Quick Navigation

Report Overview

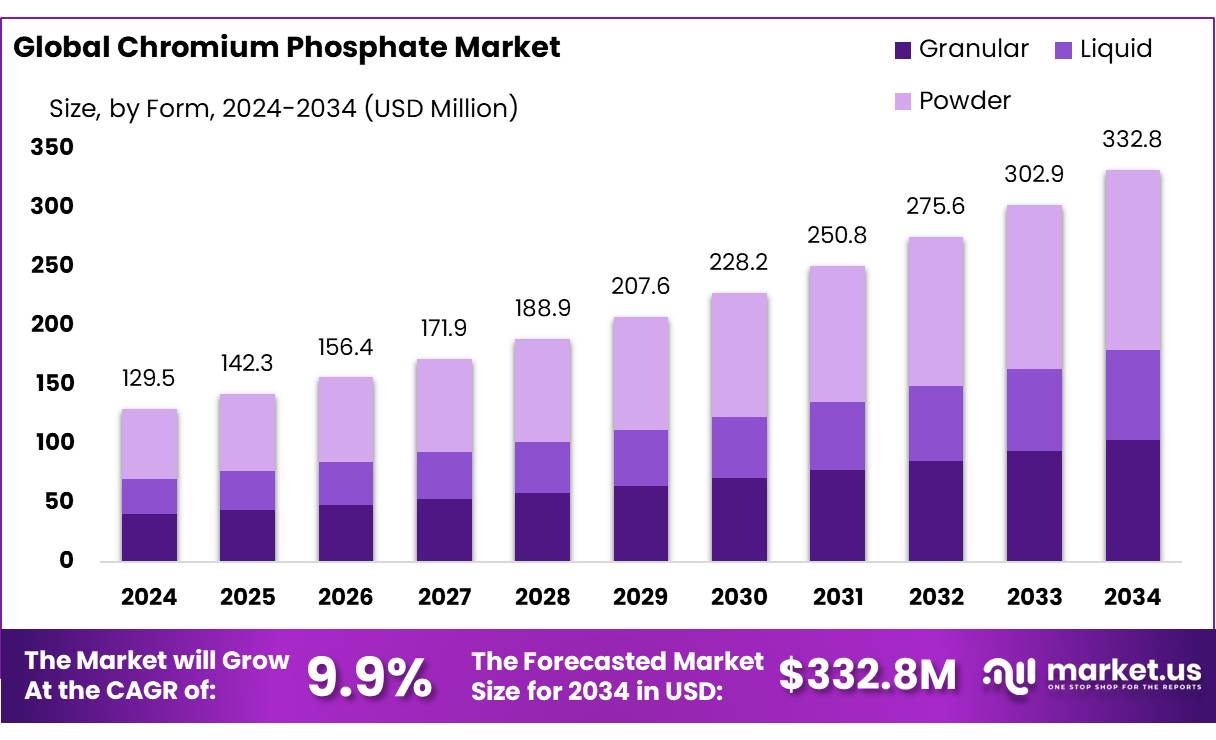

The Global Chromium Phosphate Market size is expected to be worth around USD 332.8 Million by 2034, from USD 129.5 Million in 2024, growing at a CAGR of 9.9% during the forecast period from 2025 to 2034.

Chromium phosphate is an inorganic compound increasingly recognized for its utility in various industrial applications, including its emerging role in enhancing cellulose concentrate processing. Its properties as a corrosion inhibitor, catalyst, and pigment make it valuable in sectors such as construction, automotive, and medical coatings. The integration of chromium phosphate into cellulose-based materials offers potential improvements in durability and functionality, aligning with the growing demand for advanced materials in diverse industries.

Several factors are propelling the growth of chromium phosphate in cellulose concentrates. The increasing demand for sustainable and biodegradable materials in various industries has led to the exploration of cellulose-based composites. Chromium phosphate’s ability to enhance the thermal stability and mechanical strength of cellulose materials makes it a valuable additive. Additionally, its corrosion-inhibiting properties are beneficial in extending the lifespan of cellulose-based products used in harsh environments.

Government initiatives are playing a crucial role in promoting the use of sustainable and high-performance materials. For instance, the U.S. Department of Energy supports research and development in advanced materials, including those involving chromium phosphate, to enhance energy efficiency and environmental sustainability. Similarly, the European Union’s emphasis on sustainable chemistry encourages the adoption of materials that align with environmental regulations and performance standards.

Key Takeaways

- Chromium Phosphate Market size is expected to be worth around USD 332.8 Million by 2034, from USD 129.5 Million in 2024, growing at a CAGR of 9.9%.

- Hexa-hydrated Chromium Phosphate held a dominant market position, capturing more than a 43.2% share of the global chromium phosphate market.

- Industrial Grade held a dominant market position, capturing more than a 56.3% share of the global chromium phosphate market.

- Powder held a dominant market position, capturing more than a 47.4% share in the global chromium phosphate market.

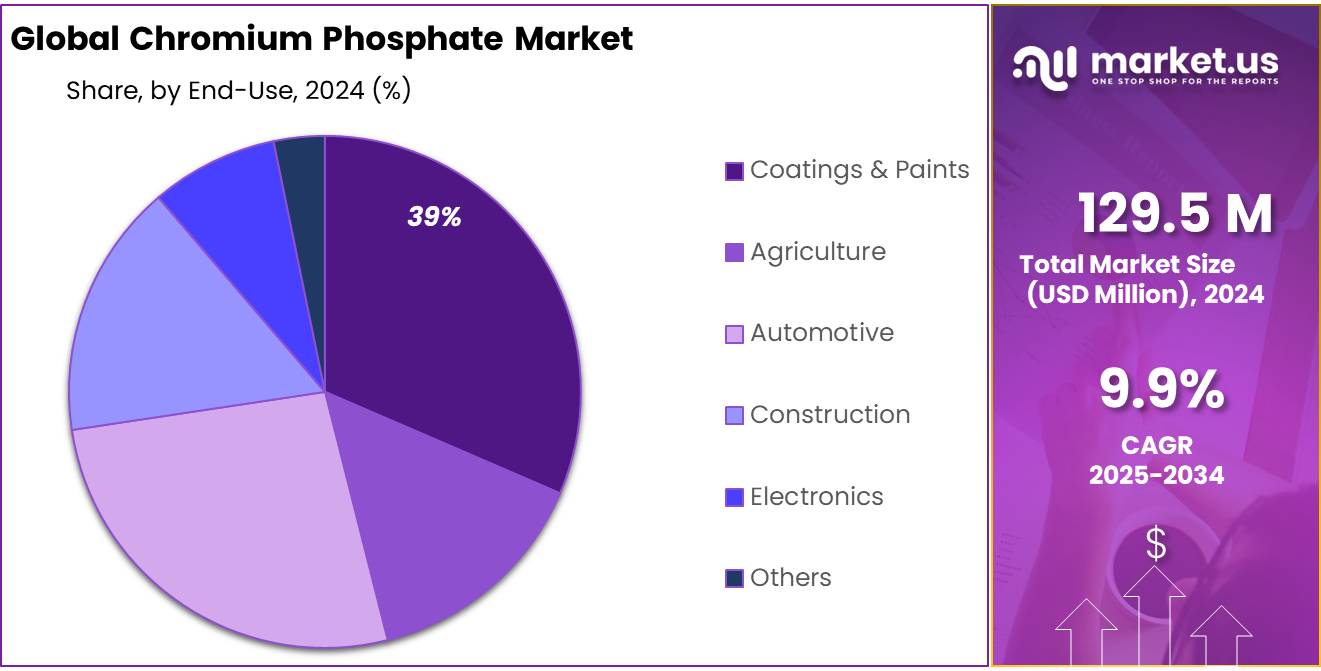

- Coatings & Paints held a dominant market position, capturing more than a 39.1% share of the global chromium phosphate market.

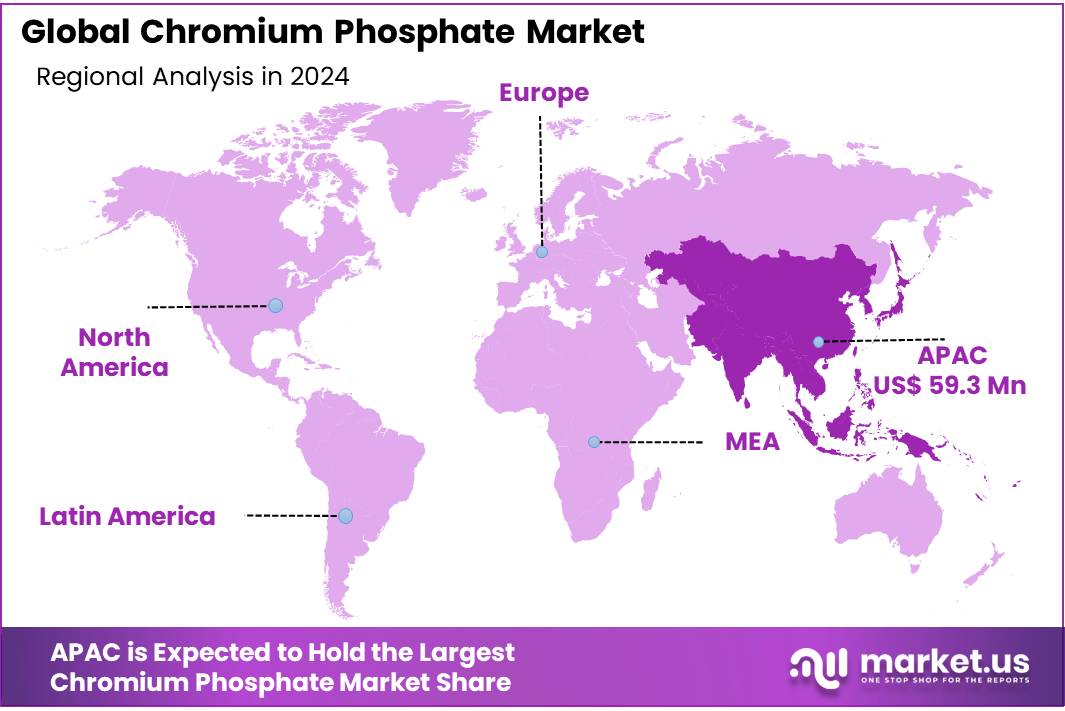

- Asia Pacific (APAC) region emerged as the dominant force in the global chromium phosphate market, securing a substantial 45.8% market share, equivalent to approximately USD 59.3 million.

By Type

Hexa-hydrated Chromium Phosphate leads with 43.2% market share in 2024, driven by its high solubility and industrial versatility.

In 2024, Hexa-hydrated Chromium Phosphate held a dominant market position, capturing more than a 43.2% share of the global chromium phosphate market. Its lead in the market can be attributed to its high solubility, stable molecular structure, and consistent performance across a wide range of industrial applications, particularly in anti-corrosion coatings and pigment formulations. The compound’s suitability for water-based systems makes it a preferred choice in environmentally compliant manufacturing processes.

Industries involved in architectural paints and protective surface treatments are increasingly adopting hexa-hydrated variants due to their ability to improve adhesion and resistance in harsh environmental conditions. Furthermore, the availability of this type at a competitive cost compared to anhydrous forms has also supported its strong uptake. As demand for durable coatings grows in construction and automotive sectors across Asia and North America, the segment is expected to retain its market dominance through 2025, supported by both performance and regulatory compliance.

By Grade

Industrial Grade leads with 56.3% share in 2024, backed by its broad usage in coatings, metallurgy, and surface treatments.

In 2024, Industrial Grade held a dominant market position, capturing more than a 56.3% share of the global chromium phosphate market. This strong performance is mainly due to its extensive use across heavy industries, especially in corrosion-resistant coatings, surface conversion treatments, and ceramic production. Industrial Grade chromium phosphate is known for its high thermal stability and compatibility with other inorganic compounds, which makes it ideal for demanding environments in sectors like automotive, construction, and aerospace.

Its affordability and ease of handling compared to specialty or pharmaceutical grades also add to its widespread appeal. Demand remains particularly strong in Asia and Europe, where infrastructure growth and metal protection requirements are fueling consumption. With steady demand across manufacturing lines and surface engineering applications, the Industrial Grade segment is expected to remain the market leader through 2025.

By Product Form

Powder form dominates with 47.4% share in 2024, favored for its ease of handling and compatibility in formulations.

In 2024, Powder held a dominant market position, capturing more than a 47.4% share in the global chromium phosphate market. This dominance is largely due to the powder form’s versatility in blending, transport, and storage, making it ideal for use in paints, coatings, and metal treatment applications.

Powdered chromium phosphate allows for precise dosing and consistent dispersion in both aqueous and solvent-based systems, which is especially important in industries focused on high-performance coatings and chemical processing. Its extended shelf life and low moisture content also make it a preferred format for bulk industrial buyers. As demand continues to grow from manufacturers across the construction and automotive sectors, the powder segment is expected to retain its lead into 2025, supported by its operational convenience and adaptability in production workflows.

By Application

Coatings & Paints lead with 39.1% market share in 2024, driven by rising demand for corrosion protection in industrial surfaces.

In 2024, Coatings & Paints held a dominant market position, capturing more than a 39.1% share of the global chromium phosphate market. This strong share is mainly due to the material’s excellent anti-corrosive and adhesion-promoting properties, which make it ideal for protective coatings on metals used in automotive, construction, and marine industries. Chromium phosphate enhances durability, resists oxidation, and supports long-term surface stability, especially in harsh environments.

Its use in primers and conversion coatings is growing as manufacturers seek more environmentally compliant and high-performance alternatives. With increasing infrastructure projects and stricter corrosion protection standards worldwide, especially in Asia and North America, the demand for chromium phosphate in coatings is expected to remain high through 2025, ensuring this segment maintains its leadership.

Key Market Segments

By Type

- Hexa-hydrated Chromium Phosphate

- Mesoporous Phase

- Films

- Amorphous Phase

By Grade

- Agricultural Grade

- Food Grade

- Industrial Grade

- Pharmaceutical Grade

By Product Form

- Granular

- Liquid

- Powder

By Application

- Coatings & Paints

- Agriculture

- Automotive

- Construction

- Electronics

- Others

Drivers

Rising Demand for Corrosion-Resistant Coatings in Infrastructure and Automotive Sectors

One of the primary drivers of the chromium phosphate market is the escalating demand for corrosion-resistant coatings, particularly in the construction and automotive industries. Chromium phosphate is extensively utilized in protective coatings due to its exceptional anti-corrosive properties, making it indispensable for safeguarding metal surfaces against environmental degradation.

In the construction sector, the surge in urbanization and infrastructure development has amplified the need for durable materials. Chromium phosphate-based coatings are favored for their ability to enhance the longevity of structures by providing robust protection against corrosion. This is especially pertinent in regions experiencing rapid industrial growth, where the integrity of buildings and infrastructure is paramount.

The automotive industry also significantly contributes to the demand for chromium phosphate. Vehicles are subjected to various environmental factors that can lead to corrosion, affecting both aesthetics and structural integrity. Chromium phosphate coatings are applied to automotive components to prevent rust and extend the lifespan of vehicles. As the global automotive market continues to expand, the requirement for effective corrosion protection solutions like chromium phosphate is anticipated to rise correspondingly.

Furthermore, governmental regulations emphasizing environmental sustainability have led to a shift towards non-toxic and eco-friendly corrosion inhibitors. Chromium phosphate serves as a safer alternative to traditional chromate-based coatings, aligning with environmental standards and reducing health hazards associated with toxic substances.

Restraints

Stringent Environmental Regulations Pose Challenges to Chromium Phosphate Market Growth

A significant challenge facing the chromium phosphate market is the increasing stringency of environmental regulations governing the production and use of chromium compounds. These regulations are primarily driven by concerns over the potential toxicity of certain chromium forms, particularly hexavalent chromium (Cr(VI)), which has been identified as carcinogenic. Although chromium phosphate typically contains trivalent chromium (Cr(III)), which is considered less harmful, the broader regulatory measures often encompass all chromium compounds, thereby impacting the entire industry.

In the United States, the Environmental Protection Agency (EPA) has established strict guidelines for chromium emissions, particularly from industrial processes. For instance, the EPA’s National Emission Standards for Hazardous Air Pollutants (NESHAP) for Chromium Electroplating and Anodizing Tanks impose stringent limits on chromium emissions to protect public health. Compliance with these standards necessitates significant investment in emission control technologies, increasing operational costs for manufacturers.

Similarly, the European Union’s Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) regulation imposes rigorous requirements on the use of chromium compounds. Under REACH, substances of very high concern (SVHCs), which include certain chromium compounds, are subject to authorization, and their use may be restricted or banned. This regulatory framework compels manufacturers to conduct comprehensive risk assessments and seek authorization for continued use, adding to the administrative and financial burden.

Opportunity

Expanding Applications in Medical Devices and Pharmaceuticals

A significant growth opportunity for the chromium phosphate market lies in its expanding applications within the medical and pharmaceutical sectors. Chromium phosphate is increasingly utilized in medical device coatings due to its antimicrobial properties, which help reduce the risk of hospital-acquired infections. This is particularly important in healthcare settings where infection control is paramount.

In addition to medical devices, chromium phosphate is being explored for its potential in pharmaceutical applications. Research indicates that chromium phosphate nanoparticles may possess anti-angiogenic properties, which could be beneficial in treating conditions like hemangioma. Furthermore, its role in inhibiting cancer cell growth and enhancing chemotherapy efficacy is under investigation, suggesting a promising avenue for future therapeutic applications.

The growth in this sector is further supported by the global increase in healthcare spending and the demand for advanced medical technologies. As populations age and the prevalence of chronic diseases rises, there is a corresponding need for medical devices and treatments that are both effective and safe. Chromium phosphate’s properties align well with these requirements, positioning it as a valuable component in the development of next-generation medical solutions.

Government initiatives aimed at promoting healthcare innovation and ensuring patient safety also contribute to this growth opportunity. Regulatory bodies are encouraging the development of materials that can improve the performance and safety of medical devices, creating a favorable environment for the adoption of chromium phosphate in this field.

Trends

Shift Towards Eco-Friendly Alternatives in Coatings and Surface Treatments

A notable trend in the chromium phosphate market is the increasing shift towards environmentally friendly alternatives in coatings and surface treatments. Industries are moving away from hazardous materials such as hexavalent chromium, aligning with stricter environmental regulations and growing sustainability goals.

This transition is evident in the automotive industry, where manufacturers are adopting chromium phosphate-based coatings to enhance vehicle durability while adhering to environmental standards. This adoption reflects the broader industry trend towards sustainable practices.

In the medical field, chromium phosphate is applied as a medication for various conditions, including leukemia, arthritis, and hemangioma. Ongoing research suggests that it inhibits cancer cell growth and enhances chemotherapy. Furthermore, chromium phosphate nanoparticles have been investigated for their anti-angiogenic properties, potentially aiding in hemangioma treatment.

As industries seek more environmentally friendly alternatives, chromium phosphate, with its low environmental impact, could see increased usage. This is especially true in the coatings and surface treatment sectors, where companies are moving away from hazardous materials.

Regional Analysis

Asia Pacific Leads Chromium Phosphate Market with 45.8% Share, Valued at $59.3 Million in 2024

In 2024, the Asia Pacific (APAC) region emerged as the dominant force in the global chromium phosphate market, securing a substantial 45.8% market share, equivalent to approximately USD 59.3 million. This leadership is primarily attributed to the region’s rapid industrialization, expansive infrastructure projects, and robust automotive and construction sectors. Countries such as China, India, Japan, and South Korea have been pivotal in driving demand, leveraging chromium phosphate’s corrosion-resistant properties in various applications.

The architectural coatings segment, in particular, has witnessed significant growth in APAC. The surge in urban development and the need for durable building materials have propelled the use of chromium phosphate in paints and coatings, ensuring longevity and resistance against environmental factors. Moreover, the automotive industry’s expansion in the region has further amplified the demand for high-performance coatings, where chromium phosphate plays a crucial role in enhancing vehicle durability and aesthetics.

Government initiatives promoting sustainable construction practices and the adoption of eco-friendly materials have also contributed to the market’s growth. Policies encouraging the reduction of volatile organic compounds (VOCs) in paints and coatings have led manufacturers to incorporate chromium phosphate, known for its environmental compatibility, into their products.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

American Elements plays a strategic role in the chromium phosphate market through its advanced materials portfolio tailored for industrial and research applications. The company provides high-purity chromium phosphate used in coatings, catalysts, and ceramics. With production facilities in the U.S. and a global distribution network, it serves sectors such as aerospace, electronics, and pharmaceuticals. Its commitment to sustainable materials and nanotechnology-based innovations keeps it competitive, particularly in emerging applications like biomedical devices and advanced surface treatments.

Brenntag SE, a leading chemical distributor headquartered in Germany, actively supports the chromium phosphate market through its wide logistics and supply chain capabilities. The company offers tailored chemical distribution services, including high-quality chromium phosphate products for use in coatings, construction materials, and automotive surface treatments. Brenntag focuses on regulatory compliance and product safety, helping clients meet environmental standards. Its extensive global reach and strong customer relationships make it a key enabler of regional market expansion, especially across Europe and Asia-Pacific.

Chemetall, a subsidiary of BASF, specializes in surface treatment technologies and contributes significantly to the chromium phosphate market. The company’s chromium phosphate solutions are integral to corrosion protection and metal pre-treatment processes, widely used in the automotive and industrial equipment sectors. With decades of expertise in surface chemistry, Chemetall emphasizes product performance and environmental compliance. It continues to develop advanced pretreatment chemistries that reduce environmental impact while enhancing adhesion and durability, positioning it as a trusted supplier in surface finishing markets.

Top Key Players in the Market

- American Elements

- Brenntag SE

- Chemetall

- CHEMOS GmbH & Co. KG

- Merck KGaA

- Nippon Chemical Industrial CO., LTD.

- Oxkem Limited

- Service Chemical Industries

- SHEPHERD CHEMICALS

Recent Developments

In 2024, Chemetall, a subsidiary of BASF, continued to strengthen its position in the chromium phosphate market by focusing on surface treatment solutions that enhance corrosion resistance. A notable development was the introduction of Gardorol CP 8019 in September 2024, a product designed to prevent rust and corrosion effectively.

In 2024, American Elements maintained its position as a key supplier in the chromium phosphate market, offering high-purity compounds tailored for specialized applications. The company provides chromium phosphate in various purity levels, including 99%, 99.9%, 99.99%, and 99.999%, catering to industries such as coatings, ceramics, and medical devices.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 129.5 Mn |

| Forecast Revenue (2034) | USD 332.8 Mn |

| CAGR (2025-2034) | 9.9% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Hexa-hydrated Chromium Phosphate, Mesoporous Phase, Films, Amorphous Phase), By Grade (Agricultural Grade, Food Grade, Industrial Grade, Pharmaceutical Grade), By Product Form (Granular, Liquid, Powder), By Application (Coatings and Paints, Agriculture, Automotive, Construction, Electronics, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | American Elements, Brenntag SE, Chemetall, CHEMOS GmbH & Co. KG, Merck KGaA, Nippon Chemical Industrial CO., LTD., Oxkem Limited, Service Chemical Industries, SHEPHERD CHEMICALS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |