Pacific held 47.2% share, worth USD 24.2 billion, in industrial sugar.

In 2025, the Industrial Sugar Market demonstrated a geographically diverse demand landscape across North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America, with each region contributing to overall industry expansion through its established food processing, beverage manufacturing, and industrial ingredient consumption base.

Among these, Asia Pacific emerged as the dominating region, accounting for 47.2% of the global market and reaching a value of USD 24.2 Bn, supported by its strong industrial manufacturing presence, large-scale sugar processing capacity, and extensive consumption across packaged foods and beverage applications. The region’s leadership position reflects its well-developed supply chain network and broad downstream industrial usage, making it the primary revenue-generating geography in the market.

North America and Europe continue to represent mature regional markets with steady industrial demand from the processed food and beverage sectors, while Latin America, the Middle East, and Africa maintain their importance through growing industrial applications and regional production capabilities.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2025, the competitive outlook of the global Industrial Sugar Market reflects the strong strategic positioning of Südzucker AG as a quality-driven participant with a well-established industrial supply presence. From an analyst’s perspective, the company’s strength lies in its ability to align refined sugar offerings with large-volume industrial requirements, particularly where consistency, purity, and supply reliability are critical. Its presence among important companies shows that it will continue to play a stable role in providing standardized sugar solutions to a wide range of industrial buyers.

Cargill, Inc. continues to represent scale, operational flexibility, and strong customer integration within the industrial sugar value chain. Analyst assessment suggests that its advantage comes from broad industrial reach and the capability to support multiple end-use sectors through efficient supply management. This positioning makes the company highly relevant for large manufacturers seeking dependable sourcing partnerships and long-term volume commitments in 2025.

For Associated British Foods plc, the analyst viewpoint remains centered on portfolio strength and industrial customer alignment. Its inclusion among leading players highlights strong commercial relevance in bulk sugar supply, particularly for processed food and beverage applications. In 2025, the company’s ability to support steady industrial demand with structured product availability and consistent business continuity appears to define its role.

Top Key Players in the Market

- Südzucker AG

- Cargill, Inc.

- Associated British Foods plc

- Raízen

- Lantic Inc.

- Mitr Phol Group

- AMERICAN CRYSTAL SUGAR

- Louis Dreyfus Company

- Tereos

- Michigan Sugar Company

- Dwarikesh Sugar Industries Limited

- Canal Sugar

Recent Developments

- In June 2025, Raízen, which works in industrial sugar, ethanol, and sugarcane processing, entered negotiations for the sale of four sugarcane mills in Brazil. This is an important asset sale development aimed at improving operational focus, reducing debt pressure, and strengthening its core sugar and bioenergy business.

- In February 2025, Cargill, Inc., which works in industrial sugar, ethanol, and bioenergy solutions, signed an agreement to acquire the remaining 50% stake in SJC Bioenergia, Brazil, taking full control. This development strengthens its sugar and renewable energy business expansion.

Report Scope

Report Features Description Market Value (2025) USD 51.3 Billion Forecast Revenue (2035) USD 86.0 Billion CAGR (2026-2035) 5.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (White sugar, Brown sugar, Liquid sugar), By Source (Sugarcane, Sugar beet), By Form (Granulated, Powdered, Syrup), By Application (Dairy Products, Bakery Products, Confectioneries, Beverages, Canned and Frozen Foods, Pharmaceutical, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Südzucker AG, Cargill, Inc., Associated British Foods plc, Raízen, Lantic Inc., Mitr Phol Group, AMERICAN CRYSTAL SUGAR, Louis Dreyfus Company, Tereos, Michigan Sugar Company, Dwarikesh Sugar Industries Limited, Canal Sugar Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Südzucker AG

- Cargill, Inc.

- Associated British Foods plc

- Raízen

- Lantic Inc.

- Mitr Phol Group

- AMERICAN CRYSTAL SUGAR

- Louis Dreyfus Company

- Tereos

- Michigan Sugar Company

- Dwarikesh Sugar Industries Limited

- Canal Sugar

Our Clients

- 182882

- March 2026