Global Calcium Ammonium Nitrate Market Size, Share, And Industry Analysis Report By Physical Form (Granular, Liquid), By Type (Nitrogen Content 27 percent, Nitrogen Content 15.5 percent), By Crop Type (Cereals and Grains, Oilseeds and Pulses, Fruits and Vegetables, Turf and Ornamentals), By Application (Soil Application, Fertigation, Foliar), By End Use (Agriculture, Chemical Manufacturing, Water Treatment, Construction), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2025-2034

- Published date: February 2026

- Report ID: 178536

- Number of Pages: 231

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

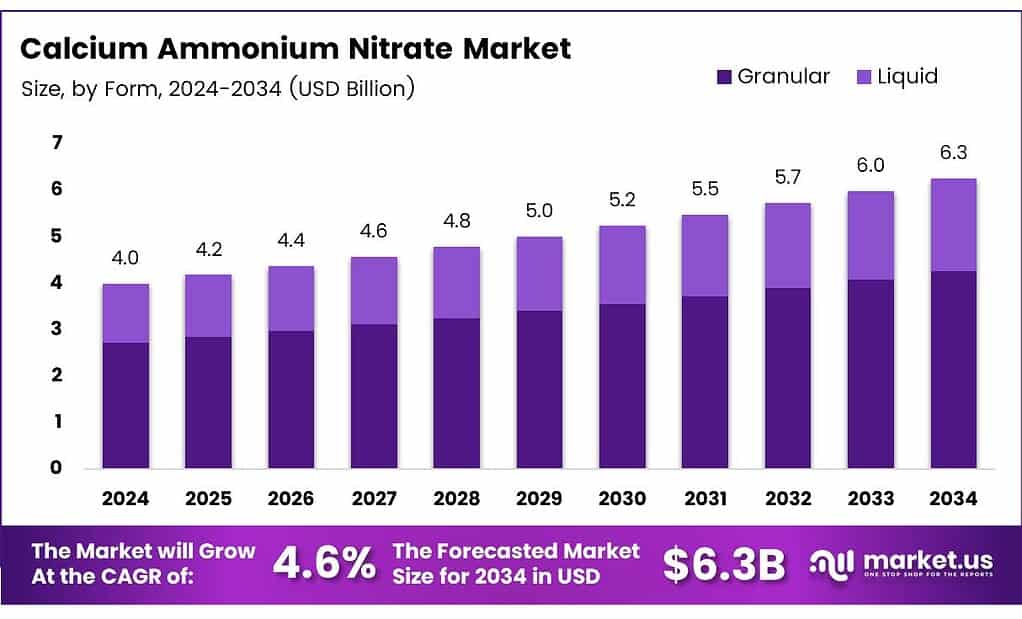

The Global Calcium Ammonium Nitrate Market size is expected to be worth around USD 6.3 billion by 2034 from USD 4.0 billion in 2024, growing at a CAGR of 4.6% during the forecast period 2025 to 2034.

Calcium Ammonium Nitrate (CAN) is a nitrogen-based fertiliser that combines ammonium nitrate with calcium carbonate. Farmers apply it widely to improve soil structure and deliver fast-acting nitrogen to crops. Its chloride-free composition makes it particularly suitable for sensitive crops and acidic farmlands.

CAN stands out from other nitrogen sources because it supplies both nitrate and ammonium nitrogen. This dual-nitrogen action supports steady crop uptake throughout key growth stages. Moreover, the calcium component neutralises soil acidity, reducing the need for separate liming treatments in intensive farming systems.

- Global import demand for CAN-type fertiliser mixtures. The United States recorded CAN-related imports valued at $110.3 million with a volume of 511.3 million kg in 2024, making it the largest national importer. This signals strong and growing demand from North American agricultural markets seeking reliable nitrogen solutions.

- The European Union recorded CAN-related imports valued at $91.2 million and a volume of 391.2 million kg in 2024. This volume reflects substantial regional demand alongside domestic EU production capacity, confirming CAN’s central role in European crop nutrition programs.

Global food demand continues to rise as population growth accelerates, particularly across Asia and Africa. Farmers in these regions require high-efficiency fertilisers that maximise yield per hectare. Consequently, CAN adoption grows as governments and agribusinesses push to close yield gaps in staple cereal production.

European decarbonization policies actively favour low-carbon, chloride-free CAN variants over alternative nitrogen sources. Regulatory frameworks such as the EU Nitrates Directive guide farmers toward precise application methods. These policies strengthen market demand for CAN formulations that align with environmental compliance and sustainable farming targets.

Key Takeaways

- The Global Calcium Ammonium Nitrate Market was valued at USD 4.0 billion in 2024 and is projected to reach USD 6.3 billion by 2034, at a CAGR of 4.6% during the forecast period from 2025 to 2034.

- Granular holds the dominant position with a market share of 72.4%.

- Nitrogen Content 27% leads the segment with a share of 52.5%.

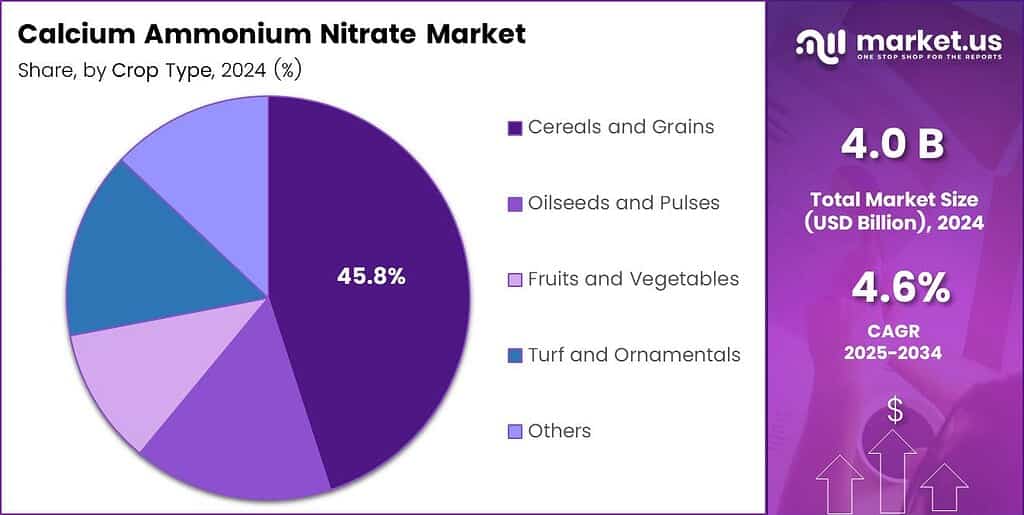

- Cereals and Grains dominate with a 45.8% share.

- Soil Application holds the leading position with 59.1% of the market.

- Agriculture accounts for the largest share at 72.9%.

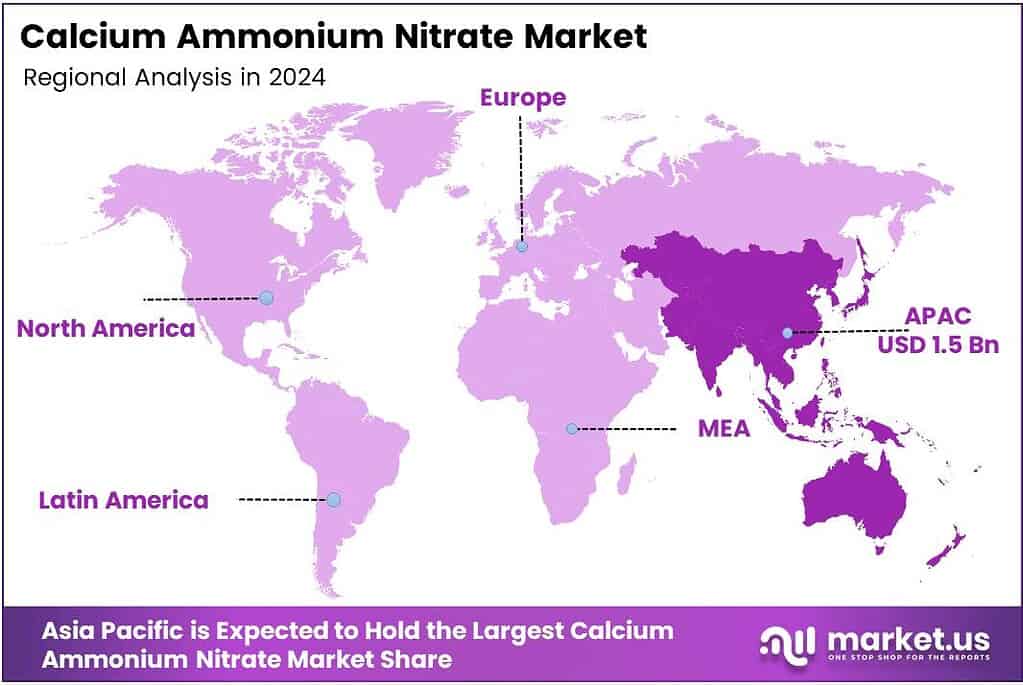

- Asia Pacific leads regional markets with a share of 38.2%, valued at USD 1.5 billion.

By Physical Form Analysis

Granular dominates with 72.4% due to ease of handling and uniform nutrient distribution.

In 2025, Granular held a dominant market position in the By Physical Form segment of the Calcium Ammonium Nitrate Market, with a 72.4% share. Granular CAN offers superior handling, storage stability, and compatibility with standard broadcast and precision application equipment. Consequently, large-scale grain and cereal farmers prefer it for its consistent nutrient release and low dust generation during application.

Liquid CAN formulations serve a growing niche in fertigation-based farming systems. Farmers using drip and micro-irrigation infrastructure increasingly adopt liquid variants to deliver soluble nitrogen directly to root zones. However, liquid CAN requires specialised storage and handling infrastructure, which currently limits its penetration compared to the dominant granular segment.

By Type Analysis

Nitrogen Content 27% dominates with 52.5% due to its balance of nutrient density and agronomic effectiveness.

In 2025, Nitrogen Content 27% held a dominant market position in the By Type segment of the Calcium Ammonium Nitrate Market, with a 52.5% share. This grade offers a high nitrogen concentration suitable for intensive cereal and grain production. Moreover, its proven agronomic track record across European and Asian markets supports its continued market leadership.

Nitrogen Content 15.5% targets specific soil and crop conditions where lower nitrogen rates prevent over-application risks. This grade finds usage in horticulture and sensitive crop environments. Additionally, producers serving markets with strict nitrate runoff regulations often recommend this variant to ensure environmental compliance.

Others in the type segment include customised blends with micronutrients or adjusted nitrogen ratios for speciality crops. These formulations address niche requirements in greenhouse production and high-value horticulture. Therefore, their growth rate outpaces standard grades as farmers invest in precision nutrition programs.

By Crop Type Analysis

Cereals and Grains dominate with 45.8% due to large planted areas and high nitrogen demand during growth stages.

In 2025, Cereals and Grains held a dominant market position in the By Crop Type segment of the Calcium Ammonium Nitrate Market, with a 45.8% share. Wheat, rice, and maize production across Asia, Europe, and the Americas drives massive nitrogen fertiliser demand. CAN’s dual-nitrogen profile supports rapid early growth and sustained productivity through the crop cycle.

Oilseeds and Pulses represent a growing end-use category as global edible oil and protein demand rises. Soybean, canola, and sunflower farmers increasingly apply CAN to meet crop nutrition requirements. However, nitrogen application rates for oilseeds remain lower than cereals, keeping this segment’s share below the dominant cereals category.

Fruits and Vegetables benefit from CAN’s low chloride content and calcium supply, which support cell structure and reduce blossom-end rot. High-value horticultural producers in greenhouse and open-field settings adopt CAN widely. Additionally, Turf and Ornamentals and Others contribute smaller but stable volumes driven by urban landscaping and speciality agriculture demand.

By Application Analysis

Soil Application dominates with 59.1% due to its simplicity and compatibility with conventional farming practices.

In 2025, Soil Application held a dominant market position in the By Application segment of the Calcium Ammonium Nitrate Market, with a 59.1% share. Broadcast and incorporation methods allow farmers to apply CAN granules efficiently across large field areas. Consequently, smallholder and commercial farm operators rely on soil application as the most accessible and cost-effective nutrient delivery method.

Fertigation is the fastest-growing application method as drip irrigation systems expand across water-scarce regions. Soluble CAN formulations dissolve easily in irrigation water and deliver nitrogen directly to root zones. Moreover, fertigation allows precise timing of nutrient delivery aligned with crop growth stages, improving nitrogen use efficiency significantly.

Foliar application of diluted CAN solutions addresses specific nutrient deficiencies during critical crop development windows. Farmers use foliar spray as a supplementary tool rather than a primary feeding method. Therefore, this segment holds the smallest share but serves an important role in precision and high-value crop nutrition programs.

By End Use Analysis

Agriculture dominates with 72.9% due to its role as the primary nitrogen source for global crop production.

In 2025, Agriculture held a dominant market position in the By End Use segment of the Calcium Ammonium Nitrate Market, with a 72.9% share. Crop farmers worldwide consume the majority of CAN output to meet nitrogen demands across cereals, vegetables, and horticulture. Additionally, government subsidy programs supporting fertiliser access in emerging markets further reinforce agricultural sector dominance.

Chemical Manufacturing uses CAN as a precursor or blending agent in speciality compound production. Industrial buyers value its consistent composition and availability from global producers. However, chemical sector consumption remains significantly smaller than agricultural demand, positioning it as a secondary but commercially important end-use category.

Water Treatment and Construction end uses apply CAN in specific niche applications such as soil stabilisation and industrial process chemistry. Others include research and laboratory use. Collectively, these non-agricultural categories represent less than 30% of total market volume, highlighting agriculture’s commanding position across all end-use segments.

Key Market Segments

By Physical Form

- Granular

- Liquid

By Type

- Nitrogen Content 27%

- Nitrogen Content 15.5%

- Others

By Crop Type

- Cereals and Grains

- Oilseeds and Pulses

- Fruits and Vegetables

- Turf and Ornamentals

- Others

By Application

- Soil Application

- Fertigation

- Foliar

By End Use

- Agriculture

- Chemical Manufacturing

- Water Treatment

- Construction

- Others

Emerging Trends

Precision Farming and Sustainable Formulations Reshape the Calcium Ammonium Nitrate Market

Precision farming technologies drive integration of stabilised CAN blends with variable-rate application systems. Farmers use GPS-guided equipment and soil sensor data to apply nitrogen exactly where crops need it. Moreover, this trend reduces input waste, lowers costs, and improves yield consistency across large-scale commercial operations.

- Regenerative agriculture practices increasingly prioritise calcium-enriched nitrate fertilisers for long-term soil health improvement. Farmers shifting toward lower-tillage and cover-crop systems value CAN’s soil pH benefits alongside nitrogen delivery. China exported CAN-type fertilisers valued at $132.7 million with a volume of 651.2 million kg in 2024, confirming the scale of global supply chains supporting these evolving farming practices.

Growing demand for biogas and renewable ammonia-based CAN aligns with the EU Carbon Border Adjustment Mechanisms. Producers explore green ammonia feedstocks to reduce lifecycle emissions of nitrogen fertilisers. Additionally, a surge in customised high-nitrogen granular variants optimised for critical cereal and fruit growth stages reflects precision nutrition’s expanding commercial importance.

Drivers

Rising Global Food Demand and Policy Support Drive Calcium Ammonium Nitrate Market Growth

Global population growth accelerates demand for staple crop production across Asia, Africa, and Latin America. Farmers adopt high-efficiency nitrogen fertilisers like CAN to boost yields on existing farmland. Consequently, growing food security pressures at national policy levels translate directly into higher fertiliser procurement and application intensity. Brazil imported CAN-type fertilisers valued at $37.9 million with a volume of 132.7 million kg in 2024, highlighting demand growth in major emerging agricultural economies.

- Rapid fertigation expansion in water-scarce regions across the Asia-Pacific and the Middle East boosts soluble nitrate usage significantly. Drip irrigation infrastructure investment enables precise, root-zone nitrogen delivery that improves resource use efficiency. Additionally, Nutrien reported nitrogen-adjusted EBITDA of $2.15 billion in FY2025, reflecting improved profitability across nitrogen products that compete with and complement CAN in global crop nutrition channels.

European nitrate directives and decarbonization policies actively favour low-carbon, chloride-free CAN variants. Regulatory bodies require farmers to adopt precision nutrition approaches that minimise nitrate runoff and greenhouse gas emissions. Moreover, government subsidy programs targeting acidic farmland neutralisation enhance CAN demand in soil correction programs across multiple markets.

Restraints

Feedstock Price Volatility and Regulatory Compliance Costs Limit Market Growth

Natural gas price volatility directly erodes producer margins in CAN manufacturing, as ammonia synthesis requires large energy inputs. When gas prices spike, production costs rise sharply, and profitability for nitrogen fertiliser producers declines. Consequently, planned capacity expansions face delays or cancellations when energy cost forecasts remain uncertain across major producing regions.

- CF Industries reported free cash flow of $1.45 billion in FY2024, demonstrating that well-capitalised producers can manage these cost pressures. However, smaller regional producers and distributors face disproportionate compliance burdens. Therefore, regulatory cost increases may accelerate market consolidation, reducing competition and limiting product variety for downstream agricultural customers.

Tightening hazardous material transport and storage regulations raises compliance costs for CAN distributors and logistics providers. Regulatory bodies in the EU, North America, and parts of Asia classify ammonium nitrate-based products under strict safety frameworks. Moreover, compliance investments in certified storage facilities and specialised transport equipment increase the overall cost base for market participants.

Growth Factors

Innovation and Market Expansion Open New Growth Avenues for Calcium Ammonium Nitrate

Innovation in liquid and micronutrient-enhanced CAN formulations creates new demand in automated micro-irrigation systems. Speciality CAN blends with zinc, boron, or sulfur address complex crop deficiencies in a single application. Moreover, manufacturers investing in customised product development capture premium pricing in high-value horticulture segments that require salinity-sensitive nutrient solutions.

- Latin America and Sub-Saharan Africa present significant untapped market potential for CAN as agricultural modernisation accelerates. Expanding smallholder access to commercial fertilisers drives volume growth in these regions. According to World Bank WITS, India imported CAN-type fertilisers valued at $50.8 million with a volume of 168.7 million kg in 2024, showing how large emerging markets rapidly increase fertiliser consumption as crop productivity programs expand.

Alignment with carbon-credit schemes enables producers to sell premium low-N₂O emission CAN into climate-smart farming programs. Buyers in voluntary carbon markets pay price premiums for verified low-emission nitrogen fertilisers. Additionally, greenhouse and protected agriculture operators increasingly require salinity-sensitive CAN products, expanding the addressable market beyond traditional open-field crop applications.

Regional Analysis

Asia Pacific Dominates the Calcium Ammonium Nitrate Market with a Market Share of 38.2%, Valued at USD 1.5 Billion

Asia Pacific leads the global Calcium Ammonium Nitrate market with a commanding share of 38.2%, valued at USD 1.5 billion in 2024. The region’s dominance reflects its vast cereal and rice cultivation areas in China, India, and Southeast Asia. Moreover, rapid fertigation adoption in water-scarce zones and government-backed food security programs continue to accelerate nitrogen fertiliser consumption across the region.

North America maintains strong CAN demand driven by large-scale corn, wheat, and soybean production in the United States and Canada. American farmers rely on diverse nitrogen sources, with CAN competing alongside urea and UAN solutions. Additionally, precision agriculture technology adoption in this region supports efficient CAN application in soil neutralisation and high-yield crop programs.

Europe represents one of the most established CAN markets globally, supported by decades of regulatory preference for chloride-free nitrogen fertilisers. The EU Nitrates Directive and decarbonization policies shape fertiliser choices toward lower-emission options, including CAN. However, energy cost pressures on European ammonia and fertiliser production create price competitiveness challenges versus imports from lower-cost producers in Eastern Europe and North Africa.

Latin America offers significant growth potential for CAN as Brazil, Mexico, and Colombia expand planted crop areas. Brazil relies heavily on fertiliser imports to sustain its large-scale soybean and corn production systems. Consequently, international CAN suppliers increasingly target Latin American distributors and agribusiness networks to capture share in this high-volume, import-dependent agricultural market.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Yara International ASA holds a leading position in the global CAN market through its extensive nitrogen fertiliser production network spanning Europe, the Americas, and Asia. The company serves agricultural customers in key grain-producing regions with a broad product portfolio, including high-grade CAN formulations. Yara’s global distribution infrastructure and agronomic service capabilities strengthen its competitive position across both developed and emerging markets.

EuroChem Group AG operates large-scale nitrogen fertiliser production facilities across Russia, Europe, and the Americas, producing CAN alongside other nitrogen products. The group targets European and global agricultural markets with competitively priced granular CAN grades. Moreover, EuroChem’s integrated mining and production model provides cost advantages that support competitive pricing strategies in markets with high price sensitivity.

CF Industries Holdings Inc. focuses primarily on North American nitrogen production, competing across the broader nitrogen fertiliser market that includes CAN-adjacent products. Supported by its low-cost North American natural gas production base. Additionally, CF Industries’ investment in green ammonia and decarbonization initiatives positions it for long-term competitiveness as sustainability requirements tighten globally.

Achema AB, based in Lithuania, produces CAN primarily for European agricultural markets and serves as a key supplier in the Baltic and Central European regions. The company benefits from proximity to major European grain production zones, reducing logistics costs for distributors and end customers. Achema’s product range includes standard and nitrogen-enriched CAN grades aligned with EU agronomic and regulatory requirements.

Top Key Players in the Market

- Yara International ASA

- EuroChem Group AG

- CF Industries Holdings Inc.

- Achema AB

- Uralchem JSC

- Fertiberia S.A.

- Koch Fertiliser LLC (Koch Ag & Energy Solutions, LLC)

- Grupa Azoty S.A.

- Acron Group

- Haifa Chemicals Ltd.

Recent Developments

- In 2025, Yara signed a binding 10-year offtake agreement with ATOME for 100% of the output of low-carbon CAN from ATOME’s Villeta project in Paraguay. The project uses renewable hydropower for ammonia production (via a long-term PPA with Paraguay’s national utility ANDE). Yara will handle distribution in South America post-collection at the site. This supports Yara’s decarbonization efforts in the CAN sector.

- In 2025, EuroChem manufactures CAN (described as a highly efficient granular fertiliser with 27% nitrogen for secure plant nitrogen supply) as part of its core agricultural products portfolio. It operates AN/CAN units at its Antwerpen facility in Belgium (part of broader nitrogen, phosphate, and complex fertiliser production across Russia, Belgium, Lithuania, Brazil, and China).

Report Scope

Report Features Description Market Value (2024) USD 4.0 Billion Forecast Revenue (2034) USD 6.3 Billion CAGR (2025-2034) 4.6% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Physical Form (Granular, Liquid), By Type (Nitrogen Content 27%, Nitrogen Content 15.5%, Others), By Crop Type (Cereals and Grains, Oilseeds and Pulses, Fruits and Vegetables, Turf and Ornamentals, Others), By Application (Soil Application, Fertigation, Foliar), By End Use (Agriculture, Chemical Manufacturing, Water Treatment, Construction, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Yara International ASA, EuroChem Group AG, CF Industries Holdings Inc., Achema AB, Uralchem JSC, Fertiberia S.A., Koch Fertiliser LLC (Koch Ag & Energy Solutions, LLC.), Grupa Azoty S.A., Acron Group, Haifa Chemicals Ltd. Customization Scope Customisation for segments, region/country-level will be provided. Moreover, additional customisation can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Calcium Ammonium Nitrate MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample

Calcium Ammonium Nitrate MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Yara International ASA

- EuroChem Group AG

- CF Industries Holdings Inc.

- Achema AB

- Uralchem JSC

- Fertiberia S.A.

- Koch Fertiliser LLC (Koch Ag & Energy Solutions, LLC)

- Grupa Azoty S.A.

- Acron Group

- Haifa Chemicals Ltd.

Our Clients

- 178536

- February 2026