Quick Navigation

- Report Overview

- Key Takeaways

- Vehicle Type Analysis

- Wheel Size Analysis

- Sales Channel Analysis

- Material Type Analysis

- Application Analysis

- End User Analysis

- Finish Type Analysis

- Manufacturing Process Analysis

- Key Market Segments

- Regional Analysis

- Key Regions and Countries

- Market Dynamics

- Drivers

- Restraints

- Challenges

- Opportunities

- Key Company Insights

- Recent Developments

- Geopolitical Impact Analysis

- Report Scope

Report Overview

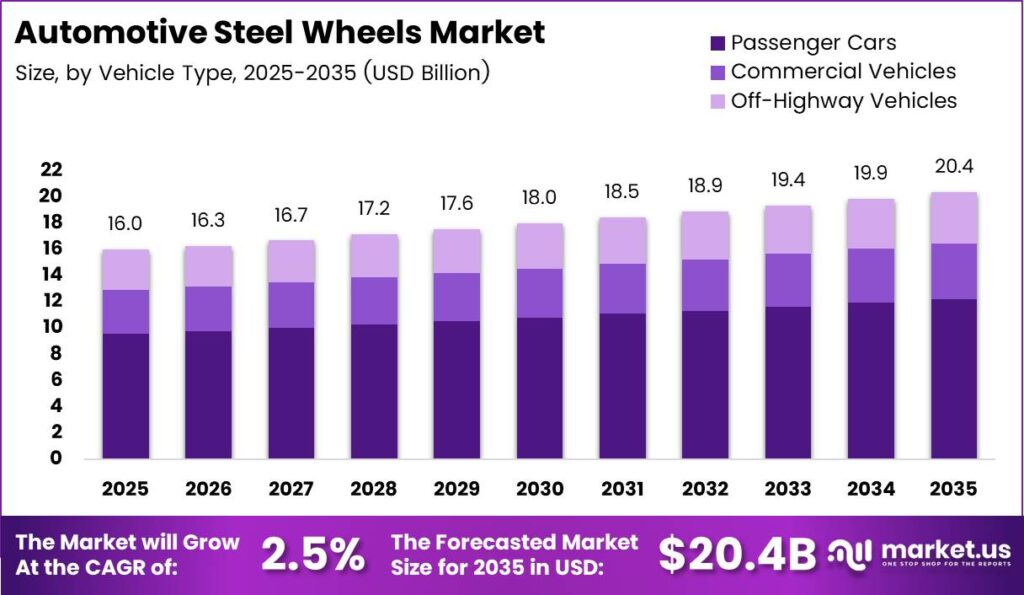

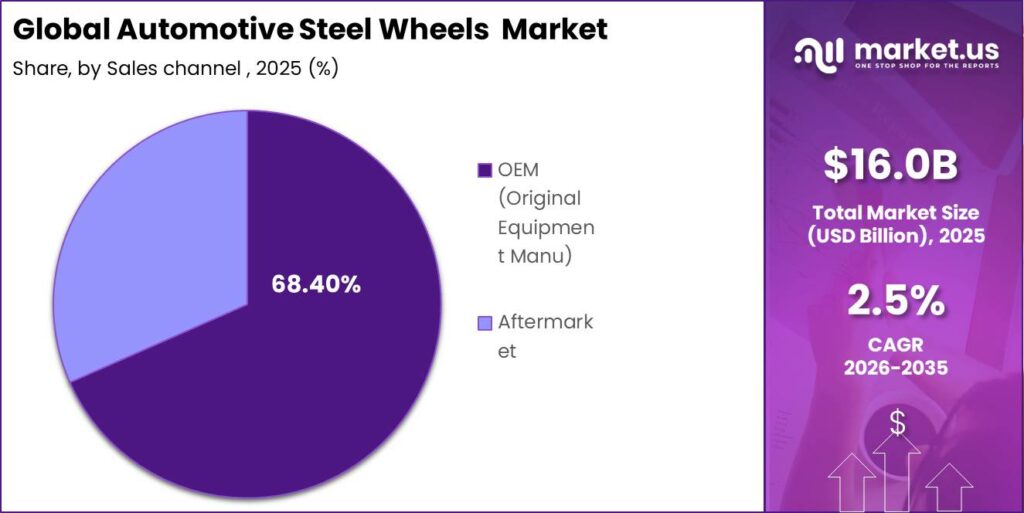

Global Automotive Steel Wheels Market size is expected to be worth around USD 20.4 Billion by 2035 from USD 16.0 Billion in 2025, growing at a CAGR of 2.5% during the forecast period 2026 to 2035. This steady expansion reflects durable demand across cost-sensitive vehicle classes. Suppliers gain predictable volume, so long-term OEM contracts stay attractive for capacity planning.

The Automotive Forging Market connects closely to steel wheels, which are pressed metal wheels fitted to passenger and commercial vehicles. Manufacturers form these wheels through stamping, flow forming, and hybrid forging. This means the market splits across vehicle type, wheel size, sales channel, material, application, end user, finish, and process. Therefore buyers can source products matched to price, durability, and load needs.

Key Takeaways

- Global Automotive Steel Wheels market reaches USD 20.4 Billion by 2035 from USD 16.0 Billion in 2025 at a CAGR of 2.5%.

- Passenger Cars lead the Vehicle Type segment with a 54.60% share.

- The 13 to 15 Inches class leads Wheel Size with a 41.20% share.

- OEM channels hold a 68.40% share of the Sales Channel segment.

- Standard Carbon Steel leads Material Type with a 62.10% share.

- Standard Road Use dominates Application with a 49.80% share.

- Automotive Manufacturers control End User with a 70.30% share.

- Painted Steel Wheels lead Finish Type with a 46.50% share.

- The Stamping Process dominates Manufacturing with a 63.70% share.

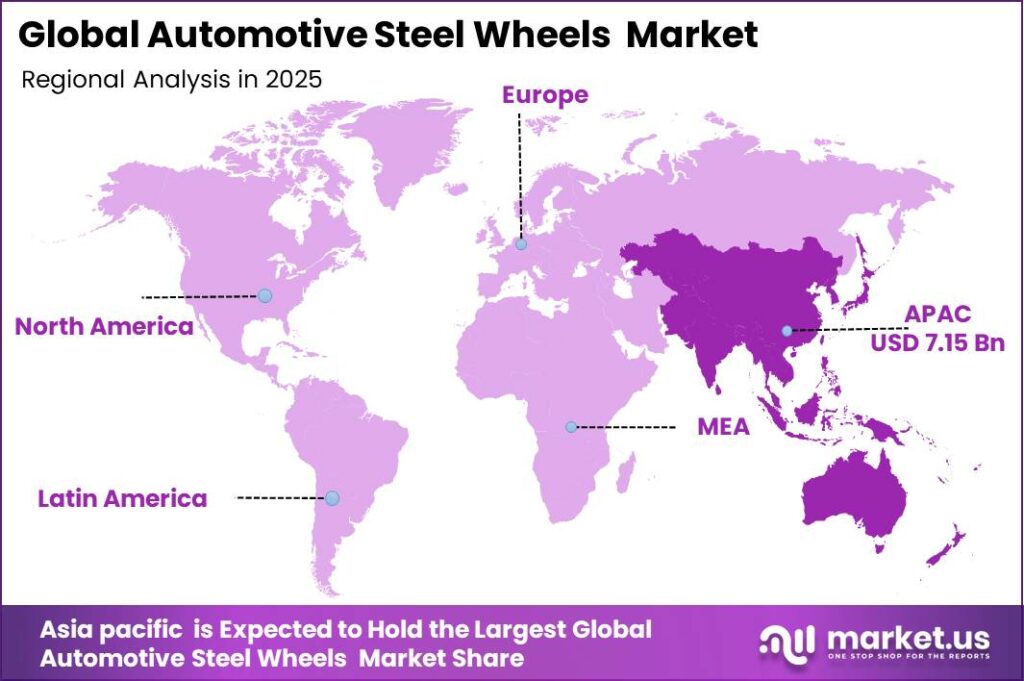

- Asia-Pacific leads all regions with a 44.80% share, valued at USD 7.15 Billion.

Government fuel-efficiency and vehicle-safety rules shape how automakers specify wheels across trims. Regulators in Europe and North America push weight targets, which steer premium models toward alloys. This creates a protected space for steel wheels in base and fleet vehicles. As a result, suppliers who serve budget and commercial programs keep stable order books despite policy pressure at the premium end.

Rising light commercial vehicle fleets in developing economies lift demand for durable steel wheels. This growth ties end-use transport activity directly to replacement and OEM wheel orders. The Automotive Casting Market competes for the same base metal supply, which affects input planning. Therefore steel wheel makers must lock coil contracts early to protect delivery schedules and margins.

As per our research, the Automotive Steel Wheels Market grows at a CAGR of 2.5%, reaching USD 20.4 Billion by 2035. This measured pace reflects a slow mix shift rather than volume loss. Companies that defend cost leadership in high-volume budget segments will hold share. Instead of chasing premium styling, they should scale efficient stamping lines to protect unit economics.

Vehicle Type Analysis

Passenger Cars dominates with 54.60% due to high budget-model steel wheel fitment.

In 2025, Passenger Cars held a dominant market position in the By Vehicle Type segment of Automotive Steel Wheels Market, with a 54.60% share. Global passenger car production exceeded 68 million units in 2023, according to OICA. Budget trims rely on steel wheels for cost control. This means suppliers with high-volume stamping capacity capture the largest, most stable contracts in this class.

Commercial Vehicles serve freight and passenger transport where load ratings matter most. World Bank data show road freight carries over 70% of inland goods tonnage in many economies. Fleet buyers favor steel for reparability and impact resistance. This creates recurring wheel demand tied to fleet renewal, so suppliers gain predictable commercial orders alongside passenger volume.

Light Commercial Vehicles carry last-mile delivery loads across expanding urban logistics networks. UNIDO industrial output data link rising manufacturing activity to higher LCV registration. Heavy Commercial Vehicles haul long-distance freight and need high-strength steel wheels. Off-Highway Vehicles operate in construction and agriculture, where steel durability wins. Together these three sub-segments hold the remaining share, giving suppliers diverse rugged-use revenue streams.

Wheel Size Analysis

13–15 Inches dominates with 41.20% due to compact and budget car prevalence.

In 2025, 13–15 Inches held a dominant market position in the By Wheel Size segment of Automotive Steel Wheels Market, with a 41.20% share. ITC Trade Map records show small-diameter wheels lead traded automotive wheel volumes. Compact and entry cars use these sizes as standard. This means high-volume small-wheel production remains the core revenue base for most steel wheel plants.

The 16 to 18 Inches class fits mid-size cars, SUVs, and many light trucks. UN Comtrade trade flows show mid-diameter wheels rising in cross-border shipments under HS code 8708. Buyers select this range for balance of load and ride. This creates a growth lane for suppliers upgrading tooling toward larger, higher-value steel wheels.

The Above 18 Inches class serves larger SUVs, pickups, and heavy vehicles needing high load capacity. Customs databases record steady import volumes for large-diameter steel wheels in truck-heavy markets. These wheels command higher unit prices due to material content. This means the remaining share offers premium margin, rewarding suppliers with heavy-gauge forming capability.

Sales Channel Analysis

OEM dominates with 68.40% due to factory-fitment supply contracts scale.

In 2025, OEM held a dominant market position in the By Sales Channel segment of Automotive Steel Wheels Market, with a 68.40% share. UNIDO manufacturing statistics tie automotive assembly output to first-fit component demand. Automakers source wheels directly for new vehicles. This means suppliers on approved OEM vendor lists secure the largest, most predictable order volumes across production cycles.

The Aftermarket channel serves replacement demand from corrosion, curb, and impact damage. WTO trade data show automotive parts trade exceeding several hundred billion dollars annually. Vehicle owners and workshops buy replacement steel wheels through this route. This creates recurring, higher-margin sales, so suppliers with strong distribution networks capture steady post-sale revenue independent of new-vehicle cycles.

Material Type Analysis

Standard Carbon Steel dominates with 62.10% due to low cost and formability.

In 2025, Standard Carbon Steel held a dominant market position in the By Material Type segment of Automotive Steel Wheels Market, with a 62.10% share. World Steel Association data report global crude steel output above 1.8 billion tonnes in 2023. Carbon steel keeps wheel costs low. This means suppliers using it protect price competitiveness in high-volume budget vehicle programs.

High-Strength Steel supports lighter, stronger wheel designs for demanding applications. IEA efficiency analysis links vehicle weight reduction to lower fuel use and emissions. Automakers adopt it to meet weight targets without full alloy costs. This creates an upgrade path, so suppliers investing in high-strength grades win performance-critical contracts.

Alloy-Coated Steel Wheels add corrosion resistance for harsh-use and coastal markets. National statistical offices report high vehicle-corrosion rates in salt-treated road regions. Buyers pay more for longer wheel life. This means the remaining share rewards suppliers offering coated products with durability-based pricing power.

Application Analysis

Standard Road Use dominates with 49.80% due to everyday passenger driving demand.

In 2025, Standard Road Use held a dominant market position in the By Application segment of Automotive Steel Wheels Market, with a 49.80% share. IMF data link rising GDP per capita to higher passenger vehicle ownership. Everyday driving drives most wheel demand. This means suppliers focused on standard road wheels serve the widest, most stable customer base across regions.

Off-Road and Heavy-Duty Use covers construction, mining, and agricultural vehicles needing rugged wheels. FAO agricultural machinery data show rising equipment use in developing farm economies. These vehicles favor steel for impact resistance. This creates durable, premium-margin demand, so suppliers with heavy-duty product lines gain a defensible niche.

Urban Mobility Vehicles include compact city cars and micro-mobility platforms. ITU digital-economy data track rising shared-mobility fleets in dense cities. Fleet and Logistics Vehicles carry delivery loads across expanding e-commerce networks. World Bank logistics indexes show rising freight activity. Together these sub-segments hold the remaining share, giving suppliers steady fleet-linked replacement demand.

End User Analysis

Automotive Manufacturers dominates with 70.30% due to direct factory-fitment purchasing volume.

In 2025, Automotive Manufacturers held a dominant market position in the By End User segment of Automotive Steel Wheels Market, with a 70.30% share. OICA production figures confirm automakers assemble tens of millions of vehicles yearly. They buy wheels in bulk for factory fitment. This means suppliers aligned with manufacturer procurement teams secure the largest recurring contracts in the market.

Fleet Operators manage large vehicle pools needing frequent wheel replacement. World Bank transport data show commercial fleets covering high annual mileage. Bulk purchasing gives them strong pricing leverage. This creates volume-driven demand, so suppliers offering fleet service programs win repeat business and predictable order flow.

Individual Vehicle Owners buy replacement wheels after damage or corrosion. Customs databases record steady consumer-level wheel imports in aftermarket-heavy regions. Government and Defense Fleets require durable, spec-compliant steel wheels. Regulatory procurement filings show steady public-sector vehicle purchases. Together these sub-segments hold the remaining share, giving suppliers diversified demand beyond core manufacturer contracts.

Finish Type Analysis

Painted Steel Wheels dominates with 46.50% due to low-cost corrosion protection standard.

In 2025, Painted Steel Wheels held a dominant market position in the By Finish Type segment of Automotive Steel Wheels Market, with a 46.50% share. ITC Trade Map data show painted wheels lead finished wheel trade volumes. Paint gives cheap corrosion protection. This means suppliers using painting lines keep unit costs low while meeting basic durability standards for budget vehicles.

Powder-Coated Wheels offer tougher, more uniform protection than standard paint. UNIDO industrial coatings output data show rising powder-coating adoption in manufacturing. Buyers select them for longer finish life. This creates an upgrade tier, so suppliers investing in powder-coating capacity earn higher margins on durability-focused orders.

Chrome-Plated Steel Wheels add a bright decorative finish for styling-focused buyers. Patent databases record ongoing plating-process innovation for automotive wheels. Anti-Corrosion Coated Wheels serve coastal and salt-road markets needing maximum protection. National statistical offices report high corrosion exposure in these regions. Together these sub-segments hold the remaining share, giving suppliers value-added finish revenue.

Manufacturing Process Analysis

Stamping Process dominates with 63.70% due to high-speed mass-production cost efficiency.

In 2025, Stamping Process held a dominant market position in the By Manufacturing Process segment of Automotive Steel Wheels Market, with a 63.70% share. UNIDO output data tie stamped metal parts to high-volume automotive assembly. Stamping delivers low per-unit cost at scale. This means suppliers running efficient stamping lines protect margins on the highest-volume wheel programs worldwide.

Flow Forming shapes wheels for lighter weight and improved strength distribution. Patent databases show rising flow-forming filings for automotive wheel production. Automakers adopt it to cut weight without alloy costs. This creates a competitive edge, so suppliers adding flow-forming capacity win weight-sensitive contracts and command better pricing.

Forging using steel hybrid processes produces the strongest wheels for heavy-duty and commercial use. Corporate annual reports from wheel makers cite forging investment for high-load applications. These wheels carry premium prices. This means the remaining share rewards suppliers with forging capability through higher-margin, performance-critical demand.

Key Market Segments

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- Off-Highway Vehicles

By Wheel Size

- 13–15 Inches

- 16–18 Inches

- Above 18 Inches

By Sales Channel

- OEM (Original Equipment Manufacturers)

- Aftermarket

By Material Type

- Standard Carbon Steel

- High-Strength Steel

- Alloy-Coated Steel Wheels

By Application

- Standard Road Use

- Off-Road & Heavy-Duty Use

- Urban Mobility Vehicles

- Fleet & Logistics Vehicles

By End User

- Automotive Manufacturers

- Fleet Operators

- Individual Vehicle Owners

- Government & Defense Fleets

By Finish Type

- Painted Steel Wheels

- Powder-Coated Wheels

- Chrome-Plated Steel Wheels

- Anti-Corrosion Coated Wheels

By Manufacturing Process

- Stamping Process

- Flow Forming

- Forging (Steel Hybrid Processes)

Regional Analysis

Asia Pacific Dominates the Automotive Steel Wheels Market with a Market Share of 44.80%, Valued at USD 7.15 Billion

Asia-Pacific leads the Automotive Steel Wheels Market with a 44.80% share, valued at USD 7.15 Billion. As per our research, the region combines high vehicle production with strong budget-model demand. Local automakers fit steel wheels on most entry-level cars. This means suppliers based in Asia-Pacific enjoy scale advantages and proximity to the largest concentration of cost-sensitive buyers.

The Aftermarket channel drives the fastest-growing regional demand for replacement steel wheels. As per our research, rising vehicle parc and harsh road conditions lift replacement rates across developing markets. Owners replace damaged and corroded wheels frequently. This creates recurring revenue, so suppliers expanding regional distribution networks capture faster-growing post-sale demand ahead of slower OEM volume.

North America and Europe hold mature demand centered on fleet and base-vehicle steel wheels. As per our research, both regions favor alloys on premium trims, which caps steel share at the top end. Latin America, the Middle East, and Africa add budget-model volume. This means suppliers should target commercial and entry segments where steel wheels stay standard across these regions.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Market Opportunity Analysis - Underserved commercial, rugged, and emerging-market segments open entry points for focused players

Commercial Vehicles remain underexploited despite steady fleet-linked demand across freight and logistics networks. As per our research, this segment holds a large portion of the remaining Vehicle Type share behind Passenger Cars at 54.60%. Fleet buyers value steel for reparability. This means new entrants targeting commercial programs can win recurring orders that premium alloy suppliers largely ignore.

The Aftermarket channel stays underserved next to OEM dominance at 68.40%. This creates room for suppliers building distribution and service networks close to vehicle owners. Replacement demand rises with vehicle age and road conditions. Therefore investors backing aftermarket-focused players can capture higher-margin, recurring sales that stay independent of new-vehicle production cycles.

Off-Road and Heavy-Duty Use trails Standard Road Use at 49.80%, yet it commands premium pricing. This reflects steel’s advantage in impact resistance for construction and agriculture. New entrants can specialize in rugged wheels rather than compete on budget volume. Instead of chasing crowded passenger contracts, focused players build defensible niches with durability-based value.

Asia-Pacific leads at 44.80%, but the Middle East, Africa, and Latin America stay underpenetrated. This signals headroom for suppliers serving budget-model and commercial demand in these regions. Vehicle ownership continues rising with income growth. Therefore early movers who localize production and distribution can secure share before larger competitors expand into these markets.

Technology and Innovation Landscape - High-strength steels, flow forming, and advanced coatings redefine competitive edges

High-Strength Steel lets manufacturers cut wheel mass while holding load capacity for demanding applications. As per our research, this material forms a rising share of the Material Type segment behind Standard Carbon Steel at 62.10%. Automakers adopt it to meet weight targets. This means suppliers investing in high-strength grades win performance-critical contracts and defend margins.

The Flow Forming process shapes wheels for lighter weight and better strength distribution than basic stamping. This technology trails the Stamping Process at 63.70%, yet it grows fastest. Automakers favor it for weight-sensitive programs. Therefore manufacturers adding flow-forming lines gain a clear edge in bidding for modern, efficiency-focused vehicle platforms.

Alloy-Coated Steel Wheels and advanced finishes extend wheel life in corrosive environments. As per our research, coated and specialty finishes hold share behind Painted Steel Wheels at 46.50%. Buyers in harsh-road markets pay for durability. This creates value-added revenue, so suppliers offering powder-coating and anti-corrosion technology command higher prices.

Forging with steel hybrid processes produces the strongest wheels for heavy-duty and commercial use. This process serves premium load-critical applications beyond conventional stamping. Fleet and off-highway buyers need this strength. Therefore manufacturers with forging capability capture high-margin demand that lower-cost stamped products cannot serve.

Drivers

Entry-level and budget passenger vehicles anchor steel wheel demand across emerging economies. These models account for over half of new registrations in many growth markets, and steel wheels appear on more than 70 to 80% of variants below key price points because they cost 30 to 50% less than aluminum. With regional light-vehicle output rising 2 to 4% yearly, this reliance adds an estimated +1.1% to the baseline CAGR of 2.5%.

Cost-sensitive buyers keep this driver structural rather than temporary. An extra $200 to 400 for alloy wheels stays prohibitive for many first-time owners. This means steel wheel suppliers secure stable, high-volume contracts even as premium mix shifts slowly upward. Therefore firms serving budget programs protect predictable revenue and factory utilization across full production cycles.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Resilient demand for entry-level and budget passenger vehicles using steel wheels | +1.1% | Asia-Pacific, Latin America, Middle East&Africa | Short term (≤ 2 years) |

| OEM cost-optimization programs favoring steel over aluminum in lower trims | +0.7% | Global | Medium term (2–4 years) |

| Growing light commercial vehicle parc in developing economies | +0.5% | Asia-Pacific, Africa | Medium term (2–4 years) |

| Aftermarket replacement demand driven by corrosion and impact damage | +0.4% | Global | Short term (≤ 2 years) |

| Localization and nearshoring of wheel manufacturing by global OEMs | +0.3% | North America, Europe | Medium term (2–4 years) |

Restraints

Alloy wheels now serve as standard fitment on most mid- and high-end passenger vehicles. Penetration frequently exceeds 80 to 90% in C-segment and above, which removes profitable volume that steel suppliers once served on higher-margin trims. As automakers push steel into base and fleet models, average steel wheel content per vehicle can fall by 20 to 40%. This exerts a decremental impact near -1.3% on the baseline CAGR of 2.5%.

Lower winter-wheel option rates deepen this pressure as buyers adopt all-season tires on single alloy sets. This means steel wheel makers face underused stamping and welding capacity built for broader demand. Therefore firms must chase cost leadership or expand into commercial and developing-market programs. Instead of defending premium trims, they should redirect capacity toward high-volume budget and fleet contracts.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward aluminum and alloy wheels in mid- to high-end segments | -1.3% | North America, Europe, China | Medium term (2–4 years) |

| Volatility in flat steel prices and energy costs squeezing wheel margins | -0.9% | Global | Short term (≤ 2 years) |

| Weight-reduction targets under tightening emissions and efficiency norms | -0.7% | Europe, North America | Long term (≥ 4 years) |

| Slowing internal combustion engine vehicle sales in mature markets | -0.6% | Europe, Japan | Medium term (2–4 years) |

| OEM platform consolidation reducing wheel design variety and sourcing points | -0.4% | Global | Medium term (2–4 years) |

Challenges

Automakers pursue vehicle mass cuts of roughly 5 to 10% per generation to meet CO2 and efficiency targets. Traditional steel wheels weigh 2 to 4 kg more per corner than alloy equivalents, which affects ride, handling, and noise performance. To stay on vendor lists, steel makers must adopt thinner, higher-strength steels that shave 10 to 20% off wheel mass. This friction drags around -1.1% on the market’s growth ceiling.

Such redesigns demand multimillion-level tooling and multi-year validation across impact, fatigue, and corrosion tests. This creates a clear opening for suppliers who master high-strength steel engineering first. This means firms that invest early can offer lighter wheels as a paid upgrade tier. Therefore the challenge itself opens a differentiated revenue stream in segments valuing robustness over absolute lightweighting.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Meeting OEM lightweighting and NVH expectations with conventional steel | -1.1% | Global | Long term (≥ 4 years) |

| Tooling and line-changeover costs for diverse OEM platform requirements | -0.9% | Global | Medium term (2–4 years) |

| Quality and corrosion-performance demands in harsh-use markets | -0.8% | Northern Europe, North America | Medium term (2–4 years) |

| Supply-chain disruptions in steel coil, coatings, and logistics | -0.7% | Global | Short term (≤ 2 years) |

| Skilled-labor and welding-automation gaps in emerging production hubs | -0.6% | Asia-Pacific, Eastern Europe | Medium term (2–4 years) |

Opportunities

Rugged-use segments such as pickups, light trucks, and farm equipment still favor steel for impact resistance and reparability. Suppliers can engineer high-strength wheels that run 10 to 15% lighter yet hold loads above 1000 kg per wheel and exceed fatigue rules by 2 to 3x. These applications replace wheels at 3 to 5% of the in-service parc yearly. This creates a large, recurring, premium-tolerant revenue stream.

Buyers in these niches accept price premiums near 5 to 10% for proven performance. This means capturing even single-digit share of global rugged demand over 2 to 4 years adds roughly +1.0% upside to the baseline CAGR of 2.5%. Therefore early movers who shift mix from lowest-cost contracts into performance niches lift average margins. Instead of competing purely on price, they build defensible, differentiated positions.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Next-generation high-strength steel wheel designs for rugged and commercial applications | +1.0% | Global | Medium term (2–4 years) |

| Value-added corrosion-resistant coatings and personalization for aftermarket steel wheels | +0.8% | North America, Europe | Short term (≤ 2 years) |

| Targeting emerging-market EVs and micro-mobility vehicles with optimized steel solutions | +0.7% | Asia-Pacific, Latin America, Africa | Medium term (2–4 years) |

| Modular wheel platforms shared across multiple OEMs to reduce per-unit cost | +0.6% | Global | Long term (≥ 4 years) |

| Closed-loop steel recycling partnerships improving lifecycle emissions profiles | +0.5% | Europe, North America | Long term (≥ 4 years) |

Key Company Insights

Steel Strips Wheels Ltd. holds a strong position in high-volume passenger and commercial steel wheel supply. The company serves cost-sensitive OEM programs where steel stays standard fitment. This scale advantage lets it win large, recurring contracts in growth regions. However, heavy reliance on budget segments exposes it to margin pressure if alloy adoption spreads faster into lower trims than expected across key markets.

Accuride Corporation focuses on commercial vehicle and heavy-duty wheel supply where durability matters most. This positioning protects the company from premium alloy substitution that hits passenger segments. Its strength in fleet and truck programs creates stable, replacement-driven demand. However, concentration in mature North American markets creates risk if commercial vehicle sales slow or nearshoring shifts sourcing patterns among global buyers.

Key Players

- Steel Strips Wheels Ltd.

- Accuride Corporation

- Maxion Wheels

- Topy Industries, Ltd.

- Tata AutoComp Systems Limited

- Ronal Group

- CLN Group

- ALCAR Holding GmbH

- Steel Wheel Corporation

- Zhejiang Wanfeng Auto Wheel Co., Ltd.

- YST Auto Wheel Co., Ltd.

- Jingu Group

- Rays Wheels

- Enkei Corporation

- BBS GmbH

Recent Developments

- April 2025: IKEA India launched its first Plan and Order Point in Bengaluru, expanding an experiential home-design consultation format that lets customers co-design interiors with experts and place orders for full home delivery.

- July 2025: IKEA UK opened a new small-format Harlow store inside a repurposed retail unit, focusing on showroom-style immersive shopping, planning services, and experiential retail integration.

- August 2025: IKEA India opened its first physical store in Delhi at Pacific Mall, introducing a compact urban experience format with 2,000+ display products and in-store design planning services.

- October 2025: Ingka Group, the IKEA retail operator, acquired AI logistics company Locus to enhance end-to-end delivery systems and strengthen omnichannel retail operations globally.

- November 2025: IKEA India expanded its omnichannel ecosystem by strengthening its distribution and design consultation network across Delhi NCR following the launch of its city-format store.

- 2026: IKEA showcased immersive experiential design installations at Milan Design Week under the “Food for Thought” concept, combining furniture, food culture, and interactive exhibition experiences.

- May 2026: IKEA unveiled the upcoming “IKEA PS 2026” experiential furniture collection, including modular, interactive, and multifunctional design products at Milan Design Week.

Geopolitical Impact Analysis

Steel wheel makers face direct input-cost pressure from global trade tension around flat steel. According to the WTO, world merchandise trade volume grew just 2.7% in 2024 amid rising tariff actions. Many economies apply steel import duties near 25%, which raises coil costs for wheel producers. This means suppliers pass higher input prices into contracts. Therefore buyers in tariff-exposed regions face tighter margins and slower sourcing decisions.

Shipping disruptions add further cost and delay to wheel and coil logistics. As reported by UNCTAD, Red Sea rerouting around Africa added roughly 10 extra transit days on affected lanes in 2024. IEA data show energy price swings above 20% lifting steel production costs. This creates supply uncertainty for wheel plants. Consequently manufacturers build regional sourcing and buffer stock to protect delivery reliability.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 16.0 Billion |

| Forecast Revenue (2035) | USD 20.4 Billion |

| CAGR (2026-2035) | 2.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Vehicle Type (Passenger Cars, Commercial Vehicles [Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs)], Off-Highway Vehicles), By Wheel Size (13–15 Inches, 16–18 Inches, Above 18 Inches), By Sales Channel (OEM, Aftermarket), By Material Type (Standard Carbon Steel, High-Strength Steel, Alloy-Coated Steel Wheels), By Application (Standard Road Use, Off-Road & Heavy-Duty Use, Urban Mobility Vehicles, Fleet & Logistics Vehicles), By End User (Automotive Manufacturers, Fleet Operators, Individual Vehicle Owners, Government & Defense Fleets), By Finish Type (Painted Steel Wheels, Powder-Coated Wheels, Chrome-Plated Steel Wheels, Anti-Corrosion Coated Wheels), By Manufacturing Process (Stamping Process, Flow Forming, Forging (Steel Hybrid Processes)) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Steel Strips Wheels Ltd., Accuride Corporation, Maxion Wheels, Topy Industries, Ltd., Tata AutoComp Systems Limited, Ronal Group, CLN Group, ALCAR Holding GmbH, Steel Wheel Corporation, Zhejiang Wanfeng Auto Wheel Co., Ltd., YST Auto Wheel Co., Ltd., Jingu Group, Rays Wheels, Enkei Corporation, BBS GmbH |

| Customization Scope | Customization for segments, region / country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License | Multi-User License (Up to 5 Users) | Corporate Use License (Unlimited User and Printable PDF) |