Global Fruit and Vegetable Pulp Market Size, Share Analysis Report By Source (Fruit Pulp, Mango, Beet, Tomato, Others, Vegetable Pulp), By Application (Food, Animal Fee, Health And Wellness, Others), By Distribution Channel (Online, Hypermarkets/Supermarkets, Specialty Stores, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 181511

- Number of Pages: 379

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

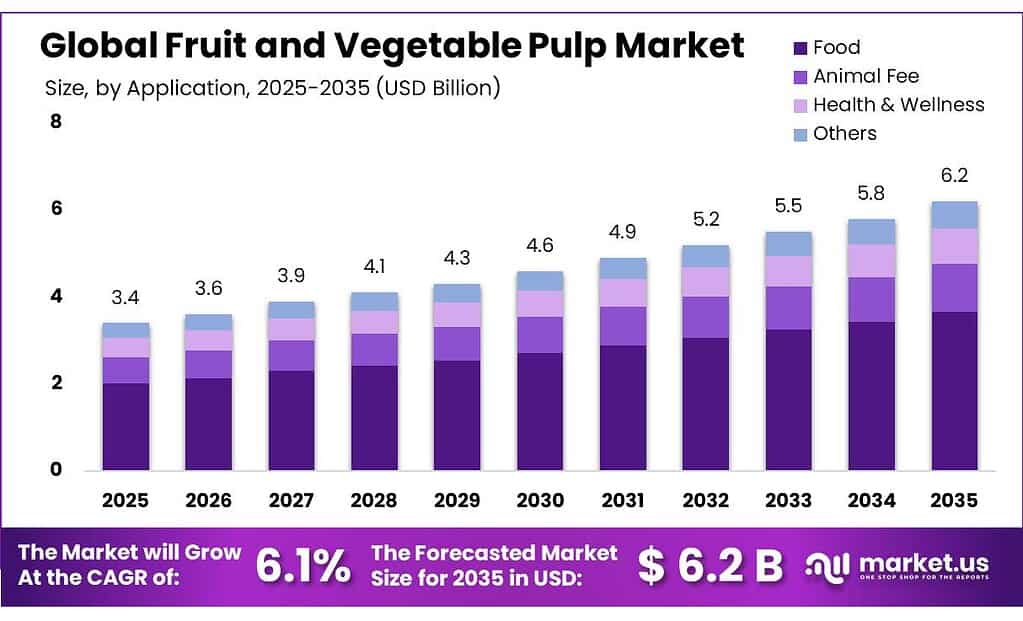

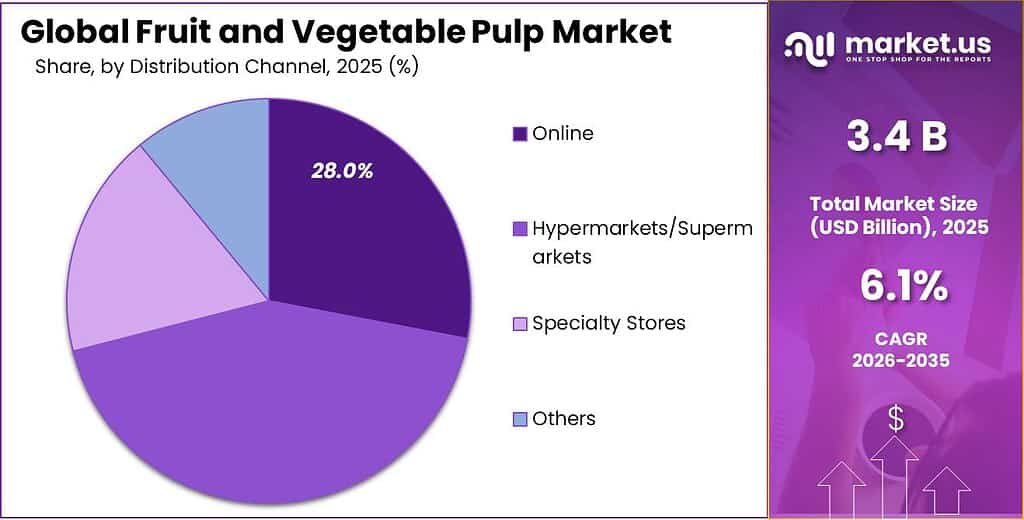

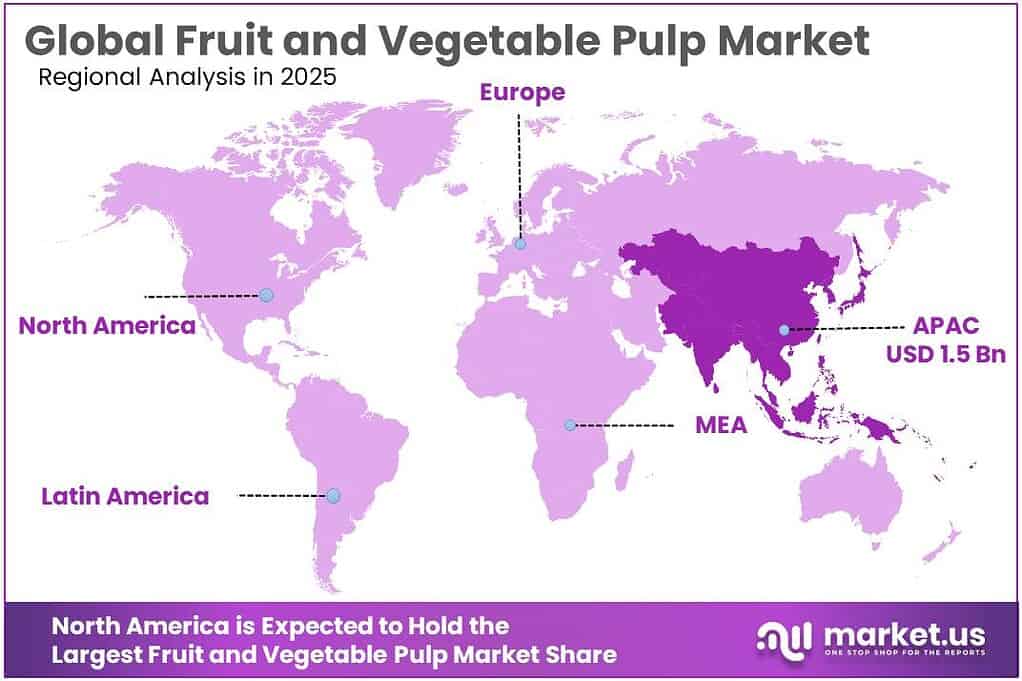

The Global Fruit and Vegetable Pulp Market size is expected to be worth around USD 6.2 Billion by 2035, from USD 3.4 Billion in 2025, growing at a CAGR of 6.1% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 45.8% share, holding USD 1.5 billion revenue.

The fruit and vegetable pulp industry sits at the intersection of agricultural processing, beverage formulation, bakery and dairy applications, and convenience foods. In industrial terms, pulp functions as a shelf-stable or aseptic intermediate that helps manufacturers standardize taste, color, viscosity, and fruit/vegetable solids across juices, nectars, smoothies, yogurts, baby food, desserts, sauces, soups, and ready meals.

Keventer illustrates export-oriented pulp specialization: it serves buyers in 15+ countries and supplies products such as tomato paste in aseptic packs of 228 kg, banana puree in 220 kg aseptic bags, and tomato paste at 28–30° brix, highlighting the industry’s shift toward standardized industrial ingredients.

Demand-side drivers are equally compelling. WHO recommends consumption of at least 400 grams of fruits and vegetables per day for adults and children above age 10, while FDA highlights that about 75% of people have dietary patterns low in vegetables, fruits, and dairy. That gap between recommended and actual intake supports long-term demand for convenient fruit- and vegetable-based formats that can be incorporated into drinks, snacks, breakfast products, and prepared foods.

On the policy side, the European Commission’s EU school scheme allocates €220.8 million per school year, including up to €130.6 million specifically for fruit and vegetables, while the FDA’s updated “healthy” claim framework, announced in late 2024 and active in 2025 implementation, is pushing manufacturers toward more nutrition-aligned formulations.

In September 2025, PepsiCo India used World Food India 2025 to highlight food-system investments tied to agriculture, water stewardship and inclusive growth, while PepsiCo globally notes that it sources approximately 50 agricultural crops and ingredients from more than 60 countries. Collectively, these developments indicate that the fruit and vegetable pulp industry is moving toward higher-value, traceable and nutrition-forward applications rather than commodity-only trading, which improves the medium-term outlook for efficient processors with sourcing depth, quality assurance and export capability.

Key Takeaways

- Fruit and Vegetable Pulp Market size is expected to be worth around USD 6.2 Billion by 2035, from USD 3.4 Billion in 2025, growing at a CAGR of 6.1%.

- Fruit Pulp held a dominant market position, capturing more than a 76.3% share.

- Food held a dominant market position, capturing more than a 59.5% share.

- Hypermarkets/Supermarkets held a dominant market position, capturing more than a 43.7% share.

- Asia Pacific continues to lead the fruit and vegetable pulp market, holding a dominant 45.8% share with a value of around USD 1.5 billion.

By Type Analysis

Fruit Pulp dominates with 76.3% share due to strong demand across beverages and processed foods

In 2025, Fruit Pulp held a dominant market position, capturing more than a 76.3% share. This leadership is largely supported by its wide usage across beverage applications such as juices, smoothies, flavored drinks, and dairy-based products like yogurt and ice cream. Fruit pulp is preferred by manufacturers because it offers natural taste, color, and nutritional value, making it suitable for clean-label and health-focused products. Mango, banana, apple, and guava pulp continue to be the most widely used varieties, especially in tropical and emerging markets where raw material availability is high.

By Nature Analysis

Food application leads with 59.5% share driven by everyday consumption across products

In 2025, Food held a dominant market position, capturing more than a 59.5% share. This strong position comes from the wide use of fruit and vegetable pulp in daily food products such as bakery items, dairy products, baby food, desserts, sauces, and ready-to-eat meals. Food manufacturers prefer pulp because it provides natural flavor, texture, and color without the need for artificial additives. It also helps improve product consistency and shelf life, which is important for large-scale production.

By Distribution Channel Analysis

Hypermarkets/Supermarkets lead with 43.7% share due to easy access and wide product range

In 2025, Hypermarkets/Supermarkets held a dominant market position, capturing more than a 43.7% share. This dominance is mainly because these stores offer a wide variety of fruit and vegetable pulp products under one roof, making it convenient for both individual buyers and small businesses. Consumers prefer these outlets as they can physically check product quality, compare brands, and choose from different packaging sizes.

Key Market Segments

By Source

- Fruit Pulp

- Mango

- Beet

- Tomato

- Others

- Vegetable Pulp

By Application

- Food

- Animal Fee

- Health & Wellness

- Others

By Distribution Channel

- Online

- Hypermarkets/Supermarkets

- Specialty Stores

- Others

Emerging Trends

Shift Toward Aseptic Processing and Longer Shelf-Life Solutions

One of the most noticeable latest trends in the fruit and vegetable pulp market is the growing shift toward aseptic processing. This method allows pulp to be stored for a much longer time without using preservatives or refrigeration, which is becoming very important for food companies managing large supply chains. Aseptic fruit pulp can typically last 12 to 24 months while still maintaining its natural taste and nutrients, making it highly attractive for manufacturers and exporters.

The demand for such solutions is also backed by the overall growth in fruit production. Global fruit production reached around 933 million tonnes in 2022, showing a strong and steady supply of raw materials that can be processed into pulp. Instead of selling all produce fresh, companies are increasingly converting it into pulp using advanced techniques like aseptic processing. This helps reduce waste and allows year-round availability of seasonal fruits.

Rising Demand for Convenient and Ready-to-Use Food Ingredients

On the regulatory side, food safety standards like the FPO mark in India, which is mandatory for processed fruit products, are ensuring that pulp products meet proper quality and hygiene standards. This builds trust among consumers and supports wider adoption. As convenience continues to drive food choices in 2025 and 2026, the use of ready-to-use pulp is expected to grow further, making it one of the key trends shaping the future of the industry.

Drivers

Rising Post-Harvest Losses Driving Demand for Pulp Processing

One of the biggest factors pushing the fruit and vegetable pulp market forward is the high level of wastage in fresh produce. Fruits and vegetables are highly perishable, and a large portion never reaches the final consumer in usable form. According to the Ministry of Food Processing Industries (MoFPI), nearly 4.58% to 15.88% of fruits and vegetables are wasted annually in India due to lack of proper storage, transport, and processing facilities

This is where pulp processing becomes very important. Instead of letting surplus produce go to waste during peak harvest seasons, it can be converted into pulp, puree, or concentrate and stored for longer periods. This not only reduces waste but also helps stabilize prices for farmers and ensures a steady supply for food manufacturers. The need to reduce such large-scale losses has made pulp processing more of a necessity than an option. It also supports food security by making fruits and vegetables available in processed form throughout the year, even when fresh supply is limited.

Government Support and Processing Expansion Strengthening the Industry

Government initiatives have played a strong role in supporting this shift toward processing. In India, schemes like the PM Formalisation of Micro Food Processing Enterprises (PMFME) have been introduced with a total outlay of ₹10,000 crore, aimed at upgrading small food processing units and improving value addition. Alongside this, the Production Linked Incentive Scheme for Food Processing (PLISFPI) has a budget of ₹10,900 crore, and has already helped increase food processing capacity by 35 lakh metric tonnes, while generating around 3.39 lakh jobs.

These initiatives are directly linked to the growth of the pulp industry because they focus on reducing post-harvest losses, improving infrastructure, and encouraging processing at the local level. Programs like Operation Greens, with an allocation of ₹500 crore, also aim to stabilize supply chains and promote processing of key crops like tomato, onion, and potato

Restraints

Weak Cold Chain and Supply Chain Gaps Limiting Industry Growth

One of the biggest restraining factors for the fruit and vegetable pulp industry is the weak supply chain infrastructure, especially cold storage and transportation systems. Fruits and vegetables are highly perishable, and without proper temperature control, they start losing quality very quickly. According to the Food and Agriculture Organization (FAO), nearly one-third of food produced globally is lost or wasted, showing how serious the issue is across the supply chain.

This directly affects the pulp industry because processors depend on fresh and good-quality raw materials. When produce gets damaged during transport or storage, it cannot be used for pulp processing or results in lower-quality output. In many regions, farmers are forced to sell produce quickly at low prices because they lack storage options, reducing the availability of consistent raw material supply for processors. Even though cold chains can help maintain freshness, FAO highlights that proper cold chain systems are still not widely available across developing regions, limiting their impact.

High Economic Losses and Inefficiencies Impacting Processing Viability

Another major challenge is the economic loss caused by inefficiencies in the supply chain. Large quantities of fruits and vegetables are wasted before they even reach processing units, leading to financial losses for farmers, traders, and processors. According to industry and academic estimates, India loses nearly ₹92,651 crore worth of food annually due to inefficient supply chains, and around 16% of fruits and vegetables are wasted because of short shelf life and poor handling practices. In some broader estimates, the total economic loss from food wastage in India ranges between ₹90,000 crore to ₹1 lakh crore every year.

Opportunity

Growing Demand for Natural and Healthy Food Products Creating Strong Opportunities

One of the biggest growth opportunities for the fruit and vegetable pulp industry comes from the rising demand for natural, healthy, and plant-based food products. Consumers today are becoming more aware of what they eat, and there is a clear shift toward products made from real fruits and vegetables rather than artificial ingredients. According to the World Health Organization (WHO), people are recommended to consume at least 400 grams of fruits and vegetables per day to maintain good health.

At the same time, global production of fruits has increased significantly, creating a strong supply base. FAO data shows that global fruit production has grown by 63% between 2000 and 2022, showing how rapidly the availability of raw material has expanded. This increase allows processors to convert more fresh produce into pulp, reducing waste and meeting the growing demand from food industries. As people continue to prefer natural and minimally processed foods, pulp becomes an ideal ingredient because it keeps the original taste and nutrients of fruits and vegetables.

Expanding Food Processing Industry and Government Support Boosting Market Potential

Another major opportunity lies in the expansion of the food processing industry, supported by strong government initiatives. In India, the Ministry of Food Processing Industries has been actively promoting value addition in agriculture. The Production Linked Incentive Scheme for Food Processing (PLISFPI) has an outlay of ₹10,900 crore, aimed at boosting processing capacity and encouraging companies to invest in value-added products.

In addition, the overall fruits and vegetables processing sector is growing steadily. According to government-supported data, the global fruits and vegetables processing market was valued at around USD 63.72 billion in 2023, showing the scale and importance of processed food demand. This growth is creating more demand for pulp as a base ingredient. As processing capacity increases, more companies are looking to secure stable supplies of fruit and vegetable pulp for consistent production.

Regional Insights

Asia Pacific dominates with 45.8% share valued at around USD 1.5 Bn due to strong production base and processing growth

Asia Pacific continues to lead the fruit and vegetable pulp market, holding a dominant 45.8% share with a value of around USD 1.5 billion, driven mainly by its massive agricultural output and strong food processing ecosystem. The region benefits from being the largest producer of fruits and vegetables globally, supported by countries like China and India.

According to FAO, global fruit and vegetable production reached 2.1 billion tonnes in 2023, with a significant portion coming from Asia, which remains the core supply hub for raw materials used in pulp production. Asia alone accounts for about 61% of global vegetable production, highlighting its dominance in the agricultural base needed for pulp manufacturing.

China plays a major role in this regional leadership, producing around 619.1 million tonnes of vegetables in 2023, making it the world’s largest producer. Similarly, India stands as the second-largest producer of fruits and vegetables globally, ensuring continuous availability of tropical fruits like mango, banana, and guava that are widely used in pulp processing.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Keventer Group is a key exporter of fruit pulp, especially mango-based products. The company processes over 25,000 MT+ of mango pulp annually and exports to 15+ countries. It has more than 29 years of experience in the export business and generates over ₹100 crore+ revenue from pulp exports. Its facilities are focused on aseptic processing, allowing extended shelf life of up to 24 months, making it suitable for global food and beverage manufacturers.

PepsiCo is a global leader with revenues exceeding USD 91 billion+ (2024) and operations in more than 200 countries. The company sources large volumes of fruits for juices and beverages under brands like Tropicana. It works with over 100,000+ farmers globally to secure raw materials. In 2025, PepsiCo expanded its sustainability initiatives, focusing on reducing water usage by 15%+ in high-risk areas and improving agricultural productivity.

Döhler GmbH is a global producer of natural ingredients with operations in over 130+ countries. The company employs around 8,000+ people worldwide and offers a wide range of fruit and vegetable-based solutions. It operates more than 50+ production sites globally, focusing on natural flavors, colors, and pulp-based ingredients. Döhler invests heavily in R&D, with multiple innovation centers supporting product development across beverage and nutrition sectors.

Top Key Players Outlook

- Keventer Group

- Conagra Brands Inc.

- Pepsico

- ABC Fruits

- Dohler GmBH

- Agrana Group

- Pursuit

- Iprona AG

- Kiril Mischeff Limited

- Ingredion

- Sunimpex

Recent Industry Developments

As of 2025, Conagra Brands Inc. reported net sales of around USD 11.6–12 billion, supported by a wide portfolio of packaged foods that heavily use processed fruits and vegetables as ingredients.

As of 2025, AGRANA Group plays reported total group revenue of about €3.5 billion, supported by operations across 51 production sites in 24 countries and a workforce of around 9,000 employees.

Report Scope

Report Features Description Market Value (2025) USD 3.4 Bn Forecast Revenue (2035) USD 6.2 Bn CAGR (2026-2035) 6.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Source (Fruit Pulp, Mango, Beet, Tomato, Others, Vegetable Pulp), By Application (Food, Animal Fee, Health And Wellness, Others), By Distribution Channel (Online, Hypermarkets/Supermarkets, Specialty Stores, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Keventer Group, Conagra Brands Inc., Pepsico, ABC Fruits, Dohler GmBH, Agrana Group, Pursuit, Iprona AG, Kiril Mischeff Limited, Ingredion, Sunimpex Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Fruit and Vegetable Pulp MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Fruit and Vegetable Pulp MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Keventer Group

- Conagra Brands Inc.

- Pepsico

- ABC Fruits

- Dohler GmBH

- Agrana Group

- Pursuit

- Iprona AG

- Kiril Mischeff Limited

- Ingredion

- Sunimpex

Our Clients

- 181511

- Mar 2026