Quick Navigation

Report Overview

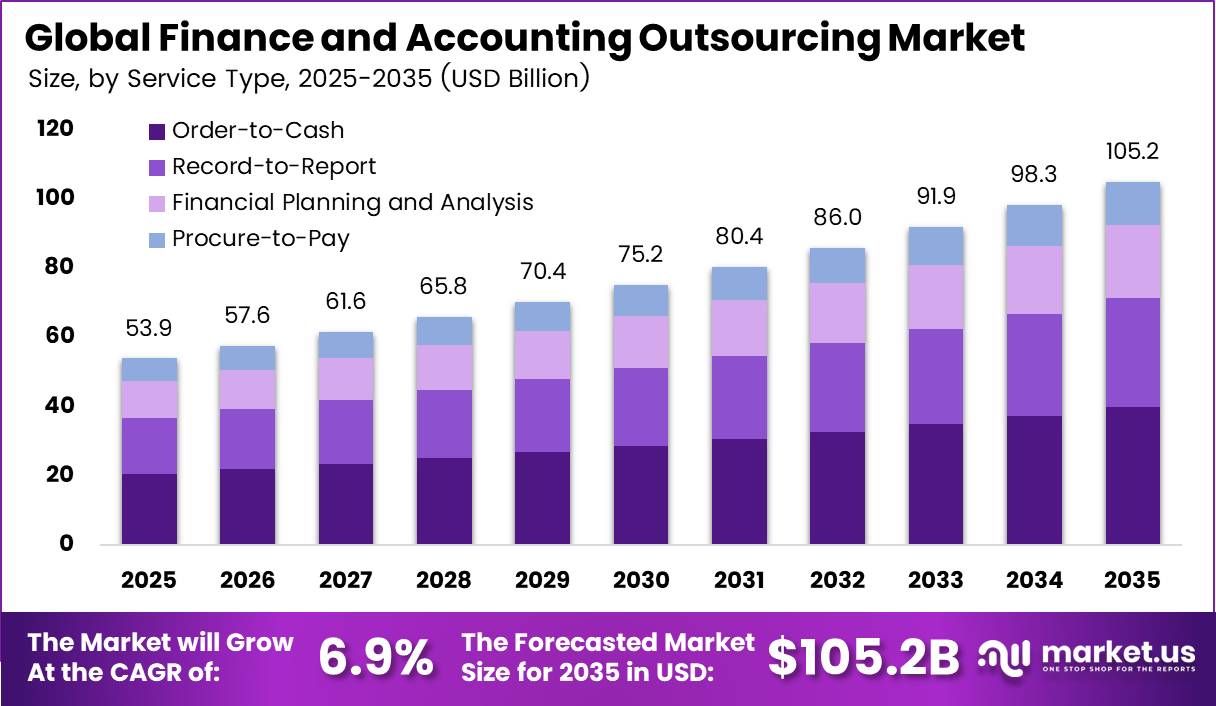

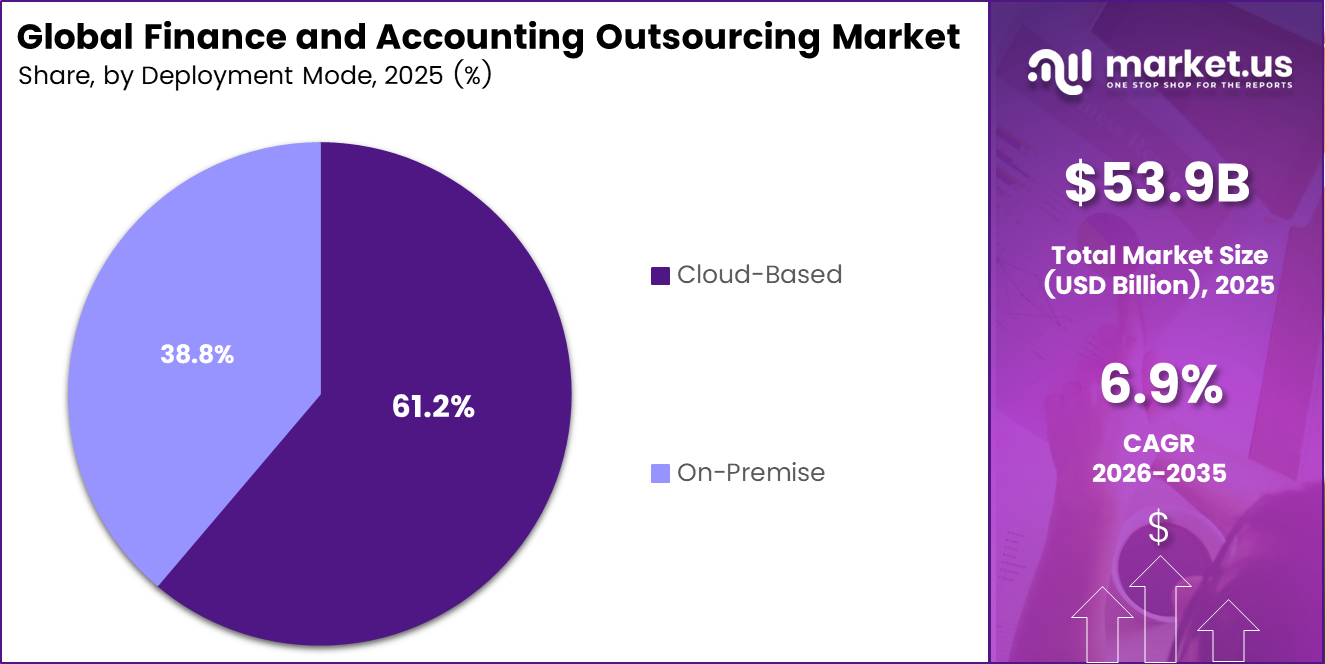

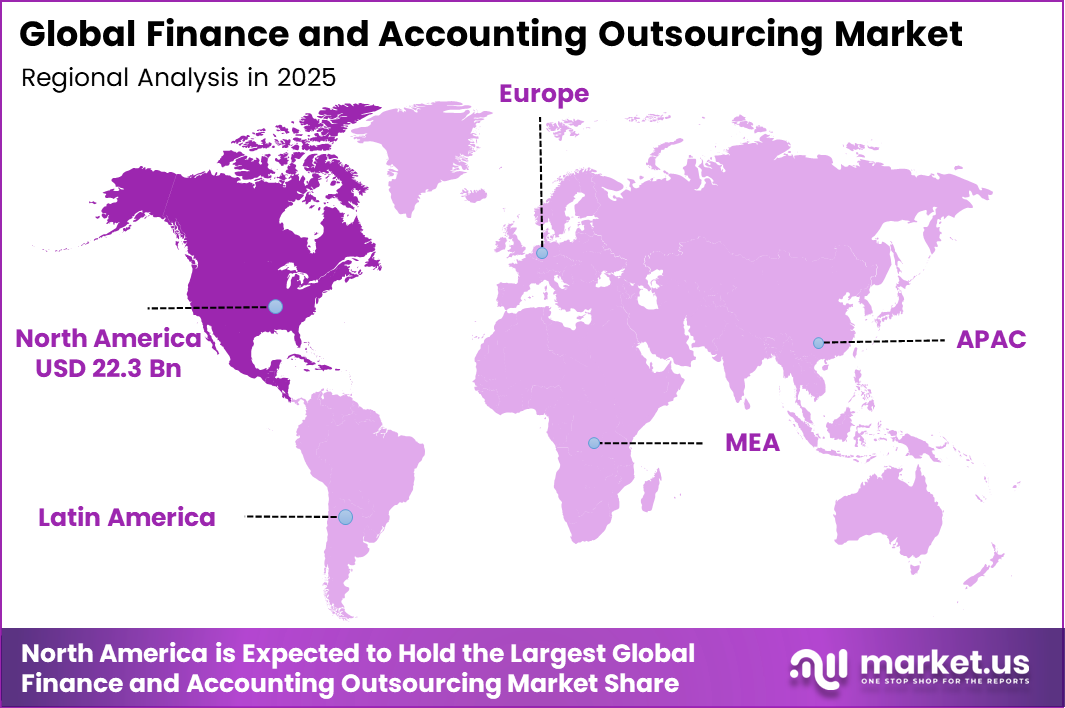

The global Finance and Accounting Outsourcing (FAO) market was valued at USD 53.9 billion in 2025 and is projected to reach USD 105.2 billion by 2035, expanding at a CAGR of 6.9% during the forecast period. This growth links directly to the rising scale of global business services. North America dominates the Finance and Accounting Outsourcing market, holding a 41.3% share and generating USD 22.3 billion in revenue.

The IMF’s World Economic Outlook projected global GDP growth at 3.0% for 2025 and 3.1% for 2026, which drives corporate demand for leaner, technology-enabled finance functions. The U.S. Bureau of Economic Analysis confirmed that U.S. private service-supplying industries contributed over 81% to U.S. GDP, reinforcing the size and maturity of the service economy that feeds FAO demand.

The U.S. Bureau of Labor Statistics projects employment in business and financial occupations to grow faster than the average for all occupations from 2024 to 2034, projecting about 942,500 openings per year, which signals a talent gap that pushes companies to outsource finance functions to specialized providers rather than build them internally.

North America holds a dominant position in the global FAO market. This leadership reflects the region’s deep base of multinational corporations across financial services, technology, healthcare, and retail that rely on third-party FAO providers to cut costs and adopt automation. The U.S. International Trade Commission reported that U.S. exports of services totaled USD 1,237.9 billion in 2025, highlighting the country’s massive engagement with global service trade flows, of which outsourced finance and accounting is a core component.

Key Takeaways

- The Global Finance and Accounting Outsourcing Market was valued at USD 53.9 billion in 2025 and is forecast to reach USD 105.2 billion by 2035.

- The market is set to expand at a CAGR of 6.9% over the forecast period from 2026 to 2035.

- By Service Type, Order-to-Cash (O2C) holds the leading position with a 37.4% share among all service type segments.

- By Deployment Mode, Cloud-Based leads with a 61.2% share and is also the fastest-growing deployment segment.

- By Enterprise Size, Large Enterprises account for the dominant share at 68.3% of total market revenue.

- By Industry Vertical, Banking, Financial Services and Insurance (BFSI) holds the leading position with a 28.3% share.

- North America leads the global FAO market with a 41.3% market share and generates USD 22.3 billion in revenue.

By Service Type

Order-to-Cash dominates with 37.4% due to direct cash flow control.

Companies lean on Order-to-Cash outsourcing because it directly protects the money they collect from customers. The World Bank reports that firms rely on collecting receivables to maintain sufficient working capital, and slow customer payments can drain daily cash flow, so businesses hand this cycle to specialists who reduce debtor days and speed up cash inflows.

Faster collections free up funds that would otherwise sit idle, which is why this service leads. Record-to-Report is now the fastest-growing service because regulators demand tighter, faster financial reporting. As global financial sector assets climbed to 187 percent of GDP in some markets, firms face heavier disclosure duties and need faster monthly closes.

By Deployment Mode

Cloud-Based dominates with 61.2% due to lower upfront hardware spending.

Cloud-Based delivery leads finance outsourcing because it removes the cost and hassle of owning servers. Eurostat found that 52.74 percent of European Union enterprises paid for cloud computing services in 2025, using them for storage, office tools, and business software. This wide base makes it easy for outsourcing partners to run finance work on shared, secure platforms that clients reach from anywhere.

The OECD notes that larger organisations show the highest cloud adoption, yet growth now spreads fast to smaller firms too. Cloud remains the fastest-growing mode as well because updates, security patches, and new features arrive automatically without client effort. Public cloud end-user spending was forecast to reach 832.1 billion US dollars in 2025, showing how quickly demand keeps rising.

By Enterprise Size

Large Enterprises dominate with 68.3% due to high transaction processing volumes.

Large Enterprises lead this market because they run huge numbers of daily transactions that need constant, skilled handling. Their global spread means many currencies, tax rules, and reporting lines, so they sign big multi-year deals with outsourcing partners to manage this scale. Bigger budgets and complex needs make them the natural core buyers of full finance and accounting services.

Small and Medium Enterprises now grow fastest because affordable outsourcing finally fits their budgets. The World Bank states that SMEs make up about 90 percent of all businesses and provide more than 50 percent of employment worldwide, showing a massive untapped buyer pool. As pay-as-you-go pricing lowers entry barriers, more of these firms hire outside teams instead of building costly in-house finance departments.

By Industry Vertical

BFSI dominates with 28.3% due to heavy regulated financial transaction loads.

Banking, Financial Services and Insurance lead demand because these firms process enormous volumes of money movements under strict rules. Financial services account for roughly 20 to 25 percent of the world economy, so the sheer size of this sector creates constant need for accurate reconciliations, compliance checks, and reporting.

IT and Telecom now grow fastest because these firms scale quickly and value lean back offices. One estimate places the core telecoms business-to-business market near 270 billion US dollars in 2026, reflecting a large and active sector. As telecom and software companies expand across borders, they outsource billing, revenue accounting, and financial planning to stay flexible.

Key Market Segments

By Service Type

- Order-to-Cash (O2C)

- Record-to-Report (R2R)

- Financial Planning and Analysis (FP&A)

- Procure-to-Pay (P2P)

By Deployment Mode

- Cloud-Based

- On-Premise

By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

By Industry Vertical

- Banking, Financial Services and Insurance (BFSI)

- IT and Telecom

- Travel and Hospitality

- Retail and E-commerce

- Manufacturing

- Healthcare and Life Sciences

- Energy and Utilities

- Others

Geopolitical Impact Analysis

The global Finance and Accounting Outsourcing market operates within a trade environment that shifted sharply in 2025. UNCTAD reported that global tariffs rose significantly in 2025, driven largely by measures introduced by the United States, with rates calculated to offset bilateral merchandise trade deficits ranging from 11% to 50% across 57 trading partner economies.

While FAO is a services category rather than a goods category, the WTO noted that the volume of services trade was forecast to grow by only 4.0% in 2025, around one percentage point lower than expected, as broader policy uncertainty weighed on cross-border business decisions.

For FAO providers that maintain delivery centers in India, the Philippines, Eastern Europe, and Latin America, heightened geopolitical scrutiny of cross-border data flows and labor arbitrage models adds compliance costs and operational risk to existing contracts. UNCTAD’s January 2026 Global Trade Update confirmed that geopolitical fragmentation is actively reshaping global value chains and investment decisions, with the greatest risks concentrated in developing economies where the bulk of FAO delivery capacity operates.

Beyond tariff pressures, supply chain disruptions and transit delays continue to affect the hardware and software infrastructure that supports cloud-based FAO platforms. The IMF noted that inward direct investment positions declined by 1.4% globally in 2024, signaling that geopolitical risk is already causing companies to reconsider the geography of their service delivery footprints.

Regional Analysis

North America: Market Leader in Finance and Accounting Outsourcing

North America dominates the Finance and Accounting Outsourcing market, holding a 41.3% share and generating USD 22.3 billion in revenue. The United States drives the bulk of this demand. The U.S. Bureau of Economic Analysis confirmed that U.S. private service-supplying industries generate more than 81% of GDP, producing a dense ecosystem of large corporations that need scalable, technology-driven finance functions.

Europe is the second largest region in the FAO market. The Centre for the Promotion of Imports from Developing Countries estimated the European FAO market at EUR 921 million by 2025, with Germany alone accounting for roughly half of that value. Around 51% of European companies outsource financial services, and 61% outsource accounting functions, reflecting deep but measured adoption.

Asia Pacific is the fastest-growing region in the Finance and Accounting Outsourcing market. India and Southeast Asian countries serve as the primary delivery hubs for global FAO services, benefiting from a large English-speaking workforce and strong process management capabilities. India’s total financial sector assets reached 187% of GDP, according to the World Bank’s 2025 Financial Sector Assessment, signaling deep financial infrastructure that supports both domestic demand and offshore delivery capacity.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Challenge

The FAO market is facing a long-term talent pipeline collapse in key regions, with demand far exceeding supply. In the U.S., about 124,200 accounting and auditing job openings are projected annually through 2034, while new CPA exam candidates fell from around 50,000 in 2016 to about 28,000 in 2024, a decline of over 32 percent. Accounting degree completions also fell 3.3 percent in 2023 to 2024 to 40,817 graduates, continuing an eight-year decline.

Hiring has become significantly slower and more constrained. CPA roles take an average of 73 days to fill, 41 percent longer than non CPA roles, and each added credential increases hiring time by 8 to 12 days. There are only 3 qualified candidates available for every 5 CPA-level roles, showing a clear structural mismatch between demand and supply.

For FAO providers, this creates rising costs and staffing pressure. Outsourcing demand is increasing as client teams weaken, but providers compete for the same shrinking talent pool. CPA-level roles cost about 20 percent more to keep vacant, while audit and assurance salaries are rising 3.7 percent year on year versus 2.1 percent overall, tightening margins despite a 12 percent rise in undergraduate accounting enrollment in 2024.

| Challenge | % CAGR Friction | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Structural Accounting Talent Pipeline Collapse | -1.8% | North America core; EU secondary; APAC delivery hubs | Long term (≥ 4 years) |

| Delivery-Hub Wage Inflation & Cost Arbitrage Erosion | -1.2% | APAC primary (India, Philippines); Latin America nearshore corridors | Medium term (2–4 years) |

| Third-Party Cybersecurity & Financial Data Breach Risk | -1.5% | Global; EU GDPR zone; North America (SOX, SEC); APAC cloud corridors | Long term (≥ 4 years) |

| Multi-Jurisdiction Regulatory Compliance Fragmentation | -1.0% | EU regulatory hubs; North America (SOX/SEC); APAC cross-border corridors | Long term (≥ 4 years) |

| Legacy ERP & AI Integration Bottlenecks | -0.9% | North America; EMEA mid-market; APAC SME corridors | Medium term (2–4 years) |

| BPO Workforce Attrition & Institutional Knowledge Erosion | -0.7% | APAC delivery hubs (India, Philippines); Latin America nearshore | Medium term (2–4 years) |

Opportunity

AI and automation in FAO are currently improving efficiency, but the bigger shift is toward a full Finance-as-a-Service model where AI agents execute end-to-end financial workflows, and pricing moves from staffing to outcomes or transactions. Agentic AI systems capable of autonomous reconciliation, anomaly detection, and journal entry generation are still mostly in early-stage enterprise adoption as of 2025, with broader FAO deployment expected within about three years, giving early builders a lead in productized workflow platforms.

This shift also represents a major pricing and margin transition. A platform-based model using AI-driven workflow IP and domain-trained systems allows providers to reprice services as software-like offerings and expand higher-value advisory layers such as FP&A and treasury optimization, with potential revenue uplift of 30 to 45 percent and cost reductions of 40 to 60 percent per transaction.

Overall, AI-native finance platforms in FAO remain a small market at under USD 2 billion in 2026, but the strategic direction is toward outcome-based pricing similar to adjacent SaaS models. Providers that successfully transition could achieve EBITDA expansion of 200 to 350 basis points, with incumbents positioned to leverage existing enterprise distribution to lead early contract redesigns into the Finance-as-a-Service model.

| Opportunity | % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| ESG & Sustainability Financial Reporting as a Standalone FAO Service Line | +2.8–3.5% | EU (CSRD-mandated), North America, APAC (ISSB adopters) | Short term (≤ 2 years) |

| Agentic AI-Powered Autonomous Finance Operations (“Finance-as-a-Service “) | +2.2–3.0% | North America core, EU, APAC tier-1 markets | Medium term (2–4 years) |

| Virtual/Fractional CFO-as-a-Service for the SMB–Mid-Market Segment | +1.8–2.5% | North America, South & Southeast Asia, LATAM | Short to Medium term |

| Digital Asset & Crypto Accounting Compliance as an Adjacent Service Vertical | +1.5–2.2% | North America, EU (MiCA), Singapore/APAC | Medium term (2–4 years) |

| Outcome-Based Pricing Model Monetization (Risk/Gain-Share Contracts) | +1.2–1.8% | North America core, UK, Western Europe | Medium to Long term |

| Healthcare & Life Sciences FAO — Specialised Vertical BPO Expansion | +1.5–2.0% | North America, EU, APAC (India, Philippines delivery) | Medium term (2–4 years) |

Driver

The expansion of ESG and multi-jurisdictional regulation is creating a new outsourced compliance segment within FAO. The EU’s Corporate Sustainability Reporting Directive, revised in 2026, requires large companies with over 1,000 employees and €450 million turnover to disclose Scope 1, 2, and 3 emissions, perform double materiality assessments, and publish climate transition plans, with phased implementation through 2029.

FAO providers are increasingly stepping into this gap by offering ESG integrated reporting capabilities, including carbon accounting, materiality frameworks, and structured ESG data pipelines. This shift is turning ESG compliance into a recurring outsourced workstream, contributing an estimated +1.8 percentage points to baseline CAGR in the short to medium term, with Europe acting as the primary driver and APAC emerging as the fastest-growing adoption region.

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Structural CPA/Accounting Talent Deficit driving outsourcing demand surge and hybrid staffing model adoption | +2.8% | North America core, LATAM nearshore corridors, EU spill-over | Short term (≤ 2 years) |

| AI, GenAI & Agentic Automation operationalization enabling full-cycle workflow transformation and outcome-based pricing | +2.5% | North America, APAC, EU | Medium term (2–4 years) |

| ESG/Regulatory Compliance Expansion (CSRD, IFRS S1/S2, SOX, GDPR) mandating outsourced specialized reporting capacity | +1.8% | EU mandatory, APAC phased, North America discretionary | Short–Medium term |

| Cost Arbitrage Rebalancing via nearshore/offshore delivery realignment and BPO salary inflation in traditional hubs | +1.5% | LATAM nearshore, India/Philippines offshore, CEE | Short term (≤ 2 years) |

| Cloud ERP & SaaS Platform Consolidation enabling scalable tech-embedded FAO delivery | +1.2% | Global; SME APAC and South America adoption accelerating | Medium–Long term |

| GCC Co-Sourcing & Outcome-Based Contract Models replacing FTE-based delivery frameworks | +1.0% | North America, EU enterprise; India/LATAM GCC corridors | Medium–Long term (2–5 years) |

Restraint

A key restraint on FAO adoption in North America and Europe is CFO and finance leadership reluctance to fully surrender control of core finance operations, reinforced by growing regulatory attention on third-party concentration risk. Surveys indicate that loss of operational control, organizational resistance to change, and data security concerns remain primary barriers to adoption, even where efficiency gains are clear.

At the same time, regulators are increasingly formalizing concentration risk in outsourcing. In Canada, supervisory frameworks now explicitly flag dependence on a limited number of external vendors as both an institution-specific and systemic risk. Industry governance norms also treat situations where a single provider handles roughly 30 to 40 percent of critical functions or 25 to 30 percent of third-party spend as escalation triggers, particularly in regulated sectors like BFSI and healthcare finance.

Additional constraints come from internal capability gaps and cost pressures, with a majority of CFOs reporting lack of internal expertise for implementation and a significant share citing budget limits. Exit strategy requirements, which mandate tested alternatives for critical outsourced functions, further increase operational overhead and reduce net ROI. Together, these factors slow adoption velocity in mid-market segments and create an estimated -1.0 percentage point drag on FAO market CAGR expansion.

| Restraint | % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-Jurisdictional Data Privacy & Regulatory Fragmentation (GDPR, DPDP, CCPA) | -2.2% | EU core, India, North America | Medium term (2–4 years) |

| Cybersecurity Breach Risk & Client Data Liability | -1.8% | North America core, EU, APAC corridors | Short term (≤ 2 years) |

| Structural Talent Attrition in Offshore Delivery Hubs | -1.5% | India primary, Philippines, Eastern Europe | Short–Medium term |

| AI-Driven In-House Automation Displacing Outsourcing Demand | -1.3% | North America, EU, developed APAC | Medium–Long term (2–5 years) |

| Client Control-Loss Resistance & Vendor Concentration Risk | -1.0% | North America core, EU mid-market | Medium term (2–4 years) |

| Transition Cost Opacity & Implementation Failure Risk | -0.8% | Global (SME corridors most exposed) | Short term (≤ 2 years) |

Key Players Analysis

The Finance and Accounting Outsourcing market features Tier 1 market leaders with global delivery scale, large revenue bases, and active investment in AI-powered platforms. Accenture leads with outsourcing revenues of USD 34.57 billion in fiscal year 2025, making it the largest single outsourcing provider globally across all service lines, including FAO.

Accenture generated total revenues of USD 64.9 billion in fiscal 2024 and earned the top position in Everest Group’s Finance and Accounting Outsourcing PEAK Matrix Assessment 2025. Genpact, the most focused pure-play FAO provider among the Tier 1 group, reported full-year 2025 net revenues of USD 5.08 billion, up 6.56% year-over-year. Genpact’s Data-Tech-AI segment generated USD 2.23 billion in fiscal 2024, growing 6.9%, showing the firm’s active shift toward analytics-driven finance services.

Genpact and Google Cloud expanded their alliance to launch agentic AI solutions for the Office of the CFO under the Finance One Revenue Lens platform, available through Google Cloud’s Agent Marketplace. Tata Consultancy Services crossed the USD 30 billion annual revenue milestone in fiscal 2025, while Infosys BPM reported revenues of INR 8,501 crore in fiscal 2025, up 7.7% year-over-year, with five live implementations of agentic AI in accounts payable underway since May 2025.

Top Key Players in the Market

- WNS (Holdings) Limited

- Wipro Limited

- Tata Consultancy Services Limited

- SAP SE

- PricewaterhouseCoopers International Limited

- Oracle Corporation

- KPMG International Limited

- International Business Machines Corporation

- Infosys Limited

- HCL Technologies Limited

- Genpact Limited

- Ernst and Young Global Limited

- Deloitte Touche Tohmatsu Limited

- Cognizant Technology Solutions Corporation

- Capgemini SE

- Accenture Plc

Recent Developments

- In May 2026, Genpact and Google Cloud expanded their strategic alliance to launch the Finance One Revenue Lens Agents, a suite of agentic AI solutions built on Google Cloud for enterprise CFO offices, made available through Google Cloud’s Agent Marketplace.

- In July 2025, Capgemini SE announced a definitive agreement to acquire WNS (Holdings) Limited at USD 76.50 per share, representing a total cash consideration of USD 3.3 billion, to build a global leader in Agentic AI-powered Intelligent Operations in the FAO space.

- In May 2025, Infosys BPM launched AI Agents for invoice processing within its Infosys Accounts Payable on Cloud solution, powered by Infosys Topaz, targeting autonomous accounts payable operations with five live enterprise implementations underway by November 2025.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 53.9 Billion |

| Forecast Revenue (2035) | USD 105.2 Billion |

| CAGR (2026-2035) | 6.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Service Type (Order-to-Cash (O2C), Record-to-Report (R2R), Financial Planning and Analysis (FPandA), Procure-to-Pay (P2P)); By Deployment Mode (Cloud-Based, On-Premise); By Enterprise Size (Large Enterprises, Small and Medium Enterprises (SMEs)); By Industry Vertical (Banking, Financial Services and Insurance (BFSI), IT and Telecom, Travel and Hospitality, Retail and E-commerce, Manufacturing, Healthcare and Life Sciences, Energy and Utilities, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | WNS (Holdings) Limited, Wipro Limited, Tata Consultancy Services Limited, SAP SE, PricewaterhouseCoopers International Limited, Oracle Corporation, KPMG International Limited, International Business Machines Corporation, Infosys Limited, HCL Technologies Limited, Genpact Limited, Ernst and Young Global Limited, Deloitte Touche Tohmatsu Limited, Cognizant Technology Solutions Corporation, Capgemini SE, Accenture Plc |

| Customization Scope | Customization for segments and region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |