Quick Navigation

Report Overview

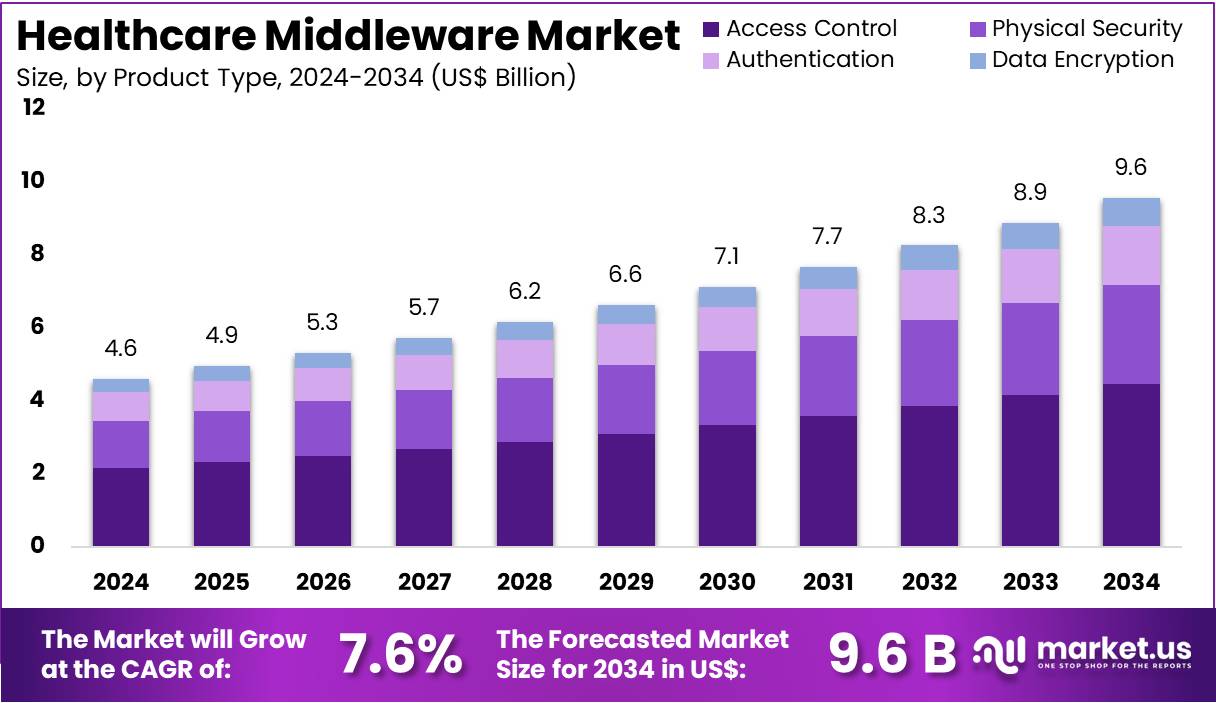

The Healthcare Middleware Market Size is expected to be worth around US$ 9.6 billion by 2034 from US$ 4.6 billion in 2024, growing at a CAGR of 7.6% during the forecast period 2025 to 2034.

Increasing demand for efficient data management in healthcare drives the adoption of healthcare middleware solutions, which act as vital intermediaries to enable seamless communication among disparate healthcare systems and applications. Middleware supports critical functions such as data integration, interoperability, workflow automation, and real-time data exchange across electronic health records (EHRs), laboratory information systems, imaging devices, and billing platforms.

The partnership between COPE Health Solutions’ Analytics for Risk Contracting (ARC) and CareJourney in March 2022 highlights the growing trend of leveraging middleware to consolidate diverse healthcare data, including claims, EHRs, lab results, and social determinants of health, into unified analytics platforms. These integrations facilitate more accurate cost and utilization assessments and improve population health management. Healthcare providers increasingly rely on middleware to streamline clinical workflows, enhance patient care coordination, and comply with regulatory requirements.

Recent innovations include the use of cloud-based middleware, API-enabled integration, and artificial intelligence to boost data processing capabilities and predictive analytics. Middleware solutions present significant opportunities to enhance decision-making, optimize resource allocation, and support value-based care initiatives. As healthcare ecosystems evolve, middleware remains a critical enabler of digital transformation, facilitating a connected and efficient healthcare infrastructure that drives improved patient outcomes and operational excellence.

Key Takeaways

- In 2024, the market for healthcare middleware generated a revenue of US$ 4.6 billion, with a CAGR of 7.6%, and is expected to reach US$ 9.6 billion by the year 2034.

- The product type segment is divided into physical security, access control, authentication, and data encryption, with access control taking the lead in 2024 with a market share of 46.7%.

- Considering technology, the market is divided into cloud-based, on-premise, and hybrid. Among these, cloud-based held a significant share of 53.2%.

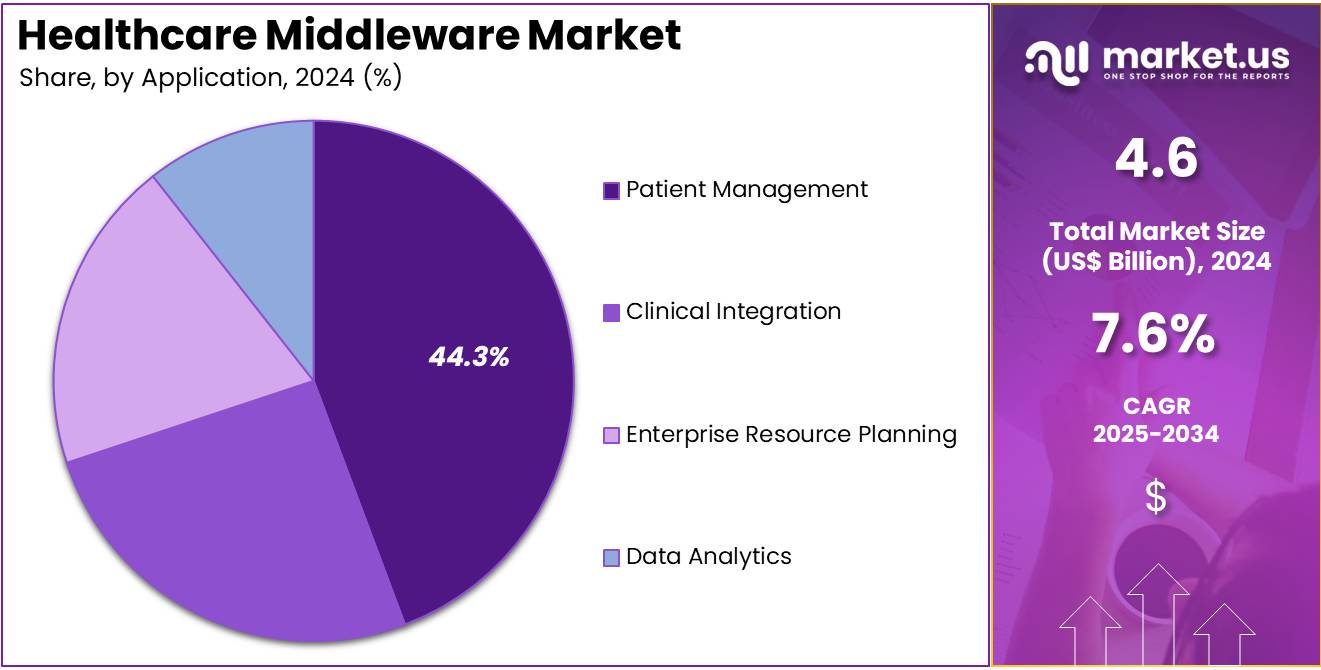

- Furthermore, concerning the application segment, the market is segregated into clinical integration, patient management, enterprise resource planning, and data analytics. The patient management sector stands out as the dominant player, holding the largest revenue share of 44.3% in the healthcare middleware market.

- The format segment is segregated into health level 7 (HL7), fast healthcare interoperability resources (FHIR), and digital imaging and communications in medicine (DICOM), with the health level 7 (HL7) segment leading the market, holding a revenue share of 49.1%.

- Considering end-user, the market is divided into hospitals & clinics, pharmaceutical companies, insurance companies, and healthcare providers. Among these, hospitals & clinics held a significant share of 57.8%.

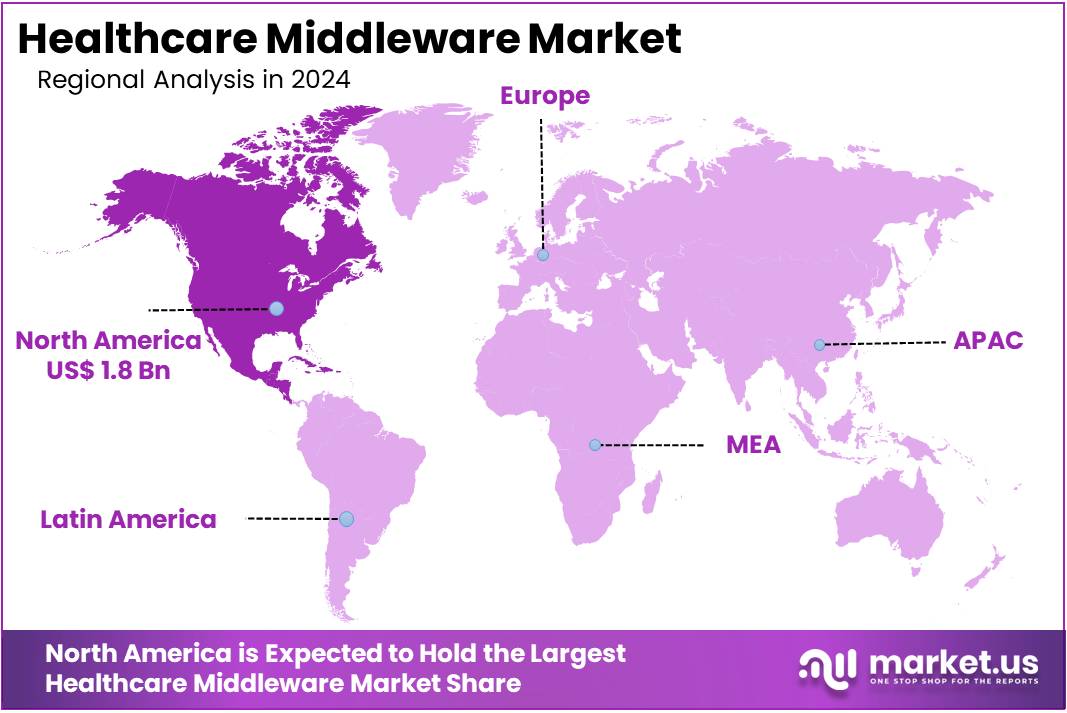

- North America led the market by securing a market share of 53.2% in 2024.

Product Type Analysis

The access control segment claimed a market share of 46.7% owing to escalating concerns over data security and patient privacy. Healthcare organizations face increasing regulatory pressure to safeguard sensitive information, making access control systems indispensable for restricting unauthorized entry to both physical and digital assets. The rise in cyber threats targeting healthcare infrastructures drives demand for robust authentication and identity management solutions.

Moreover, integration of access control with other security technologies enhances operational efficiency by automating user permissions and auditing processes. Advancements in biometric and multi-factor authentication further propel the segment’s adoption. As healthcare providers prioritize compliance with data protection laws and seek to prevent breaches, the access control segment will likely maintain strong momentum within security-focused middleware solutions.

Technology Analysis

The cloud-based held a significant share of 53.2% due to its scalability, cost-effectiveness, and flexibility in managing complex healthcare data ecosystems. Cloud deployments offer healthcare providers seamless access to integration tools without significant upfront investments in IT infrastructure. Increasing adoption of telemedicine and mobile health applications also fuels demand for cloud-based middleware solutions that facilitate real-time data exchange across distributed networks.

Additionally, cloud platforms simplify compliance with evolving healthcare regulations by enabling centralized security updates and disaster recovery options. The ability to scale resources on demand supports fluctuating workloads typical in healthcare settings. As interoperability and digital transformation initiatives accelerate, the cloud-based segment will likely become the preferred technology choice for middleware deployment.

Application Analysis

The patient management segment had a tremendous growth rate, with a revenue share of 44.3% as providers increasingly focus on enhancing patient outcomes through coordinated care. Middleware solutions that streamline patient data integration across scheduling, electronic health records, and billing systems improve operational efficiency and reduce administrative errors. Rising demand for personalized treatment plans and chronic disease management drives adoption of patient management tools embedded within middleware platforms.

Furthermore, value-based care models emphasize patient-centric workflows, which middleware supports by enabling seamless communication among care teams. The integration of analytics into patient management allows for better resource allocation and quality monitoring. These factors collectively stimulate growth in this critical application area of healthcare middleware.

Format Analysis

The health level 7 (HL7) segment grew at a substantial rate, generating a revenue portion of 49.1% due to its widespread acceptance as a standard for clinical data exchange. HL7 protocols enable interoperability between disparate healthcare systems, allowing real-time sharing of patient information, lab results, and clinical documentation. Increasing regulatory emphasis on data standardization and meaningful use compliance encourages providers to adopt HL7-based middleware solutions.

The format’s compatibility with emerging technologies such as FHIR also supports its continued relevance in integration architectures. Moreover, healthcare organizations seek middleware that ensures seamless communication among electronic health record systems, diagnostics, and pharmacy applications. As interoperability becomes central to healthcare digitization, HL7’s robust framework will maintain its leadership in middleware formats.

End-user Analysis

The hospitals & clinics held a significant share of 57.8% as these institutions manage vast volumes of patient and administrative data requiring integration across multiple departments. Increasing demand for comprehensive patient care coordination encourages hospitals and clinics to invest in middleware that facilitates seamless data exchange between electronic health records, diagnostic devices, and billing systems.

Regulatory mandates and reimbursement models tied to data accuracy and timely reporting further drive adoption. The rising trend of adopting cloud-based and mobile-enabled middleware solutions enhances real-time access to critical information. Additionally, hospitals seek middleware platforms that support interoperability and security to protect sensitive health data. These factors collectively position hospitals & clinics as key growth drivers within the healthcare middleware market.

Key Market Segments

By Product Type

- Physical Security

- Access Control

- Authentication

- Data Encryption

By Technology

- Cloud-based

- On-premise

- Hybrid

By Application

- Clinical Integration

- Patient Management

- Enterprise Resource Planning

- Data Analytics

By Format

- Health Level 7 (HL7)

- Fast Healthcare Interoperability Resources (FHIR)

- Digital Imaging and Communications in Medicine (DICOM)

By End-user

- Hospitals & Clinics

- Pharmaceutical Companies

- Insurance Companies

- Healthcare Providers

Drivers

The growing complexity of healthcare IT ecosystems is driving the market

The increasing complexity of healthcare IT ecosystems is a primary driver for the healthcare middleware market. Modern healthcare organizations utilize a vast and expanding array of disparate software applications, electronic health records (EHRs), medical devices, and administrative systems. These systems often operate on different platforms, use varying data formats, and require seamless communication to ensure efficient operations, coordinated patient care, and accurate data analytics.

Healthcare middleware acts as an essential intermediary, enabling these diverse systems to interact effectively by translating and routing data. Without robust middleware solutions, managing the interoperability challenges inherent in such complex environments would be extremely difficult and resource-intensive, making it indispensable for digital transformation initiatives in healthcare. As a reflection of this growing complexity and investment, US national health expenditures increased by 7.5% in 2023, reaching US$ 4.9 trillion, signaling the continuous evolution and investment in the broader healthcare landscape that necessitates underlying IT infrastructure like middleware.

Restraints

High implementation costs and the scarcity of specialized IT talent are restraining the market

High implementation costs and the scarcity of specialized IT talent are significantly restraining the healthcare middleware market. Deploying and configuring middleware solutions within complex healthcare environments often requires substantial upfront investment in software licenses, infrastructure, and expert consultation.

Furthermore, effectively managing, customizing, and maintaining these solutions demands a specialized IT workforce with deep knowledge of healthcare data standards, integration protocols, and cybersecurity best practices. The ongoing shortage of skilled healthcare IT professionals, particularly those with expertise in integration and middleware technologies, poses a considerable challenge. This scarcity increases labor costs and extends project timelines, making it difficult for healthcare organizations to fully leverage middleware’s benefits or even initiate necessary integration projects.

Opportunities

The rising demand for real-time data exchange and advanced analytics is creating growth opportunities

The rising demand for real-time data exchange and advanced analytics is creating significant growth opportunities in the market. Healthcare providers and payers increasingly need immediate access to comprehensive patient data from various sources to support clinical decision-making, population health management, and value-based care models. Middleware facilitates this real-time data flow, acting as a crucial layer that connects data sources to analytics platforms and reporting tools.

The ability to collect, process, and deliver timely, accurate insights from integrated data is essential for improving patient outcomes, identifying trends, and optimizing operational efficiencies. This growing emphasis on data-driven healthcare is driving the demand for advanced middleware solutions capable of handling large volumes of diverse data.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors profoundly influence the healthcare middleware market. Economic conditions directly impact healthcare organizations’ IT budgets, affecting their capacity to invest in complex software solutions; economic prosperity generally encourages greater expenditure on digital transformation initiatives, including middleware, while downturns can lead to budget cuts and delayed projects.

Geopolitical instability can disrupt global supply chains for critical IT hardware that underpins middleware deployments, causing price volatility and extended lead times for equipment necessary for robust infrastructure. For instance, in 2023, the US imported approximately US$ 104 billion in automatic data processing machines (HTS 8471), which include servers and components vital for these systems.

Despite potential challenges from economic fluctuations and supply chain disruptions, the unwavering imperative for healthcare interoperability, patient data accessibility, and digital transformation ensures a resilient demand for these essential software layers, prompting organizations to prioritize efficiency and strategic investment in core IT capabilities.

Current U.S. tariff policies can indirectly influence the healthcare middleware market by raising the cost of necessary IT infrastructure. Although middleware is software-based, its functionality depends on physical components like servers, networking tools, and storage devices. Many of these are imported and fall under tariffed categories. As a result, healthcare providers and cloud service vendors face higher procurement costs. These expenses can raise the total project budget or increase the ongoing operational cost of running middleware platforms within healthcare systems.

Tariffs on IT hardware—particularly those listed under the Harmonized Tariff Schedule (HTS), such as HTS 8471 for automatic data processing machines—can significantly affect capital expenditure. This cost escalation becomes a burden when healthcare institutions plan to deploy or scale middleware solutions. Middleware enables data exchange between disparate healthcare systems. However, rising hardware costs may delay deployments or reduce budgets for integration projects. This puts financial pressure on providers looking to modernize IT systems.

Despite cost concerns, the demand for healthcare middleware remains strong. The need for real-time data sharing, system integration, and interoperability continues to drive market investment. Healthcare organizations are responding by exploring non-tariffed supply sources and optimizing current infrastructure. These strategic adjustments help reduce cost impact while maintaining system efficiency. As interoperability remains a regulatory and clinical priority, middleware investments are expected to continue.

Latest Trends

The shift towards cloud-native and API-led architectures is a recent trend

The shift towards cloud-native and API-led architectures is a significant recent trend in the market. Healthcare organizations are increasingly migrating their IT infrastructure and applications to cloud environments to benefit from scalability, flexibility, and reduced operational overhead. This transition necessitates middleware solutions that are designed for cloud deployments, capable of integrating cloud-based applications with on-premise systems, and leveraging microservices architectures for greater agility.

Additionally, the adoption of Application Programming Interfaces (APIs), particularly those based on open standards like FHIR, is becoming central to modern integration strategies. Middleware plays a critical role in managing these APIs, ensuring secure and efficient data exchange between interconnected healthcare systems and applications.

Oracle, a major provider of middleware and cloud services, reported that its Cloud Infrastructure (IaaS) revenue grew by 52% in the second quarter of fiscal year 2025 (ending November 30, 2024), reflecting the strong industry movement towards cloud adoption, which includes the foundational middleware layer.

Regional Analysis

North America is leading the Healthcare Middleware Market

North America dominated the market with the highest revenue share of 39.2% owing to the increasing need for seamless data exchange and interoperability among diverse healthcare IT systems. The US Department of Health & Human Services (HHS) continues to push for greater interoperability to improve patient care coordination. The Office of the National Coordinator for Health Information Technology (ONC) actively supports the development and adoption of standards for health information exchange.

The widespread implementation of Electronic Health Records (EHRs), with a high adoption rate among US hospitals as reported by the ONC, necessitates robust middleware solutions to facilitate data flow between these systems and other applications. This demand for efficient data integration across the healthcare ecosystem is fueling the expansion of the middleware market.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to the increasing adoption of digital health technologies and the growing focus on establishing interconnected healthcare systems across the region. Governments in the Asia Pacific are investing in national digital health initiatives that require effective middleware for data integration.

For instance, the development of health information exchange platforms is underway in several countries. The rising number of hospitals and healthcare facilities, coupled with the increasing implementation of EHRs and other healthcare applications, is expected to drive the demand for solutions that enable seamless communication and data sharing among these systems.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the healthcare middleware market pursue growth by developing flexible integration platforms that support interoperability across diverse healthcare systems. They invest in strategic collaborations and acquisitions to expand their technological capabilities and market reach. Emphasizing data security and compliance with healthcare regulations remains a priority to maintain customer confidence. Companies also focus on innovation by incorporating AI and cloud-based solutions to enhance real-time data processing and analytics.

Oracle Corporation, a major player in this market, offers comprehensive middleware solutions designed to streamline data exchange and application integration in healthcare environments. Established in 1977, Oracle serves a global clientele across various industries, providing robust platforms that improve operational efficiency and support digital transformation initiatives within healthcare organizations.

Top Key Players in the Healthcare Middleware Market

- 3M

- Athenahealth

- Cerner

- eHealth Technologies

- GE Healthcare

- McKesson Corporation

- Microsoft

- Oracle Corporation

Recent Developments

- In March 2022: Microsoft launched Azure Health Data Services, a platform-as-a-service offering developed to help healthcare organizations effectively manage their data. This service allows users to upload, store, and analyze healthcare information while supporting widely accepted standards such as FHIR (Fast Healthcare Interoperability Resources) and DICOM (Digital Imaging and Communications in Medicine). The platform has been recognized for strengthening data interoperability and streamlining data workflows across healthcare systems.

- In April 2021: 3M Health Information Systems introduced a new technology platform aimed at assisting healthcare providers and payers in optimizing care delivery and resource utilization. The solution was developed to support clinical decision-making and enhance operational efficiency within healthcare environments.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 4.6 billion |

| Forecast Revenue (2034) | US$ 9.6 billion |

| CAGR (2025-2034) | 7.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Physical Security, Access Control, Authentication, and Data Encryption), By Technology (Cloud-based, On-premise, and Hybrid), By Application (Clinical Integration, Patient Management, Enterprise Resource Planning, and Data Analytics), By Format (Health Level 7 (HL7), Fast Healthcare Interoperability Resources (FHIR), and Digital Imaging and Communications in Medicine (DICOM)), By End-user (Hospitals & Clinics, Pharmaceutical Companies, Insurance Companies, and Healthcare Providers) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | 3M, Athenahealth, Cerner, eHealth Technologies, GE Healthcare, McKesson Corporation, Microsoft, and Oracle Corporation. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |