Quick Navigation

Report Overview

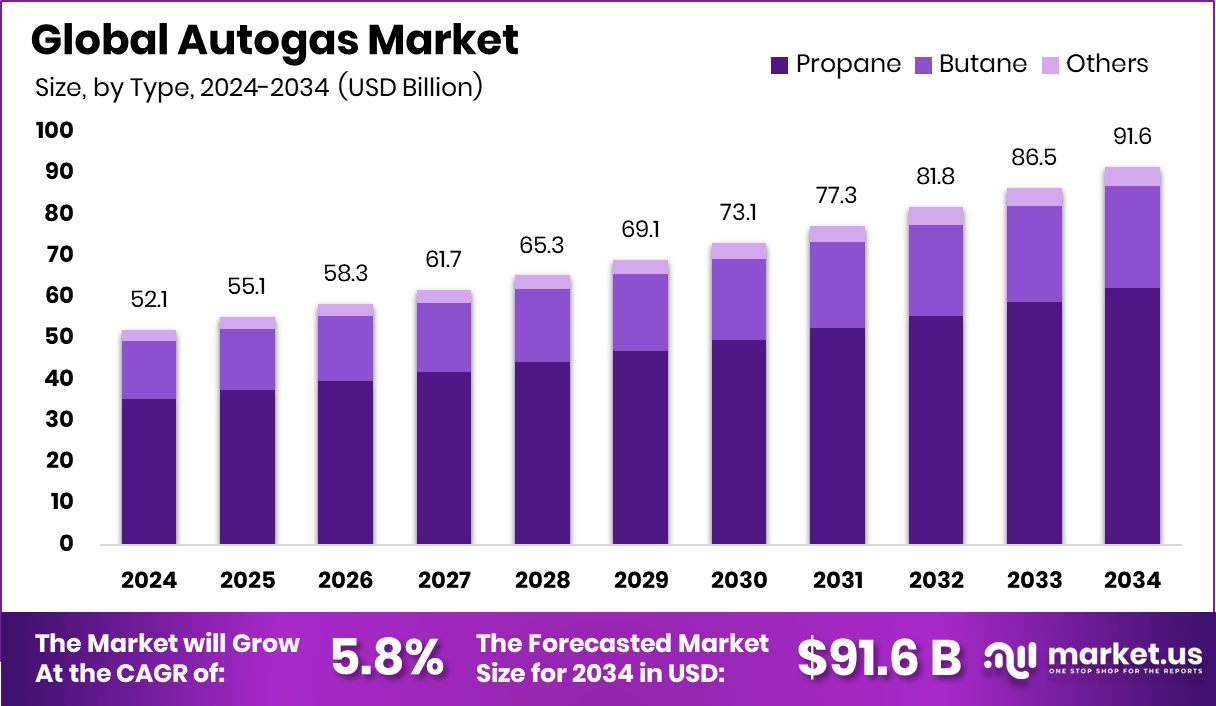

Global Autogas Market is expected to be worth around USD 91.6 billion by 2034, up from USD 52.1 billion in 2024, and grow at a CAGR of 5.8% from 2025 to 2034. Strong government support in Asia-Pacific boosts autogas usage, driving the 47.9% share.

Autogas, commonly known as LPG (liquefied petroleum gas) used for vehicles, is a clean-burning alternative fuel made primarily of propane or a propane-butane mix. It is stored in liquid form under pressure and is widely used in light-duty vehicles, taxis, and commercial fleets due to its lower emissions and cost-effectiveness compared to gasoline and diesel. Autogas combustion produces fewer particulates and greenhouse gases, making it a preferred fuel for environmentally conscious transport.

The autogas market revolves around the production, distribution, and consumption of LPG as a vehicle fuel. It includes infrastructure such as filling stations, retrofitting services, fuel supply chains, and associated vehicle technologies. The market caters to both OEM (original equipment manufacturer) and aftermarket segments, spanning across private vehicles, taxis, public transport fleets, and logistics operations. It is influenced by fuel pricing, regulatory policies, environmental goals, and consumer awareness.

Stringent emission regulations and rising fuel prices are compelling governments and consumers to consider cleaner, cheaper alternatives. Autogas offers up to 20% lower carbon dioxide emissions than petrol, which is a key driver for its adoption in urban mobility policies. In several regions, fiscal incentives and subsidies further encourage vehicle conversions, pushing steady growth. According to an industry report, Missouri Provides Nearly $1 million in Propane School Bus Funding for School Districts

The rising cost of conventional fuels and the need for affordable transportation options lead to increased demand for autogas. Commercial fleets, especially in emerging economies, are converting to LPG to reduce fuel expenses and maintenance costs. Public transport and taxi operators are particularly active in adopting autogas due to high fuel usage.

Key Takeaways

- Global Autogas Market is expected to be worth around USD 91.6 billion by 2034, up from USD 52.1 billion in 2024, and grow at a CAGR of 5.8% from 2025 to 2034.

- Propane dominates the Autogas Market by type, accounting for 67.9% due to widespread vehicle compatibility.

- Liquefied Petroleum Gas leads the Autogas Market by product type with 87.3% share from extensive adoption.

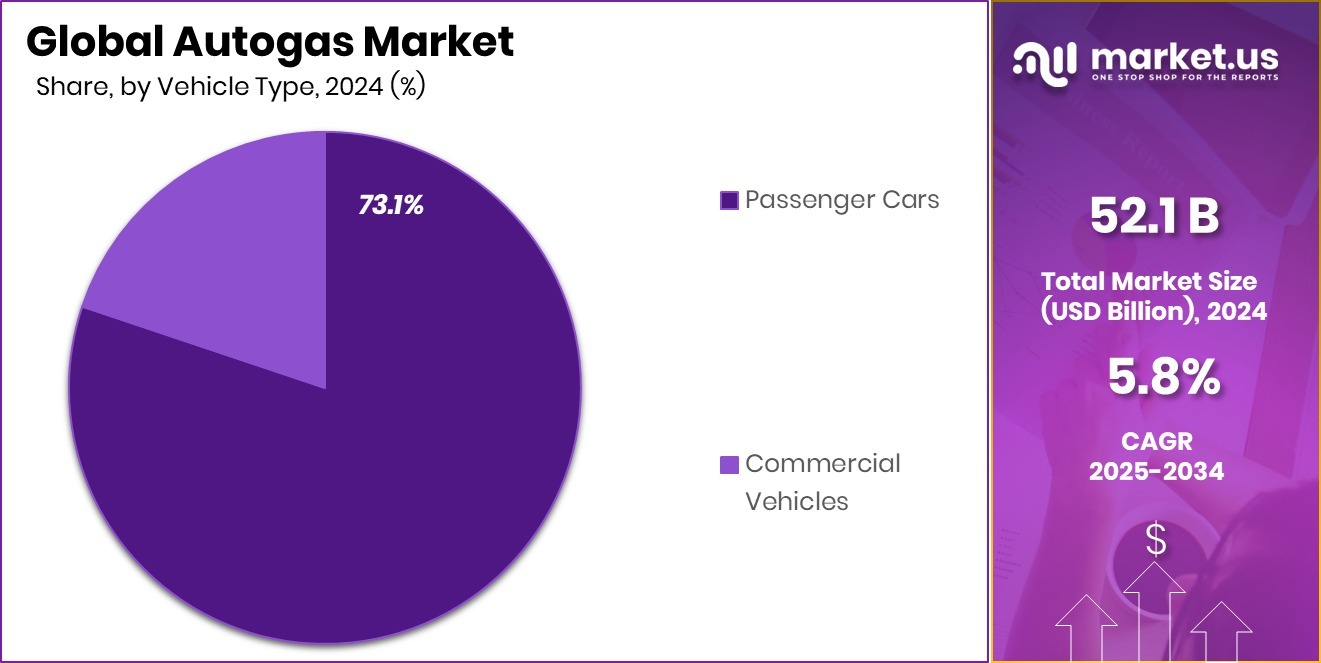

- Passenger Cars represent 73.1% of the Autogas Market by vehicle type, driven by urban transport needs.

- Aftermarket conversions capture 67.8% of the Autogas Market by conversion type, enabling cost-effective fuel switching.

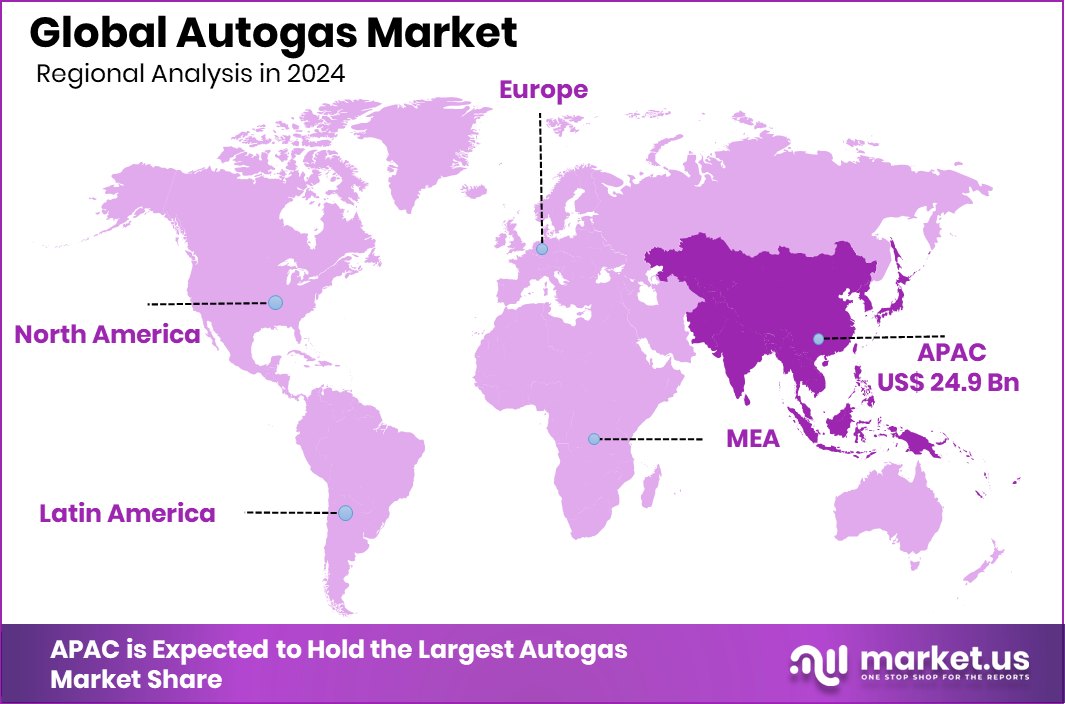

- The autogas market in Asia-Pacific reached a value of USD 24.9 billion.

By Type Analysis

Propane dominates the Autogas Market by type, holding a 67.9% share.

In 2024, Propane held a dominant market position in the By Type segment of the Autogas Market, accounting for a significant 67.9% share. This dominance is primarily attributed to propane’s widespread availability, cleaner combustion profile, and relatively lower cost compared to conventional fuels.

Its chemical properties make it highly efficient for internal combustion engines, resulting in reduced engine wear and lower maintenance costs—an attractive proposition for fleet operators and cost-conscious consumers. Propane’s compatibility with existing vehicle technologies and the ease of retrofitting further enhance its market penetration.

Government initiatives across multiple countries supporting the use of low-emission fuels have also played a key role in reinforcing propane’s market leadership. As environmental regulations become stricter, propane’s cleaner-burning nature compared to diesel and petrol strengthens its appeal. Moreover, propane’s favorable storage and distribution characteristics make it suitable for diverse geographic and climatic conditions, encouraging infrastructure development in both urban and semi-urban regions.

Its adoption has particularly gained momentum in public transportation, commercial fleets, and taxis, where fuel economy and reduced emissions are crucial factors. Given these advantages, propane is expected to maintain its leading position in the Autogas Market’s type segment over the coming years, supported by continued policy backing and rising demand for alternative fuels.

By Product Type Analysis

Liquefied Petroleum Gas leads the Autogas Market product types with 87.3% market share.

In 2024, Liquefied Petroleum Gas (LPG) held a dominant market position in the By Product Type segment of the Autogas Market, capturing an impressive 87.3% share. This commanding lead is largely due to LPG’s established presence as a clean, efficient, and cost-effective fuel for automotive use.

Its high energy density and reliable performance have made it the preferred choice for both private and commercial vehicle owners seeking an alternative to conventional fuels. Additionally, LPG’s lower carbon footprint and reduced harmful emissions compared to petrol and diesel have positioned it as a favorable solution amid increasing regulatory pressure for cleaner transportation.

The infrastructure supporting LPG, including refueling stations and vehicle conversion systems, is also more mature and widespread compared to other alternative fuels, enabling smoother adoption and greater consumer confidence. Furthermore, the affordability of LPG—both in terms of fuel price and conversion cost—has made it particularly attractive in price-sensitive markets.

Strong governmental backing through subsidies, tax rebates, and supportive emission norms has further solidified LPG’s position in the autogas landscape. As consumer awareness grows and environmental concerns intensify, LPG is expected to maintain its dominance within the product type category, continuing to lead the shift toward sustainable automotive fuel solutions.

By Vehicle Type Analysis

Passenger cars represent 73.1% of the global Autogas Market by vehicle type.

In 2024, Passenger Cars held a dominant market position in the By Vehicle Type segment of the Autogas Market, accounting for a substantial 73.1% share. This dominance is primarily driven by the growing consumer preference for economical and environmentally friendly fuel alternatives in personal transportation.

Autogas, particularly in the form of LPG, offers a significant reduction in fuel costs and vehicle emissions, making it an appealing choice for budget-conscious car owners and environmentally aware drivers.

The ease of retrofitting passenger cars with autogas-compatible systems has further supported its uptake in this segment. In many urban centers, where pollution control policies are becoming increasingly strict, autogas-powered passenger vehicles are gaining traction as a viable solution to comply with emission norms while keeping operational costs low.

Additionally, the relatively low maintenance requirements and extended engine life associated with autogas use have reinforced its popularity in this category. With continued support from regulatory bodies and rising awareness among individual vehicle owners, passenger cars are expected to remain the leading contributors to the autogas market within the vehicle type segment.

By Conversion Type Analysis

Aftermarket conversions account for 67.8% in the Autogas Market conversion segment.

In 2024, Aftermarket held a dominant market position in the By Conversion Type segment of the Autogas Market, securing a notable 67.8% share. This leadership is primarily attributed to the cost-effectiveness and flexibility that aftermarket conversions offer to vehicle owners.

Many consumers, particularly in cost-sensitive regions, opt to convert their existing petrol or diesel vehicles to autogas rather than purchasing factory-fitted models. This allows them to benefit from lower fuel costs and reduced emissions without the higher upfront investment of new vehicles.

The widespread availability of aftermarket conversion kits and service providers has significantly contributed to the segment’s expansion. Additionally, regulatory support in the form of approvals for certified retrofitting and incentives for alternative fuel adoption has encouraged this trend. Commercial drivers, such as taxi and delivery operators, often favor aftermarket solutions due to their quick turnaround time and immediate cost savings on fuel expenditure.

The dominance of this segment reflects the practical approach many vehicle owners are taking in adopting autogas—prioritizing affordability, convenience, and environmental benefit. As awareness of autogas benefits continues to grow and as governments promote low-emission mobility, the aftermarket segment is expected to maintain its strong position in the overall conversion type landscape.

Key Market Segments

By Type

- Propane

- Butane

- Others

By Product Type

- Compressed Natural Gas

- Liquefied Petroleum Gas

- Liquefied Natural Gas

- Others

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

By Conversion Type

- Aftermarket

- OEM

Driving Factors

High Fuel Savings Make Autogas a Top Choice

One of the biggest reasons people and businesses are choosing autogas is the clear fuel cost savings. Autogas, especially in the form of LPG, is cheaper than petrol or diesel in many countries. For drivers who travel long distances daily, such as taxi operators or delivery vehicles, switching to autogas can mean spending much less on fuel every month.

These savings add up over time and help lower the overall cost of vehicle ownership. Because of this, more car owners and fleet operators are switching to autogas. With fuel prices remaining high in many places, the strong cost advantage of autogas is a major reason behind its growing popularity across the world.

Restraining Factors

Limited Refueling Stations Reduce Autogas Adoption Speed

A major challenge holding back the growth of the autogas market is the limited number of refueling stations. In many regions, especially rural areas or smaller cities, autogas pumps are not as common as petrol or diesel stations. This lack of easy access makes drivers hesitant to switch to autogas, even if it is cheaper. People worry they may not find a station nearby when needed, which creates range anxiety.

For commercial fleet operators, route planning becomes more difficult if refueling options are scarce. Without a strong and wide network of autogas refueling infrastructure, adoption remains slow, especially outside urban centers. Expanding this network is key to overcoming this hurdle in the future.

Growth Opportunity

Growing Demand in Developing Countries Drives Opportunity

One of the biggest growth opportunities for the autogas market lies in developing countries. Many of these nations are searching for affordable and cleaner fuel options to meet rising transport needs. Autogas fits well because it is cheaper than petrol or diesel and produces fewer harmful emissions. In places where public transport and taxi services are expanding, switching to autogas can help reduce fuel costs and improve air quality.

Governments in these regions are also starting to support alternative fuels through tax breaks and conversion incentives. As urbanization increases and more vehicles hit the roads, the demand for cost-effective fuel like autogas is expected to grow quickly, especially in Asia, Africa, and Latin America.

Latest Trends

Renewable Propane Gains Momentum in Autogas Market

A notable trend in the autogas market is the increasing adoption of renewable propane. Produced from sustainable sources like biomass and vegetable oils, renewable propane offers a cleaner alternative to conventional fuels. It seamlessly integrates with existing autogas infrastructure, allowing vehicles to operate without modifications. This compatibility makes the transition to renewable propane straightforward for both consumers and fleet operators.

Renewable propane addresses these concerns by significantly reducing greenhouse gas emissions. Its growing popularity is evident among various sectors, including school transportation and commercial fleets, which are seeking sustainable and cost-effective fuel options.

Regional Analysis

Asia-Pacific held a 47.9% share in the autogas market during 2024.

In 2024, Asia-Pacific emerged as the dominant region in the global autogas market, accounting for a substantial 47.9% share, equivalent to USD 24.9 billion. This leading position is driven by widespread adoption of autogas in densely populated countries where fuel affordability and air quality regulations are major concerns.

Government-backed incentives, favorable fuel pricing policies, and a growing fleet of passenger and commercial vehicles are key contributors to the region’s dominance. Additionally, the availability of autogas infrastructure and retrofitting services across urban areas supports steady growth.

In Europe, the autogas market is supported by stringent emission norms and environmental regulations aimed at reducing vehicle-related pollution. Countries in this region have long promoted LPG as a cleaner alternative fuel, contributing to a consistent user base. North America presents moderate adoption, primarily concentrated in select fleets and government transport segments where cost savings are prioritized.

In Latin America and the Middle East & Africa, adoption remains comparatively lower but shows potential due to growing awareness of low-emission fuels and interest in fuel diversification. However, limited infrastructure and economic constraints challenge wider market expansion in these regions.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, Aygaz A.Ş. reinforced its leadership position in the autogas sector through a strong domestic market presence and a robust distribution network across Turkey. The company has consistently invested in expanding its autogas infrastructure, including refueling stations and vehicle conversion services, making it one of the most accessible autogas providers in its region.

BP plc continues to support autogas as part of its broader low-carbon energy transition strategy. The company leverages its extensive retail fuel network to promote LPG as a cleaner-burning automotive fuel across select European and Asian markets. BP’s approach involves aligning its autogas offerings with national emission reduction targets, making it an active player in regions where regulatory policies favor alternative fuels.

Chevron Corporation maintains a more focused and regionalized participation in the autogas space. While its core business remains upstream and downstream oil, Chevron has strategically engaged in markets where autogas adoption is on the rise, particularly through partnerships and supply agreements.

Top Key Players in the Market

- AmeriGas Partners LP

- Aygaz A.S.

- BP plc

- Chevron Corporation

- China Petroleum & Chemical Corporation

- ConocoPhillips Company

- Ferrellgas Partners LP

- Flogas Britain Limited

- Indian Oil Corporation Ltd.

- Lange Gas

- NGL Energy Partners LP

- Petronas Dagangan Berhad

- Repsol SA

- SHV Energy Private Limited

- Suburban Propane Partners LP

- Total Energies SE

Recent Developments

- In February 2025, BP announced a significant strategic shift, increasing its investment in oil and gas production by approximately 20%, aiming to spend between $13 billion and $15 billion annually through 2027. This move marked a departure from its previous emphasis on renewable energy, reflecting a renewed focus on traditional energy sources to meet global demand.

- In September 2024, Aygaz introduced “Aygaz 100+ Octane,” a new autogas product designed for more efficient combustion and reduced exhaust emissions. This innovation aligns with the company’s commitment to providing cleaner energy solutions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 52.1 Billion |

| Forecast Revenue (2034) | USD 91.6 Billion |

| CAGR (2025-2034) | 5.8% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Propane, Butane, Others), By Product Type (Compressed Natural Gas, Liquefied Petroleum Gas, Liquefied Natural Gas, Others), By Vehicle Type (Passenger Cars, Commercial Vehicles), By Conversion Type (Aftermarket, OEM) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | AmeriGas Partners LP, Aygaz A.S., BP plc, Chevron Corporation, China Petroleum & Chemical Corporation, ConocoPhillips Company, Ferrellgas Partners LP, Flogas Britain Limited, Indian Oil Corporation Ltd., Lange Gas, NGL Energy Partners LP, Petronas Dagangan Berhad, Repsol SA, SHV Energy Private Limited, Suburban Propane Partners LP, Total Energies SE |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |