Global Hyperpigmentation Treatment Market By Treatment Type (Topical Agents, Laser Therapy, Chemical Peels, Microdermabrasion) By Indication (Age spots, Post-inflammatory hyperpigmentation (PIH), Melasma, Freckles, Others) By Skin Tone (Fitzpatrick skin type I & II, Fitzpatrick skin type III & IV, Fitzpatrick skin type V & VI) By End-User (Dermatology Clinics, Aesthetic Centers, Hospitals, Homecare Settings) By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: Sep 2025

- Report ID: 157822

- Number of Pages: 214

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

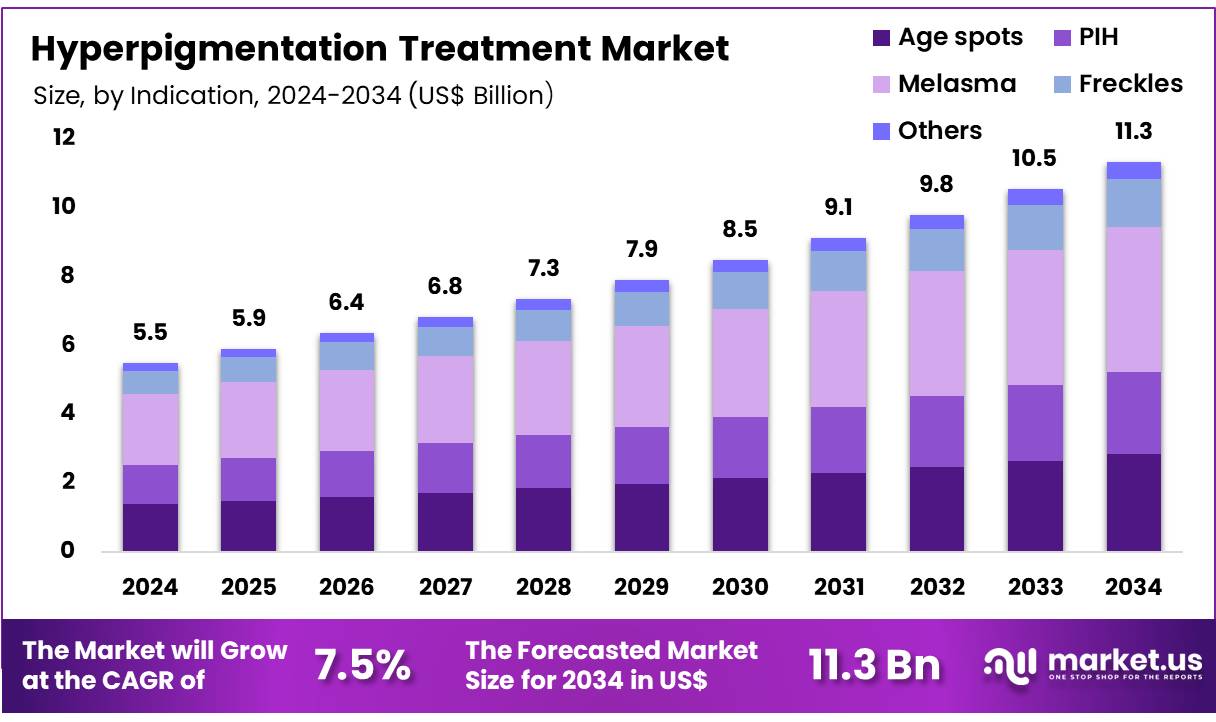

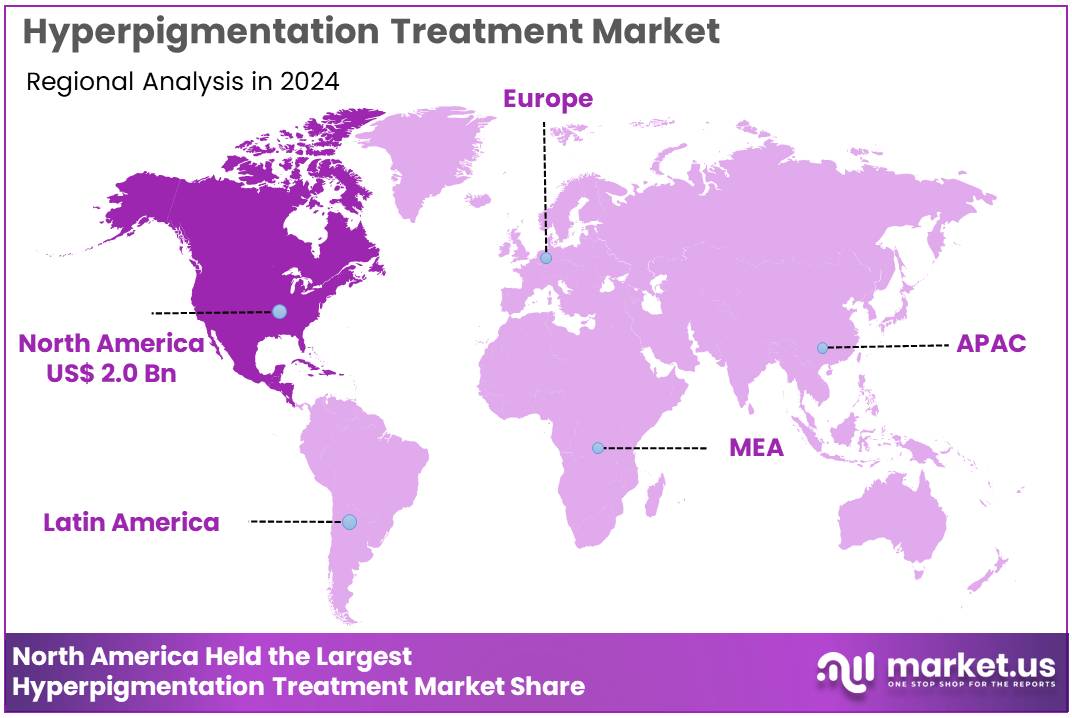

Global Hyperpigmentation Treatment Market size is expected to be worth around US$ 11.3 Billion by 2034 from US$ 5.5 Billion in 2024, growing at a CAGR of 7.5% during the forecast period from 2025 to 2034. In 2024, North America led the market, achieving over 35.8% share with a revenue of US$ 2.0 Billion.

Hyperpigmentation, a common skin condition marked by uneven skin tone and dark spots, affects a large segment of the population and has prompted rising demand for effective treatments. Recent data and clinical studies illustrate both the scale of the problem and the promising advances in treatment.

A key study conducted in India found that 20–30% of women aged 40–65 present with facial melasma, a form of hyperpigmentation. A large multicenter epidemiological survey reported hyperpigmentation as confluent macules in over 80% of patients seen in dermatology clinics across several regions of India. Contributing factors include ultraviolet (UV) exposure, hormonal changes (such as during pregnancy or via contraceptives), genetic predisposition, and skin-inflammation.

Treatment modalities are evolving. Topical formulations (such as hydroquinone, vitamin C, retinoids), chemical peels, and energy-based therapies including laser and light treatments are increasingly used. Recent clinical studies report that certain laser therapies (for example, 755 nm fractionated lasers) deliver 50–75% improvement in post-inflammatory hyperpigmentation (PIH) over multi-year follow up in Asian skin types.

As awareness of skin health and aesthetic wellness continues to grow, the need for safe, effective, and affordable treatment options becomes more urgent. Stakeholders in healthcare, dermatology, and wellness industries are called upon to advance research, improve access, and ensure that treatments are tailored to varied skin types.

Key Takeaways

- Market Size: Global Hyperpigmentation Treatment Market size is expected to be worth around US$ 11.3 Billion by 2034 from US$ 5.5 Billion in 2024.

- Market Growth: The market growing at a CAGR of 7.5% during the forecast period from 2025 to 2034.

- Treatment Type Analysis: Topical Agents hold the largest share, accounting for 36.3% of the global market in 2024.

- Indication Analysis: Melasma holds the leading position, accounting for 37.2% of the global market share.

- Skin Tone Analysis: In 2024, Fitzpatrick skin types III & IV dominate the market, holding a 40.0% share of the global revenue.

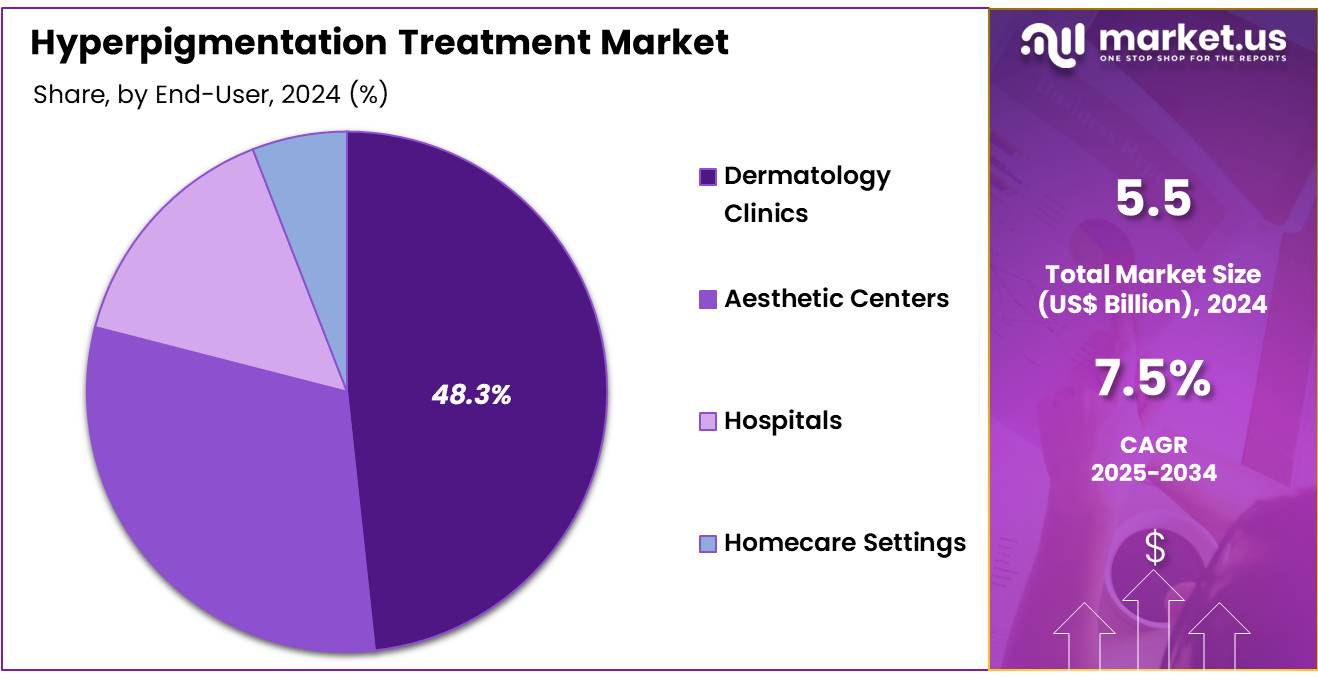

- End-Use Analysis: Dermatology Clinics dominate the market, accounting for a 48.3% share of the global revenue in 2024

- Regional Analysis: In 2024, North America led the market, achieving over 35.8% share with a revenue of US$ 2.0 Billion.

Treatment Type Analysis

In 2024, the hyperpigmentation treatment market is divided into four main types: Topical Agents, Laser Therapy, Chemical Peels, and Microdermabrasion. Among these, Topical Agents hold the largest share, accounting for 36.3% of the global market.

The strong position of topical agents is mainly due to their easy use, wide availability, and lower cost. These treatments include creams, gels, and serums that contain ingredients like hydroquinone, retinoids, and natural extracts. Many of these products are available over the counter or by prescription, making them a preferred choice for people with dark spots, melasma, or acne marks.

Laser Therapy is also widely used and is known for its fast and targeted results. However, it is more expensive and requires professional equipment, which limits its use to clinics and specialized centers. It may also not be suitable for all skin types due to the risk of side effects.

Chemical Peels and Microdermabrasion cover smaller parts of the market. Chemical peels help remove the top layer of the skin to reduce surface-level pigmentation. Microdermabrasion is a gentle skin exfoliation method often used for light pigmentation and skin maintenance.

Overall, topical treatments lead the market because they are affordable, non-invasive, and easy to use at home. Their popularity is expected to grow as more effective and skin-friendly products become available.

Indication Analysis

The hyperpigmentation treatment market is segmented based on indications into Melasma, Post-Inflammatory Hyperpigmentation (PIH), Age Spots, Freckles, and Others. Among these, Melasma holds the leading position, accounting for 37.2% of the global market share.

The dominance of the melasma segment is driven by its high prevalence, especially among women of reproductive age, and its strong link to hormonal changes, sun exposure, and genetic factors. Treatments targeting melasma often include topical agents, chemical peels, and laser-based therapies, making it a major focus area for both pharmaceutical and cosmetic brands.

Post-inflammatory hyperpigmentation (PIH) is another significant segment, resulting mainly from acne, eczema, or skin injuries. It is more common in individuals with darker skin tones and is seeing increased treatment demand due to the global rise in acne cases and inflammatory skin conditions.

Age spots, typically associated with aging and UV exposure, are also contributing to market growth, particularly among older adults seeking cosmetic improvement. Freckles, though usually benign, are treated primarily for aesthetic reasons using light-based therapies and topical formulations.

The Others category includes conditions like liver spots and pigmentation from medical conditions or drugs. Overall, melasma remains the largest and most addressed indication, supported by growing awareness, rising demand for aesthetic treatments, and ongoing product innovation targeting this chronic skin condition.

Skin Tone Analysis

In 2024, the hyperpigmentation treatment market is segmented by skin tone based on the Fitzpatrick skin type classification, which includes Type I & II (light skin tones), Type III & IV (medium skin tones), and Type V & VI (dark skin tones). Among these, Fitzpatrick skin types III & IV dominate the market, holding a 40.0% share of the global revenue.

This dominance is primarily attributed to the higher susceptibility of skin types III & IV to develop melasma, post-inflammatory hyperpigmentation (PIH), and sun-induced pigmentation, particularly in regions with high UV exposure such as Asia, Latin America, and parts of Southern Europe. Individuals with these skin types often seek treatments that are both effective and safe, leading to increased demand for non-invasive and well-tolerated solutions such as topical agents and laser therapies designed for pigmented skin.

Skin types I & II, which include very fair to fair skin tones, represent a smaller market share. Although they are less prone to hyperpigmentation, age spots and freckles are common concerns among this group, especially in Western countries.

Skin types V & VI, representing darker skin tones, also account for a significant share due to the prevalence of PIH and the increasing awareness and accessibility of suitable treatments in Africa, the Middle East, and South Asia. However, treatment options must be carefully chosen to avoid pigmentation worsening or scarring.

End User Analysis

In 2024, the hyperpigmentation treatment market is segmented by end-user into Dermatology Clinics, Aesthetic Centers, Hospitals, and Homecare Settings. Among these, Dermatology Clinics dominate the market, accounting for a 48.3% share of the global revenue.

The strong performance of dermatology clinics is driven by the rising preference for specialized care, access to trained dermatologists, and availability of advanced treatment technologies. Clinics often offer a wide range of procedures including laser therapy, chemical peels, and prescription-based topical treatments tailored to specific skin conditions such as melasma, age spots, and post-inflammatory hyperpigmentation. Their ability to provide personalized treatment plans and follow-up care makes them the most trusted option among patients seeking effective and safe results.

Aesthetic Centers represent a growing segment, particularly for consumers seeking cosmetic improvement through non-invasive or minimally invasive procedures. These centers are expanding rapidly in urban areas and cater to demand for skin lightening, pigmentation correction, and anti-aging treatments.

Hospitals, though equipped with dermatology departments, typically focus on medical treatment rather than aesthetic care. As a result, their share is moderate, mostly serving cases with underlying medical conditions. Homecare Settings account for a smaller share but are expected to grow steadily, supported by the availability of over-the-counter products, online dermatology consultations, and the increasing use of skincare apps and at-home devices.

Key Market Segments

By Treatment Type

- Topical Agents

- Hydroquinone

- Retinoids (Tretinoin)

- Vitamin C (Ascorbic Acid)

- Alpha Hydroxy Acids (AHAs)

- Corticosteroids

- Others

- Laser Therapy

- Q-Switched Lasers

- Fractional Lasers

- Pulsed Dye Lasers (PDL)

- Others

- Chemical Peels

- Glycolic Acid Peels

- Salicylic Acid Peels

- Trichloroacetic Acid (TCA) Peels

- Jessner’s Peel

- Others

- Microdermabrasion

- Crystal

- Diamond

- Phototherapy

- Microneedling

- Others

By Indication

- Age spots

- Post-inflammatory hyperpigmentation (PIH)

- Melasma

- Freckles

- Others

By Skin Tone

- Fitzpatrick skin type I & II

- Fitzpatrick skin type III & IV

- Fitzpatrick skin type V & VI

By End-User

- Dermatology Clinics

- Aesthetic Centers

- Hospitals

- Homecare Settings

Driving Factors

The hyperpigmentation treatment market is being driven by the rising prevalence of pigmentation disorders such as melasma, age spots, and post-inflammatory hyperpigmentation. Increasing consumer awareness about skin health and aesthetics has further accelerated demand, particularly among younger populations concerned with early signs of aging and uneven skin tone. Growing disposable incomes and accessibility to dermatological treatments have broadened patient bases across both developed and emerging economies.

Additionally, the availability of advanced therapeutic options, including topical agents like retinoids, hydroquinone alternatives, and combination therapies, has enhanced clinical outcomes and improved patient compliance. The expansion of aesthetic dermatology clinics and e-commerce platforms offering over-the-counter pigmentation products has also contributed to growth. Furthermore, increasing adoption of minimally invasive and non-invasive procedures such as laser therapy and chemical peels, supported by growing awareness campaigns from skincare brands, continues to fuel market expansion.

Trending Factors

A key trend shaping the hyperpigmentation treatment market is the shift toward integrated and personalized treatment regimens. Multi-modal approaches combining topical therapies with energy-based devices, such as picosecond lasers, intense pulsed light (IPL), and radiofrequency microneedling, are being widely adopted to achieve more consistent results.

Consumer preference for clean-label, fragrance-free, and hypoallergenic formulations is influencing product innovation, with brands increasingly targeting inclusivity by developing solutions effective across different Fitzpatrick skin types. Another notable trend is the rise of teledermatology and digital skin analysis tools, enabling remote consultations and AI-driven treatment recommendations. This has increased access to expert care while expanding market penetration in underserved regions.

Furthermore, demand for cosmeceuticals, incorporating clinically validated ingredients such as niacinamide, vitamin C, and botanical extracts, is rising. Strategic collaborations between dermatologists, technology providers, and cosmetic companies are further reinforcing personalized treatment protocols and enhancing patient engagement.

Restraining Factors

Despite the promising growth outlook, several restraints limit the hyperpigmentation treatment market. Recurrence of pigmentation after treatment remains a major challenge, leading to patient dissatisfaction and lower adherence. Safety concerns regarding long-term use of hydroquinone, a commonly used depigmenting agent, have led to regulatory restrictions in some countries, reducing product availability.

Furthermore, treatment outcomes are often variable across different skin tones and types, with higher risks of post-treatment hypopigmentation or hyperpigmentation in darker skin tones, which restricts uniform adoption. High costs associated with advanced devices, such as lasers and light-based therapies, also create affordability barriers, particularly in cost-sensitive markets. Limited insurance coverage and reimbursement for aesthetic procedures further reduce accessibility.

Moreover, the requirement for multiple treatment sessions and prolonged maintenance regimens affects patient compliance. These factors collectively restrain widespread market adoption and create a need for more affordable, safe, and long-lasting solutions.

Opportunity

Significant opportunities exist in the hyperpigmentation treatment market, particularly within emerging economies in Asia-Pacific, the Middle East, and Latin America, where rising disposable incomes and increasing demand for aesthetic dermatology are expanding the customer base. Advances in energy-based devices that are safer and more effective for darker skin tones are creating untapped growth potential.

Development of biomarker-driven, precision-based therapies that can predict treatment outcomes also represents a key future growth avenue. In addition, the rapid expansion of dermo-cosmetic and over-the-counter skincare products through e-commerce platforms provides companies with a direct-to-consumer opportunity, catering to a growing preference for self-care.

Strategic partnerships between device manufacturers, pharmaceutical firms, and cosmetic brands are expected to create integrated treatment ecosystems. Rising investments in clinical studies to validate novel active ingredients and combination therapies will enhance credibility, supporting stronger adoption. These opportunities collectively position the market for sustained and diversified growth.

Regional Analysis

In 2024, North America held a dominant market position, capturing more than 35.8% share and holding US$ 2.0 billion market value for the year. The region’s leadership is supported by strong consumer awareness, high healthcare spending, and the wide availability of advanced dermatology services. Rising demand for non-invasive and minimally invasive treatments, including laser therapy, chemical peels, and topical agents, has accelerated market growth.

The United States leads within North America due to a large patient pool, high disposable income, and a strong preference for aesthetic procedures. Canada follows with increasing adoption of advanced skincare treatments and growing influence of cosmeceuticals. Favorable regulatory frameworks and the presence of specialized dermatology clinics further strengthen the market position.

Digital platforms, teledermatology, and direct-to-consumer channels are expanding access to treatments across the region. This dominance is expected to continue, as rising awareness and innovation sustain long-term demand.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

The hyperpigmentation treatment market is characterized by the presence of diversified players operating across pharmaceuticals, medical devices, and cosmeceuticals. Companies active in this space emphasize research and development to introduce safer and more effective depigmenting agents, including botanical extracts, antioxidants, and peptide-based formulations.

Device manufacturers are focusing on innovations in energy-based platforms such as lasers, intense pulsed light, and radiofrequency systems to achieve improved outcomes with reduced downtime. Skincare brands are expanding into over-the-counter dermo-cosmetics, targeting consumers seeking self-care solutions and preventive regimes. Strategic collaborations between device innovators, clinical researchers, and consumer skincare providers are increasingly common, allowing integration of advanced therapies with retail offerings.

E-commerce channels and direct-to-consumer models are reshaping distribution strategies, improving accessibility and consumer engagement. In addition, emerging players from developing markets are introducing cost-effective solutions, intensifying competition. Collectively, the market reflects strong innovation pipelines, patient-centric approaches, and expanding global reach.

Market Key Players

- Galderma S.A.

- L’Oréal S.A.

- AbbVie Inc.

- Obagi Cosmeceuticals LLC

- Johnson & Johnson

- Unilever plc

- The Ordinary (DECIEM)

- Beiersdorf AG

- Candela Medical

- Pierre Fabre Dermo-Cosmétique

- ISDIN

- Lumenis Be Ltd.

- Cynosure LLC

- Alma Lasers Ltd.

- Cutera Inc.

- Fotona d.o.o.

- Sciton Inc.

- Syneron Medical Ltd.

- Strata Skin Sciences Inc.

- Procter & Gamble

Recent Developments

- Obagi Cosmeceuticals LLC February 2025: Obagi announced launch of new skincare solutions targeting skin brightening, oxidative stress, and hydration, aiming for a healthier and more radiant complexion. These introduce additional options in its brightening and discoloration-treatment portfolio.

- L’Oréal S.A. August 2024: L’Oréal acquired a 10% stake in Galderma Group, from several institutional investors (Sunshine SwissCo, ADIA, Auba Investment). The acquisition is part of a broader scientific partnership, particularly targeting collaboration in dermatology and injectable aesthetics.

- Galderma S.A.: October 2022: Galderma introduced the A-LUMINATE Brightening Serum via its brand ALASTIN Skincare. The serum is formulated to reduce visible surface hyperpigmentation (dark spots, melasma) without harsh or irritating ingredients, using a peptide/antioxidant blend and PATH-3 Technology. It is intended for long-term daily use and complements in-office treatments.

- AbbVie Inc.: SkinMedica, a brand under Allergan Aesthetics (AbbVie), released the HA5® Hydra Collagen Hydrating Foaming Cleanser on August 19, 2025. It includes a blend of hyaluronic acid forms and vegan collagens, aiming for gentle cleansing with hydration benefits. While focused on hydration and skin barrier health, smoother, more radiant skin helps in managing appearance of discoloration/hyperpigmentation.

Report Scope

Report Features Description Market Value (2024) US$ 11.3 Billion Forecast Revenue (2034) US$ 5.5 Billion CAGR (2025-2034) 7.5% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Treatment Type (Topical Agents, Laser Therapy, Chemical Peels, Microdermabrasion) By Indication (Age spots, Post-inflammatory hyperpigmentation (PIH), Melasma, Freckles, Others) By Skin Tone (Fitzpatrick skin type I & II, Fitzpatrick skin type III & IV, Fitzpatrick skin type V & VI) By End-User (Dermatology Clinics, Aesthetic Centers, Hospitals, Homecare Settings) Regional Analysis North America-US, Canada, Mexico;Europe-Germany, UK, France, Italy, Russia, Spain, Rest of Europe;APAC-China, Japan, South Korea, India, Rest of Asia-Pacific;South America-Brazil, Argentina, Rest of South America;MEA-GCC, South Africa, Israel, Rest of MEA Competitive Landscape Galderma S.A., L’Oréal S.A., AbbVie Inc., Obagi Cosmeceuticals LLC, Johnson & Johnson, Unilever plc, The Ordinary (DECIEM), Beiersdorf AG, Candela Medical, Pierre Fabre Dermo-Cosmétique, ISDIN, Lumenis Be Ltd., Cynosure LLC, Alma Lasers Ltd., Cutera Inc., Fotona d.o.o., Sciton Inc., Syneron Medical Ltd., Strata Skin Sciences Inc., Procter & Gamble Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Hyperpigmentation Treatment MarketPublished date: Sep 2025add_shopping_cartBuy Now get_appDownload Sample

Hyperpigmentation Treatment MarketPublished date: Sep 2025add_shopping_cartBuy Now get_appDownload Sample -

-

- Galderma S.A.

- L'Oréal S.A.

- AbbVie Inc.

- Obagi Cosmeceuticals LLC

- Johnson & Johnson

- Unilever plc

- The Ordinary (DECIEM)

- Beiersdorf AG

- Candela Medical

- Pierre Fabre Dermo-Cosmétique

- ISDIN

- Lumenis Be Ltd.

- Cynosure LLC

- Alma Lasers Ltd.

- Cutera Inc.

- Fotona d.o.o.

- Sciton Inc.

- Syneron Medical Ltd.

- Strata Skin Sciences Inc.

- Procter & Gamble

Our Clients

- 157822

- Sep 2025