Global Automotive Drive Shaft Market Size, Share, Growth Analysis By Design Type (Hollow Shaft, Solid Shaft, Two-piece/Slip-in Tube, Composite/Carbon Fiber Shaft), By Material (Conventional Steel, High Strength Alloy Steel, Aluminum, Carbon-Fiber/CFRP), By Position Type (Rear Axle Shafts, Front Axle Shafts, Inter-axle/Propeller Shafts for AWD), By Vehicle Type (Passenger Cars, Light Commercial Vehicles, Medium and Heavy Commercial Vehicles), By Powertrain/Propulsion (Internal Combustion Engine (ICE), Hybrid (HEV and PHEV), Battery Electric Vehicle (BEV)), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179136

- Number of Pages: 267

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaways

- By Design Type Analysis

- By Material Analysis

- By Position Type Analysis

- By Vehicle Type Analysis

- By Powertrain / Propulsion Analysis

- Key Market Segments

- Drivers

- Restraints

- Growth Factors

- Emerging Trends

- Regional Analysis

- Key Regions and Countries

- Key Company Insights

- Recent Developments

- Report Scope

Report Overview

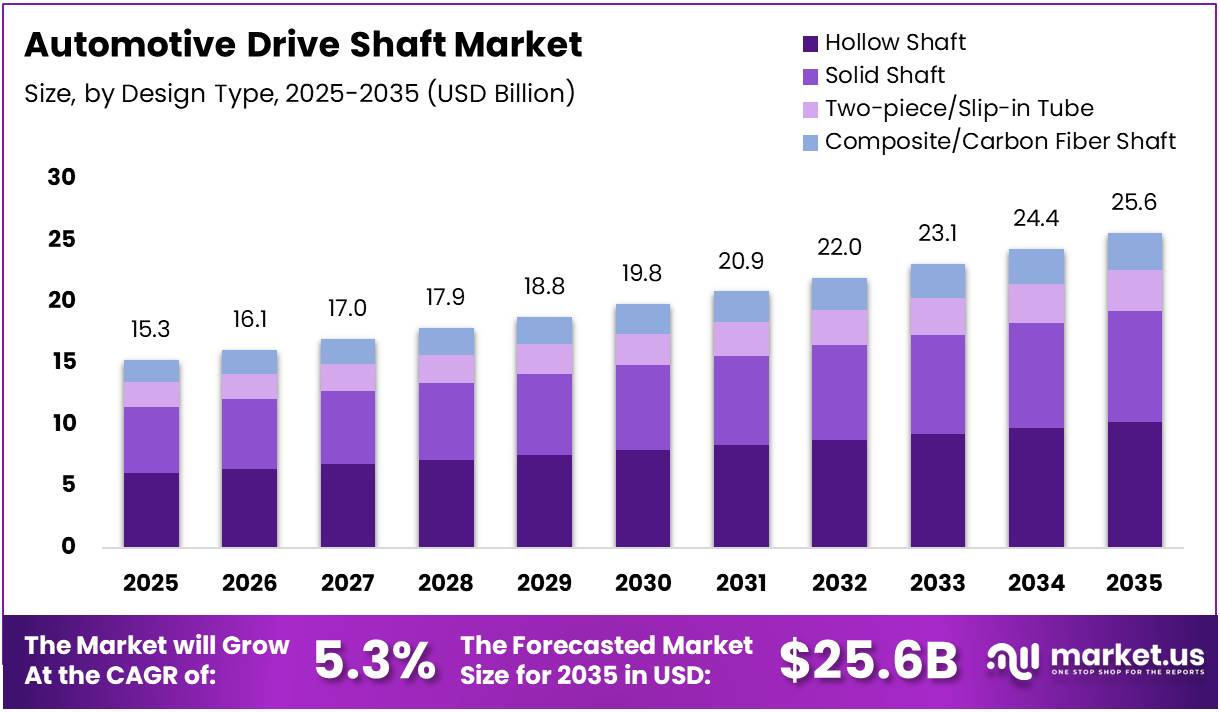

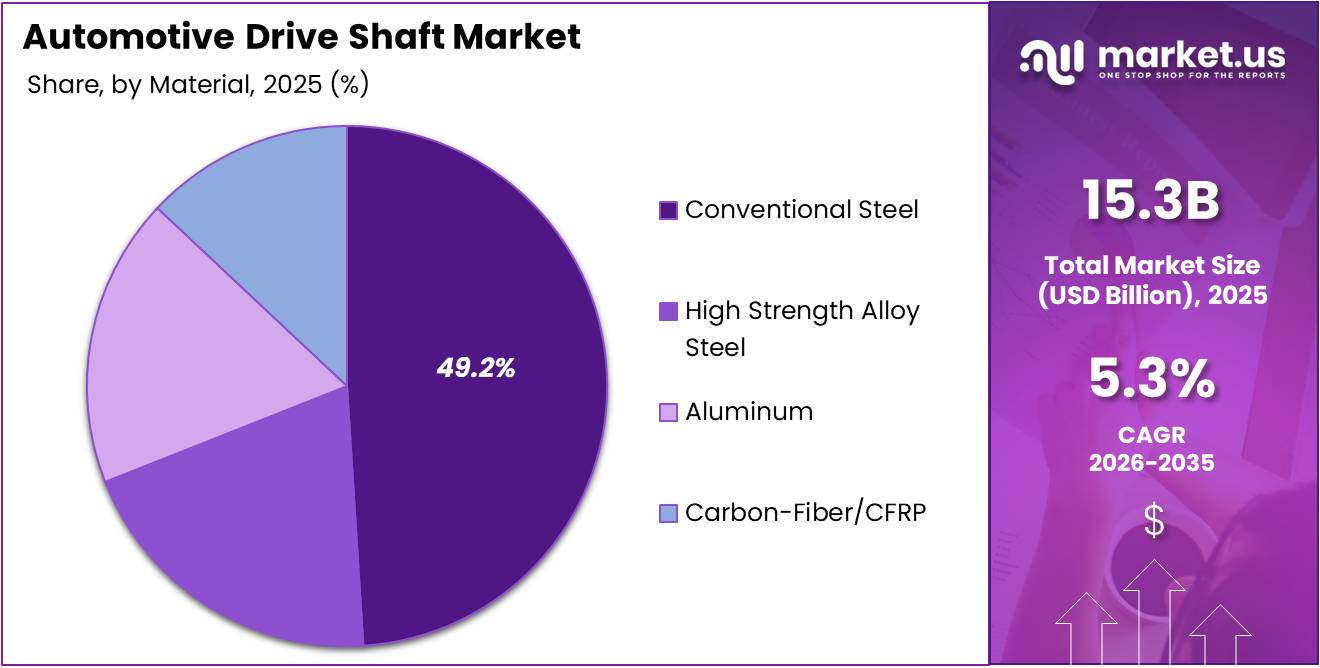

The Global Automotive Drive Shaft Market size is expected to be worth around USD 25.6 Billion by 2035 from USD 15.3 Billion in 2025, growing at a CAGR of 5.3% during the forecast period 2026 to 2035.

The automotive drive shaft is a mechanical component that transmits torque from the engine or transmission to the wheels. It forms a core part of a vehicle’s drivetrain system. Moreover, drive shafts are used across a wide range of vehicle types, including passenger cars, SUVs, and commercial vehicles worldwide.

Drive shafts are engineered using materials such as conventional steel, high-strength alloys, aluminum, and carbon fiber composites. Each material offers distinct advantages in weight, strength, and cost. Consequently, manufacturers select materials based on vehicle performance requirements, OEM platform strategies, and increasingly stringent fuel efficiency standards.

Market growth is largely driven by rising global production of all-wheel drive and four-wheel drive vehicles. Increasing demand for high-torque transmission in SUVs and light trucks is also contributing. Additionally, continuous expansion of automotive manufacturing in emerging economies is supporting sustained market growth across the forecast period.

Government regulations targeting vehicle emissions and fuel efficiency are pushing automakers toward lightweight drivetrain solutions. Therefore, the adoption of composite and hollow shaft designs is accelerating. These innovations align directly with global sustainability goals and support OEM efforts to reduce overall vehicle curb weight.

Electric and hybrid vehicle platforms are generating new demand for specialized high-speed drive shafts. However, the conventional shaft segment remains dominant due to the large installed base of ICE vehicles globally. The aftermarket replacement segment is also expanding as vehicle lifespans increase and fleet owners seek cost-effective drivetrain maintenance options.

According to research published in the International Journal of Simulation Modelling (IJSIMM), composite drive shafts deliver a weight reduction of up to 65% compared to conventional steel. Furthermore, CFRP drive shafts can achieve over 30% weight reduction compared to traditional metallic counterparts, making them highly attractive for next-generation vehicle platforms.

The same IJSIMM study confirms that optimized composite drive shafts demonstrate up to 79.6% weight reduction versus steel tubes in simulation. Additionally, shape optimization can reduce maximum torsional stress by 11.5%, increase fatigue life by 3.7 times, and decrease component weight by approximately 25%.

Key Takeaways

- The global Automotive Drive Shaft Market is valued at USD 15.3 Billion in 2025 and is projected to reach USD 25.6 Billion by 2035.

- The market is growing at a CAGR of 5.3% during the forecast period 2026 to 2035.

- By Design Type, Hollow Shaft dominates with a market share of 39.6% in 2025.

- By Material, Conventional Steel holds the leading position with a share of 49.2%.

- By Position Type, Rear Axle Shafts account for the largest share at 44.8%.

- By Vehicle Type, Passenger Cars represent the dominant segment with 59.3% market share.

- By Powertrain, Internal Combustion Engine (ICE) vehicles lead with a commanding 71.1% share.

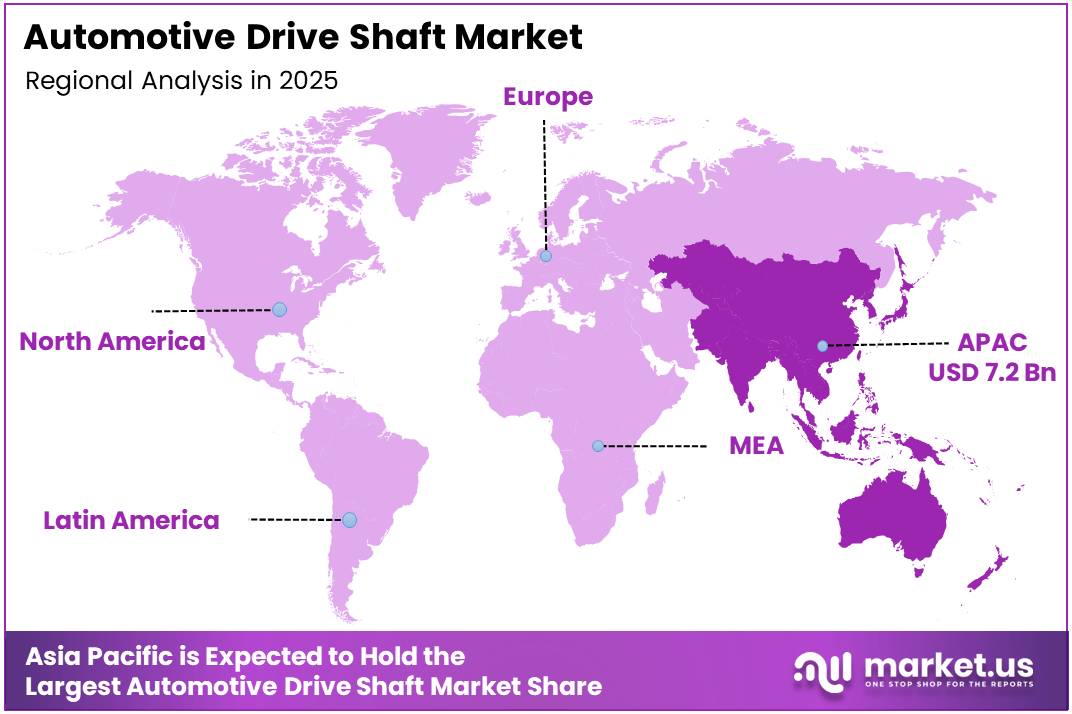

- Asia Pacific is the dominant region, holding 47.2% of the global market, valued at USD 7.2 Billion in 2025.

By Design Type Analysis

Hollow Shaft dominates with 39.6% due to its lightweight properties and wide adoption in passenger and commercial vehicle drivetrain systems.

In 2025, Hollow Shaft held a dominant market position in the By Design Type segment of the Automotive Drive Shaft Market, with a 39.6% share. Hollow shafts offer significant weight savings compared to solid alternatives. Moreover, their vibration dampening properties and torsional strength make them a preferred choice for modern high-efficiency vehicle platforms.

Solid Shaft remains relevant in heavy-duty and high-torque applications where structural rigidity is paramount. These shafts are commonly used in rear-wheel drive trucks and larger commercial vehicles. However, their higher weight compared to hollow designs limits their use in fuel-sensitive passenger car segments where weight reduction is a priority.

Two-piece/Slip-in Tube shafts are widely used in longer-wheelbase vehicles such as rear-wheel drive sedans and pickups. They accommodate driveline length variations and reduce vibration. Additionally, their modular design supports easier manufacturing and assembly processes, making them cost-effective for mid-size and full-size vehicle applications.

Composite/Carbon Fiber Shaft represents the fastest-growing sub-segment, driven by the need for extreme weight reduction and high performance. These shafts are increasingly adopted in electric vehicles and premium passenger cars. Consequently, continued investment in composite manufacturing technologies is expected to expand this sub-segment’s share over the forecast period.

By Material Analysis

Conventional Steel dominates with 49.2% due to its cost-effectiveness, wide availability, and proven performance in mass-market vehicle production.

In 2025, Conventional Steel held a dominant market position in the By Material segment of the Automotive Drive Shaft Market, with a 49.2% share. Steel drive shafts remain the most widely used due to their low production cost and reliable mechanical properties. Moreover, their established manufacturing infrastructure supports high-volume OEM supply chains globally.

High Strength Alloy Steel is gaining traction as automakers seek improved performance without significantly increasing costs. These materials offer better fatigue resistance and torque capacity than conventional steel. Consequently, high-strength alloy steel shafts are increasingly specified in SUVs, trucks, and performance-oriented passenger vehicle platforms requiring enhanced drivetrain durability.

Aluminum drive shafts are valued for their favorable strength-to-weight ratio and corrosion resistance. They are commonly used in lightweight vehicle architectures and performance applications. Additionally, rising aluminum adoption in vehicle body structures is creating complementary demand for aluminum drivetrain components, particularly in electric and hybrid vehicle segments.

Carbon-Fiber/CFRP shafts represent the premium end of the material spectrum, offering the highest weight savings and torsional performance. Their adoption is accelerating in electric vehicles and high-performance models. However, higher manufacturing costs remain a constraint, and continued advancements in CFRP production efficiency are expected to broaden their commercial application range.

By Position Type Analysis

Rear Axle Shafts dominate with 44.8% due to high demand from rear-wheel and all-wheel drive vehicle platforms across passenger and commercial segments.

In 2025, Rear Axle Shafts held a dominant market position in the By Position Type segment of the Automotive Drive Shaft Market, with a 44.8% share. These shafts are integral to rear-wheel drive and all-wheel drive vehicles. Moreover, strong demand from pickup trucks, SUVs, and commercial vehicle categories continues to reinforce this segment’s leadership position globally.

Front Axle Shafts are critical components in front-wheel drive and all-wheel drive vehicles, which account for the majority of global passenger car production. Their design requirements are more complex due to steering articulation. Consequently, continuous engineering improvements in constant velocity joints and shaft geometry are enhancing durability and performance in this segment.

Inter-axle/Propeller Shafts for AWD are seeing growing demand driven by the expanding global market for all-wheel drive and four-wheel drive vehicles. These shafts transfer power between front and rear axles in complex drivetrains. Additionally, rising consumer preference for AWD-equipped crossovers and SUVs in North America, Europe, and Asia Pacific is sustaining strong growth momentum.

By Vehicle Type Analysis

Passenger Cars dominate with 59.3% due to their large global production volumes and widespread use of front-wheel and all-wheel drive configurations.

In 2025, Passenger Cars held a dominant market position in the By Vehicle Type segment of the Automotive Drive Shaft Market, with a 59.3% share. Passenger cars represent the largest vehicle production segment globally. Moreover, the growing popularity of SUVs and crossovers within the passenger car category is further amplifying demand for advanced drive shaft solutions.

Light Commercial Vehicles represent a significant and steadily growing segment, driven by increasing last-mile delivery and logistics activity worldwide. These vehicles require robust and durable drive shafts to handle varied load conditions. Additionally, the expansion of e-commerce infrastructure is boosting light commercial vehicle production across emerging and developed markets alike.

Medium and Heavy Commercial Vehicles demand high-torque, heavy-duty drive shafts designed for extreme load-bearing and long-distance performance. Infrastructure development and freight transportation growth are key demand drivers. Consequently, manufacturers in this segment continue to develop reinforced shaft designs using high-strength alloy steel to meet the rigorous operational demands of fleet operators.

By Powertrain / Propulsion Analysis

Internal Combustion Engine (ICE) dominates with 71.1% due to its continued dominance in global vehicle production and the large existing fleet of ICE vehicles.

In 2025, Internal Combustion Engine held a dominant market position in the By Powertrain/Propulsion segment of the Automotive Drive Shaft Market, with a 71.1% share. ICE vehicles continue to represent the majority of global automotive production and sales. Moreover, the extensive global service infrastructure supporting ICE platforms sustains consistent demand for conventional drive shaft solutions.

Hybrid (HEV and PHEV) vehicles require specialized drive shafts capable of handling both combustion and electric torque inputs. This dual-powertrain configuration places unique demands on shaft design and material selection. Additionally, growing government incentives for hybrid vehicles across major markets are accelerating hybrid platform production and consequently driving demand for high-performance hybrid-compatible shafts.

Battery Electric Vehicle (BEV) platforms are transforming drive shaft requirements with the need for high-speed, lightweight, and compact shaft solutions. Some EV architectures adopt hub motors that reduce shaft usage. However, multi-motor AWD EVs continue to require advanced drive shaft components, and the rapid EV market expansion is creating sustained long-term growth opportunities for specialized shaft manufacturers.

Key Market Segments

By Design Type

- Hollow Shaft

- Solid Shaft

- Two-piece/Slip-in Tube

- Composite/Carbon Fiber Shaft

By Material

- Conventional Steel

- High Strength Alloy Steel

- Aluminum

- Carbon-Fiber/CFRP

By Position Type

- Rear Axle Shafts

- Front Axle Shafts

- Inter-axle/Propeller Shafts for AWD

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Medium and Heavy Commercial Vehicles

By Powertrain / Propulsion

- Internal Combustion Engine (ICE)

- Hybrid (HEV and PHEV)

- Battery Electric Vehicle (BEV)

Drivers

Rising AWD/4WD Production and High-Torque Demand Drive Automotive Drive Shaft Market Growth

Rising global production of all-wheel drive and four-wheel drive vehicles is a primary growth driver for the automotive drive shaft market. Automakers are expanding AWD platforms across crossovers, SUVs, and trucks. Consequently, demand for reliable and high-performance propeller and axle shafts is increasing consistently across both emerging and mature automotive markets.

Increasing demand for high-torque transmission systems in SUVs and light trucks is pushing manufacturers to develop more capable and durable drive shaft solutions. These vehicles require shafts that can handle greater torsional loads without adding excess weight. Therefore, investment in high-strength alloy and composite shaft technologies is accelerating among leading OEM suppliers.

Continuous expansion of automotive manufacturing in emerging economies such as India, Southeast Asia, and Brazil is further supporting market growth. New production facilities in these regions are creating localized demand for drive shaft components. Additionally, growing middle-class vehicle ownership in these markets is driving both OEM production volumes and aftermarket replacement demand simultaneously.

Restraints

Shift Toward Direct Drive EV Architectures and Engineering Complexity Restrain Market Growth

The increasing shift toward hub motor and direct drive architectures in battery electric vehicles is reducing the need for conventional drive shafts in certain EV platforms. As more automakers adopt in-wheel motor technology, traditional shaft components become redundant. Consequently, this structural change in powertrain design poses a long-term restraint on conventional drive shaft demand.

Complex engineering requirements for high-speed and high-torque drive shaft applications create significant development challenges for manufacturers. Designing shafts that maintain structural integrity under extreme rotational speeds while minimizing vibration and noise requires advanced simulation and testing capabilities. Therefore, smaller suppliers often struggle to meet the technical specifications demanded by premium and performance vehicle programs.

Additionally, the transition to electric vehicle platforms requires entirely new shaft designs that differ significantly from ICE-compatible components. This forces manufacturers to invest heavily in retooling and R&D. Moreover, the pace of EV adoption varies considerably by region, creating demand uncertainty that complicates long-term production planning and capital allocation for drive shaft manufacturers globally.

Growth Factors

Lightweight Materials, EV Expansion, and Aftermarket Demand Accelerate Automotive Drive Shaft Market Growth

Development of lightweight composite and carbon fiber drive shafts presents a major growth opportunity for the market. These advanced materials deliver significant weight reduction while maintaining superior torsional performance. Moreover, stricter global fuel efficiency regulations are encouraging automakers to adopt composite shaft solutions across both mainstream and premium vehicle segments to reduce overall vehicle mass.

Expansion of electric and hybrid vehicle platforms is creating strong demand for specialized high-speed drive shafts designed for electrified powertrains. These platforms require shafts with unique performance characteristics compared to conventional ICE applications. Consequently, manufacturers investing early in EV-compatible shaft technologies are positioned to capture a growing share of the rapidly expanding electrified vehicle drivetrain market.

Rising aftermarket replacement demand is another key growth factor, driven by the extended average lifespan of vehicles in service globally. Aging fleets require regular drivetrain maintenance and component replacement. Additionally, increasing vehicle parc in developing regions is expanding the aftermarket customer base, creating a reliable and growing revenue stream for drive shaft manufacturers and independent parts distributors.

Emerging Trends

Modular Designs, Hollow Configurations, and Smart Monitoring Reshape the Automotive Drive Shaft Market

Adoption of modular and scalable drive shaft designs is gaining momentum as automakers shift toward platform-based vehicle development strategies. Standardized shaft architectures allow manufacturers to reuse components across multiple models and powertrains. Moreover, this approach reduces development costs, shortens time-to-market, and simplifies supply chain management for both OEMs and tier-one drivetrain component suppliers.

Increased use of hollow and multi-piece shaft configurations is a prominent trend driven by the need for weight optimization across all vehicle segments. Hollow shafts reduce mass without compromising torsional stiffness or fatigue resistance. Consequently, their adoption is expanding beyond performance vehicles into mainstream passenger cars and light commercial vehicles as efficiency requirements become more stringent globally.

Integration of smart monitoring systems for predictive maintenance is emerging as a transformative trend in the drive shaft segment. Sensors embedded in drivetrain components can detect vibration anomalies and torque irregularities in real time. Additionally, this technology supports proactive maintenance scheduling, reduces unexpected vehicle downtime, and aligns with the broader automotive industry trend toward connected and intelligent vehicle systems.

Regional Analysis

Asia Pacific Dominates the Automotive Drive Shaft Market with a Market Share of 47.2%, Valued at USD 7.2 Billion

Asia Pacific leads the global automotive drive shaft market, holding a dominant share of 47.2%, valued at USD 7.2 Billion in 2025. The region benefits from the world’s largest automotive manufacturing base, concentrated in China, Japan, South Korea, and India. Moreover, rapid growth in SUV and passenger car production across these countries continues to reinforce Asia Pacific’s market leadership.

North America Automotive Drive Shaft Market Trends

North America represents a significant market for automotive drive shafts, supported by strong demand for trucks, SUVs, and all-wheel drive vehicles. The United States is the primary contributor, driven by robust consumer preference for light trucks and crossovers. Additionally, the growing adoption of hybrid and electric vehicles is creating new demand for specialized high-speed shaft solutions in the region.

Europe Automotive Drive Shaft Market Trends

Europe is a mature and innovation-driven market for automotive drive shafts, with Germany, France, and the UK leading regional production. Stringent EU emissions regulations are accelerating the shift toward lightweight composite shaft materials. Furthermore, the region’s strong presence of premium automotive OEMs is driving demand for advanced high-performance drivetrain components across both passenger and commercial vehicle segments.

Latin America Automotive Drive Shaft Market Trends

Latin America presents a growing market opportunity, primarily led by Brazil and Mexico, which serve as key automotive production hubs in the region. Rising vehicle ownership rates and expanding manufacturing investments are driving steady demand. However, economic volatility and import dependency on raw materials and components remain challenges that can affect production costs and market growth pace.

Middle East and Africa Automotive Drive Shaft Market Trends

The Middle East and Africa region represents an emerging market for automotive drive shafts, supported by rising vehicle sales and fleet expansion in GCC countries and South Africa. Infrastructure development and increasing commercial vehicle activity are key demand drivers. Additionally, growing imports of passenger vehicles are creating consistent aftermarket replacement demand for drive shaft components across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

GKN PLC (Melrose Industries PLC) is one of the most recognized names in global driveline technology, offering a comprehensive range of drive shafts and constant velocity joints for passenger and commercial vehicles. The company serves major OEMs across multiple continents and has a strong focus on lightweight and electrified drivetrain solutions, making it a strategic partner for next-generation vehicle programs.

Dana Incorporated is a global leader in drivetrain and sealing solutions, supplying drive shafts for light vehicles, commercial trucks, and off-highway equipment. The company has made significant investments in electric vehicle driveline technologies. Moreover, Dana’s diversified customer base and end-market exposure across multiple vehicle segments provide strong resilience and long-term revenue stability within the global automotive drive shaft market.

JTEKT Corporation is a prominent supplier of driveline components including drive shafts and steering systems, with deep manufacturing capabilities across Asia and Europe. The company’s engineering expertise in precision components supports high-performance drivetrain applications. Additionally, JTEKT’s close integration with major Japanese and international OEMs gives it a competitive advantage in delivering application-specific shaft solutions at scale.

Hyundai Wia Corporation is a key player in the automotive drive shaft market, closely aligned with the Hyundai Motor Group and supplying drivetrain components to multiple global OEM customers. The company’s vertically integrated manufacturing model supports cost-efficient production. Furthermore, Hyundai Wia’s ongoing expansion in electric vehicle component manufacturing positions it well for growth as electrified platform demand continues to rise across the Asia Pacific region.

Key Players

- GKN PLC (Melrose Industries PLC)

- Dana Incorporated

- JTEKT Corporation

- Hyundai Wia Corporation

- Nexteer Automotive Group Ltd.

- American Axle and Manufacturing Holdings Inc.

- NTN Corporation

- Showa Corporation

- IFA Rotorion Holding GmbH

- ZF Friedrichshafen AG

Recent Developments

- December 2025 – Munich-based industrial group AEQUITA completed the sale of drive shaft and joint manufacturer IFA Rotorion to Neapco, a leading global supplier of driveline solutions. This transaction strengthens Neapco’s product portfolio and expands its manufacturing footprint within the global automotive drive shaft supply chain.

- January 2025 – American Axle & Manufacturing (AAM) reached an agreement to acquire Dowlais Group plc, the parent company of GKN Automotive, in a transaction valued at approximately $1.4 billion. This strategic acquisition significantly expands AAM’s global driveline capabilities and positions the combined entity as a major force in the automotive drive shaft and driveline components market.

Report Scope

Report Features Description Market Value (2025) USD 15.3 Billion Forecast Revenue (2035) USD 25.6 Billion CAGR (2026-2035) 5.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Design Type (Hollow Shaft, Solid Shaft, Two-piece/Slip-in Tube, Composite/Carbon Fiber Shaft), By Material (Conventional Steel, High Strength Alloy Steel, Aluminum, Carbon-Fiber/CFRP), By Position Type (Rear Axle Shafts, Front Axle Shafts, Inter-axle/Propeller Shafts for AWD), By Vehicle Type (Passenger Cars, Light Commercial Vehicles, Medium and Heavy Commercial Vehicles), By Powertrain/Propulsion (Internal Combustion Engine (ICE), Hybrid (HEV and PHEV), Battery Electric Vehicle (BEV)) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape GKN PLC (Melrose Industries PLC), Dana Incorporated, JTEKT Corporation, Hyundai Wia Corporation, Nexteer Automotive Group Ltd., American Axle and Manufacturing Holdings Inc., NTN Corporation, Showa Corporation, IFA Rotorion Holding GmbH, ZF Friedrichshafen AG Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Automotive Drive Shaft MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Automotive Drive Shaft MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- GKN PLC (Melrose Industries PLC)

- Dana Incorporated

- JTEKT Corporation

- Hyundai Wia Corporation

- Nexteer Automotive Group Ltd.

- American Axle and Manufacturing Holdings Inc.

- NTN Corporation

- Showa Corporation

- IFA Rotorion Holding GmbH

- ZF Friedrichshafen AG

Our Clients

- 179136

- Feb 2026