Quick Navigation

Report Overview

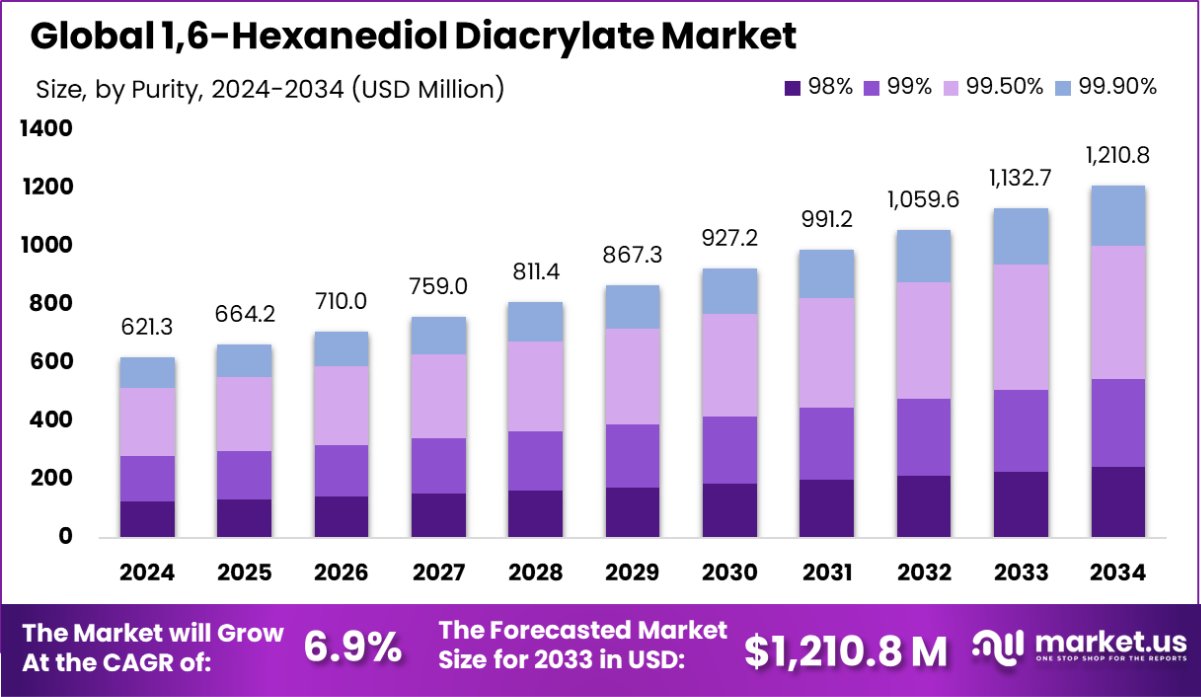

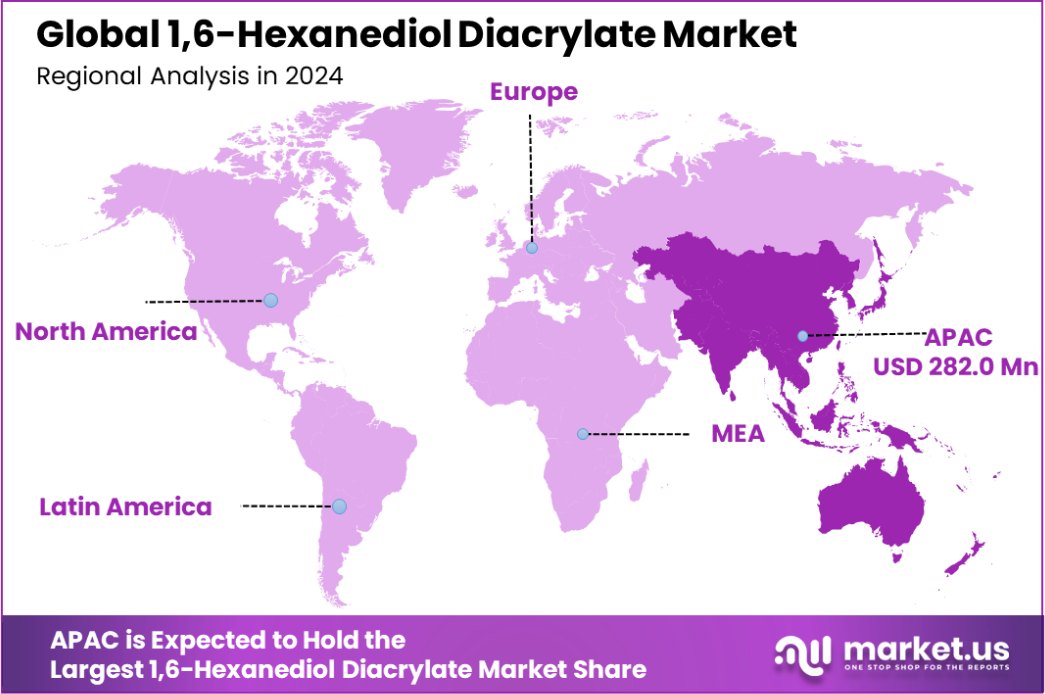

Global 1,6-Hexanediol Diacrylate Market is expected to be worth around USD 1,210.8 Million by 2034, up from USD 621.3 Million in 2024, and grow at a CAGR of 6.9% from 2025 to 2034. In 2024, Asia-Pacific dominated the 1,6-Hexanediol Diacrylate market with 42.3%, reaching USD 282.0 million.

1,6-Hexanediol diacrylate (HDDA) is a difunctional acrylate monomer used primarily in the production of polymers and resins. It features two acrylate groups, which make it highly effective as a cross-linking agent in various polymerization processes. HDDA is known for its excellent adhesive properties and resistance to heat and chemicals, making it a valuable component in coatings, inks, adhesives, and sealants, as well as in the composite and electronics industries.

The 1,6-Hexanediol Diacrylate market is witnessing growth driven by the increasing demand for high-performance materials across various sectors, including automotive, industrial coatings, and electronics. The expansion of the UV-cured resins market also significantly contributes to the growth of the HDDA market due to its effectiveness in UV-curing applications, which offer environmental benefits like reduced solvent emissions.

The market’s growth is fueled by the rising adoption of UV curing technology, particularly in the coatings and ink sectors. The ability of HDDA to enhance the properties of UV-curable resins, such as durability and chemical resistance, aligns with industry trends favoring sustainable and efficient manufacturing processes. Additionally, technological advancements in acrylic resins and polymers are opening new applications for HDDA, further propelling market expansion.

Demand for 1,6-Hexanediol Diacrylate is driven by its extensive use in high-performance adhesives and sealants, particularly in the automotive and construction industries. As these sectors continue to seek more durable and robust materials capable of withstanding harsh environments, the demand for HDDA is expected to rise.

Emerging opportunities in the 1,6-Hexanediol Diacrylate market lie in the expanding electronics sector, where HDDA-based polymers are used in the manufacture of flexible displays and circuit boards. Additionally, the ongoing development of bio-based acrylates presents an opportunity for market expansion, appealing to the growing consumer and regulatory demand for sustainable and environmentally friendly products.

Key Takeaways

- Global 1,6-Hexanediol Diacrylate Market is expected to be worth around USD 1,210.8 Million by 2034, up from USD 621.3 Million in 2024, and grow at a CAGR of 6.9% from 2025 to 2034.

- By Purity: 99.5% purity level holds a market share of 37.4%.

- By Viscosity: Medium viscosity (10-100 cPs) captures 38.4% of the market.

- By Grade: Monomer grade dominates with a 46.4% market share.

- By Application: Coatings and adhesives lead, comprising 52.1% of applications.

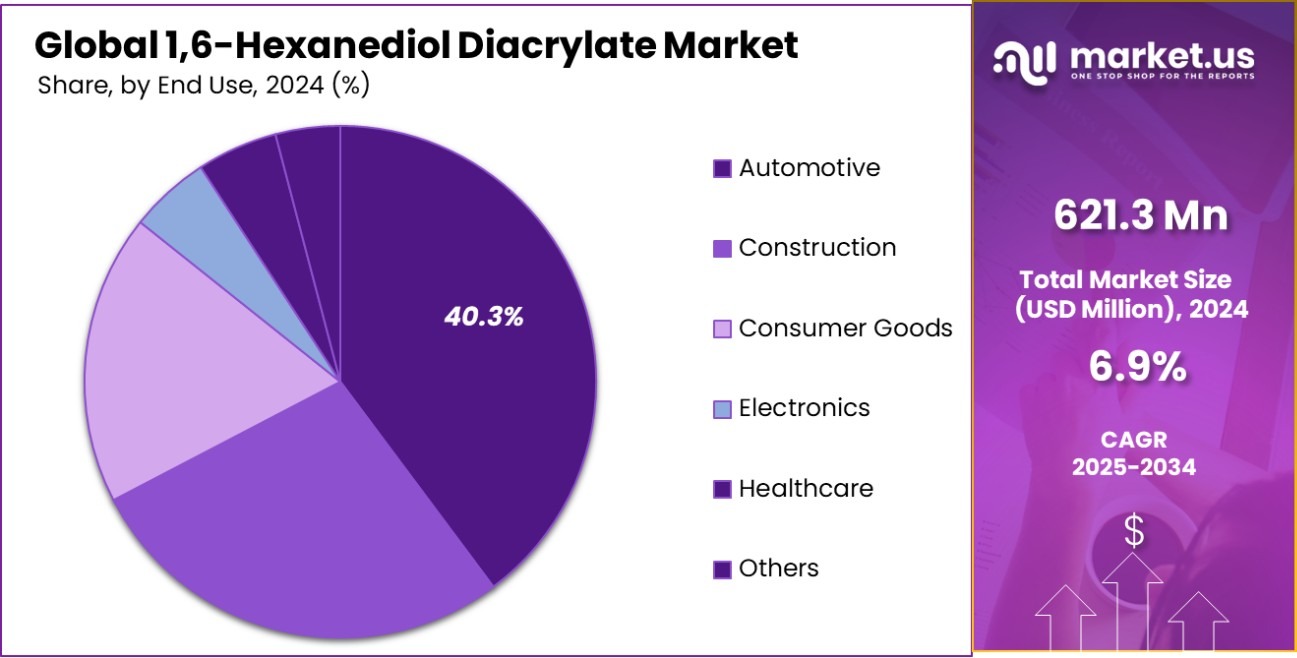

- By End-Use: The automotive sector utilizes 40.3% of the market’s supply.

- Asia-Pacific dominated with a 42.3% share, USD 282.0 Mn.

By Purity Analysis

1,6-Hexanediol Diacrylate with 99.5% purity constitutes 37.4% of the market, highlighting quality demand.

In 2024, 99.5% Purity held a dominant market position in the By Purity segment of the 1,6-Hexanediol Diacrylate Market, capturing a 37.4% share. The demand for 99.5% purity grade is driven by its broad applicability in high-performance coatings, adhesives, and UV-curable formulations, where consistent chemical composition is crucial for product efficiency. Its widespread use in the electronics and automotive industries further solidifies its market leadership.

Following closely, 99.9% of Purity accounted for a significant portion of the market. The preference for 99.9% purity stems from its superior stability and lower impurity levels, making it ideal for advanced polymer applications and high-end industrial coatings. This segment continues to grow, particularly in precision engineering and medical device coatings, where ultra-high purity is a prerequisite.

Meanwhile, 99% Purity and 98% Purity segments collectively contributed to the market landscape, catering to cost-sensitive applications, such as standard adhesives and industrial coatings. The 98% Purity variant, being the most economical, finds adoption in large-scale manufacturing where performance thresholds are less stringent.

By Viscosity Analysis

Medium viscosity (10-100 cPs) 1,6-Hexanediol Diacrylate holds a 38.4% market share, favored for balanced flow properties.

In 2024, Medium Viscosity (10-100 cPs) held a dominant market position in the By Viscosity segment of the 1,6-Hexanediol Diacrylate Market, capturing a 38.4% share. This viscosity range is widely preferred for its optimal balance between flowability and performance, making it ideal for applications in coatings, adhesives, and photopolymer formulations.

The increasing demand for UV-curable coatings and 3D printing resins has significantly driven the adoption of medium-viscosity formulations, as they offer superior spreading characteristics without excessive thinning or thickening.

Low Viscosity (0-10 cPs) followed closely, catering to formulations requiring high penetration and rapid curing, particularly in advanced adhesives and inkjet printing applications. The segment benefits from its ability to enhance substrate wetting and adhesion, particularly in precision coatings and electronics.

Meanwhile, High Viscosity (100-1000 cPs) and Very High Viscosity (1000 cPs and above) segments collectively contributed to niche applications, where enhanced film thickness and mechanical performance are critical. These viscosity grades find usage in structural adhesives and specialized coatings that require high durability and resistance.

By Grade Analysis

The monomer grade of 1,6-Hexanediol Diacrylate dominates, capturing 46.4% of the market due to versatility.

In 2024, Monomer held a dominant market position in the By Grade segment of the 1,6-Hexanediol Diacrylate Market, capturing a 46.4% share. The widespread adoption of monomer-grade 1,6-Hexanediol Diacrylate is primarily driven by its essential role as a reactive diluent in UV-curable coatings, adhesives, and 3D printing formulations.

Its excellent crosslinking ability and rapid polymerization characteristics make it a preferred choice in applications requiring enhanced mechanical strength, durability, and resistance to environmental degradation. The increasing demand for high-performance coatings in the electronics, automotive, and construction industries has further strengthened its market presence.

Following monomer, the Acrylates segment accounted for a substantial share, benefiting from its use in high-end polymer applications and specialty coatings. Acrylates provide excellent adhesion, flexibility, and chemical resistance, making them ideal for protective coatings and advanced industrial formulations.

The Di-functional grade, while having a smaller market share, caters to specialized applications requiring improved elasticity and impact resistance. Its role in engineered polymers and high-performance resins remains crucial for industries that prioritize mechanical reinforcement.

By Application Analysis

Coatings and adhesives are the largest application segment at 52.1%, driving substantial market growth.

In 2024, Coatings and Adhesives held a dominant market position in the By Application segment of the 1,6-Hexanediol Diacrylate Market, capturing a 52.1% share. This segment’s growth is primarily driven by the increasing demand for UV-curable coatings and high-performance adhesives across industries such as automotive, construction, and industrial manufacturing.

The superior crosslinking properties of 1,6-Hexanediol Diacrylate enhance adhesion strength, durability, and chemical resistance, making it an essential component in advanced coatings and adhesive formulations. Rising regulations promoting low-VOC (volatile organic compound) formulations have further accelerated its adoption in environmentally friendly coatings.

The Electronics segment followed closely, leveraging the compound’s excellent electrical insulation properties and resistance to moisture and thermal degradation. Its role in printed circuit boards, conformal coatings, and encapsulation materials is growing with advancements in miniaturization and high-performance electronics.

In the Medical Devices segment, 1,6-Hexanediol Diacrylate is gaining traction due to its biocompatibility and UV-curing applications in medical adhesives and coatings, particularly in implantable devices and diagnostic tools.

Meanwhile, the Packaging segment continues to expand, particularly in UV-curable inks and coatings that provide superior scratch resistance and adhesion on flexible and rigid packaging materials.

By End-Use Analysis

The automotive sector is a major end-user, accounting for 40.3% of the market, reflecting robust demand.

In 2024, Automotive held a dominant market position in the By End-Use segment of the 1,6-Hexanediol Diacrylate Market, capturing a 40.3% share. The increasing demand for UV-curable coatings, adhesives, and sealants in automotive manufacturing has been a major driver for this segment.

The compound’s excellent mechanical strength, chemical resistance, and durability make it a preferred material in protective coatings, structural adhesives, and automotive refinishing applications. Additionally, the push for lightweight and fuel-efficient vehicles has led to greater adoption of high-performance coatings that improve wear resistance and longevity.

The Construction segment followed, benefiting from the increasing use of weather-resistant coatings, industrial adhesives, and sealants. 1,6-Hexanediol Diacrylate is widely used in protective coatings for building exteriors, wood coatings, and high-strength adhesives for structural applications.

In Consumer Goods, the compound is gaining traction in high-performance coatings and adhesives used for furniture, appliances, and sporting goods, ensuring superior finish quality and durability.

Meanwhile, the Electronics and Healthcare segments continue to expand, with applications in printed circuit boards, medical adhesives, and biocompatible coatings. The increasing adoption of UV-curable formulations in medical device manufacturing further supports market growth.

Key Market Segments

By Purity

- 98%

- 99%

- 99.5%

- 99.9%

By Viscosity

- Low Viscosity (0-10 cps)

- Medium Viscosity (10-100 cPs)

- High Viscosity (100-1000 cPs)

- Very High Viscosity (1000 cps and above)

By Grade

- Monomer

- Acrylates

- Di functional

- Others

By Application

- Coatings and Adhesives

- Electronics

- Medical Devices

- Packaging

- Others

By End-Use

- Automotive

- Construction

- Consumer Goods

- Electronics

- Healthcare

- Others

Driving Factors

Growing Demand for UV-curable coatings and Adhesives

One of the biggest drivers of the 1,6-Hexanediol Diacrylate (HDDA) market is the rising demand for UV-curable coatings and adhesives. Industries like automotive, electronics, and packaging are shifting towards UV-cured materials because they offer fast drying, high durability, and lower environmental impact.

These coatings provide better scratch resistance, chemical stability, and adhesion strength, making them ideal for high-performance applications. Additionally, strict environmental regulations promoting low-VOC solutions are pushing manufacturers to adopt HDDA-based formulations, boosting market growth significantly.

Restraining Factors

Health and Environmental Concerns Limit Market Growth

A key challenge for the 1,6-Hexanediol Diacrylate (HDDA) market is the health and environmental risks associated with its use. HDDA is classified as a skin and respiratory irritant, leading to strict safety regulations in workplaces.

Additionally, concerns over its potential toxicity and long-term exposure effects have resulted in stringent environmental laws that limit its widespread adoption. Companies must invest in protective measures and compliance standards, which increase production costs and slow market growth, especially in regions with strict chemical safety regulations like Europe and North America.

Growth Opportunity

Expansion of UV-Curable Technology in 3D Printing

A major growth opportunity in the 1,6-Hexanediol Diacrylate (HDDA) market lies in the rapid expansion of UV-curable technology in 3D printing. As industries like automotive, healthcare, and electronics increasingly adopt additive manufacturing, the demand for high-performance resins is rising.

HDDA’s fast curing, high strength, and excellent adhesion make it a preferred component in 3D printing formulations. The shift towards customized manufacturing, rapid prototyping, and sustainable production methods further strengthens HDDA’s role in next-generation 3D printing applications, driving market expansion.

Latest Trends

Rising Adoption of Bio-Based UV-Curable Materials

A key trend in the 1,6-Hexanediol Diacrylate (HDDA) market is the growing shift toward bio-based UV-curable materials. With increasing regulations on petroleum-derived chemicals and a focus on sustainable manufacturing, companies are developing eco-friendly alternatives for HDDA in coatings, adhesives, and 3D printing applications.

Bio-based HDDA offers lower toxicity, reduced carbon footprint, and better biodegradability while maintaining high-performance properties. As industries seek greener solutions without compromising efficiency, the adoption of sustainable UV-curable materials is expected to grow, reshaping the HDDA market.

Regional Analysis

In 2024, Asia-Pacific dominated the 1,6-Hexanediol Diacrylate Market, holding a 42.3% share, valued at USD 282.0 Mn.

In 2024, Asia-Pacific dominated the 1,6-Hexanediol Diacrylate Market, accounting for a 42.3% share, valued at USD 282.0 million. The region’s strong position is driven by rapid industrialization, expanding electronics manufacturing, and increasing demand for UV-curable coatings and adhesives in countries like China, Japan, and South Korea. The growing adoption of advanced materials in the automotive, packaging, and construction industries has further fueled regional demand.

North America holds a significant market share, supported by technological advancements in 3D printing and medical devices, along with strict environmental regulations driving demand for low-VOC coatings. The United States remains a key contributor due to rising investment in high-performance polymer applications.

Europe follows closely, benefiting from strict sustainability regulations and increasing adoption of bio-based UV-curable materials. Countries like Germany, France, and the UK are focusing on eco-friendly coatings and high-performance adhesives, driving regional growth.

The Middle East & Africa and Latin America markets are expanding steadily, fueled by growing construction activity, automotive advancements, and increasing investments in industrial coatings. While these regions currently have a smaller market share, their rising manufacturing capabilities and infrastructure projects present significant growth opportunities in the long term.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, the 1,6-Hexanediol Diacrylate (HDDA) market remains competitive, with Asia-Pacific-based companies leading the global supply. Zhejiang Satellite Petrochemical, Wuxi Zhongheng Chemical, and Jiangsu Rihua Fine Chemical continue to strengthen their positions through cost-effective production, strong distribution networks, and an expanding customer base across high-growth industries like coatings, adhesives, and electronics. These companies benefit from Asia’s growing manufacturing sector and increasing demand for UV-curable materials.

Showa Denko, Yinyong Chemicals, and DIC Corporation are leveraging their R&D expertise to develop high-performance and bio-based HDDA formulations, that align with global sustainability trends. Shandong Huangtai Jinyue Chemical and Sumitomo Chemical are investing in capacity expansion and vertical integration, ensuring steady raw material supply to meet the rising demand in the automotive, packaging, and construction sectors.

Mitsubishi Chemical, Nagase Specialty Materials, Kuraray Co., Ltd., and Nisshin Chemical maintain a strong market presence due to their technological leadership and commitment to high-purity, specialized HDDA grades. Their innovations in low-VOC and environmentally friendly solutions position them well in Europe and North America, where strict environmental regulations drive market trends.

Meanwhile, Shenyang Zhongyi Chemical, Haihang Chemistry, and Shanghai-based manufacturers are expanding their global reach by targeting emerging markets in the Middle East, Africa, and Latin America.

Top Key Players in the Market

- Zhejiang Satellite Petrochemical

- Wuxi Zhongheng Chemical

- Jiangsu Rihua Fine Chemical

- Showa Denko

- Yinyong Chemicals

- DIC Corporation

- Shandong Huangtai Jinyue Chemical

- Sumitomo Chemical

- Shanghai

- Haihang Chemistry

- Mitsubishi Chemical

- Nagase Specialty Materials

- Kuraray Co., Ltd.

- Nisshin Chemical

- Shenyang Zhongyi Chemical

Recent Developments

- In January 2025, Announced a joint venture with a European chemical company to produce 1,6-Hexanediol Diacrylate and related products for the automotive coatings industry.

- In May 2024, Introduced an eco-friendly, bio-based 1,6-Hexanediol Diacrylate derived from renewable resources, targeting environmentally conscious customers in the coatings and adhesives industries.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 621.3 Million |

| Forecast Revenue (2034) | USD 1,210.8 Million |

| CAGR (2025-2034) | 6.9% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Purity (98%, 99%, 99.5%, 99.9%), By Viscosity (Low Viscosity (0-10 cps), Medium Viscosity (10-100 cPs), High Viscosity (100-1000 cPs), Very High Viscosity (1000 cps and above)), By Grade (Monomer, Acrylates, Di functional, Others), By Application (Coatings and Adhesives, Electronics, Medical Devices, Packaging, Others), By End-Use (Automotive, Construction, Consumer Goods, Electronics, Healthcare, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Zhejiang Satellite Petrochemical, Wuxi Zhongheng Chemical, Jiangsu Rihua Fine Chemical, Showa Denko, Yinyong Chemicals, DIC Corporation, Shandong Huangtai Jinyue Chemical, Sumitomo Chemical, Shanghai, Haihang Chemistry, Mitsubishi Chemical, Nagase Specialty Materials, Kuraray Co., Ltd., Nisshin Chemical, Shenyang Zhongyi Chemical |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |