Quick Navigation

Report Overview

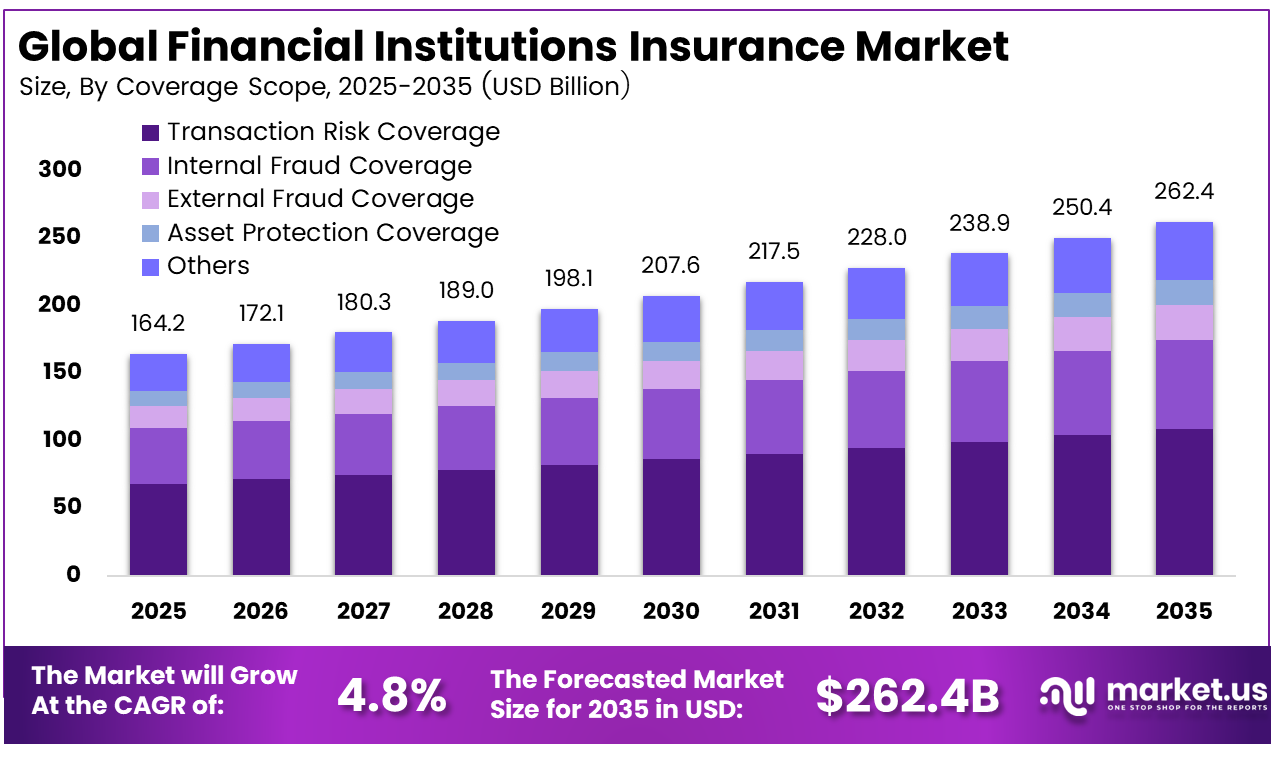

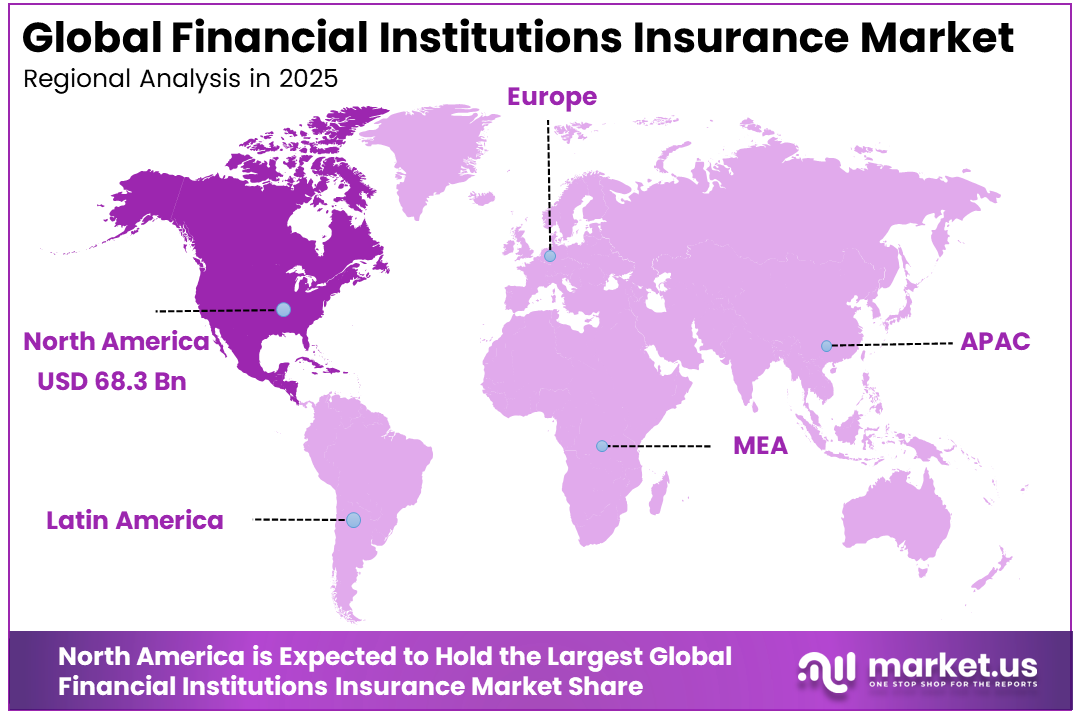

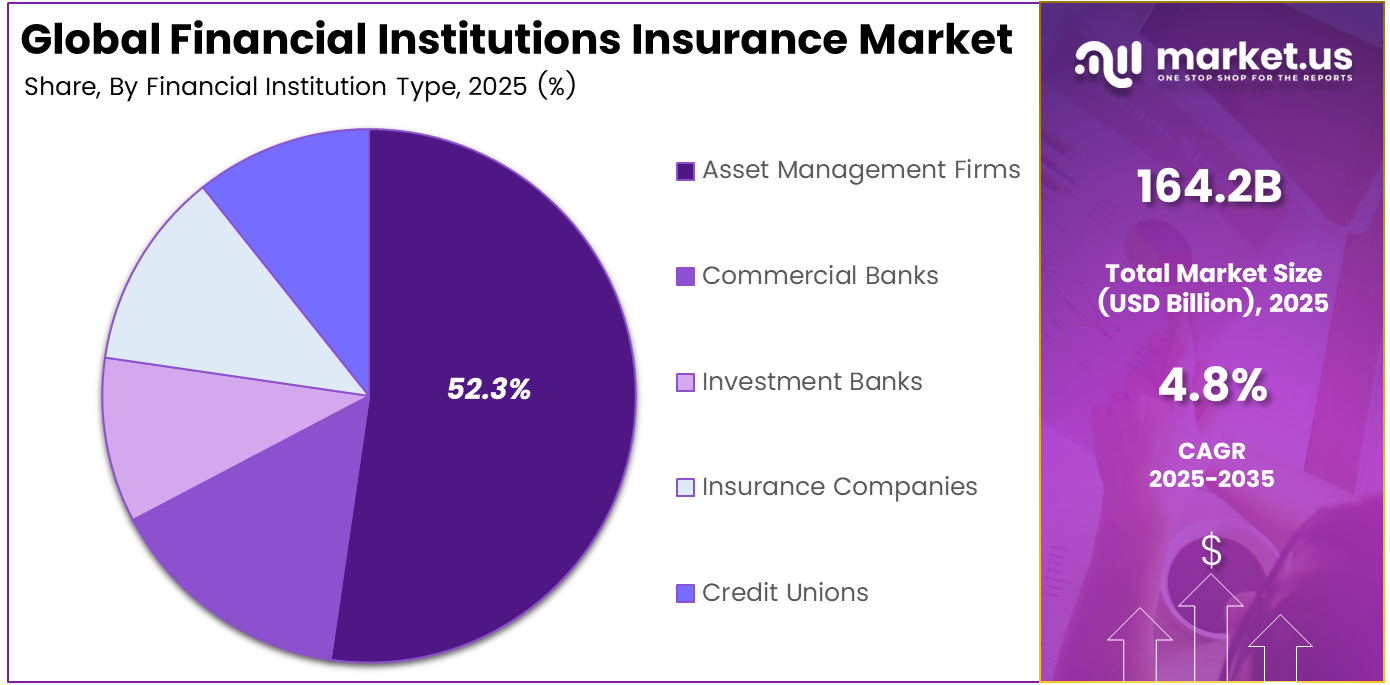

The Global Financial Institutions Insurance Market size is expected to be worth around USD 262.4 billion by 2035, from USD 164.2 billion in 2025, growing at a CAGR of 4.8% during the forecast period from 2026 to 2035. North America held a dominant market position, capturing more than a 41.6% share, holding USD 68.3 billion in revenue.

Financial Institutions Insurance refers to specialized coverage designed to protect banks, asset managers, payment firms, and other financial organizations from losses linked to cyber incidents, fraud, professional errors, regulatory actions, and transaction risks. It supports business continuity, legal defense, client trust, and stronger risk management in complex financial operating environments.

Top driving factors include tighter supervision, frequent regulatory fines, and higher litigation risk. Stronger legal frameworks, along with developed credit and bond markets, support deeper insurance use in the financial sector. Complex products, cross-border operations, and geopolitical shocks are also pushing institutions to shift low-probability but high-severity risks into specialist insurance programs.

The market for Financial Institutions Insurance is driven by rising cyber threats, stricter regulatory oversight, and growing litigation exposure across banks, asset managers, and payment firms. Financial institutions need tailored coverage to protect against fraud, professional errors, transaction risks, and operational disruption. Increasing digital banking activity and complex financial products are also strengthening demand for specialized insurance protection.

Demand is supported by income growth, urbanization, and wider financial inclusion, which expand the customer base and raise transaction volumes that require protection. A higher share of younger and digitally active users is also increasing online payments and mobile banking activity, creating greater exposure to cyber fraud, system outages, and operational losses.

For instance, in March 2026, Allianz continued to grow in financial institutions insurance by expanding structured cyber and crime cover for banks and fintechs. The carrier is bundling risk-engineering insights, incident response, and balance-sheet protection, aiming to differentiate on service quality rather than price alone in a competitive market.

Key Takeaway

- In 2025, the Transaction Risk Coverage segment held a dominant market position, capturing a 41.6% share of the Global Financial Institutions Insurance Market.

- In 2025, the Asset Management Firms segment held a dominant market position, capturing a 52.3% share of the Global Financial Institutions Insurance Market.

- In 2025, the Direct Sales segment held a dominant market position, capturing a 68.1% share of the Global Financial Institutions Insurance Market.

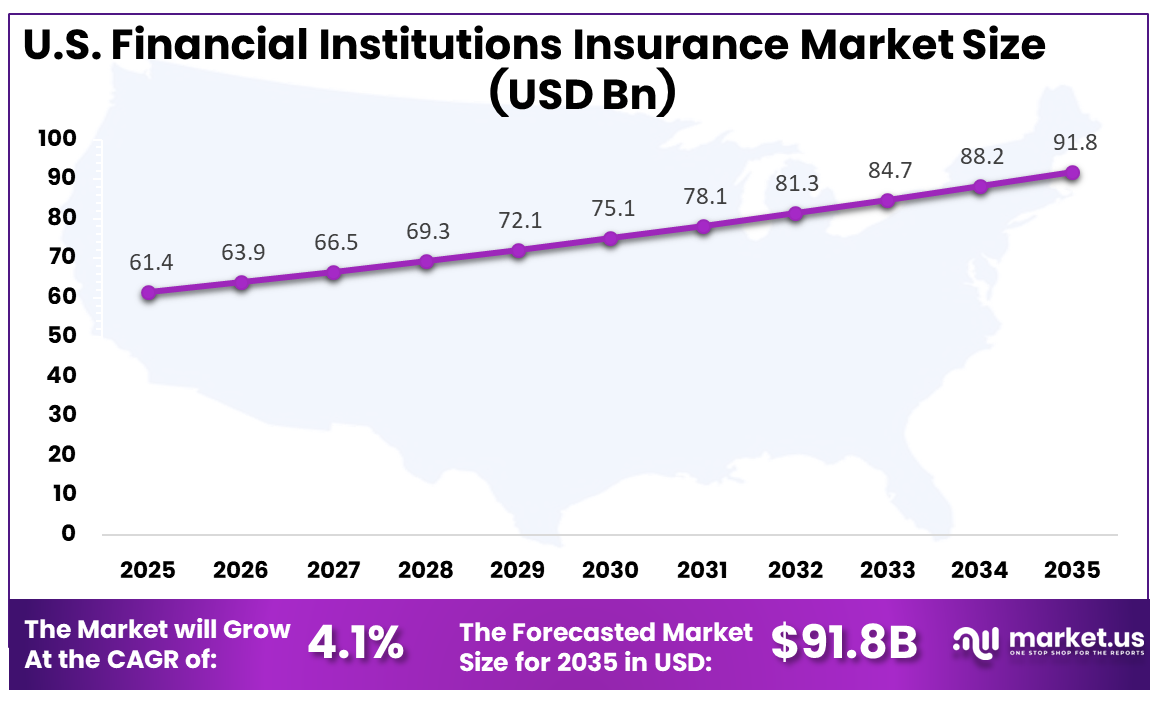

- The U.S. Financial Institutions Insurance Market was valued at USD 61.4 Billion in 2025, with a robust CAGR of 4.1%.

- In 2025, North America held a dominant market position in the Global Financial Institutions Insurance Market, capturing more than a 41.6% share.

Role of Generative AI

Generative AI is changing how financial institutions buy insurance and distribute protection to their clients. Banks and insurers are using AI models to summarize policy wording, handle routine queries, and support underwriting decisions. This helps reduce turnaround time, improve consistency, and support faster insurance servicing across complex financial products.

Some surveys suggest that well over 40% of large financial firms are already experimenting with generative AI in claims triage, document review, and customer service. At the same time, AI is creating new insurable risks, including technology errors, algorithmic bias, and data breaches linked to AI systems.

Investment and Business Benefits

Investment opportunities are growing as insurers create products for fintech platforms, digital banks, and payment companies. These firms face rising cyber and operational risks but often lack long claims histories. Capital can also support covers linked to environmental, social, and governance risks, including green project financing, climate litigation, and changing disclosure duties.

Business benefits extend beyond claim payments, as many policies now include pre-breach and post-breach services such as cyber incident response, forensic support, and legal advisory. These services can reduce downtime and lower total loss severity by noticeable double-digit percentages in some reported cases, while also improving controls and operating resilience.

Regional Analysis

In 2025, North America held a dominant market position in the Global Financial Institutions Insurance Market, capturing more than a 41.6% share, holding USD 68.3 billion in revenue. This dominance is due to North America’s large base of banks, asset managers, insurers, fintech firms, and investment institutions. The region has strict regulatory oversight, high litigation exposure, and strong demand for cyber, professional liability, and transaction risk coverage. Financial institutions also rely on specialized insurance to protect client assets, manage operational disruptions, and support confidence in complex financial activities.

For instance, in February 2026, AXA XL continued to build out its U.S. middle-market franchise with new leadership in the East and expansion in the West, targeting mid-sized corporates that increasingly demand sophisticated property, casualty, and specialty programs. This sustained build-out underscores AXA XL’s ambition to be a primary partner for North American financial institutions’ complex risks.

U.S. Financial Institutions Insurance Market Size

The market for Financial Institutions Insurance within the U.S. is growing tremendously and is currently valued at USD 61.4 billion; the market has a projected CAGR of 4.1%. This dominance is due to the strong presence of banks, asset managers, payment firms, and investment institutions across North America. The region has a mature insurance ecosystem, strict regulatory oversight, and high exposure to cyber, litigation, and transaction-related risks. Financial institutions also prefer specialized coverage to protect client assets, reduce operational losses, and manage reputational risk, which supports steady demand for insurance solutions.

For instance, in June 2025, AIG expanded its cyber and financial lines offerings for banks and asset managers in North America, tightening its focus on resilience against complex digital and fraud risks. The enhanced suite bundles cyber, professional indemnity, and crime cover, reinforcing AIG’s role as a key risk partner to U.S. financial institutions in a volatile threat landscape.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Coverage Scope Analysis

In 2025, the Transaction Risk Coverage segment held a dominant market position, capturing a 41.6% share of the Global Financial Institutions Insurance Market. This dominance is due to the rising need to protect financial institutions from losses linked to complex deals, lending arrangements, and investment transactions. These risks often involve legal, tax, and warranty-related issues, so institutions prefer coverage that can reduce uncertainty and support smoother deal execution.

Transaction risk coverage is also gaining importance as financial institutions operate in stricter regulatory environments. It helps buyers, sellers, and investors manage hidden liabilities that may appear after a transaction is completed. This makes the coverage useful for improving confidence in high-value financial agreements.

For instance, in April 2026, AIG expanded its transactional risk practice, focusing on complex cross-border deals for financial institutions. The move reflects growing demand from banks and asset managers that want dedicated support on warranty, indemnity, and contingent risk covers in volatile markets. AIG is positioning its underwriting teams closer to dealmakers to respond quickly during fast-moving transactions.

Financial Institution Type Analysis

In 2025, the Asset Management Firms segment held a dominant market position, capturing a 52.3% share of the Global Financial Institutions Insurance Market. This dominance is due to the high responsibility that asset management firms carry while handling client funds, investment decisions, and fund operations. These firms face risks from professional errors, cyber incidents, regulatory reviews, and governance failures, which makes insurance a necessary part of their wider risk management structure.

Asset management firms also work in a highly trust-based environment, where reputation and compliance are critical. Insurance helps protect them from claims linked to advice, portfolio management, and fiduciary duties. As investment products become more complex, these firms continue to need broader and more tailored protection.

For instance, in May 2025, Chubb promoted its Asset Management Protector solution as asset managers face more complex operational and regulatory challenges. The modular design allows firms to combine professional liability, directors and officers, and employment practices coverage. This flexibility suits managers running multiple fund types under one platform, with varied risk profiles.

Distribution Channel Analysis

In 2025, the Direct Sales segment held a dominant market position, capturing a 68.1% share of the Global Financial Institutions Insurance Market. This dominance is due to the preference of large financial institutions for direct discussions when buying specialized insurance. Direct sales allow insurers and clients to review risk details closely, adjust policy terms, and build coverage that fits internal controls, regulatory duties, and business exposure more accurately.

Direct sales are also preferred because financial institution insurance often involves sensitive information and complex liability structures. A direct channel supports clearer communication, faster decision-making, and better coordination between insurers, brokers, legal teams, and risk managers. This makes it suitable for customized and high-value insurance programs.

For instance, in June 2025, Willis Towers Watson pointed out that many financial institutions now use a hybrid approach, mixing direct and brokered placements. The broker helps clients decide which lines benefit most from broad market competition. Others are placed directly where relationship and speed are paramount.

Key Market Segments

By Coverage Scope

- Internal Fraud Coverage

- External Fraud Coverage

- Transaction Risk Coverage

- Asset Protection Coverage

- Others

By Financial Institution Type

- Asset Management Firms

- Commercial Banks

- Investment Banks

- Insurance Companies

- Credit Unions

By Distribution Channel

- Insurance Brokers

- Direct Sales

- Reinsurance Companies

Emerging Trends

A key trend is the shift from AI as a support tool to AI as an autonomous decision maker in selected insurance workflows. Insurers are now among the leading sectors globally in AI adoption, close to the technology and telecom industries. Agent-based AI is handling underwriting, claims triage, and billing tasks.

Personalization is also becoming a major trend in financial institutions’ insurance. Around 44% of insurance companies expect generative AI to have the largest positive impact on user experience and personalization. This supports dynamic pricing, targeted protection offers, and context-aware servicing through financial services AI agents.

Growth Factors

Digital financial services and embedded protection are major growth factors for financial institutions’ insurance. As more customers use online and mobile platforms for payments, lending, and investments, insurance attach points are increasing. In India, AI is seen as potentially improving banking operations by up to about 46%, supporting scalable insurance delivery.

Rising risk complexity is also supporting market growth. Climate-linked events, cyber incidents, and fraud are becoming more frequent and severe. Around 78% of insurers are investing in real-time fraud detection, while roughly 49% use enhanced data aggregation to manage risk, making specialist insurance covers more important.

Market Dynamics

Drivers - Regulatory and Cyber Pressure

Financial institutions are facing stricter oversight as regulators focus on cyber resilience, operational continuity, and customer protection. Banks, asset managers, and payment firms must show stronger controls against system failures, fraud, and data loss. This pressure increases the need for insurance that supports financial recovery and business stability.

Cyber threats are also becoming more advanced, creating greater exposure for institutions that handle sensitive financial data and high transaction volumes. Insurance helps firms manage losses linked to breaches, service disruption, and legal claims. It also supports risk planning by encouraging stronger internal controls and incident response readiness.

For instance, in April 2026, AXA XL updated its financial services offering, emphasising broad protection for investment advisers, funds, and other institutions facing changing supervisory standards worldwide. The proposition focuses on management liability and professional risks, including the impact of operational failures and regulatory action, helping clients respond to more intensive oversight across multiple jurisdictions.

Restraint - Complex Policy Terms

Complex policy terms remain a major restraint for financial institutions’ insurance. Coverage often includes cyber risk, professional liability, crime, transaction risk, and directors’ liability. Each area has its own exclusions, limits, and conditions, making it difficult for buyers to understand the full level of protection.

Many institutions also struggle to compare policies across providers because wording can vary widely. Small differences in exclusions or claims conditions can create major coverage gaps during an incident. This makes policy selection time-consuming and often requires support from legal, compliance, and risk teams.

For instance, in January 2024, Travelers launched a new financial institution bond tailored for asset managers, combining crime and dishonesty protections in a single product. While the bond responds to real operational risks, the interplay between bond terms, cyber policies, and management liability cover can be intricate, adding to the documentation that risk managers must interpret.

Opportunities - Digital Transformation

Digital transformation is creating strong opportunities for financial institutions and insurance. Online banking, mobile payments, digital lending, and fintech partnerships are expanding the risk landscape. Insurers can design tailored covers for cyber fraud, technology failures, data misuse, and service interruption linked to digital financial operations.

AI and automation are also creating new insurance needs. Financial institutions increasingly require protection for model errors, algorithmic bias, and digital compliance failures. This gives insurers room to build more flexible products that support modern banking, digital platforms, and technology-led financial services.

For instance, in May 2025, the SafeWeb Pro partnership allows Chubb to deliver cyber risk protection through a digital platform that blends monitoring, training, and liability insurance. Financial institutions and fintechs can use the solution to track threats in real time while maintaining relevant cover, showing how digital tools can enhance engagement and risk transfer efficiency.

Challenges - Third-Party Risk

Third-party risk is a major challenge for financial institutions’ insurance. Banks and financial firms depend heavily on cloud providers, payment processors, software vendors, and data service companies. If one important partner fails, service disruption, data loss, or financial damage can affect many institutions at once.

This dependence makes risk assessment more difficult for insurers. Vendor networks are often complex, and exposure can spread across several systems and locations. Financial institutions must improve due diligence, contract controls, and incident planning to make third-party risks more manageable for insurance coverage.

For instance, in May 2026, the Allianz–Coalition agreement makes Coalition the exclusive partner for Allianz’s commercial cyber segment, so the success of this portfolio depends heavily on a single strategic provider. Financial institutions covered under the program must also understand how responsibilities are divided between insurer and technology partner, which adds another layer of third-party dependency to manage.

Key Players Analysis

One of the leading players in May 2026, AIG expanded its financial institutions insurance portfolio by sharpening cyber, crime, and professional indemnity offerings for banks and asset managers. The insurer is leaning on advanced risk analytics to tighten underwriting discipline while helping clients navigate rising digital fraud and regulatory pressure in capital markets.

Top Key Players in the Market

- AIG

- Chubb

- Zurich Insurance Group

- Allianz

- AXA XL

- Travelers

- Liberty Mutual

- Berkshire Hathaway

- Marsh

- Aon

- Willis Towers Watson

- Munich Re

- Swiss Re

- Beazley

- Sompo International

- Others

Recent Developments

- In April 2026, Chubb strengthened its role in financial lines by scaling specialty coverage for securities claims and operational risk at global banks and investment firms. The company is pairing loss-prevention advisory with broader limits, aiming to capture a larger share of complex financial institutions’ placements worldwide.

- In March 2026, Zurich refined its financial institutions proposition with integrated D&O, E&O, and cyber solutions targeted at lenders and payment players. The focus is on consistent wording across regions and improved claims responsiveness, positioning Zurich as a preferred partner for cross-border financial groups managing interconnected risks.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 164.2 Billion |

| Forecast Revenue (2035) | USD 262.4 Billion |

| CAGR (2026-2035) | 4.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Coverage Scope (Internal Fraud Coverage, External Fraud Coverage, Transaction Risk Coverage, Asset Protection Coverage, Others), By Financial Institution Type (Commercial Banks, Investment Bank, Asset Management Firms, Insurance Companies, Credit Unions), By Distribution Channel (Insurance Brokers, Direct Sales, Reinsurance Companies) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | AIG, Chubb, Zurich Insurance Group, Allianz, AXA XL, Travelers, Liberty Mutual, Berkshire Hathaway, Marsh, Aon, Willis Towers Watson, Munich Re, Swiss Re, Beazley, Sompo International, Others |

| Customization Scope | Customization at the segment and region/country levels will be provided. Moreover, customization can be tailored to the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |