Global Aliphatic Hydrocarbon Market Size, Share, And Enhanced Productivity By Product (Saturated, Unsaturated), By Application (Paints and Coatings, Adhesives and Sealants, Polymer and Rubber, Surfactant, Dyes, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2026-2035

- Published date: February 2026

- Report ID: 179703

- Number of Pages: 205

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

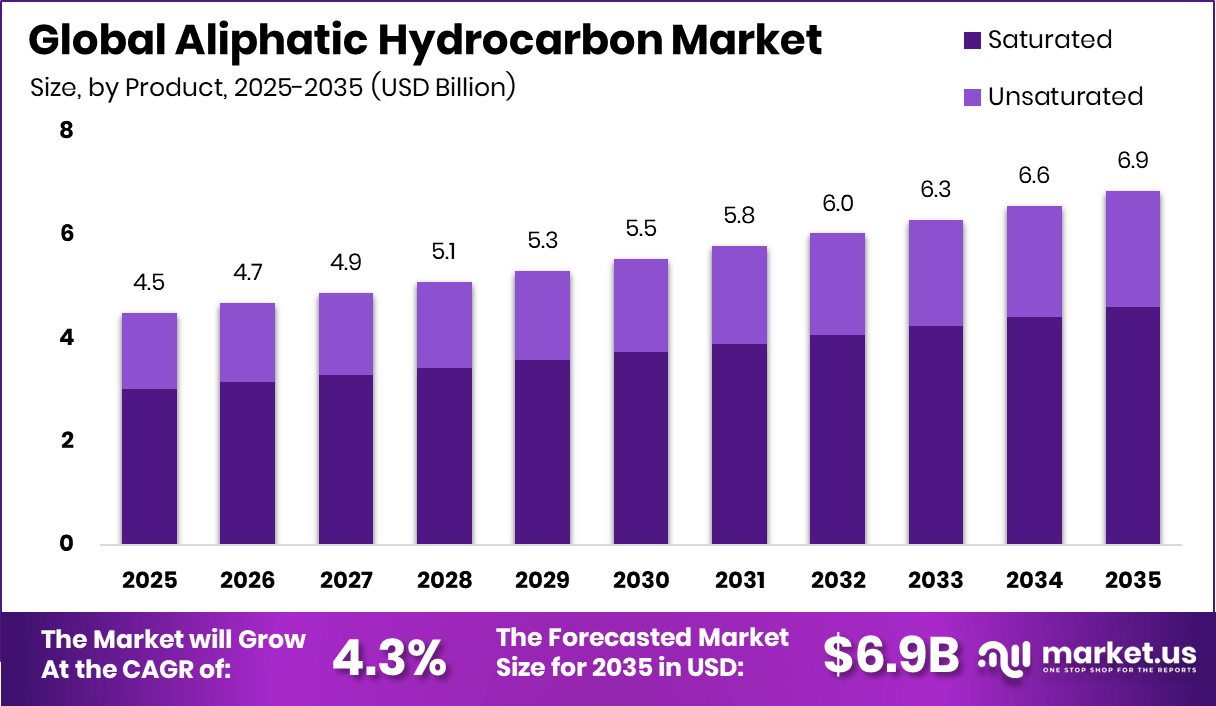

The Global Aliphatic Hydrocarbon Market is expected to be worth around USD 6.9 billion by 2035, up from USD 4.5 billion in 2025, and is projected to grow at a CAGR of 4.3% from 2026 to 2035. Asia Pacific continues driving demand, sustaining its 45.8% share and USD 2.0 Bn value.

The Aliphatic Hydrocarbon Market consists of chemical compounds made from straight-chain, branched, or non-aromatic structures that serve as essential ingredients in coatings, adhesives, rubber processing, surfactants, and dyes. These hydrocarbons are valued for their stability, clean-burning nature, and compatibility with a wide range of industrial formulations. The market is commonly divided by product type into saturated and unsaturated hydrocarbons, and by application into paints and coatings, adhesives and sealants, polymer and rubber, surfactants, dyes, and other industrial uses.

Aliphatic hydrocarbons are organic compounds made primarily from hydrogen and carbon, typically derived from petroleum or natural gas. They are widely used as solvents, diluents, processing aids, and blending components across many manufacturing operations. Their consistent performance and ability to support formulation stability make them indispensable in several industries.

The Aliphatic Hydrocarbon Market represents the commercial ecosystem built around sourcing, refining, processing, and distributing these materials. Demand rises steadily due to their integral role in creating smooth-flowing coatings, flexible sealants, and efficient rubber materials. The market continues evolving as industries seek reliable raw materials for performance-driven products.

Growth factors strengthen the market as manufacturers expand production capacity and invest in new technologies. Recent funding activities—such as Ecoat securing €21 million, Berger Paints raising Tk167 crore for a new factory, and reported deals like a coatings business valued at $6.8 billion—reflect active investment flows that support downstream demand for hydrocarbon-based inputs.

Demand also increases as more industries modernize their operations, requiring stable solvents and processing agents. Strategic movements—including Nippon Paint Holdings’ $2.3 billion deal for AOC and AkzoNobel’s €10.1 billion divestment—signal continued opportunities for market expansion, especially where new facilities and business restructuring stimulate raw material consumption.

Key Takeaways

- The Global Aliphatic Hydrocarbon Market is expected to be worth around USD 6.9 billion by 2035, up from USD 4.5 billion in 2025, and is projected to grow at a CAGR of 4.3% from 2026 to 2035.

- Aliphatic Hydrocarbon Market shows strong dominance of saturated products, capturing 67.3% share across global segments.

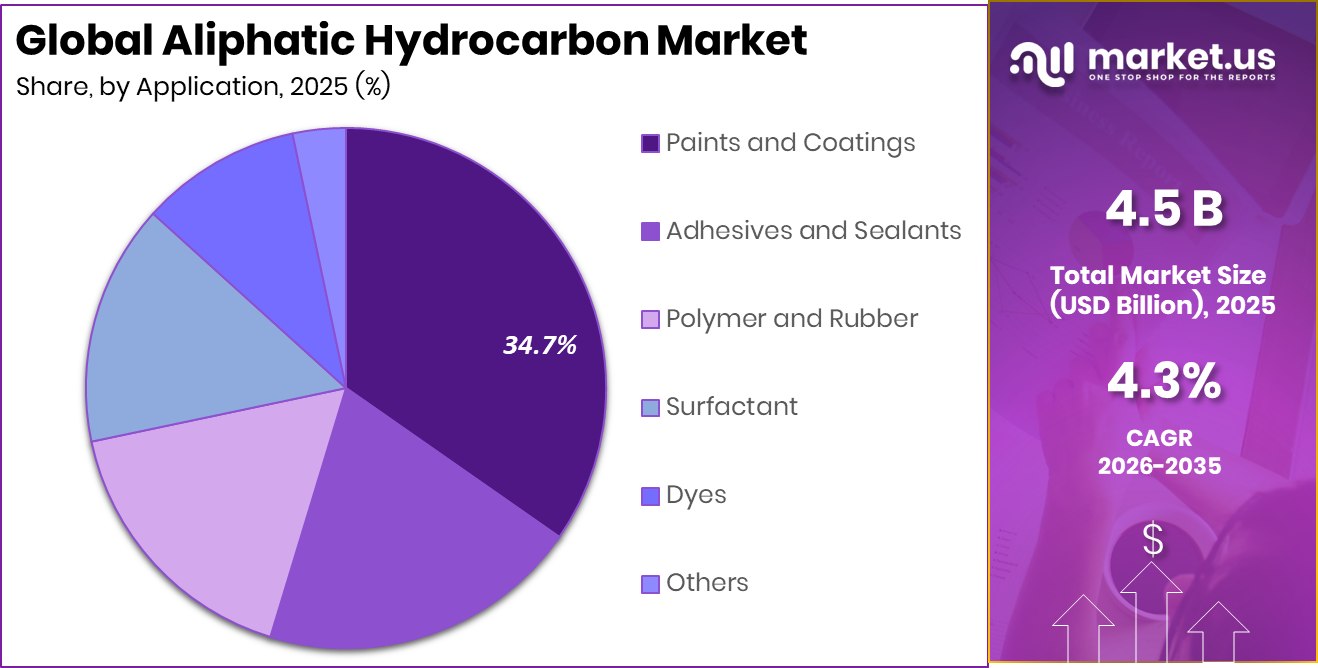

- Aliphatic Hydrocarbon Market growth is supported by rising paint and coatings demand, holding 34.7% application share.

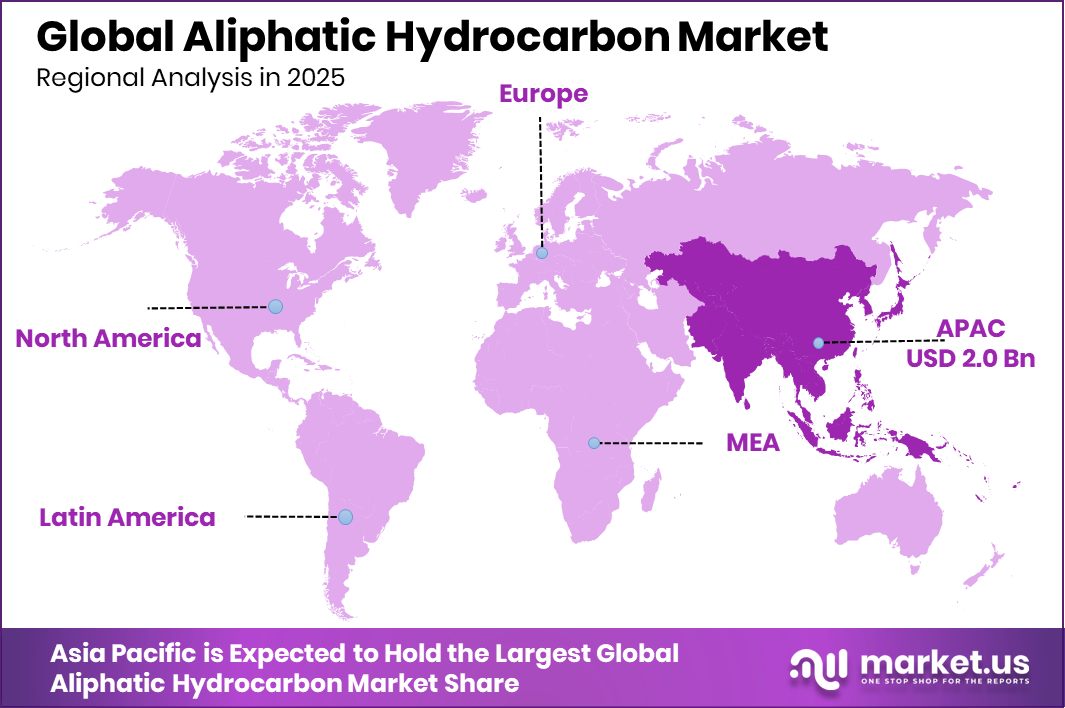

- The Asia Pacific records a strong market value, reaching USD 2.0 Bn in 2025.

By Product Analysis

Aliphatic Hydrocarbon Market reports saturated products at a stable 67.3% for manufacturers.

In 2025, the Aliphatic Hydrocarbon Market continues to show strong momentum across the saturated product segment, which holds a 67.3% share and reflects its broad industrial acceptance. This segment benefits from consistent use in adhesives, paints, rubber processing, and industrial cleaning formulations, where high stability and low reactivity are essential.

Industries prefer saturated hydrocarbons because they offer dependable performance in controlled environments, helping manufacturers maintain uniform product quality. Their compatibility with multiple formulations and ability to support large-scale production make them an integral part of modern chemical supply chains. As demand rises from automotive, construction, and industrial manufacturing, saturated hydrocarbons remain a core component that supports steady long-term market expansion.

By Application Analysis

Aliphatic Hydrocarbon Market shows paints and coatings applications reaching 34.7% across industries.

In 2025, the Aliphatic Hydrocarbon Market maintains a strong presence in the paints and coatings segment, which accounts for 34.7% share, driven by consistent industrial consumption. This application benefits from the material’s ability to enhance flow behavior, drying time, and surface finish across architectural, automotive, and protective coatings. Manufacturers rely on these hydrocarbons to ensure smooth application and stable formulation performance, especially in environments requiring controlled evaporation rates.

Demand remains supported by infrastructure upgrades, refurbishment activities, and the steady rise in protective coating needs across industries. With ongoing advancements in coating technologies, aliphatic hydrocarbons continue to play a vital role in improving product efficiency and supporting reliable large-scale production for coating formulators worldwide.

Key Market Segments

By Product

- Saturated

- Unsaturated

By Application

- Paints and Coatings

- Adhesives and Sealants

- Polymer and Rubber

- Surfactant

- Dyes

- Others

Driving Factors

Rising demand in industrial coating applications

Rising demand in industrial coating applications continues to play a major role in supporting the Aliphatic Hydrocarbon Market, driven by the need for reliable solvent systems that ensure smooth application, stable performance, and consistency across large-scale projects. This requirement is reinforced as industries expand their coating capabilities to improve durability and surface quality in construction, automotive, and manufacturing activities.

Alongside this demand, large sustainability-oriented investments such as Indonesia’s Proyek Hijaunesia Staple Financing for the Gajahmungkur 100 MW Floating Solar PV Project signal broader industrial development, which indirectly boosts the consumption of hydrocarbon-based materials used in coating formulations and supporting processes. Together, these elements help maintain a steady upward push in market demand.

Restraining Factors

Volatile raw material prices are impacting production

Volatile raw material prices impacting production remain a persistent restraint for the Aliphatic Hydrocarbon Market, as fluctuations in crude oil and feedstock availability create challenges for cost management and long-term planning. Manufacturers often face uncertainty regarding procurement, making it difficult to maintain stable pricing for downstream users. This financial pressure becomes more complex as innovation in adjacent industries accelerates.

Notable developments like Albert Invent raising $7.5 million in a seed round to advance material science tools using AI and machine learning highlight how new technologies may shift some demand toward alternative or optimized materials. As pricing instability continues, companies must balance operational efficiency with the need for reliable hydrocarbon sourcing.

Growth Opportunity

Increasing adoption in rubber processing industries

Increasing adoption in rubber processing industries offers strong growth opportunities for the Aliphatic Hydrocarbon Market, as these hydrocarbons play a key role in improving elasticity, processing efficiency, and compound performance. The rubber sector continues to expand across automotive, industrial equipment, and consumer products, creating a consistent requirement for dependable processing aids.

Additional momentum comes from advancements in medical and high-performance materials, highlighted by Tissium securing €50 million to expand its work in surgical adhesives for nerve and hernia repair applications. Although unrelated directly, such funding reflects rising innovation in materials science, indirectly supporting demand for hydrocarbons used in various developmental and production stages. These combined factors create a positive outlook for future market expansion.

Latest Trends

Shift toward cleaner hydrocarbon solvent grades

A clear shift toward cleaner hydrocarbon solvent grades has emerged as one of the key trends in the Aliphatic Hydrocarbon Market, driven by the push for lower odor, improved purity, and reduced environmental impact across industrial applications. Manufacturers and end-users increasingly prefer refined aliphatic grades that support better formulation stability and workplace safety. This shift aligns with ongoing innovation in materials and chemical technologies.

For instance, Citrine Informatics raising $16 million in Series C financing demonstrates growing investment in data-driven material development, enhancing how companies design, evaluate, and optimize formulations. These technological advances support the trend toward cleaner, performance-oriented hydrocarbons, shaping future product preferences and influencing long-term production strategies.

Regional Analysis

In 2025, the Asia Pacific holds a 45.8% share in the aliphatic hydrocarbon market.

In 2025, the Aliphatic Hydrocarbon Market shows steady regional expansion across North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America, each driven by distinct industrial needs and consumption patterns. Asia Pacific remains the dominating region, holding 45.8% share and reaching USD 2.0 Bn, supported by strong manufacturing activity and growing demand from coatings, adhesives, and industrial applications.

North America continues to benefit from stable chemical production and well-established end-use industries, contributing to consistent market uptake. Europe reflects steady growth due to its focus on performance materials, along with demand from automotive refinishing and construction-related coatings.

The Middle East & Africa region shows moderate progress, supported by industrial expansion and gradual adoption of chemical formulations. Latin America maintains stable consumption, driven by manufacturing recovery and increased use across paints, cleaning agents, and processing applications.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2025, ExxonMobil Corporation continues to strengthen its position in the global Aliphatic Hydrocarbon Market by leveraging its wide refining capabilities and consistent product quality. The company’s large-scale production infrastructure supports uninterrupted supply across multiple industries, including coatings, adhesives, cleaning agents, and industrial processing. ExxonMobil’s strong distribution network further enhances its ability to meet regional demand shifts, particularly in fast-growing Asian markets. Its integrated operations help maintain efficiency and product consistency, allowing the company to retain a competitive advantage in both high-volume and specialty hydrocarbon grades.

BASF SE demonstrates steady progress in the aliphatic hydrocarbon market through its focus on diversified chemical solutions and robust portfolio management. In 2025, the company’s expertise in formulation chemistry enables it to serve customers requiring dependable, high-purity aliphatic hydrocarbons for coatings, solvents, and industrial processing. BASF’s established manufacturing presence across major regions strengthens its ability to respond to changing consumption trends while ensuring product availability. Its continuous emphasis on performance, reliability, and application-focused offerings positions BASF as a critical supplier within the global value chain.

Shell Global maintains a strong competitive stance in the 2025 Aliphatic Hydrocarbon Market by capitalizing on its extensive refining assets and long-standing expertise in hydrocarbon production. The company’s consistent output supports large-scale industrial users that rely on stable, high-quality aliphatic hydrocarbons. Shell’s broad regional presence, particularly in Asia and Europe, allows it to efficiently serve diverse end-use sectors. With a solid operational base and wide product reach, Shell continues to play an essential role in maintaining supply stability and supporting ongoing demand across global industries.

Top Key Players in the Market

- ExxonMobil Corporation

- BASF SE

- Shell Global

- LyondellBasell Industries N.V.

- Total S.A.

- Reliance Industries Limited

- Chevron Phillips Chemical

- Mitsubishi Chemical Corporation

- Sasol

- Ineos Group Limited

- Dow

Recent Developments

- In May 2024, ExxonMobil completed its acquisition of Pioneer Natural Resources, a significant U.S. shale producer, strengthening its presence in the Permian Basin and boosting its crude oil and liquids production capabilities. This large transaction expanded ExxonMobil’s upstream footprint and access to raw hydrocarbons used across refining and chemical operations.

- In May 2024, BASF announced it would increase the production capacity of its Basoflux® paraffin inhibitors at its Tarragona, Spain site, to meet growing demand in the Oil & Gas industry. This investment supports more efficient paraffin control solutions and is expected to start delivering products in early 2025, helping customers improve flow and processing in hydrocarbon-related operations.

Report Scope

Report Features Description Market Value (2025) USD 4.5 Billion Forecast Revenue (2035) USD 6.9 Billion CAGR (2026-2035) 4.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Saturated, Unsaturated), By Application (Paints and Coatings, Adhesives and Sealants, Polymer and Rubber, Surfactant, Dyes, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape ExxonMobil Corporation, BASF SE, Shell Global, LyondellBasell Industries N.V., Total S.A., Reliance Industries Limited, Chevron Phillips Chemical, Mitsubishi Chemical Corporation, Sasol, Ineos Group Limited, Dow Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Aliphatic Hydrocarbon MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample

Aliphatic Hydrocarbon MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- ExxonMobil Corporation

- BASF SE

- Shell Global

- LyondellBasell Industries N.V.

- Total S.A.

- Reliance Industries Limited

- Chevron Phillips Chemical

- Mitsubishi Chemical Corporation

- Sasol

- Ineos Group Limited

- Dow

Our Clients

- 179703

- February 2026