Quick Navigation

Report Overview

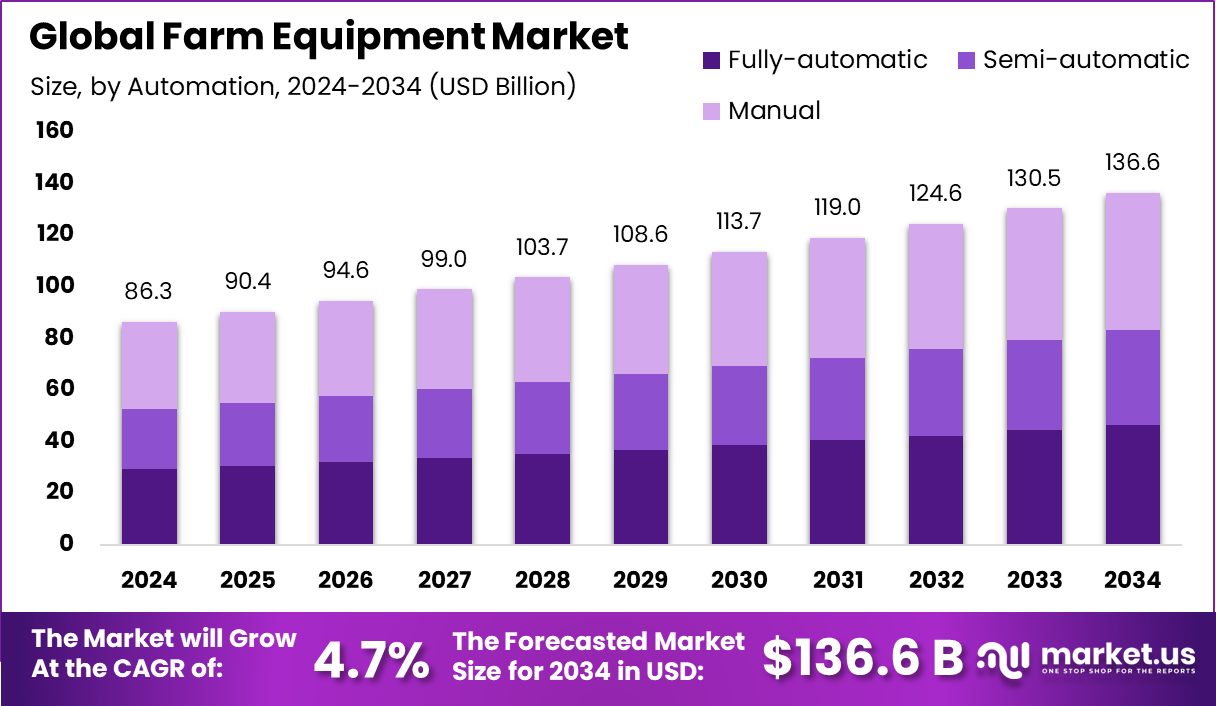

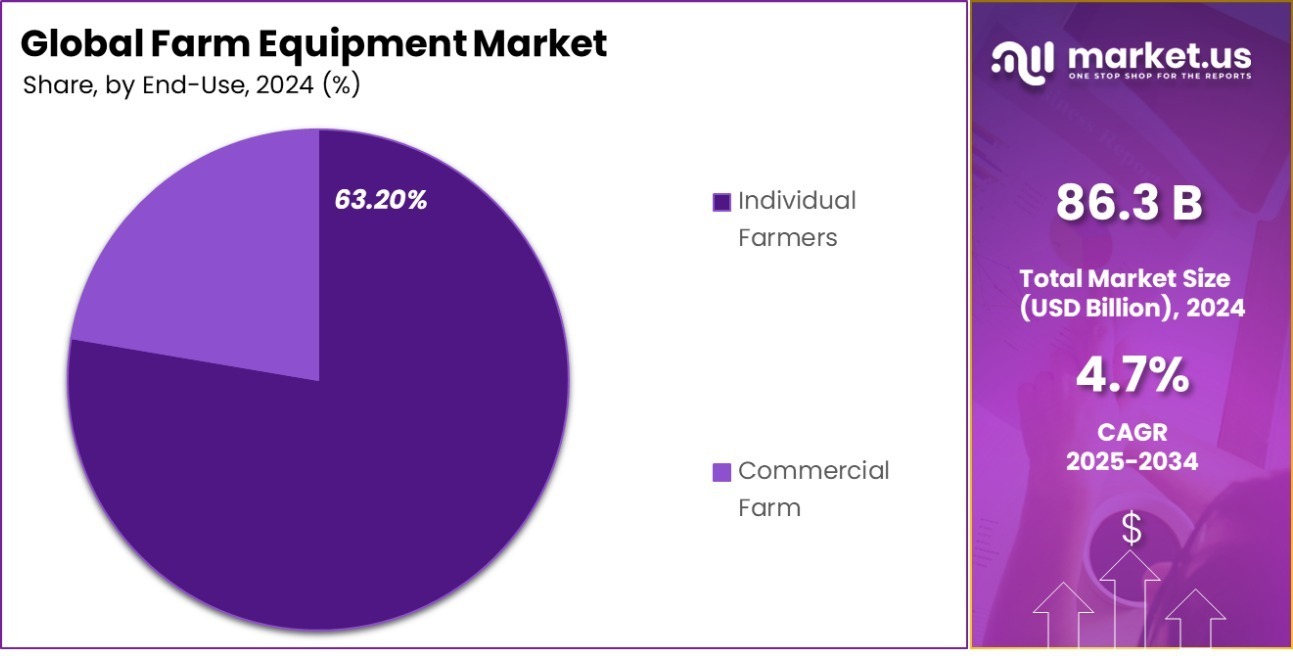

Global Farm Equipment Market is expected to be worth around USD 136.6 billion by 2034, up from USD 86.3 billion in 2024, and grow at a CAGR of 4.7% from 2025 to 2034. Strong agricultural activity and mechanization in Asia-Pacific drive the market’s 53.20% and USD 45.9 billion size.

Farm equipment refers to the machinery and tools used in agriculture to enhance the efficiency and effectiveness of farming operations. This equipment ranges from basic hand tools to complex machinery like tractors, harvesters, and irrigation systems. The purpose of farm equipment is to assist in various agricultural processes, including planting, irrigation, harvesting, and crop processing, thereby reducing labor and increasing productivity.

The farm equipment market encompasses the sale and manufacture of machinery designed for agricultural use. This market is driven by the rising demand for food products, advancements in agricultural technology, and the integration of smart technologies into farming practices.

SS Tractor Factory, a pre-owned tractor and farm equipment platform, secured ₹4 crore (~$500,000) in pre-seed funding led by All In Capital, with Bharat Founders Fund, Devc, and angel investors participating. The funds will boost technology, customer experience, and market reach. With a ₹1,000 crore revenue target in three years, it rides on India’s 11.31% tractor sales surge in January 2025, where M&M clocked 14.51% growth.

One major growth factor for the farm equipment market is technological innovation, which includes the development of automated and GPS-enabled machinery. These advancements improve crop yields and efficiency, attracting investment from farming operations looking to optimize their processes.

Demand in the farm equipment market is primarily driven by the increasing need for food production to support a growing global population. As urbanization continues and arable land decreases, there is a pressing need to enhance the productivity of existing agricultural lands. This necessity pushes farmers towards adopting modern equipment that can achieve higher outputs with less time and effort.

Key Takeaways

- Global Farm Equipment Market is expected to be worth around USD 136.6 billion by 2034, up from USD 86.3 billion in 2024, and grow at a CAGR of 4.7% from 2025 to 2034.

- Manual automation holds a 39.20% share, reflecting traditional practices still prevalent among farmers.

- Tractors dominate the equipment type in the farm equipment market, accounting for a strong 67.20% market share.

- The 31-70 HP power output range contributes 32.10%, ideal for mid-scale farming operations globally.

- Cultivation and soil preparation lead applications in farm equipment, capturing 36.70% market usage.

- Individual farmers represent the majority of end-users in this market, contributing a notable 63.20% share.

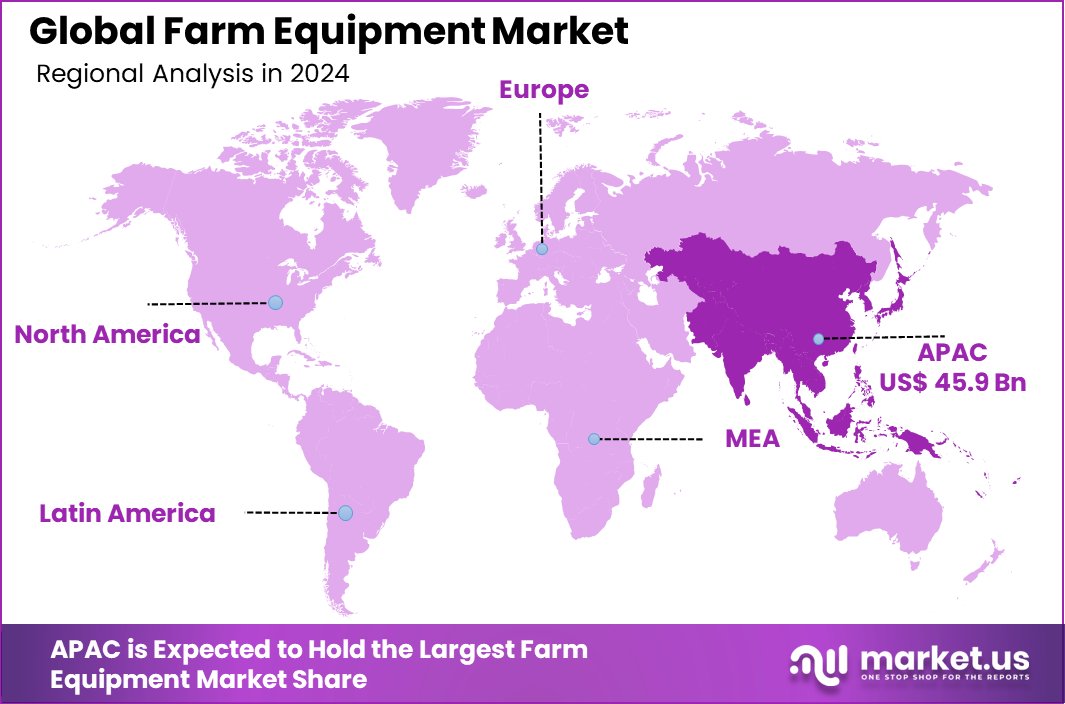

- In 2024, the Asia-Pacific farm equipment market reached a value of USD 45.9 billion.

By Automation Analysis

Manual automation accounts for 39.20%, indicating continued reliance on traditional methods.

In 2024, Manual held a dominant market position in the By Automation segment of the Farm Equipment Market, with a 39.20% share. This leadership can be attributed to its affordability, ease of maintenance, and widespread adoption among small to medium-sized farms, particularly in developing regions.

Manual equipment continues to be a practical choice in areas where large-scale mechanization remains economically unfeasible. Moreover, the preference for manual tools persists in fragmented landholdings, where advanced machinery cannot operate efficiently. Farmers in the Asia-Pacific, Latin America, and parts of Africa continue to rely heavily on manual farm equipment due to lower operational costs and minimal training requirements.

Although automation technologies are gaining traction, manual systems remain resilient due to their reliability and adaptability across various terrains. Additionally, seasonal farming and labor availability influence the selection of manual over automated solutions.

Even in regions witnessing mechanization, many farmers retain manual tools for supplementary tasks, ensuring continued demand. The segment’s prominence highlights a dual-approach strategy in agricultural practices—balancing traditional tools with emerging automation.

By Equipment Type Analysis

Tractors dominate equipment sales, contributing a significant 67.20% of the market share.

In 2024, Tractors held a dominant market position in the By Equipment Type segment of the Farm Equipment Market, with a 67.20% share. This overwhelming share reflects the critical role tractors play in modern farming operations, serving as a multipurpose tool for a wide range of agricultural tasks.

Their usage spans plowing, tilling, harrowing, planting, and hauling, making them indispensable for both small-scale and commercial farms. The high demand for tractors is driven by their efficiency in reducing manual labor and increasing productivity, especially in large-scale farmlands.

Regions with expanding mechanization trends, such as Asia-Pacific and North America, have contributed significantly to this dominance. Farmers increasingly invest in tractors due to rising labor costs and the growing need for timely field operations.

Additionally, government subsidies and rural credit schemes supporting tractor purchases have fueled adoption in emerging markets. The integration of basic technology in entry-level tractors makes them accessible to small and marginal farmers, further driving volume sales.

By Power Output Analysis

Power output of 31–70 HP holds 32.10% market share globally.

In 2024, 31–70 HP held a dominant market position in the By Power Output segment of the Farm Equipment Market, with a 32.10% share. This segment’s strong performance is largely due to its versatility and suitability for a wide range of agricultural applications across small to medium-sized farms. Equipment in this power range offers a balanced mix of performance and affordability, making it a preferred choice for farmers in both developed and emerging economies.

The 31–70 HP tractors and machines are well-suited for key tasks such as tilling, plowing, spraying, and light-duty hauling, especially in crops like cereals, vegetables, and fruits. Their compact size allows easier maneuverability in smaller or uneven fields while still delivering adequate power for core farming activities.

The popularity of this segment is particularly noticeable in regions such as Asia-Pacific and Latin America, where fragmented landholdings dominate agricultural landscapes.

Incentives and government-backed programs supporting farm mechanization in these regions have further boosted demand for mid-range horsepower equipment. Farmers are increasingly leaning toward this power band for its cost-efficiency and operational flexibility.

By Application Analysis

Cultivation and soil preparation lead applications with 36.70% usage in farming equipment.

In 2024, Cultivation and Soil Preparation held a dominant market position in the By Application segment of the Farm Equipment Market, with a 36.70% share. This significant share reflects the fundamental role of soil preparation in ensuring healthy crop growth and maximizing yield. Equipment used for tilling, plowing, harrowing, and leveling is essential in creating optimal soil conditions, which directly influences seeding success and nutrient availability.

The demand for cultivation and soil preparation machinery remains high across all farming regions, especially in areas with seasonal cropping and varied soil structures. The segment’s growth is fueled by the increasing need to boost farm productivity and efficiency, particularly in the face of shrinking arable land and rising food demand.

Small to medium farms, especially in Asia-Pacific and parts of Africa, rely heavily on these machines to improve soil structure and manage residues from previous harvests. Moreover, advancements in mechanized tools for primary and secondary tillage operations have enhanced performance, reduced labor costs, and improved operational speed.

By End-use Analysis

Individual farmers represent 63.20% of the end-use market for farm equipment.

In 2024, Individual Farmers held a dominant market position in the by-end-use segment of the Farm Equipment Market, with a 63.20% share. This significant contribution is primarily driven by the increasing trend of farm mechanization among small and mid-scale farmers, particularly in developing regions.

The affordability of compact and mid-range equipment has enabled more individual farmers to invest in modern tools, enhancing their productivity and operational efficiency. The rising adoption of precision farming practices and GPS-guided machinery further supports this growth among individual end-users.

Moreover, favorable government subsidies, loan facilities, and technical training programs tailored for individual agricultural workers have significantly boosted market penetration in this category.

However, the continued dominance of individual farmers underscores a decentralized yet robust demand base, especially in economies where small-scale farming forms the backbone of agricultural output. The 2024 data reflects how the empowerment of individual cultivators is reshaping demand dynamics across the global farm equipment landscape.

Key Market Segments

By Automation

- Fully-automatic

- Semi-automatic

- Manual

By Equipment Type

- Tractors

- Combines

- Sprayers

- Balers

- Other

By Power Output

- Upto 30 HP

- 31-70 HP

- 71-130 HP

- 131-250 HP

- Above 250 HP

By Application

- Cultivation and Soil Preparation

- Planting and Seeding

- Harvesting

- Livestock

- Others

By End-use

- Individual Farmers

- Commercial Farm

Driving Factors

Rising Mechanization in Farming Boosts Equipment Demand

One of the biggest reasons behind the growth of the farm equipment market is rising mechanization. Across many countries, farmers are shifting from manual labor to machines for faster and more efficient farming.

This is especially true in countries like India, Brazil, and China, where the government is promoting modern agriculture. Tractors, harvesters, seed drills, and irrigation tools are becoming more common in small and medium farms.

These machines help save time, reduce labor costs, and increase productivity per acre. As food demand grows with population, farmers need to produce more in less time—making farm equipment essential. Also, better access to loans and subsidies is making it easier for farmers to buy equipment and upgrade old tools.

Restraining Factors

High Equipment Costs Limit Small Farmer Adoption

A major challenge in the farm equipment market is the high cost of machines. Tractors, harvesters, and advanced tools are often too expensive for small and medium-sized farmers, especially in developing countries.

Many farmers still rely on traditional methods because they cannot afford new machinery. Even with government subsidies or loans, the upfront cost, maintenance, fuel, and spare parts can be overwhelming.

This financial burden slows down the adoption of modern equipment. Also, in rural areas, limited access to financing or leasing options makes it harder to invest in new technology. Unless affordable solutions or rental services are provided widely, the growth of the farm equipment market will remain limited in cost-sensitive regions.

Growth Opportunity

Growing Demand for Smart Farming Equipment Solutions

One big growth opportunity in the farm equipment market is smart farming technology. Farmers are starting to use GPS-guided tractors, drones, sensors, and software that collect and analyze farm data.

These smart tools help farmers plan better, save on seeds and fertilizers, and grow more crops with fewer resources. As digital technology becomes more affordable and internet access improves in rural areas, more farmers are willing to try precision farming tools.

Companies offering user-friendly, connected equipment have a big chance to grow in this space. Governments are also supporting smart farming through policies and training programs. This shift toward digital agriculture is opening up new doors for farm equipment manufacturers focused on innovation and sustainability.

Latest Trends

Autonomous Tractors Gaining Traction in Agriculture

One of the newest trends in the farm equipment market is the rise of autonomous tractors. These self-driving machines use GPS, cameras, and sensors to operate without a driver. Farmers can control them remotely or set them to follow a fixed path.

This helps save labor, reduce human errors, and improve efficiency—especially during planting or harvesting seasons. Big companies like John Deere and CNH Industrial are already testing and launching such equipment.

As labor shortages grow in many countries, especially in the U.S. and Europe, demand for autonomous solutions is rising. While the technology is still expensive, its long-term benefits are encouraging adoption. Over the next few years, autonomous tractors could change how farms operate globally.

Regional Analysis

Asia-Pacific holds the largest farm equipment market share, accounting for 53.20% of global demand.

The global farm equipment market shows strong regional variation, with Asia-Pacific emerging as the dominant region. Holding a substantial 53.20% share of the global market, Asia-Pacific accounted for a value of USD 45.9 billion in 2024.

This dominance is driven by the region’s large agricultural base, increasing mechanization in countries like India and China, and supportive government subsidies that encourage the adoption of modern farming machinery.

In contrast, North America and Europe maintain mature markets with a steady demand for technologically advanced equipment, including precision farming tools and autonomous tractors. These regions benefit from high farm income levels and strong infrastructure but exhibit slower growth compared to Asia-Pacific.

Meanwhile, Latin America is showing moderate growth due to expanding commercial farming in countries such as Brazil and Argentina. The Middle East & Africa remains a developing region in this space, with gradual adoption driven by irrigation equipment and basic machinery due to the arid climate and growing food security concerns. However, limited access to financing in the MEA remains a barrier.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, the global farm equipment market saw strong positioning from leading players like AGCO Corporation, Alamo Group, Autonomous Solutions, and Case IH. These companies continued to shape the competitive landscape through innovation, product expansion, and regional penetration strategies.

AGCO Corporation remained a key force with its portfolio of brands like Fendt, Massey Ferguson, and Valtra. The company focused heavily on precision agriculture technologies and smart machinery, aligning with the global trend toward digital farming. Its investments in data-driven equipment, along with increased demand from Asia-Pacific and North America, supported its strong performance.

Alamo Group maintained its relevance through specialized agricultural machinery and attachments. Known for durable and cost-effective equipment, the group focused on mid-sized farms and municipal markets. In 2024, its performance was steady, especially in North America and Latin America, where demand for mowing and vegetation management equipment remained strong.

Autonomous Solutions gained traction by focusing on autonomy in farm equipment. The company stood out by offering retrofit kits and fully autonomous solutions that appealed to progressive farms in the U.S., Canada, and parts of Europe. With labor shortages impacting traditional farming, Autonomous Solutions positioned itself well to address this gap.

Case IH, a brand under CNH Industrial, continued to lead in high-horsepower tractors and harvesting equipment. With strong dealer networks and technology partnerships, Case IH grew its footprint in both emerging and developed regions. Its push toward sustainable equipment further strengthened its global standing.

Top Key Players in the Market

- AGCO Corporation.

- Alamo Group Autonomous Solutions

- Case IH

- CLAAS

- Daedong Industrial Co. Ltd

- Deere & Company,

- Escorts Limited

- Iseki & Co. Ltd

- JCB

- Kubota Corporation

- KUHN SAS

- Mahindra and Mahindra Limited

- Minsk Tractor Works

- New Holland

- Sonalika

- Tractors and Farm Equipment Limited

Recent Developments

- In 2024, Case IH faced a tough year with a 22% drop in sales, reaching $14 billion. Shipments slowed, dealer inventories shrank, and Q4 sales alone fell 31%. The company is now cutting production to match lower market demand.

- In 2023, JCB designs and manufactures farm and construction equipment like backhoe loaders, tractors, and telehandlers. Also they increased profits to £805.8 million. Despite global slowdowns, JCB focused on innovation, electric machinery, and expanding sales in India and North America.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 86.3 Billion |

| Forecast Revenue (2034) | USD 136.6 Billion |

| CAGR (2025-2034) | 4.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Automation (Fully-automatic, Semi-automatic, Manual), By Equipment Type (Tractors, Combines, Sprayers, Balers, Other), By Power Output(Upto 30 HP, 31-70 HP, 71-130 HP, 131-250 HP, Above 250 HP), By Application (Cultivation and Soil Preparation, Planting and Seeding, Harvesting, Livestock, Others), By End-use(Individual Farmers, Commercial Farm) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | AGCO Corporation., Alamo Group Autonomous Solutions, Case IH, CLAAS, Daedong Industrial Co. Ltd, Deere & Company,, Escorts Limited, Iseki & Co. Ltd, JCB, Kubota Corporation, KUHN SAS, Mahindra and Mahindra Limited, Minsk Tractor Works, New Holland, Sonalika, Tractors and Farm Equipment Limited |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |